ACC200: Activity Based Costing to Improve Profitability Sewing Easy

VerifiedAdded on 2023/06/12

|7

|774

|72

Report

AI Summary

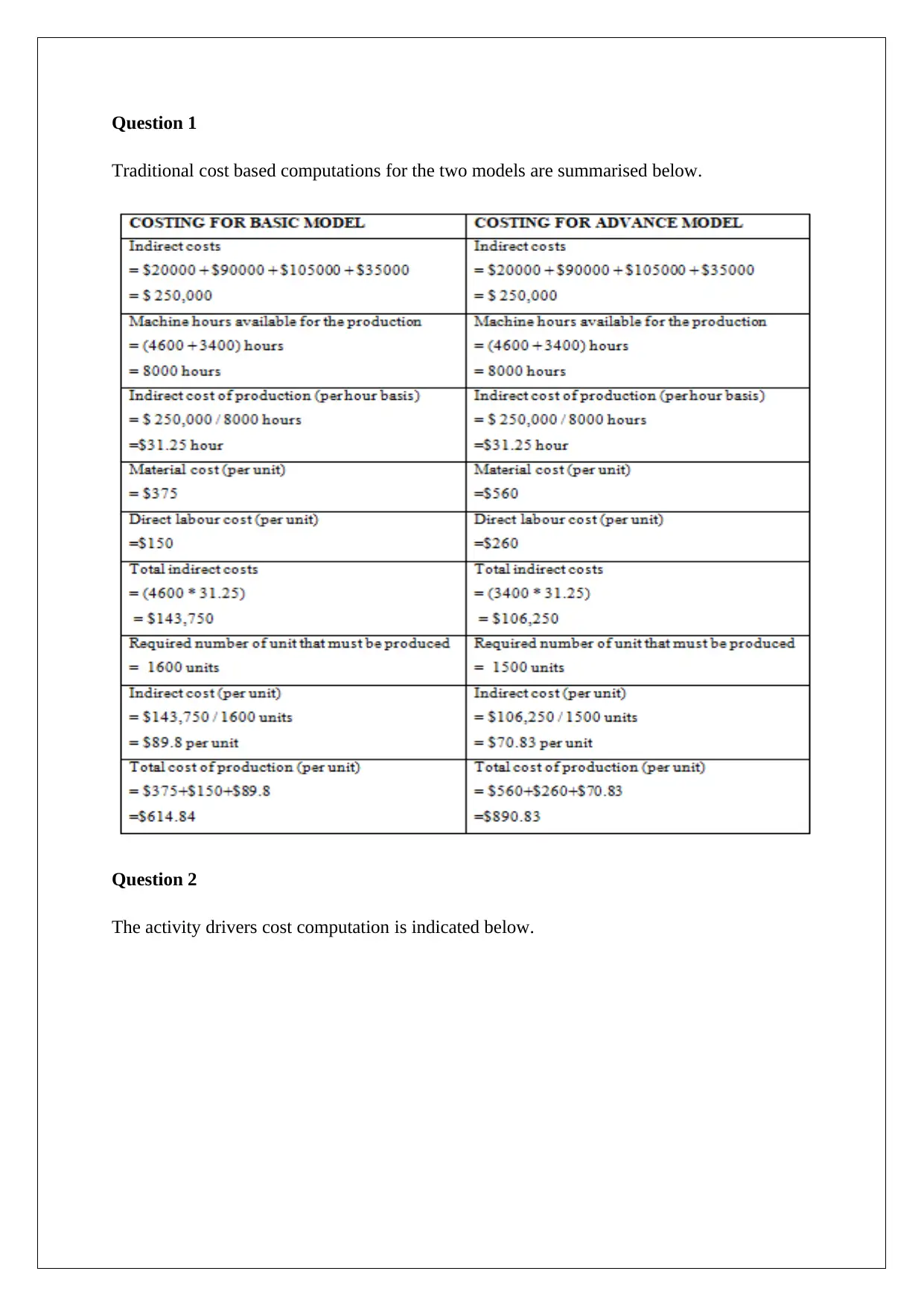

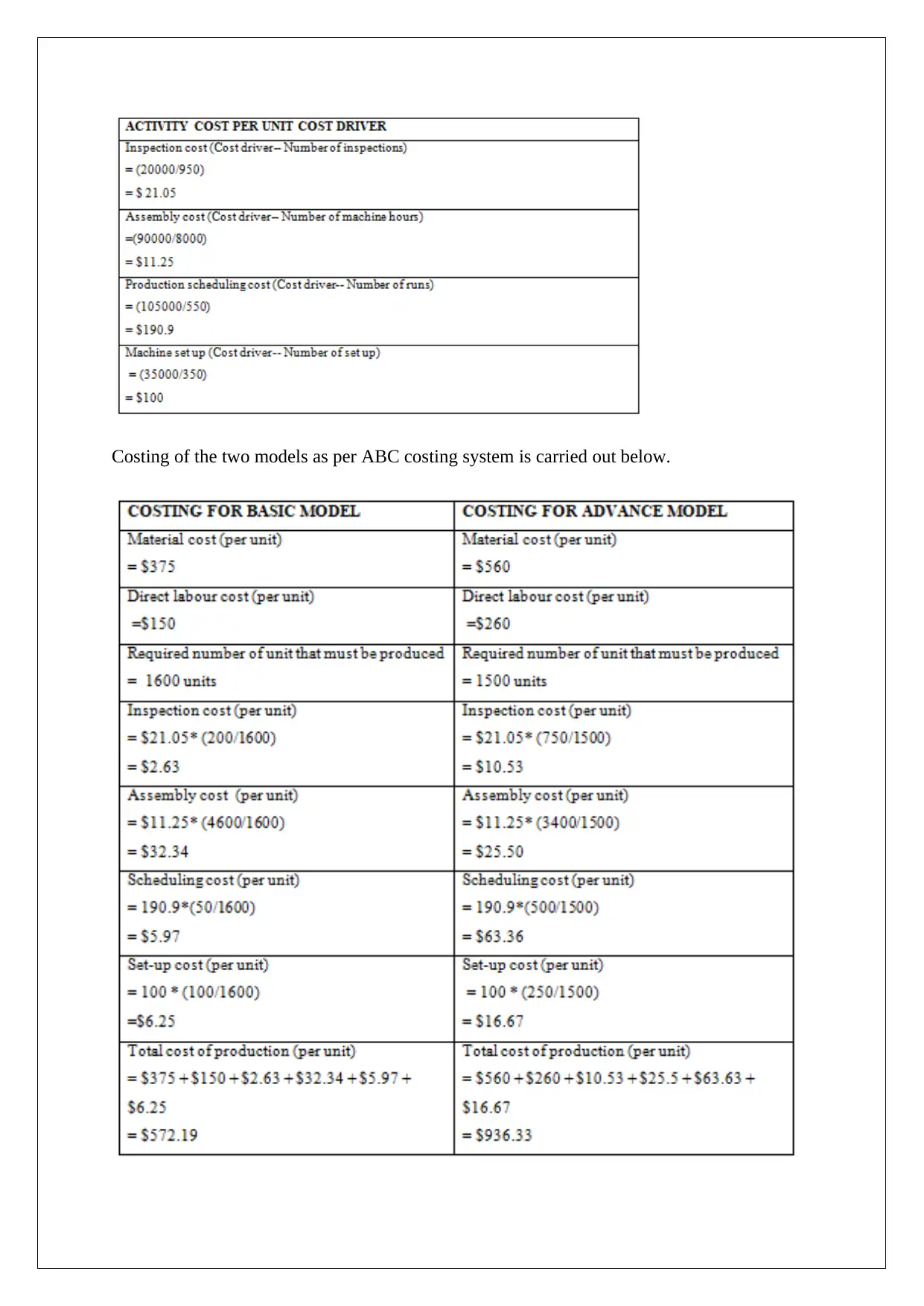

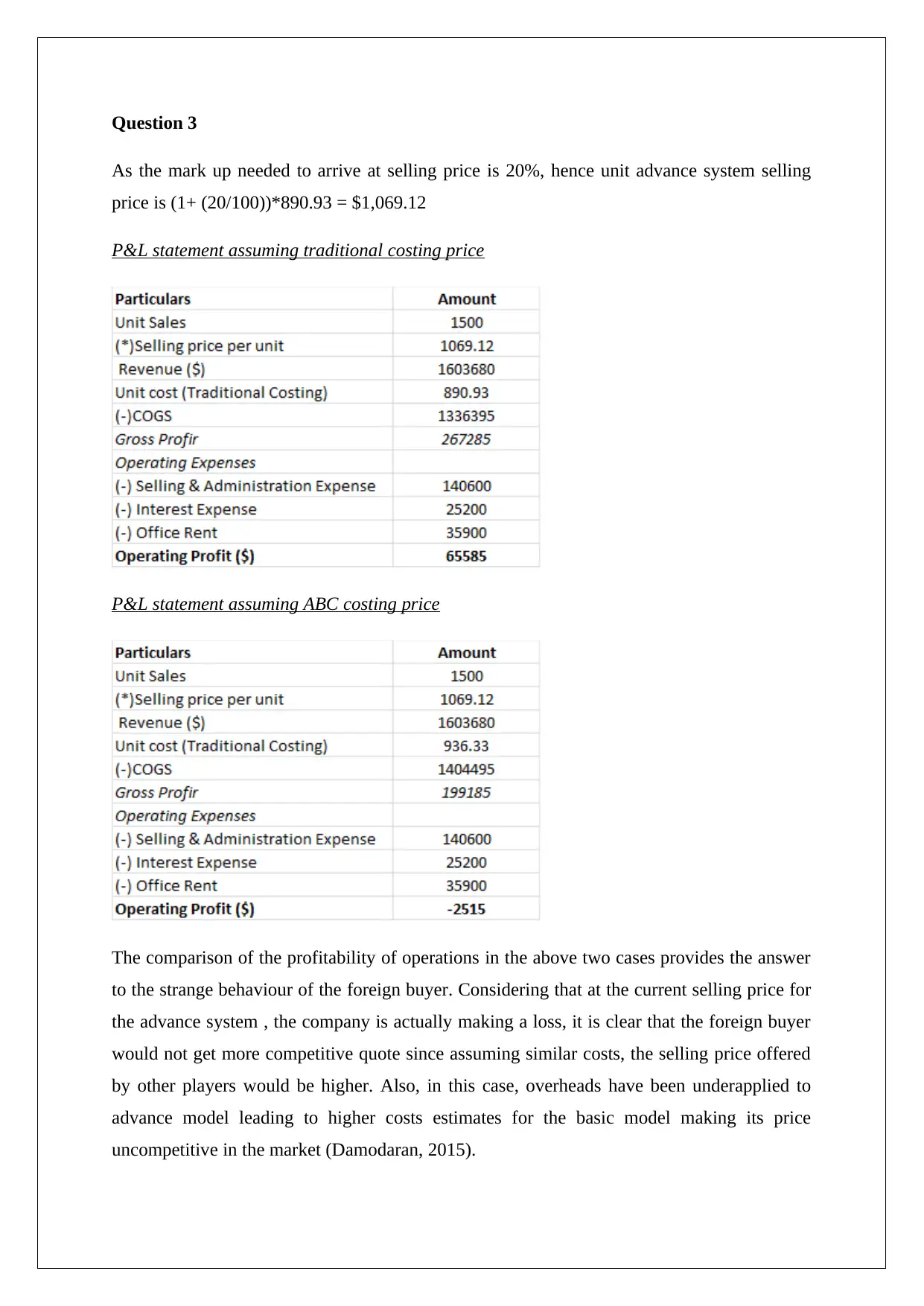

This report analyzes Sewing Easy Ltd's costing methods, comparing traditional costing with activity-based costing (ABC) to understand discrepancies in profitability between their basic and advanced sewing machine models. The analysis reveals that the traditional costing system inaccurately allocates overhead costs, leading to an underestimation of the advanced model's costs and an overestimation of the basic model's costs. The report advocates for a transition to ABC to improve pricing decisions, enhance management decision-making, and ensure long-term competitiveness. It also addresses the limitations of ABC, such as its complexity and implementation challenges, and suggests measures to align product pricing with accurate costing and competitor prices. The report concludes that adopting ABC provides a strategic advantage by enabling better resource allocation and informed decision-making, ultimately impacting the firm's profitability and market position. Desklib provides access to similar reports and study tools for students.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.