Financial Accounting: Costing Methods, Journal Entries, and Analysis

VerifiedAdded on 2023/06/15

|8

|878

|149

Homework Assignment

AI Summary

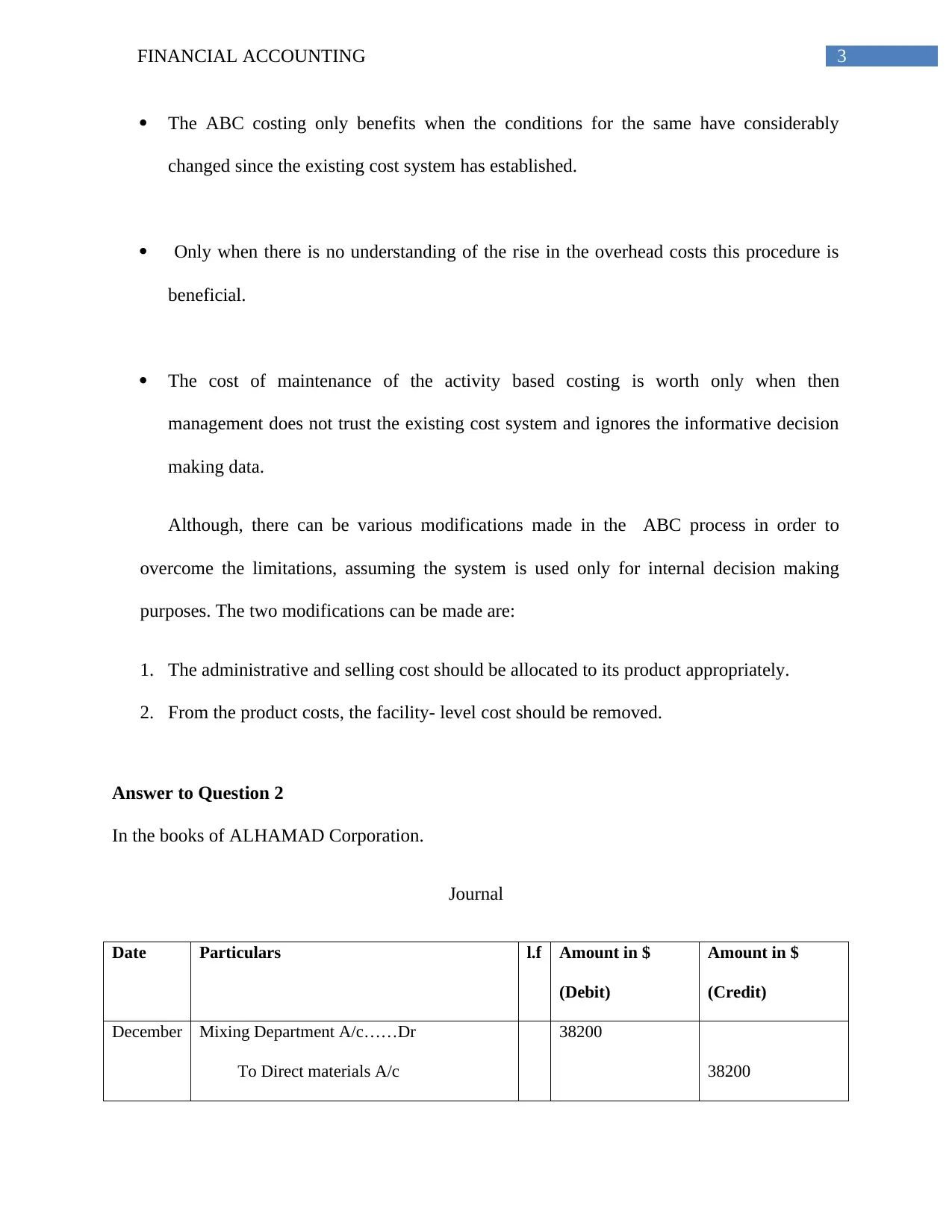

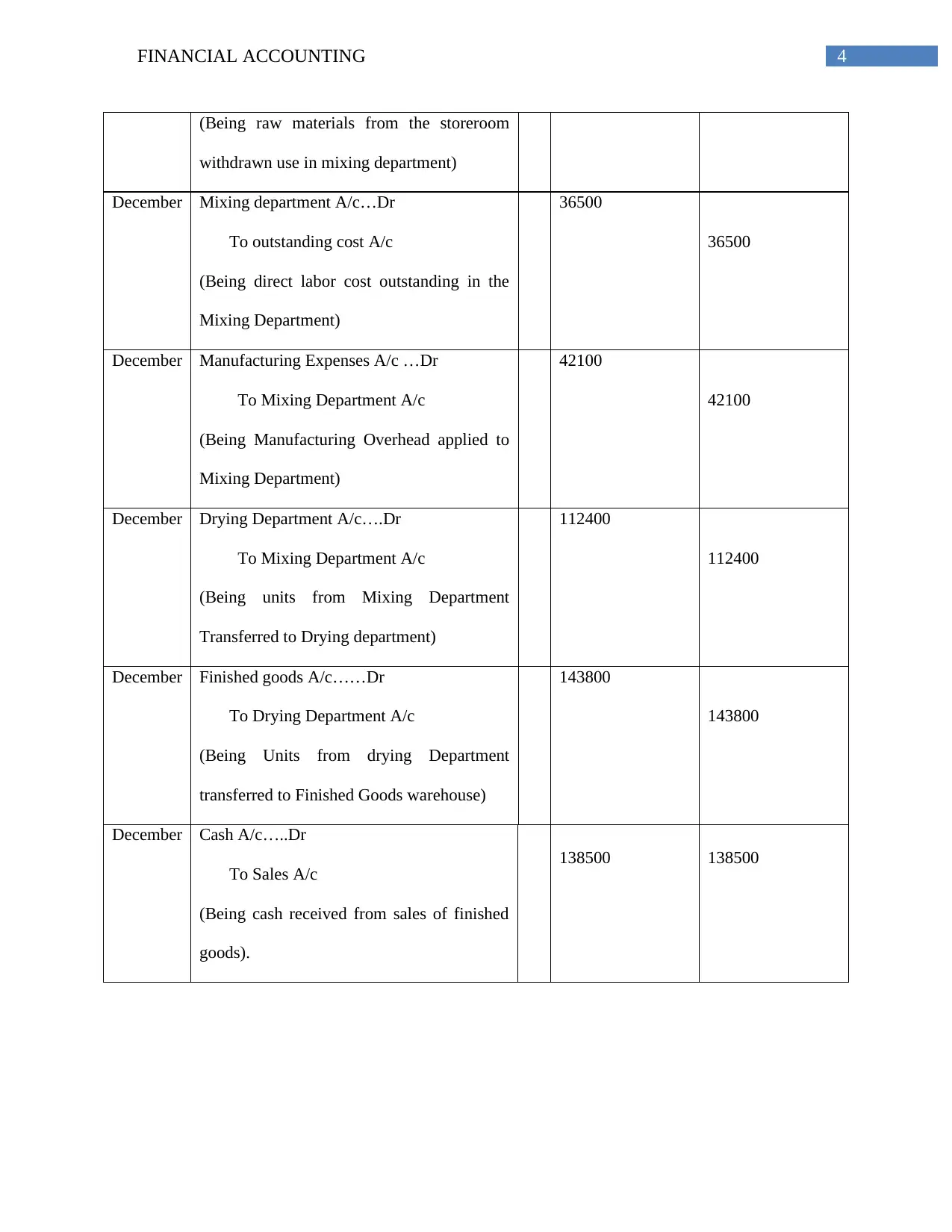

This assignment solution delves into key financial accounting concepts. It begins by explaining activity-based costing (ABC), highlighting its advantages such as improved accuracy and better understanding of activities, as well as its limitations like high implementation costs. Modifications to ABC for internal decision-making are also discussed. The solution then provides journal entries for ALHAMAD Corporation, covering transactions in the mixing and drying departments. It further addresses the concept of plant-wide overhead allocation and concludes with a breakeven analysis, calculating the breakeven point in units and determining the selling price needed to achieve a specific breakeven point. Desklib offers a wealth of similar solved assignments and study resources for students.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.