Activity Based Costing: Emerging Model, Implementation, and Comparison

VerifiedAdded on 2023/06/04

|14

|2530

|389

Report

AI Summary

This report provides a comprehensive overview of Activity Based Costing (ABC) as an emerging cost model. It details the application of ABC in manufacturing firms, outlining the steps for implementation, including activity identification, assigning overhead costs, identifying cost drivers, and allocating overhead costs to products. The report further discusses the advantages of ABC, such as accurate product costing, cost behavior information, and improved decision-making, as well as its disadvantages, including its complexity and cost. A comparison between ABC and traditional costing methods is presented, highlighting the differences in focus, application, and usage. The report concludes that while ABC enhances cost processes, its complexity may deter some managers, while traditional costing offers a simpler but less accurate alternative.

Activity Based

Costing

An Emerging Cost

Model

Costing

An Emerging Cost

Model

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Introduction

ABC, also known as Activity Based Costing, is a method which helps the firms to ascertain

the cost related to the production of products and monitoring of production activities. The

method identifies the consumption of resources and ascertain final results. Resources are

being allotted to various production activities and then these activities are assigned to

different cost objects. The method helps the management in making good understanding of

the products and services it offers, its customers and the profit it makes by selling products

to the target customer group. The method is being used by the firms to identify the indirect

expenses incurred on various products of the firm, to consider the direct and indirect costs

on the products, to set the of prices more precisely and to know which indirect cost could be

reduced or cut back. This report includes application of ABC in manufacturing firms, steps

for implementation of activity based costing, merits and demerits of activity based costing.

Introduction

ABC, also known as Activity Based Costing, is a method which helps the firms to ascertain

the cost related to the production of products and monitoring of production activities. The

method identifies the consumption of resources and ascertain final results. Resources are

being allotted to various production activities and then these activities are assigned to

different cost objects. The method helps the management in making good understanding of

the products and services it offers, its customers and the profit it makes by selling products

to the target customer group. The method is being used by the firms to identify the indirect

expenses incurred on various products of the firm, to consider the direct and indirect costs

on the products, to set the of prices more precisely and to know which indirect cost could be

reduced or cut back. This report includes application of ABC in manufacturing firms, steps

for implementation of activity based costing, merits and demerits of activity based costing.

3

Implementatio

n

www.website.com

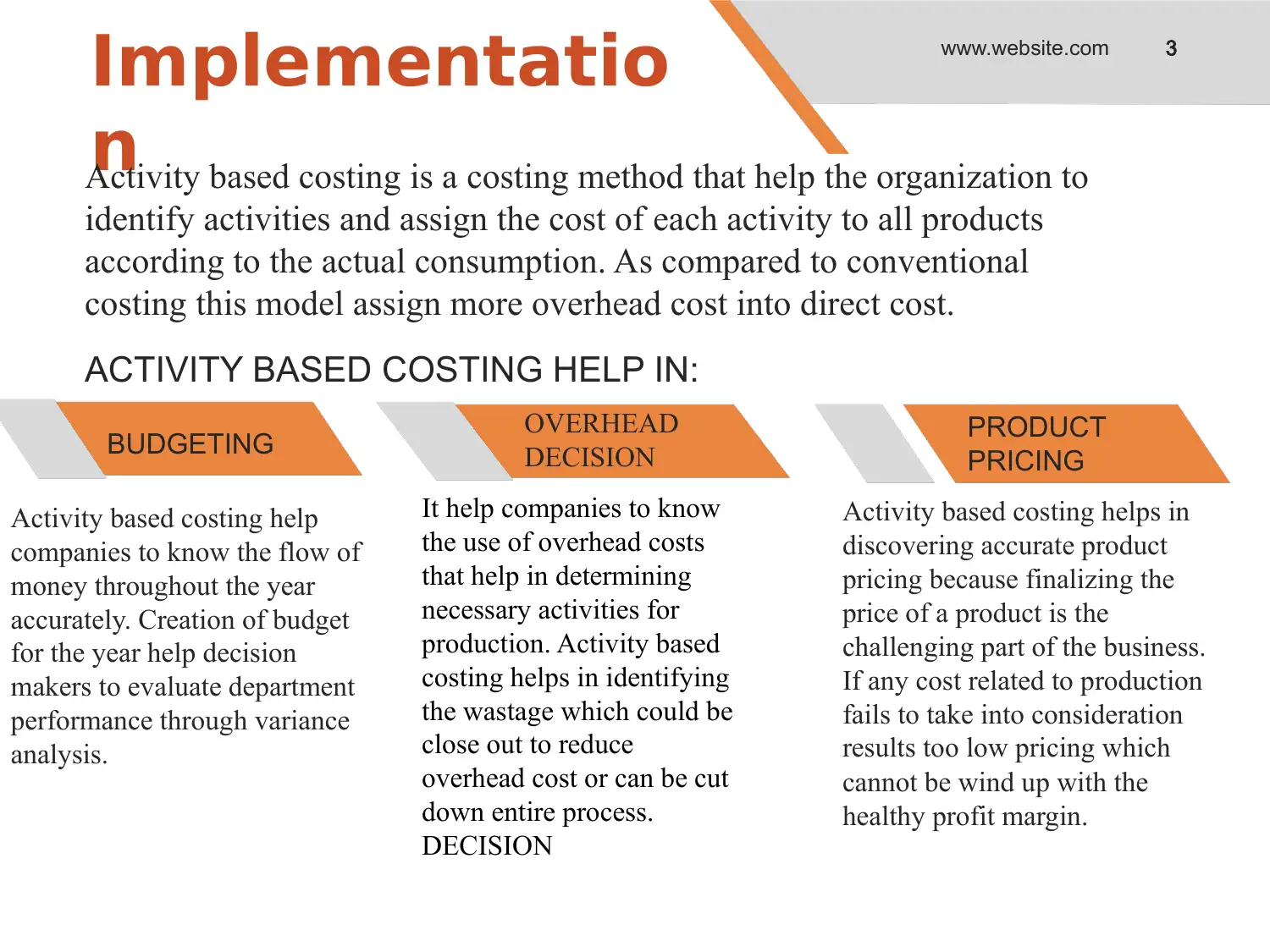

Activity based costing is a costing method that help the organization to

identify activities and assign the cost of each activity to all products

according to the actual consumption. As compared to conventional

costing this model assign more overhead cost into direct cost.

ACTIVITY BASED COSTING HELP IN:

BUDGETING

Activity based costing help

companies to know the flow of

money throughout the year

accurately. Creation of budget

for the year help decision

makers to evaluate department

performance through variance

analysis.

PRODUCT

PRICING

Activity based costing helps in

discovering accurate product

pricing because finalizing the

price of a product is the

challenging part of the business.

If any cost related to production

fails to take into consideration

results too low pricing which

cannot be wind up with the

healthy profit margin.

It help companies to know

the use of overhead costs

that help in determining

necessary activities for

production. Activity based

costing helps in identifying

the wastage which could be

close out to reduce

overhead cost or can be cut

down entire process.

DECISION

OVERHEAD

DECISION

Implementatio

n

www.website.com

Activity based costing is a costing method that help the organization to

identify activities and assign the cost of each activity to all products

according to the actual consumption. As compared to conventional

costing this model assign more overhead cost into direct cost.

ACTIVITY BASED COSTING HELP IN:

BUDGETING

Activity based costing help

companies to know the flow of

money throughout the year

accurately. Creation of budget

for the year help decision

makers to evaluate department

performance through variance

analysis.

PRODUCT

PRICING

Activity based costing helps in

discovering accurate product

pricing because finalizing the

price of a product is the

challenging part of the business.

If any cost related to production

fails to take into consideration

results too low pricing which

cannot be wind up with the

healthy profit margin.

It help companies to know

the use of overhead costs

that help in determining

necessary activities for

production. Activity based

costing helps in identifying

the wastage which could be

close out to reduce

overhead cost or can be cut

down entire process.

DECISION

OVERHEAD

DECISION

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

ABC Calculation:

www.website.com

Identify all the activities related to production of product.

Divide the total overhead of each cost pool by total cost drivers that gives cost driver

rate

Multiply cost driver rate by number of cost drivers.

Divide the activities into cost pools.

Calculate total overhead of each cost pool.

Assign cost drivers (hours, units) of each cost pool.

Calculate cost driver rate by dividing total overhead.

ABC Calculation:

www.website.com

Identify all the activities related to production of product.

Divide the total overhead of each cost pool by total cost drivers that gives cost driver

rate

Multiply cost driver rate by number of cost drivers.

Divide the activities into cost pools.

Calculate total overhead of each cost pool.

Assign cost drivers (hours, units) of each cost pool.

Calculate cost driver rate by dividing total overhead.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

IMPLEMENETIN

G STEPS

www.website.com

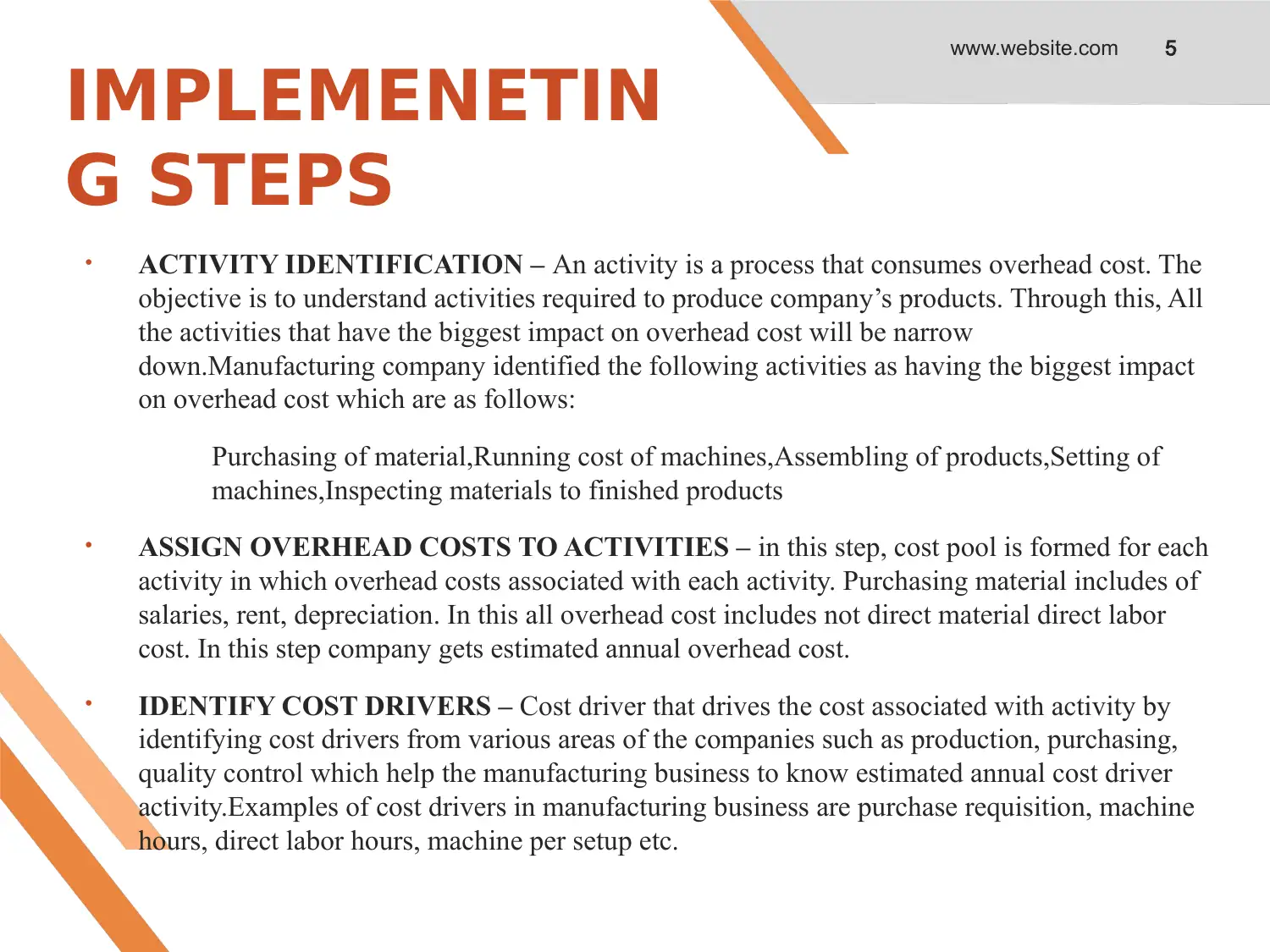

• ACTIVITY IDENTIFICATION – An activity is a process that consumes overhead cost. The

objective is to understand activities required to produce company’s products. Through this, All

the activities that have the biggest impact on overhead cost will be narrow

down.Manufacturing company identified the following activities as having the biggest impact

on overhead cost which are as follows:

Purchasing of material,Running cost of machines,Assembling of products,Setting of

machines,Inspecting materials to finished products

• ASSIGN OVERHEAD COSTS TO ACTIVITIES – in this step, cost pool is formed for each

activity in which overhead costs associated with each activity. Purchasing material includes of

salaries, rent, depreciation. In this all overhead cost includes not direct material direct labor

cost. In this step company gets estimated annual overhead cost.

• IDENTIFY COST DRIVERS – Cost driver that drives the cost associated with activity by

identifying cost drivers from various areas of the companies such as production, purchasing,

quality control which help the manufacturing business to know estimated annual cost driver

activity.Examples of cost drivers in manufacturing business are purchase requisition, machine

hours, direct labor hours, machine per setup etc.

IMPLEMENETIN

G STEPS

www.website.com

• ACTIVITY IDENTIFICATION – An activity is a process that consumes overhead cost. The

objective is to understand activities required to produce company’s products. Through this, All

the activities that have the biggest impact on overhead cost will be narrow

down.Manufacturing company identified the following activities as having the biggest impact

on overhead cost which are as follows:

Purchasing of material,Running cost of machines,Assembling of products,Setting of

machines,Inspecting materials to finished products

• ASSIGN OVERHEAD COSTS TO ACTIVITIES – in this step, cost pool is formed for each

activity in which overhead costs associated with each activity. Purchasing material includes of

salaries, rent, depreciation. In this all overhead cost includes not direct material direct labor

cost. In this step company gets estimated annual overhead cost.

• IDENTIFY COST DRIVERS – Cost driver that drives the cost associated with activity by

identifying cost drivers from various areas of the companies such as production, purchasing,

quality control which help the manufacturing business to know estimated annual cost driver

activity.Examples of cost drivers in manufacturing business are purchase requisition, machine

hours, direct labor hours, machine per setup etc.

6

IMPLEMENETIN

G STEPS

www.website.com

• PRE DETERMINED OVERHEAD RATE FOR EACH ACTIVITY – pre determined

overhead cost will be calculated by dividing estimated overhead cost and estimated cost driver

activity that shows overhead cost for each purchase requisition processes.

• ALLOCATE OVERHEAD COSTS TO PRODUCTS – Once activity pools and rates

known, the next step is to assign them cost. Overhead costs are assigned to products by

multiplying predetermined overhead rate by cost driver activity.

• PREPARE AND DISTRIBUTE MANAGEMENT REPORTS – After completing ABC

costing, the data should be send to cost object owners in a concise manner.

IMPLEMENETIN

G STEPS

www.website.com

• PRE DETERMINED OVERHEAD RATE FOR EACH ACTIVITY – pre determined

overhead cost will be calculated by dividing estimated overhead cost and estimated cost driver

activity that shows overhead cost for each purchase requisition processes.

• ALLOCATE OVERHEAD COSTS TO PRODUCTS – Once activity pools and rates

known, the next step is to assign them cost. Overhead costs are assigned to products by

multiplying predetermined overhead rate by cost driver activity.

• PREPARE AND DISTRIBUTE MANAGEMENT REPORTS – After completing ABC

costing, the data should be send to cost object owners in a concise manner.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7ADVANTAGES OF

ACTIVITY BASED

COSTING

www.website.com

ACCURATE PRODUCT COSTING – it produces reliable product cost by focusing on cause and

effect relationship of cost incurrence. It helps the manufacturing business to know the activities

which cause costs which consume activities. In a large organization overhead cost constitute a large

share of total cost which is important to know accurate costing of product.

COST BEHAVIOUR INFORMATION – help in cost behavior reduces cost and the activities that

do not add value in a product. Helps in decision making for manager to control fixed overhead cost

as it is visible to manager through variance analysis.

TRACING ACTIVITIES – with the help of knowing cost drivers, ABC help decision makers to

trace more overheads to the products and resulting in efficiency of operations.

OVERHEAD COST – ABC help many departments in an organization like production etc. will

know their overhead cost related to production of product through which it is easy to reduce cost per

unit and effective utilization of resources.

BETTER DECISION MAKING – Activity based costing helps in fixing selling prices of products

as the manager has reliable product cost data.

COST MANAGEMENT – Cost drivers is help to design new products or existing products as they

have overhead cost that can be applied in costing. Activity based costing useful for cost management

and performance appraisals.

ACTIVITY BASED

COSTING

www.website.com

ACCURATE PRODUCT COSTING – it produces reliable product cost by focusing on cause and

effect relationship of cost incurrence. It helps the manufacturing business to know the activities

which cause costs which consume activities. In a large organization overhead cost constitute a large

share of total cost which is important to know accurate costing of product.

COST BEHAVIOUR INFORMATION – help in cost behavior reduces cost and the activities that

do not add value in a product. Helps in decision making for manager to control fixed overhead cost

as it is visible to manager through variance analysis.

TRACING ACTIVITIES – with the help of knowing cost drivers, ABC help decision makers to

trace more overheads to the products and resulting in efficiency of operations.

OVERHEAD COST – ABC help many departments in an organization like production etc. will

know their overhead cost related to production of product through which it is easy to reduce cost per

unit and effective utilization of resources.

BETTER DECISION MAKING – Activity based costing helps in fixing selling prices of products

as the manager has reliable product cost data.

COST MANAGEMENT – Cost drivers is help to design new products or existing products as they

have overhead cost that can be applied in costing. Activity based costing useful for cost management

and performance appraisals.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

DISADVANTAGE

S OF ACTIVITY

BASED

COSTING

www.website.com

EXPENSIVE AND COMPLEX METHOD – As there are numbers of cost pools and drivers which

makes it complex and costly therefore it is not recommended to use activity based costing in all firms

for all product lines.

SELECTION OF DRIVERS – As there are numerous cost drivers, common cost, varying cost

driver rates which makes difficult for the organization to select each drivers. It could be possible that

cost driver will not relate to product but it looks in a management view.

SMALLER FIRMS – All firms are not using activity based costing due to its cost of maintaining

therefore Activity based costing is not useful for small firms, it could be possible that it will be

beneficial for small firms if the costing of products will be beneficial, if it is costly resulting in high

selling prices and lowers the profitability.

LACK OF COMMUNICATION – As companies uses Activity based costing method affect

behavioral change management result in lack of communication and failed ti implement the ABC

method.

RESISTANCE – operational managers that would need to spend substantial time and efforts through

which employees pose resistance towards this method.

DISADVANTAGE

S OF ACTIVITY

BASED

COSTING

www.website.com

EXPENSIVE AND COMPLEX METHOD – As there are numbers of cost pools and drivers which

makes it complex and costly therefore it is not recommended to use activity based costing in all firms

for all product lines.

SELECTION OF DRIVERS – As there are numerous cost drivers, common cost, varying cost

driver rates which makes difficult for the organization to select each drivers. It could be possible that

cost driver will not relate to product but it looks in a management view.

SMALLER FIRMS – All firms are not using activity based costing due to its cost of maintaining

therefore Activity based costing is not useful for small firms, it could be possible that it will be

beneficial for small firms if the costing of products will be beneficial, if it is costly resulting in high

selling prices and lowers the profitability.

LACK OF COMMUNICATION – As companies uses Activity based costing method affect

behavioral change management result in lack of communication and failed ti implement the ABC

method.

RESISTANCE – operational managers that would need to spend substantial time and efforts through

which employees pose resistance towards this method.

9

Advantages of ABC over

traditional costing techniques:

ABC or Activity Based Costing and Traditional Costing are the methods which are being used in

allocation of overheads to the products that firm produces. Both of these methods estimates the

total amount of indirect cost on the overall production and assignment of these indirect costs to

individual product based on the rate of cost driver. The major difference in both the methods is

the accuracy of the results and complexity of the method. Traditional costing assign the overheads

to the products on the basis of average rate of arbitrary is considered to be more simple method

than ABC method. But the results from the traditional costing method are less accurate compared

to the ABC. ABC is more typical to understand and apply as it is a long method to assign the costs

to products. It firstly assign overheads to the activities that are being conducted to produce the

product and then it assigns overheads to the individual product on the basis of usage of the

products.

www.website.com

Advantages of ABC over

traditional costing techniques:

ABC or Activity Based Costing and Traditional Costing are the methods which are being used in

allocation of overheads to the products that firm produces. Both of these methods estimates the

total amount of indirect cost on the overall production and assignment of these indirect costs to

individual product based on the rate of cost driver. The major difference in both the methods is

the accuracy of the results and complexity of the method. Traditional costing assign the overheads

to the products on the basis of average rate of arbitrary is considered to be more simple method

than ABC method. But the results from the traditional costing method are less accurate compared

to the ABC. ABC is more typical to understand and apply as it is a long method to assign the costs

to products. It firstly assign overheads to the activities that are being conducted to produce the

product and then it assigns overheads to the individual product on the basis of usage of the

products.

www.website.com

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Traditional

Costing:

www.website.com

Traditional Costing is a method in which overheads are assigned to products on the basis of pre-

established indirect cost rate. This methods is considered to be the best when direct costs are more

than indirect costs. There are some steps to apply traditional costing method:

1. Firstly, indirect cost is needed to be identified.

2. Estimation of indirect cost is done for a specific period of time, i.e., for a year, quarter or month.

3. Cost driver needs to be selected which would have a link with the cost.

4. Estimation of a value for cost driver is done for a specific period.

5. Computation of pre-established indirect cost rate would be done.

6. Finally, indirect costs are assigned to the products with the help of indirect cost rate.

Traditional

Costing:

www.website.com

Traditional Costing is a method in which overheads are assigned to products on the basis of pre-

established indirect cost rate. This methods is considered to be the best when direct costs are more

than indirect costs. There are some steps to apply traditional costing method:

1. Firstly, indirect cost is needed to be identified.

2. Estimation of indirect cost is done for a specific period of time, i.e., for a year, quarter or month.

3. Cost driver needs to be selected which would have a link with the cost.

4. Estimation of a value for cost driver is done for a specific period.

5. Computation of pre-established indirect cost rate would be done.

6. Finally, indirect costs are assigned to the products with the help of indirect cost rate.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

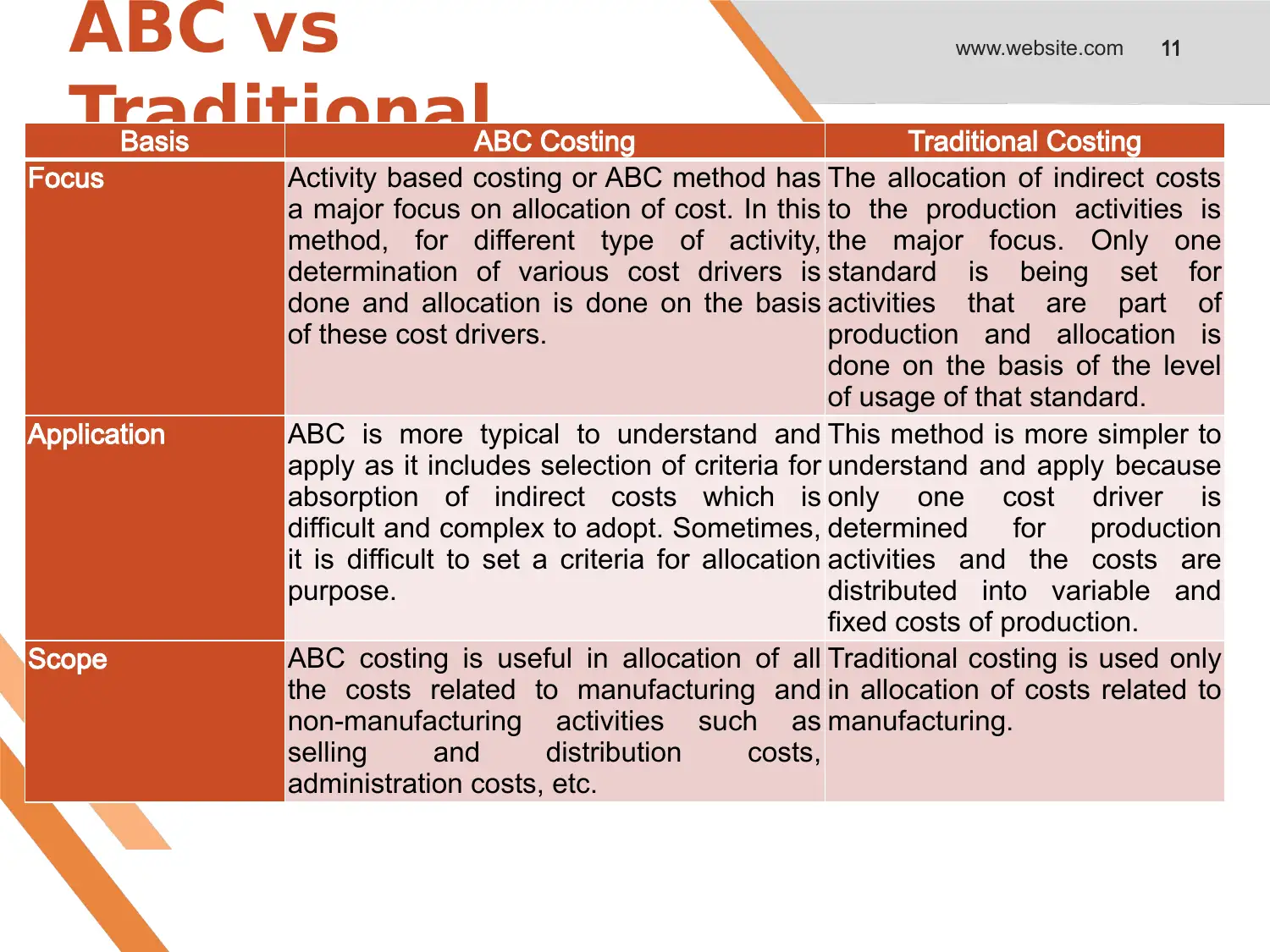

11ABC vs

TraditionalBasis ABC Costing Traditional Costing

Focus Activity based costing or ABC method has

a major focus on allocation of cost. In this

method, for different type of activity,

determination of various cost drivers is

done and allocation is done on the basis

of these cost drivers.

The allocation of indirect costs

to the production activities is

the major focus. Only one

standard is being set for

activities that are part of

production and allocation is

done on the basis of the level

of usage of that standard.

Application ABC is more typical to understand and

apply as it includes selection of criteria for

absorption of indirect costs which is

difficult and complex to adopt. Sometimes,

it is difficult to set a criteria for allocation

purpose.

This method is more simpler to

understand and apply because

only one cost driver is

determined for production

activities and the costs are

distributed into variable and

fixed costs of production.

Scope ABC costing is useful in allocation of all

the costs related to manufacturing and

non-manufacturing activities such as

selling and distribution costs,

administration costs, etc.

Traditional costing is used only

in allocation of costs related to

manufacturing.

www.website.com

TraditionalBasis ABC Costing Traditional Costing

Focus Activity based costing or ABC method has

a major focus on allocation of cost. In this

method, for different type of activity,

determination of various cost drivers is

done and allocation is done on the basis

of these cost drivers.

The allocation of indirect costs

to the production activities is

the major focus. Only one

standard is being set for

activities that are part of

production and allocation is

done on the basis of the level

of usage of that standard.

Application ABC is more typical to understand and

apply as it includes selection of criteria for

absorption of indirect costs which is

difficult and complex to adopt. Sometimes,

it is difficult to set a criteria for allocation

purpose.

This method is more simpler to

understand and apply because

only one cost driver is

determined for production

activities and the costs are

distributed into variable and

fixed costs of production.

Scope ABC costing is useful in allocation of all

the costs related to manufacturing and

non-manufacturing activities such as

selling and distribution costs,

administration costs, etc.

Traditional costing is used only

in allocation of costs related to

manufacturing.

www.website.com

12ABC vs

TraditionalBasis ABC Costing Traditional Costing

Usage of method by

the Management

ABC could only be utilize for management

motive because it can not be used by more

than one user as they would not find it suitable

metric for their operations. It helps the

management in pooling of cost and allocation

of costs more properly.

The values determined by using

traditional costing method could

become a part of profit and loss

statement as a cost value as it only

determine the value of cost of

product.

Influence on

Operations

The firm requires to make deep investigation

of its activities related to production and cost

incurred by the firm for the same. ABC helps

the management in improving their processes

in long run. This method eventually helps

businesses to manage their production costs.

Using Traditional Costing method

makes things difficult for the

management in gathering the data

related to production as they do

not provide various cost centres to

the firm.

www.website.com

Activity Based Costing (ABC) helps in improving the processes of business and indirect cost would be

allocated to each and every product that firm produces. In this method businesses would be able to

exclude the cost, such as factory costs, that are not related to the products that firm produces. When the

costs are allocated to each and every product or activity, it helps the firm to improve its processes. This

method also helps in determining the products that are useless for the business and then firm can stop

their production.

TraditionalBasis ABC Costing Traditional Costing

Usage of method by

the Management

ABC could only be utilize for management

motive because it can not be used by more

than one user as they would not find it suitable

metric for their operations. It helps the

management in pooling of cost and allocation

of costs more properly.

The values determined by using

traditional costing method could

become a part of profit and loss

statement as a cost value as it only

determine the value of cost of

product.

Influence on

Operations

The firm requires to make deep investigation

of its activities related to production and cost

incurred by the firm for the same. ABC helps

the management in improving their processes

in long run. This method eventually helps

businesses to manage their production costs.

Using Traditional Costing method

makes things difficult for the

management in gathering the data

related to production as they do

not provide various cost centres to

the firm.

www.website.com

Activity Based Costing (ABC) helps in improving the processes of business and indirect cost would be

allocated to each and every product that firm produces. In this method businesses would be able to

exclude the cost, such as factory costs, that are not related to the products that firm produces. When the

costs are allocated to each and every product or activity, it helps the firm to improve its processes. This

method also helps in determining the products that are useless for the business and then firm can stop

their production.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.