Deakin University MAA262 Management Accounting Assignment Solution

VerifiedAdded on 2023/06/07

|10

|1193

|316

Homework Assignment

AI Summary

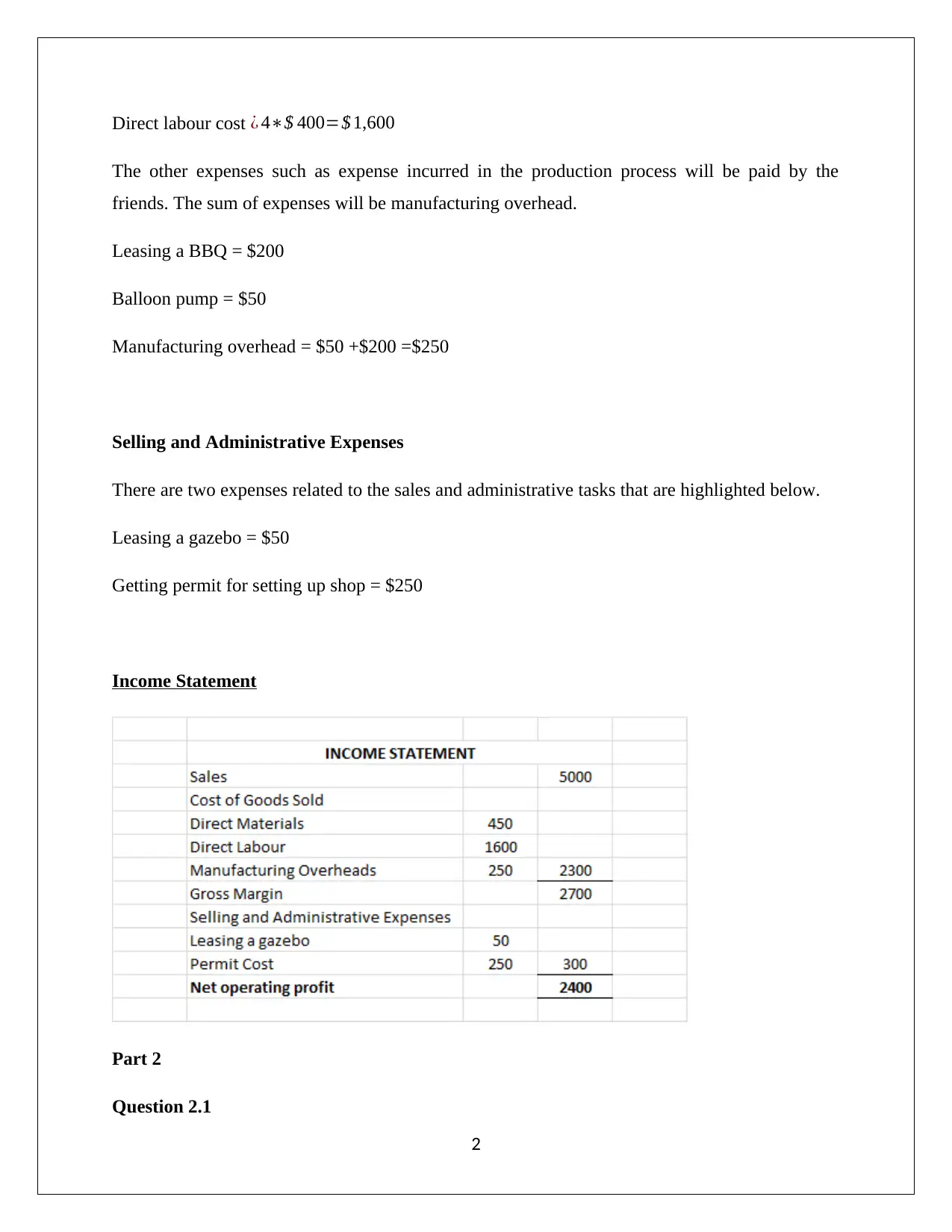

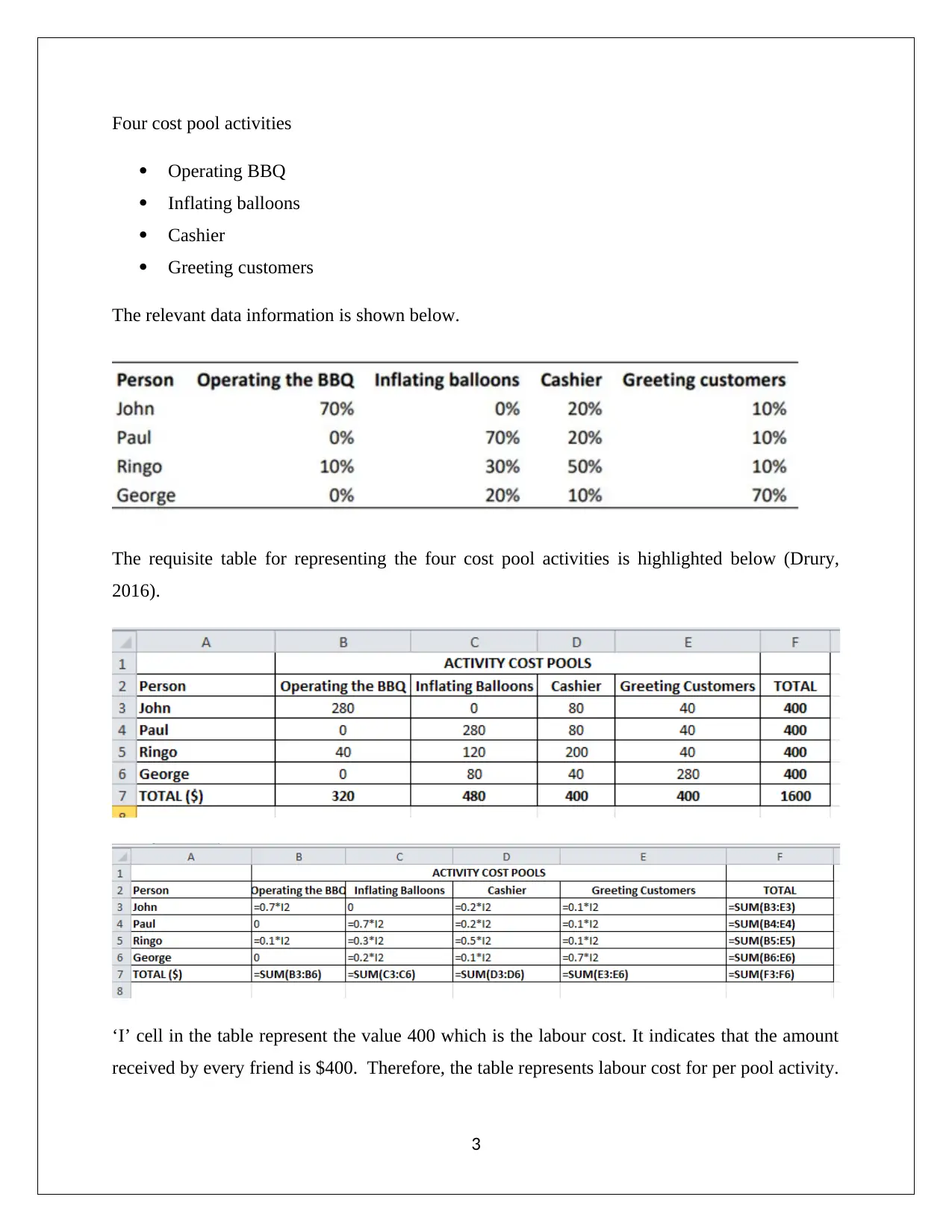

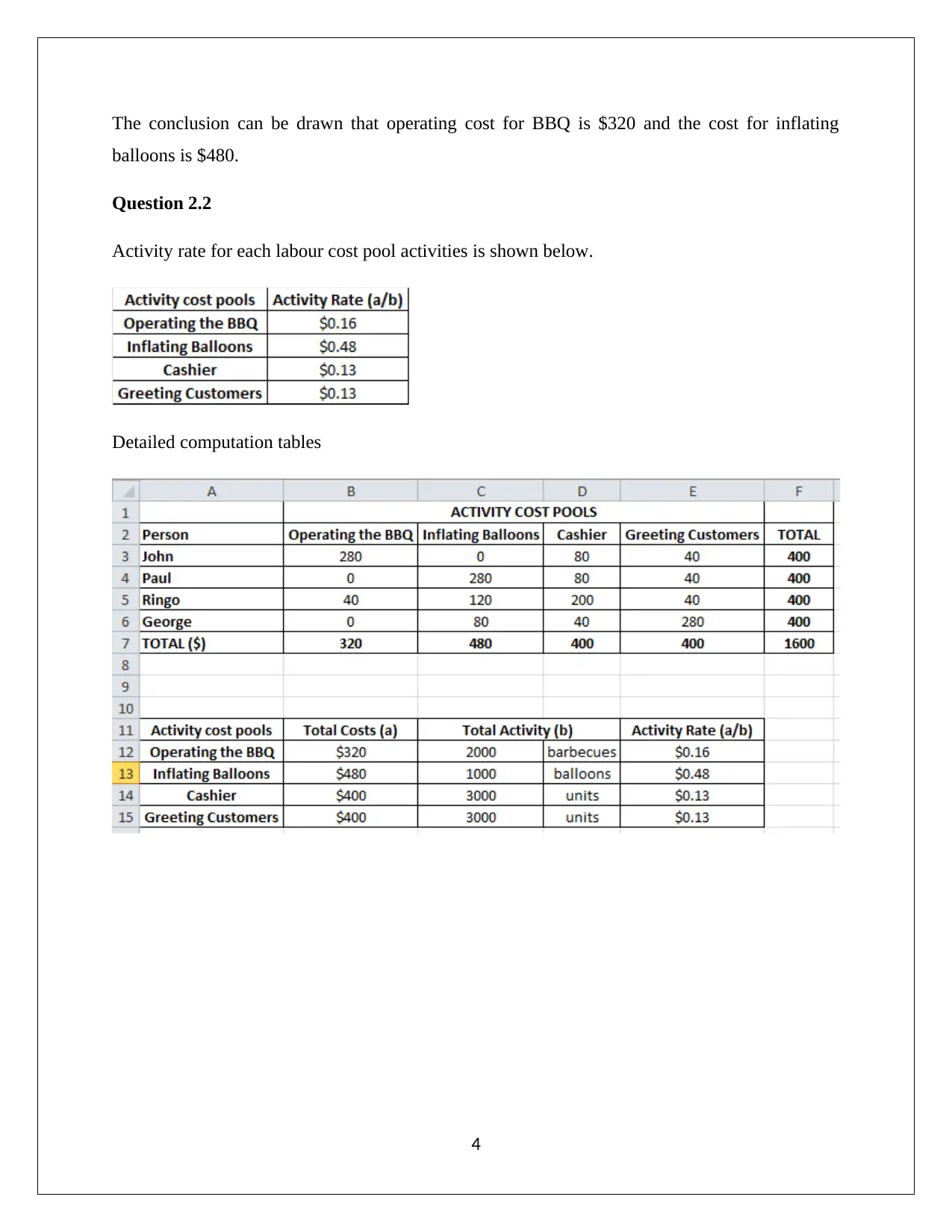

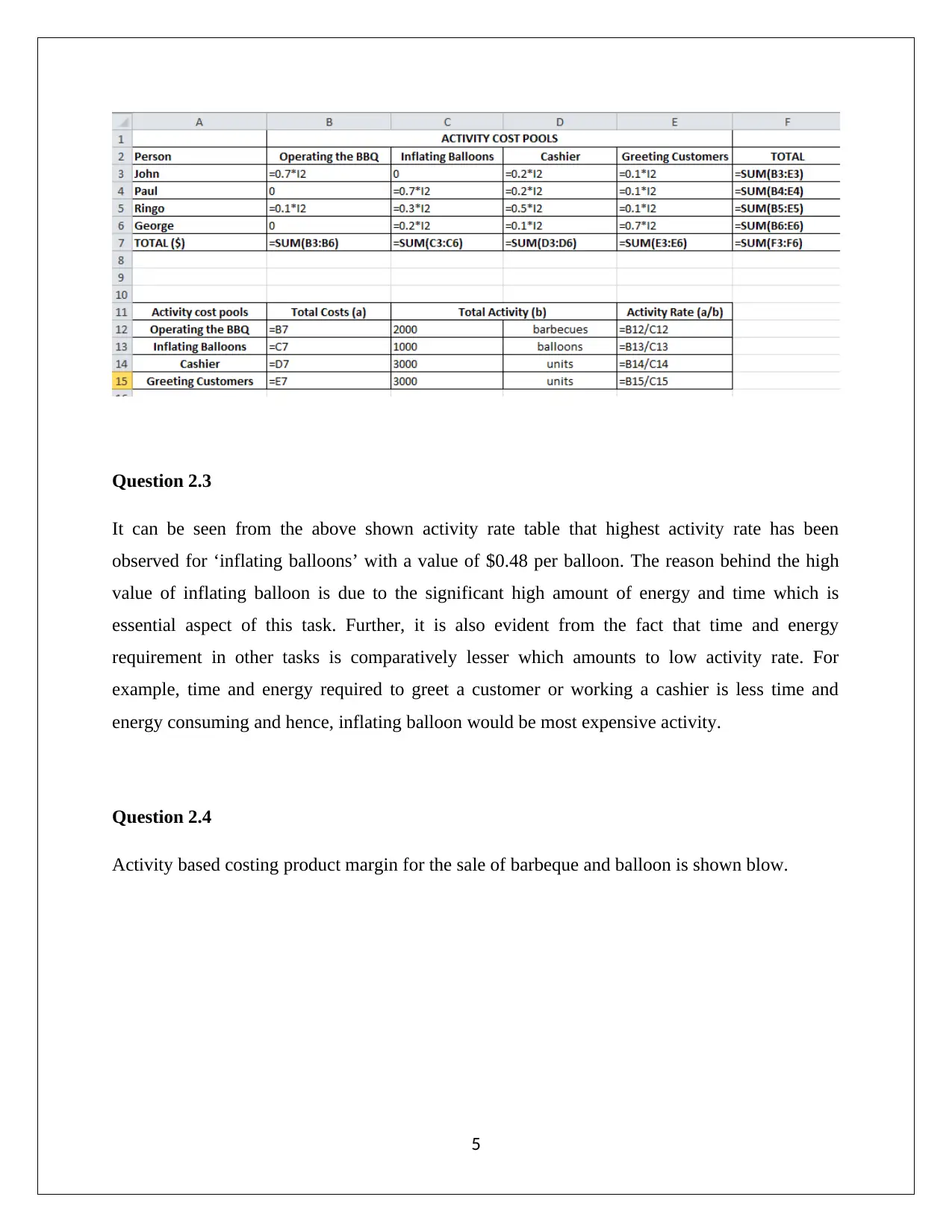

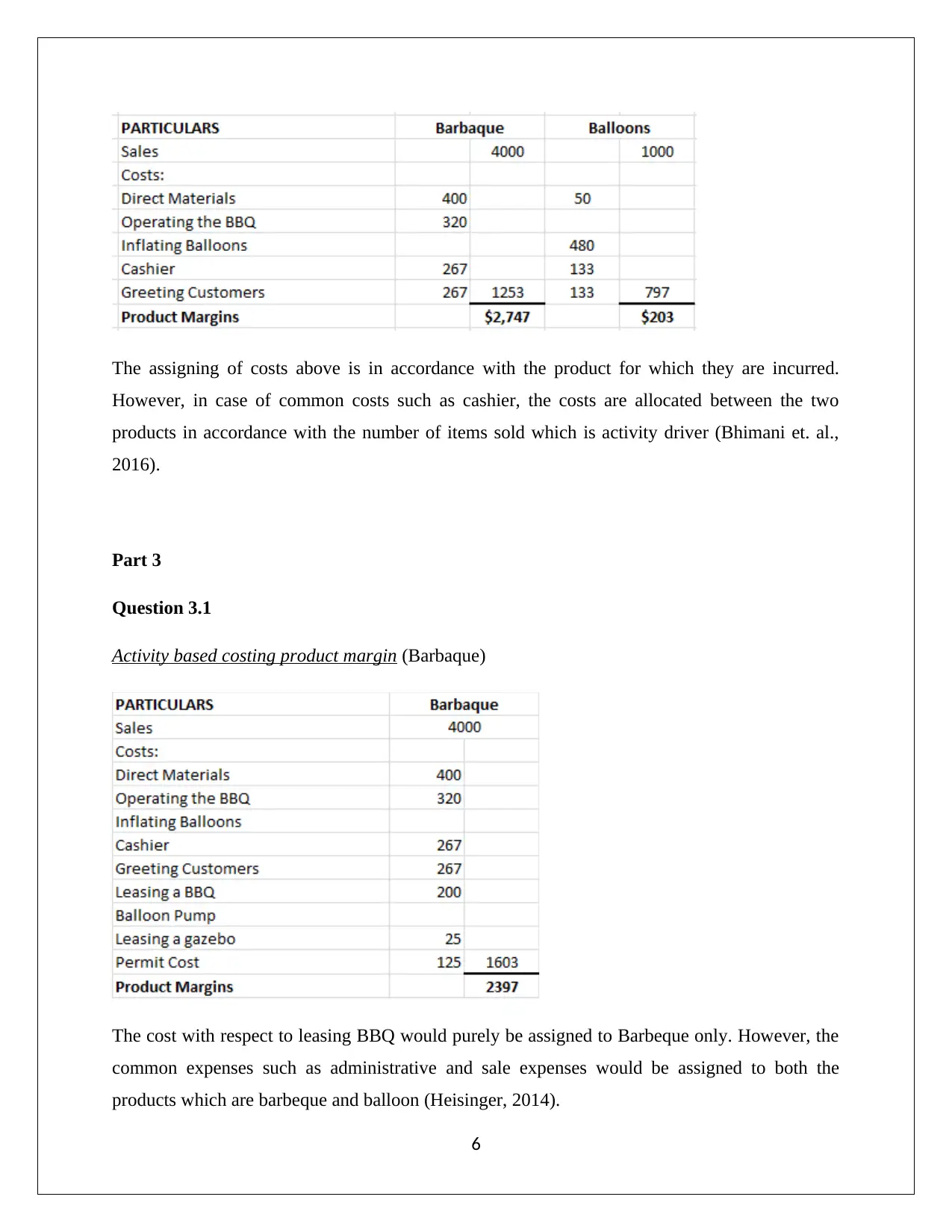

This assignment solution addresses a management accounting problem involving a small business selling barbeques and balloons. It begins with calculating the income statement, including net sales, cost of goods sold, and various expenses. The solution then delves into activity-based costing (ABC), identifying cost pools and activity rates for tasks like operating the BBQ, inflating balloons, and cashiering. It analyzes product margins for both barbeque and balloon sales, assigning costs based on activity drivers. Furthermore, the assignment evaluates the fairness of profit distribution among partners and assesses the profitability of selling balloons. The analysis includes detailed calculations, tables, and conclusions, providing a comprehensive understanding of cost accounting principles and their application in business decision-making.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.