Activity Based Costing Model: Implementation in CSL Limited

VerifiedAdded on 2023/06/13

|10

|2693

|393

Report

AI Summary

This report provides an in-depth analysis of the Activity Based Costing (ABC) model and its potential benefits for CSL Limited, a global biotechnology company. It examines the features of the ABC model, highlighting its advantages over traditional costing methods in accurately allocating overhead costs to various activities. The report discusses how the ABC model can align with CSL Limited's strategic goals, particularly in research and development, by providing detailed cost information for better decision-making and cost control. Recommendations are made for the implementation of the ABC model within CSL Limited, including cost driver and activity analysis. Additionally, the report suggests the adoption of a top-down costing model to further enhance cost management in clinical activities. The ultimate goal is to improve operational efficiency, support strategic priorities, and achieve long-term objectives through effective cost management practices.

1

Activity Based Costing

Activity Based Costing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Executive Summary

The present report is developed to gain an adequate understanding of the Activity based

costing model and its benefits realized by the business corporations. It has been extracted from

the overall analysis carried put in report that ABC costing is largely efficient in providing an

accurate determination of overhead costs to the business corporations on the basis of level of

output. The examination of the implementation of ABC costing method in CSL Limited has

depicted that the method is highly effective in realizing its corporate strategies and objectives.

The company is recommend to adopt the use of ABC costing method in comparison to

traditional method of costing for accurate identification of cost incurred in each of its clinical

research activities. In addition to ABC costing model, it is recommended to adopt the use of top

down costing model for accurate identification of the operational costs of its different clinical

activities.

Executive Summary

The present report is developed to gain an adequate understanding of the Activity based

costing model and its benefits realized by the business corporations. It has been extracted from

the overall analysis carried put in report that ABC costing is largely efficient in providing an

accurate determination of overhead costs to the business corporations on the basis of level of

output. The examination of the implementation of ABC costing method in CSL Limited has

depicted that the method is highly effective in realizing its corporate strategies and objectives.

The company is recommend to adopt the use of ABC costing method in comparison to

traditional method of costing for accurate identification of cost incurred in each of its clinical

research activities. In addition to ABC costing model, it is recommended to adopt the use of top

down costing model for accurate identification of the operational costs of its different clinical

activities.

3

Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

A: Activity Based Costing Model and its features..........................................................................4

B: Aligning of the ABC Model with the Current Goals and Strategies..........................................6

C: Recommendations about the implementation of ABC model in CSL Limited.........................9

D: Suggestion of other management accounting tool that is suitable for the chosen company....10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

A: Activity Based Costing Model and its features..........................................................................4

B: Aligning of the ABC Model with the Current Goals and Strategies..........................................6

C: Recommendations about the implementation of ABC model in CSL Limited.........................9

D: Suggestion of other management accounting tool that is suitable for the chosen company....10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Introduction

The purpose of the cost and management accounting system is allocate the different cost

between costs of goods sold and inventories in order to find the profit for internal and external

reporting. It also provides the relevant information to help the managers to take relevant

decisions and provides information to plan, control, and to measure performance. Management

accounting is essentially based on the principle that all production costs are absorbed in the cost

object. There are mainly two types of cost: direct cost and indirect cost. Direct cost is easily

traceable and can be directly allocated to the cost object while indirect cost is not easily traceable

and these costs are allocated on the basis of understanding of cost accounting system. Prior to

activity based costing, costs are allocated using the traditional costing system. Traditional costing

system uses only one overhead rate to allocate the indirect cost while activity based costing

allocates the indirect costs on the basis it is consumed in each production activity (Wagener,

2008).

In this report there will critical discussion of activity based costing model and its features.

On the basis of the critical discussion there will be discussion that how ABC model apply to the

chosen company. In this explanation detailed overview of the company will be provided and how

ABC model helps company to achieve their strategies. Recommendation will be given to

implement the ABC model in the chosen company. Apart from the ABC Costing model, another

management accounting tool has been suggested that is relevant to the chosen company.

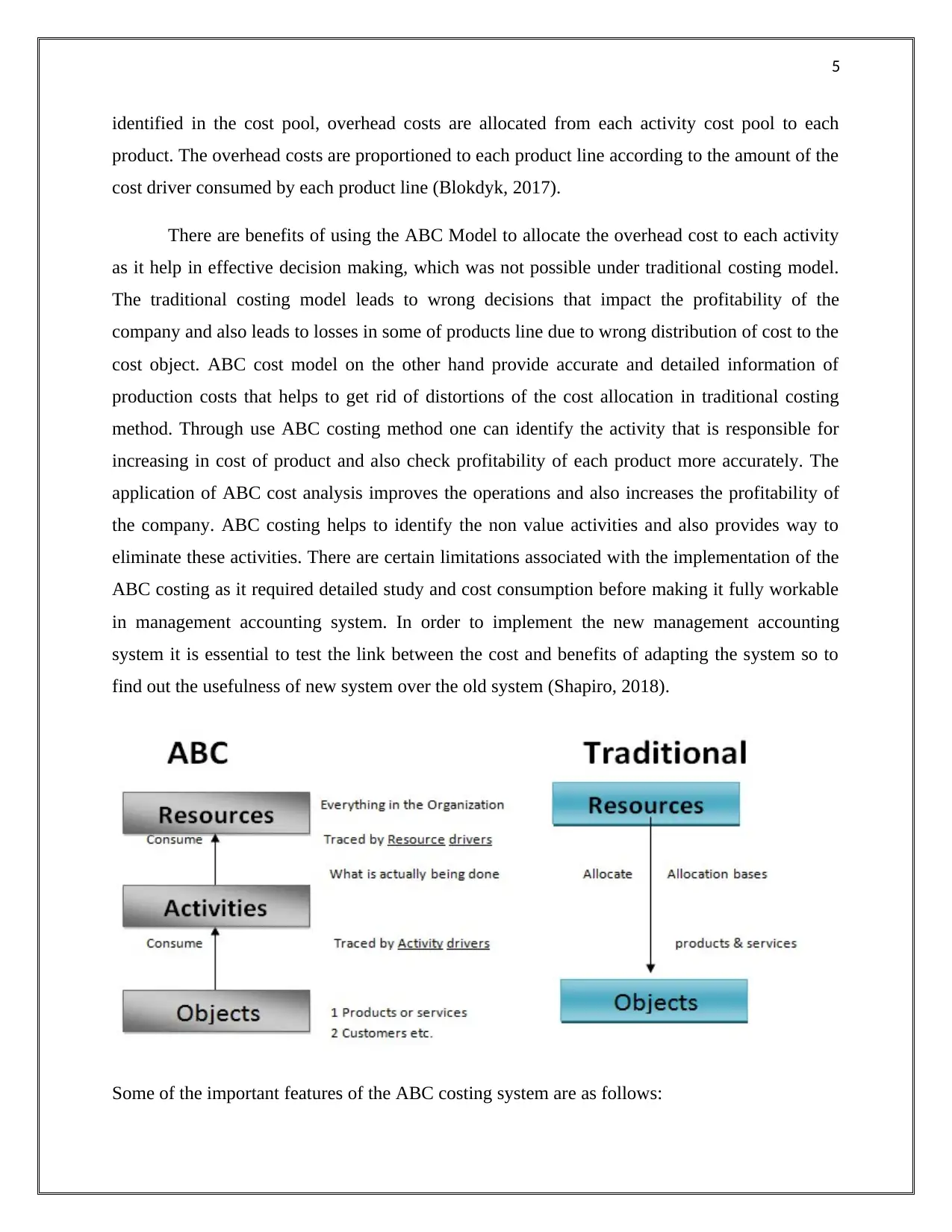

A: Activity Based Costing Model and its features

The ABC Costing model is widely used management tool in manufacturing and service

industry. It became famous due to its unique feature of allocating the indirect costs to the cost

object as it was used in each activity undertaken in the organization. Basically ABC costing

model is the two stage procedure that is applied to assign the overhead costs to the products. At

the first stage all the significant activities are identified that occurs during the production of each

product. Overhead costs are assigned to each activity on the basis of the resources consumed by

each activity. At stage two, activity cost pool statement is prepared to assign the overhead cost to

each activity and to find out the cost driver of each cost pool. On the basis of the overhead rate

Introduction

The purpose of the cost and management accounting system is allocate the different cost

between costs of goods sold and inventories in order to find the profit for internal and external

reporting. It also provides the relevant information to help the managers to take relevant

decisions and provides information to plan, control, and to measure performance. Management

accounting is essentially based on the principle that all production costs are absorbed in the cost

object. There are mainly two types of cost: direct cost and indirect cost. Direct cost is easily

traceable and can be directly allocated to the cost object while indirect cost is not easily traceable

and these costs are allocated on the basis of understanding of cost accounting system. Prior to

activity based costing, costs are allocated using the traditional costing system. Traditional costing

system uses only one overhead rate to allocate the indirect cost while activity based costing

allocates the indirect costs on the basis it is consumed in each production activity (Wagener,

2008).

In this report there will critical discussion of activity based costing model and its features.

On the basis of the critical discussion there will be discussion that how ABC model apply to the

chosen company. In this explanation detailed overview of the company will be provided and how

ABC model helps company to achieve their strategies. Recommendation will be given to

implement the ABC model in the chosen company. Apart from the ABC Costing model, another

management accounting tool has been suggested that is relevant to the chosen company.

A: Activity Based Costing Model and its features

The ABC Costing model is widely used management tool in manufacturing and service

industry. It became famous due to its unique feature of allocating the indirect costs to the cost

object as it was used in each activity undertaken in the organization. Basically ABC costing

model is the two stage procedure that is applied to assign the overhead costs to the products. At

the first stage all the significant activities are identified that occurs during the production of each

product. Overhead costs are assigned to each activity on the basis of the resources consumed by

each activity. At stage two, activity cost pool statement is prepared to assign the overhead cost to

each activity and to find out the cost driver of each cost pool. On the basis of the overhead rate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

identified in the cost pool, overhead costs are allocated from each activity cost pool to each

product. The overhead costs are proportioned to each product line according to the amount of the

cost driver consumed by each product line (Blokdyk, 2017).

There are benefits of using the ABC Model to allocate the overhead cost to each activity

as it help in effective decision making, which was not possible under traditional costing model.

The traditional costing model leads to wrong decisions that impact the profitability of the

company and also leads to losses in some of products line due to wrong distribution of cost to the

cost object. ABC cost model on the other hand provide accurate and detailed information of

production costs that helps to get rid of distortions of the cost allocation in traditional costing

method. Through use ABC costing method one can identify the activity that is responsible for

increasing in cost of product and also check profitability of each product more accurately. The

application of ABC cost analysis improves the operations and also increases the profitability of

the company. ABC costing helps to identify the non value activities and also provides way to

eliminate these activities. There are certain limitations associated with the implementation of the

ABC costing as it required detailed study and cost consumption before making it fully workable

in management accounting system. In order to implement the new management accounting

system it is essential to test the link between the cost and benefits of adapting the system so to

find out the usefulness of new system over the old system (Shapiro, 2018).

Some of the important features of the ABC costing system are as follows:

identified in the cost pool, overhead costs are allocated from each activity cost pool to each

product. The overhead costs are proportioned to each product line according to the amount of the

cost driver consumed by each product line (Blokdyk, 2017).

There are benefits of using the ABC Model to allocate the overhead cost to each activity

as it help in effective decision making, which was not possible under traditional costing model.

The traditional costing model leads to wrong decisions that impact the profitability of the

company and also leads to losses in some of products line due to wrong distribution of cost to the

cost object. ABC cost model on the other hand provide accurate and detailed information of

production costs that helps to get rid of distortions of the cost allocation in traditional costing

method. Through use ABC costing method one can identify the activity that is responsible for

increasing in cost of product and also check profitability of each product more accurately. The

application of ABC cost analysis improves the operations and also increases the profitability of

the company. ABC costing helps to identify the non value activities and also provides way to

eliminate these activities. There are certain limitations associated with the implementation of the

ABC costing as it required detailed study and cost consumption before making it fully workable

in management accounting system. In order to implement the new management accounting

system it is essential to test the link between the cost and benefits of adapting the system so to

find out the usefulness of new system over the old system (Shapiro, 2018).

Some of the important features of the ABC costing system are as follows:

6

ABC costing divided the total cost into fixed and variable cost because such information

is necessary to design the best cost system for both service and manufacturing

organization

Under this system proper distinction is made between the cost behaviour patterns. The

different cost patterns used by the ABC costing model to allocate the cost are related to

the volume, diversity, events and time.

This method uses cost drivers to allocate the cost overhead to different product as it

provide reasonable allocation of all indirect cost

Cost driver chosen reflects the cost behaviour pattern applied in the business (Wiese,

2009)

B: Aligning of the ABC Model with the Current Goals and Strategies

An Identification of Mission & Objectives of CSL Limited

CSL Limited is a recognized global biotechnology company involved in carrying out

research, development, manufacturing and marketing of products for treatment and prevention of

serious medical diseases and conditions. The company is listed on ASX and is headquartered in

Melbourne, Australia. The company mainly provides its biopharmaceutical products in Australia,

the US and the UK, Germany, Switzerland and other regions of the world. It carries out its

business operations with the two main segments, CSL Behring and Seqirus. The major product

areas of the company includes development and distribution of blood plasma derivatives,

vaccines, anti-venom and cell culture reagents used in treatment of various medical and genetic

conditions.

The company is highly committed to promote the health and well-being of people by

providing them innovative and higher quality drugs. It aims at developing and delivering

innovative biotherapies and influenza vaccines for saving lives of people from various life-

threatening medical conditions. The company passion is to improve the quality of life of large

number of patients by saving them from various life threatening conditions. The strong values

and principles of the company are fundamental to its long-term success. As such, the company

mission is recognized as discovering, developing and delivering innovative medical therapies for

the betterment of patients. The company for achieving its mission places special emphasis on

ABC costing divided the total cost into fixed and variable cost because such information

is necessary to design the best cost system for both service and manufacturing

organization

Under this system proper distinction is made between the cost behaviour patterns. The

different cost patterns used by the ABC costing model to allocate the cost are related to

the volume, diversity, events and time.

This method uses cost drivers to allocate the cost overhead to different product as it

provide reasonable allocation of all indirect cost

Cost driver chosen reflects the cost behaviour pattern applied in the business (Wiese,

2009)

B: Aligning of the ABC Model with the Current Goals and Strategies

An Identification of Mission & Objectives of CSL Limited

CSL Limited is a recognized global biotechnology company involved in carrying out

research, development, manufacturing and marketing of products for treatment and prevention of

serious medical diseases and conditions. The company is listed on ASX and is headquartered in

Melbourne, Australia. The company mainly provides its biopharmaceutical products in Australia,

the US and the UK, Germany, Switzerland and other regions of the world. It carries out its

business operations with the two main segments, CSL Behring and Seqirus. The major product

areas of the company includes development and distribution of blood plasma derivatives,

vaccines, anti-venom and cell culture reagents used in treatment of various medical and genetic

conditions.

The company is highly committed to promote the health and well-being of people by

providing them innovative and higher quality drugs. It aims at developing and delivering

innovative biotherapies and influenza vaccines for saving lives of people from various life-

threatening medical conditions. The company passion is to improve the quality of life of large

number of patients by saving them from various life threatening conditions. The strong values

and principles of the company are fundamental to its long-term success. As such, the company

mission is recognized as discovering, developing and delivering innovative medical therapies for

the betterment of patients. The company for achieving its mission places special emphasis on

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

developing a competent team of scientists and researchers for manufacturing of medicines for

helping millions of patients across the world. The objectives of the company is to remain patient-

focused and development of innovative solutions to wide range of rare and serious diseases of

the patients for securing their well-being (CSL Limited, 2018).

Identification of the Corporate Strategies of CSL Limited

The company’s long-term strategy is to become a global leader in development of rare

biopharmaceutical products for treatment of patients fighting from rare and serious diseases. For

achieving this strategy, the company is making continuous progress on becoming fastest growing

protein based technology businesses and a leading provider of vaccines products. The strategy is

realized by development and manufacturing of life-saving therapies by placing high focus on

product safety and quality (CSL Limited, 2018).

Explanation of ABC model assistance in achieving the company’s strategies

The company involved in development of innovative medical products and services has

to incur large-scale research and development investment for the use of modern medical

techniques and processes for researching and development of improved and better

biopharmaceutical products for the patients. As such, the company needs the implementation of

an efficient system of costing for covering expensive healthcare service costs. This is because the

traditional method of costing such as absorption costing is less accurate for identification of

overhead cost related with manufacturing of products. The traditional method of costing does not

prove to be effective in development of specific actions for control of deviations in context of

particular costing problems. Thus, the use of ABC costing method by CSL Limited will prove to

be largely effective in gaining more detailed information related with cost activities of the

hospital and thus development of efficient methods for cost control (Michela and Lapsley, 2005).

CSL Limited strategic priority is to become a global leader in development and

delivering of rare biopharmaceutical products such as vaccines for prevention of people from

life-threatening diseases. Therefore, the R&D activities of the company are highly complex and

require the use of an efficient costing system for identification of expenses incurred in each

activity for proper allocation of R&D expenditure by the financial manager. This will help in

improving the quality and controlling costs and assessing the overall expenses that the company

developing a competent team of scientists and researchers for manufacturing of medicines for

helping millions of patients across the world. The objectives of the company is to remain patient-

focused and development of innovative solutions to wide range of rare and serious diseases of

the patients for securing their well-being (CSL Limited, 2018).

Identification of the Corporate Strategies of CSL Limited

The company’s long-term strategy is to become a global leader in development of rare

biopharmaceutical products for treatment of patients fighting from rare and serious diseases. For

achieving this strategy, the company is making continuous progress on becoming fastest growing

protein based technology businesses and a leading provider of vaccines products. The strategy is

realized by development and manufacturing of life-saving therapies by placing high focus on

product safety and quality (CSL Limited, 2018).

Explanation of ABC model assistance in achieving the company’s strategies

The company involved in development of innovative medical products and services has

to incur large-scale research and development investment for the use of modern medical

techniques and processes for researching and development of improved and better

biopharmaceutical products for the patients. As such, the company needs the implementation of

an efficient system of costing for covering expensive healthcare service costs. This is because the

traditional method of costing such as absorption costing is less accurate for identification of

overhead cost related with manufacturing of products. The traditional method of costing does not

prove to be effective in development of specific actions for control of deviations in context of

particular costing problems. Thus, the use of ABC costing method by CSL Limited will prove to

be largely effective in gaining more detailed information related with cost activities of the

hospital and thus development of efficient methods for cost control (Michela and Lapsley, 2005).

CSL Limited strategic priority is to become a global leader in development and

delivering of rare biopharmaceutical products such as vaccines for prevention of people from

life-threatening diseases. Therefore, the R&D activities of the company are highly complex and

require the use of an efficient costing system for identification of expenses incurred in each

activity for proper allocation of R&D expenditure by the financial manager. This will help in

improving the quality and controlling costs and assessing the overall expenses that the company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

will incur in delivering its products and services to the target consumers. The departmental

structure used in traditional method of costing does not seem to be apt as per the corporate

strategy of CSL Limited. This is because it is not suitable for accurately reflecting the cost

involved in different type of activities involved in offering the required products and services to

the patients. ABC costing method is highly efficient in developing a relation between cost of

patient care and the patient outcomes. It will accurately help in identifying of wasteful activities

and thus improving the operational efficiency by aligning the strategic priorities of the company

with its overall mission and goals (Popesko and Novak, 2014).

The analysis of the overall cost incurred by the company on the basis of patient level will

help in providing an accurate measurement of the operational cost and facilitating the managers

to develop a n adequate understanding of the actual cost of health care. It will help the company

to realize its corporate strategies by implementation of adequate control measures that will

facilitate in achieving its long-term goals and objectives. This can be achieved largely by the use

of ABC costing method by identification of the correlation between a specific R& D activity and

the resources required for carrying out it and thus determining accurately the resources cost (Zhu

and Lin, 2012).

C: Recommendations about the implementation of ABC model in CSL Limited

CSL Limited is recommended to implement the model of ABC costing by use of

following tools as follows:

Cost Driver Analysis: The method adopts the use of identifying the causes of overhead

for allocating the overhead cost as per the number of units of produced manufactured by

the company. This requires the company to gain an adequate understanding of the major

cost drivers of clinical research that can be categorized on the basis of clinical procedures

costs, administrative staff costs and the site monitoring costs. This is essential for

improving the efficiency of clinical trial and reduction of significant costs (Kinney and

Raiborn, 2012).

Activity Analysis: This method involves the use of following steps that are, gaining an

analysis of overall activities required in delivering products to the patients, gathering of

cost data. Aligning the cost as per each activity, development of output metrics and

will incur in delivering its products and services to the target consumers. The departmental

structure used in traditional method of costing does not seem to be apt as per the corporate

strategy of CSL Limited. This is because it is not suitable for accurately reflecting the cost

involved in different type of activities involved in offering the required products and services to

the patients. ABC costing method is highly efficient in developing a relation between cost of

patient care and the patient outcomes. It will accurately help in identifying of wasteful activities

and thus improving the operational efficiency by aligning the strategic priorities of the company

with its overall mission and goals (Popesko and Novak, 2014).

The analysis of the overall cost incurred by the company on the basis of patient level will

help in providing an accurate measurement of the operational cost and facilitating the managers

to develop a n adequate understanding of the actual cost of health care. It will help the company

to realize its corporate strategies by implementation of adequate control measures that will

facilitate in achieving its long-term goals and objectives. This can be achieved largely by the use

of ABC costing method by identification of the correlation between a specific R& D activity and

the resources required for carrying out it and thus determining accurately the resources cost (Zhu

and Lin, 2012).

C: Recommendations about the implementation of ABC model in CSL Limited

CSL Limited is recommended to implement the model of ABC costing by use of

following tools as follows:

Cost Driver Analysis: The method adopts the use of identifying the causes of overhead

for allocating the overhead cost as per the number of units of produced manufactured by

the company. This requires the company to gain an adequate understanding of the major

cost drivers of clinical research that can be categorized on the basis of clinical procedures

costs, administrative staff costs and the site monitoring costs. This is essential for

improving the efficiency of clinical trial and reduction of significant costs (Kinney and

Raiborn, 2012).

Activity Analysis: This method involves the use of following steps that are, gaining an

analysis of overall activities required in delivering products to the patients, gathering of

cost data. Aligning the cost as per each activity, development of output metrics and

9

carrying out overall analysis of cost. It will prove to be largely helpful in assigning the

indirect costs to the number of products manufactured by the company (Haider and Asif,

2012).

D: Suggestion of other management accounting tool that is suitable for the chosen company

The management accounting tool other ABC costing model that can be used in the health

care industry and which is suitable for the CSL Limited is Top Down cost allocation approach.

This method is also known as macro costing, gross costing or average costing. This cost

allocation approach uses information such as current utilization and actual expenses to find out

the direct and indirect cost. Than these cost are allocated to various specialties and services areas

so that no expenses is left to be allocated to cost center. This method is most suitable in health

care industry as it allocate the overall cost expenses in meaningful manner as compare to

traditional costing approach (Baveja and Kipp, 2014).

Conclusion

ABC costing model has been considered as the alternative approach to the traditional

costing model because it takes into all the limitations of the traditional costing system and

provide a new approach to allocate the cost to the cost object. Apart from ABC costing model,

top down model has been suggested as it helps to allocate the cost in proper manner in health

care industry.

carrying out overall analysis of cost. It will prove to be largely helpful in assigning the

indirect costs to the number of products manufactured by the company (Haider and Asif,

2012).

D: Suggestion of other management accounting tool that is suitable for the chosen company

The management accounting tool other ABC costing model that can be used in the health

care industry and which is suitable for the CSL Limited is Top Down cost allocation approach.

This method is also known as macro costing, gross costing or average costing. This cost

allocation approach uses information such as current utilization and actual expenses to find out

the direct and indirect cost. Than these cost are allocated to various specialties and services areas

so that no expenses is left to be allocated to cost center. This method is most suitable in health

care industry as it allocate the overall cost expenses in meaningful manner as compare to

traditional costing approach (Baveja and Kipp, 2014).

Conclusion

ABC costing model has been considered as the alternative approach to the traditional

costing model because it takes into all the limitations of the traditional costing system and

provide a new approach to allocate the cost to the cost object. Apart from ABC costing model,

top down model has been suggested as it helps to allocate the cost in proper manner in health

care industry.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

References

Baveja, L. and Kipp, R. 2014. Top down cost allocation can help the universal health care

schemes in developing countries set better packages rates. [Online]. Available on:

http://in.milliman.com/uploadedFiles/insight/2014/universal-healthcare-schemes.pdf [Accessed

on: 17 May, 2018].

Blokdyk, G. 2017. Activity-based Costing ABC: Beyond the Basics. CreateSpace Independent

Publishing Platform.

CSL Limited. 2018. [Online]. Available at: https://www.csl.com/ [Accessed on: 17 May 2018].

Haider, A. and Asif, E. 2012. Quality Operations Procedures for Pharmaceutical, API, and

Biotechnology. CRC Press.

Kinney, M. and Raiborn, C. 2012. Cost Accounting: Foundations and Evolutions. Cengage

Learning.

Michela, A. and Lapsley, I. 2005. Activity Based Costing In Healthcare: A UK Case Study.

Research In Healthcare Financial Management 10(1), pp.61-75.

Popesko, B. and Novak, P. 2014. Application of ABC Method in Hospital Management. Recent

Researches in Economics and Management Transformation.

Shapiro, J.F. 2018. On the Connections Between Activity Based Costing Models and

Optimization Models for Decision Support (Classic Reprint). Fb&c Limited.

Wagener, D. 2008. Activity-Based costing and its later development into activity based

budgeting and management. GRIN Verlag.

Wiese, N. 2009. Activity-Based-Costing (ABC). GRIN Verlag.

Zhu, F. and Lin, M. 2012. Test and Optimization of ABC-System. Proceedings of 2012

International Conference on Mechanical Engineering and Material Science.

References

Baveja, L. and Kipp, R. 2014. Top down cost allocation can help the universal health care

schemes in developing countries set better packages rates. [Online]. Available on:

http://in.milliman.com/uploadedFiles/insight/2014/universal-healthcare-schemes.pdf [Accessed

on: 17 May, 2018].

Blokdyk, G. 2017. Activity-based Costing ABC: Beyond the Basics. CreateSpace Independent

Publishing Platform.

CSL Limited. 2018. [Online]. Available at: https://www.csl.com/ [Accessed on: 17 May 2018].

Haider, A. and Asif, E. 2012. Quality Operations Procedures for Pharmaceutical, API, and

Biotechnology. CRC Press.

Kinney, M. and Raiborn, C. 2012. Cost Accounting: Foundations and Evolutions. Cengage

Learning.

Michela, A. and Lapsley, I. 2005. Activity Based Costing In Healthcare: A UK Case Study.

Research In Healthcare Financial Management 10(1), pp.61-75.

Popesko, B. and Novak, P. 2014. Application of ABC Method in Hospital Management. Recent

Researches in Economics and Management Transformation.

Shapiro, J.F. 2018. On the Connections Between Activity Based Costing Models and

Optimization Models for Decision Support (Classic Reprint). Fb&c Limited.

Wagener, D. 2008. Activity-Based costing and its later development into activity based

budgeting and management. GRIN Verlag.

Wiese, N. 2009. Activity-Based-Costing (ABC). GRIN Verlag.

Zhu, F. and Lin, M. 2012. Test and Optimization of ABC-System. Proceedings of 2012

International Conference on Mechanical Engineering and Material Science.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.