Semester 1 Accounting & Finance: Activity Based Costing System

VerifiedAdded on 2023/05/31

|8

|1470

|307

Essay

AI Summary

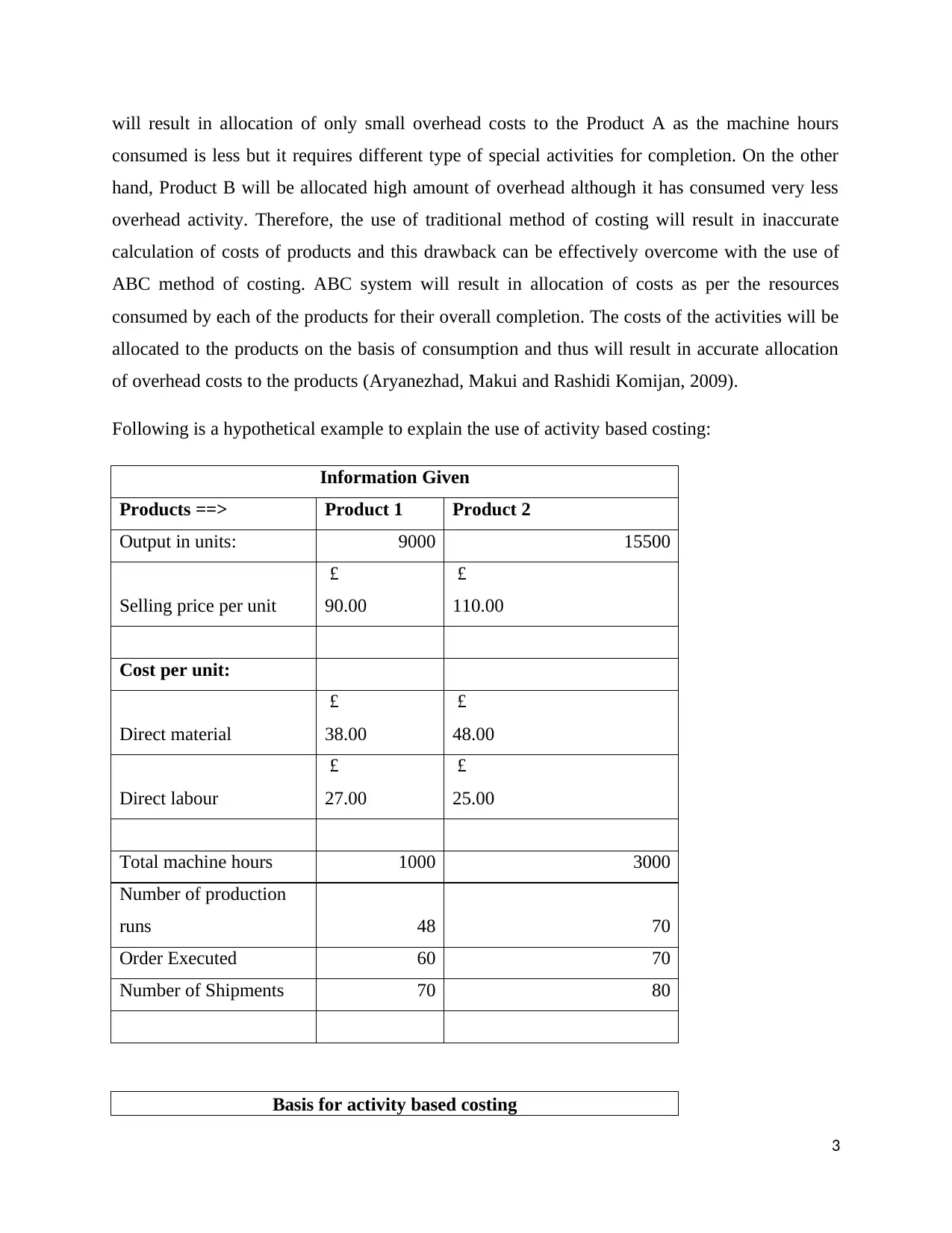

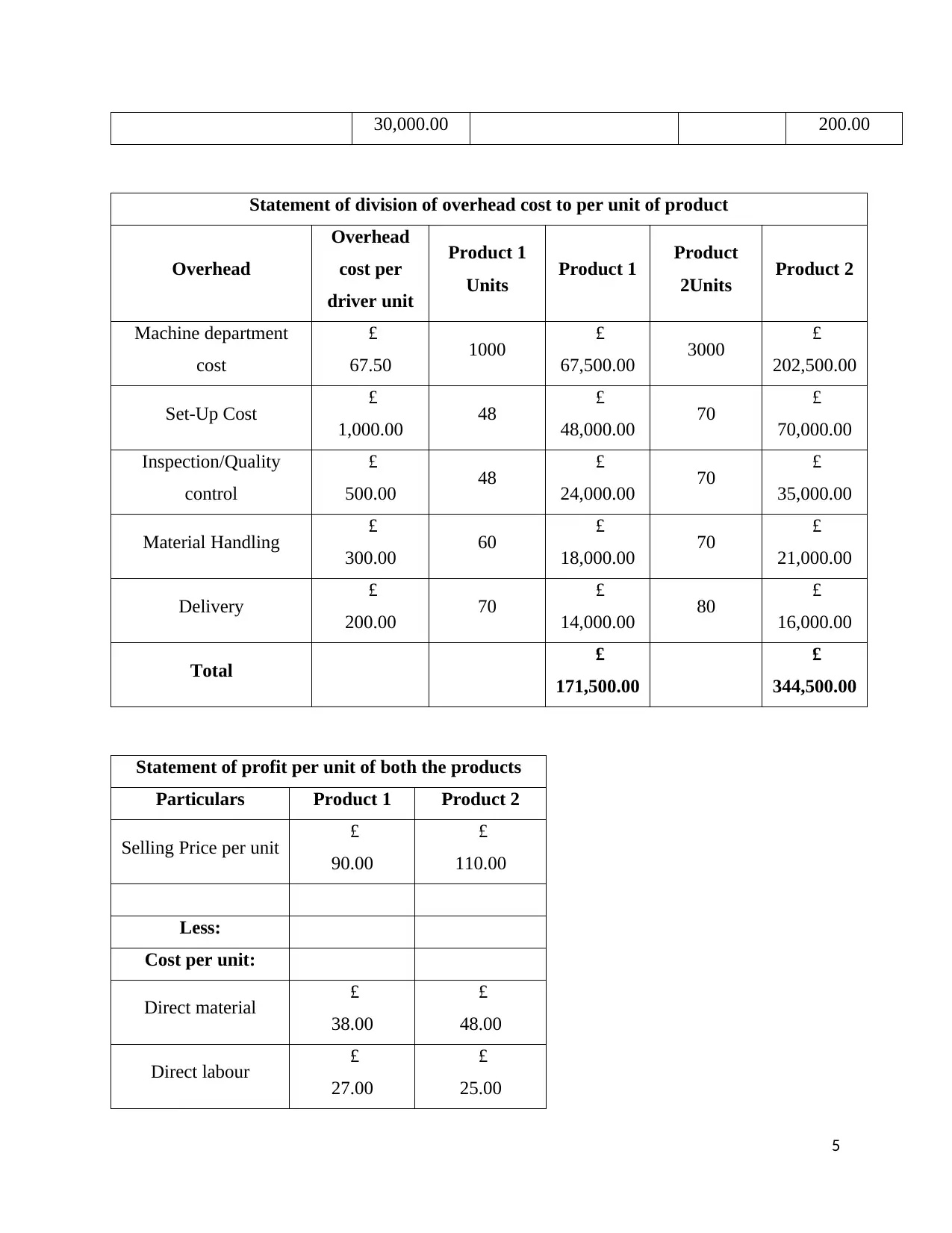

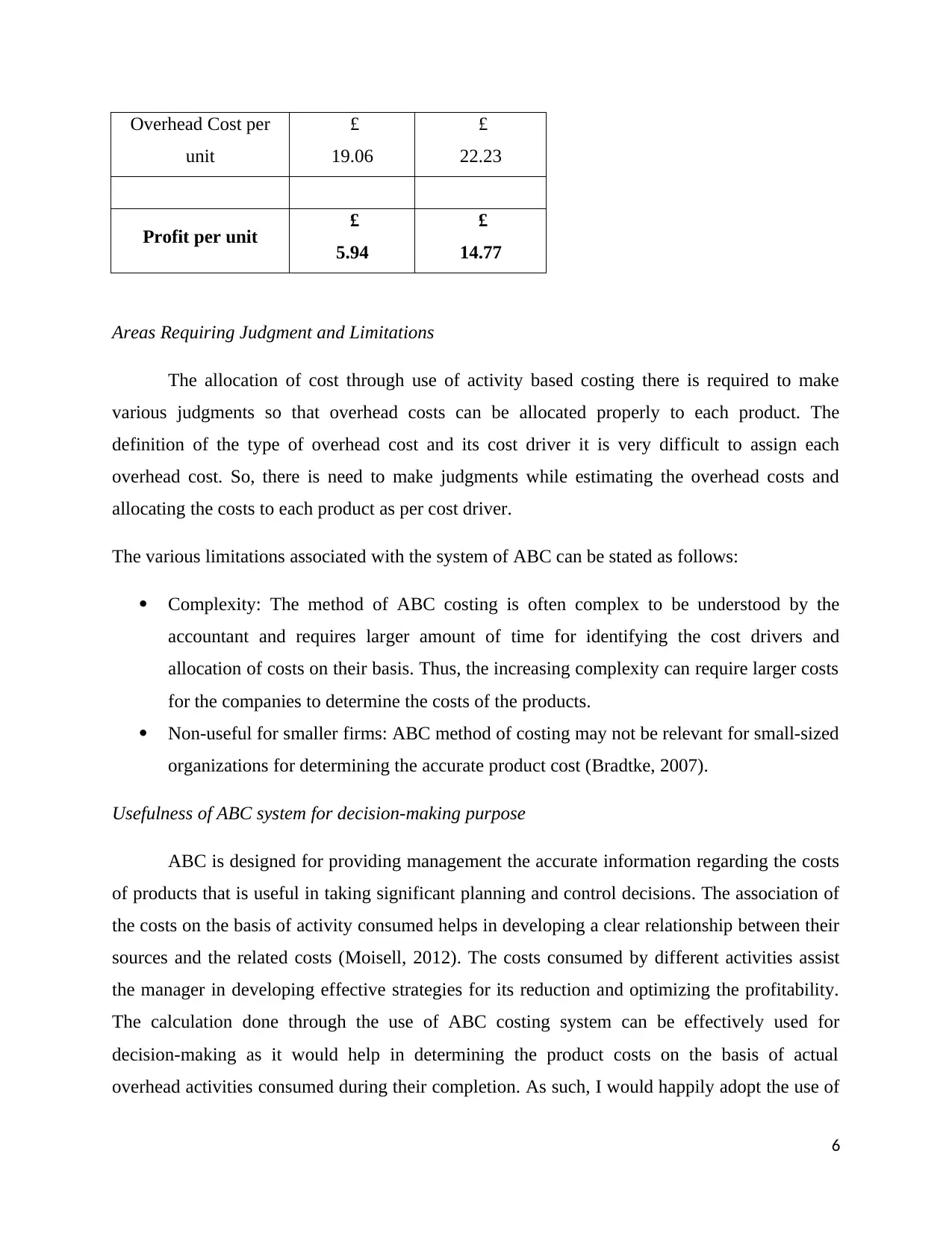

This essay discusses the application and usefulness of the Activity-Based Costing (ABC) system in management accounting for allocating costs to products, contrasting it with traditional methods. It highlights the increasing competition driving businesses to adopt efficient accounting systems for accurate cost information. The ABC system identifies activities as cost drivers and allocates overhead costs accordingly, providing a more precise product costing compared to conventional methods that often rely on machine hours, which can lead to inaccurate cost allocations, especially for products with varying activity requirements. A hypothetical example illustrates the ABC system's application, detailing the allocation of overhead costs per unit for two products. The essay also addresses the judgmental aspects and limitations of ABC, such as complexity and suitability for smaller firms, while emphasizing its utility in decision-making by providing accurate cost information for planning, control, and profitability optimization. Ultimately, the essay concludes that the ABC costing system is more effective than traditional methods for informed decision-making.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.