University Cost Accounting Report: Laurie Manufacturing Case Study

VerifiedAdded on 2023/01/16

|12

|1339

|43

Report

AI Summary

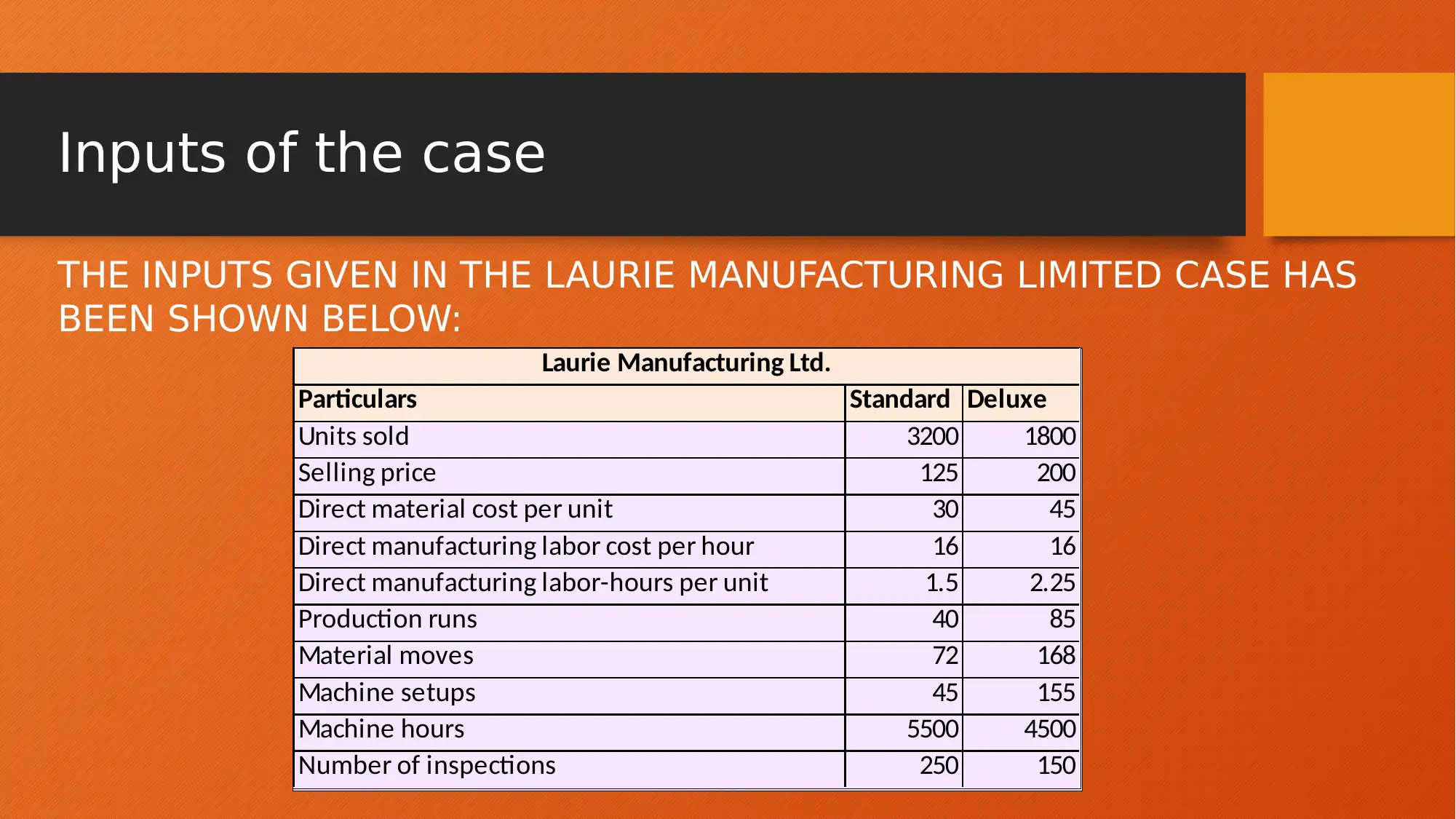

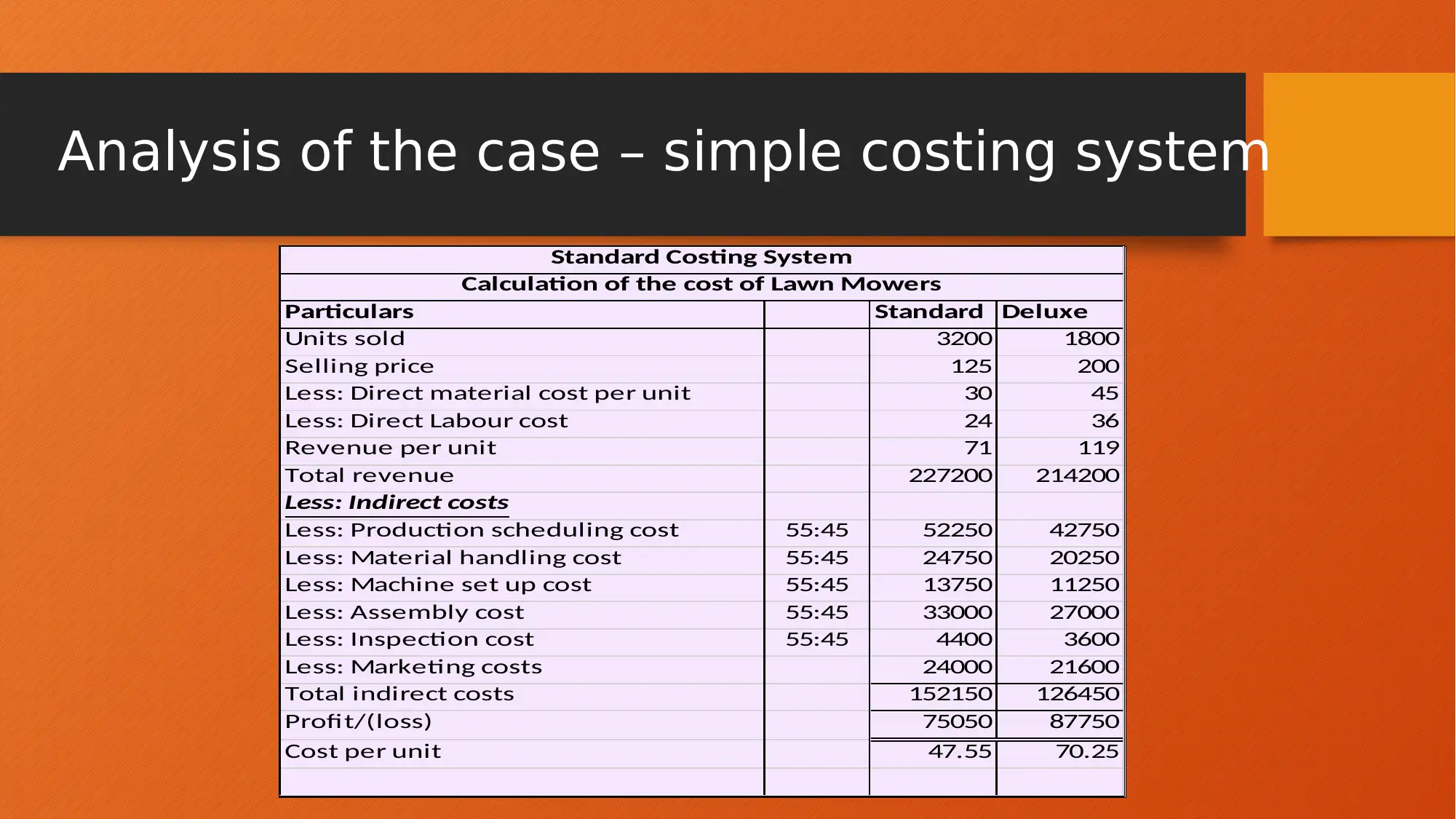

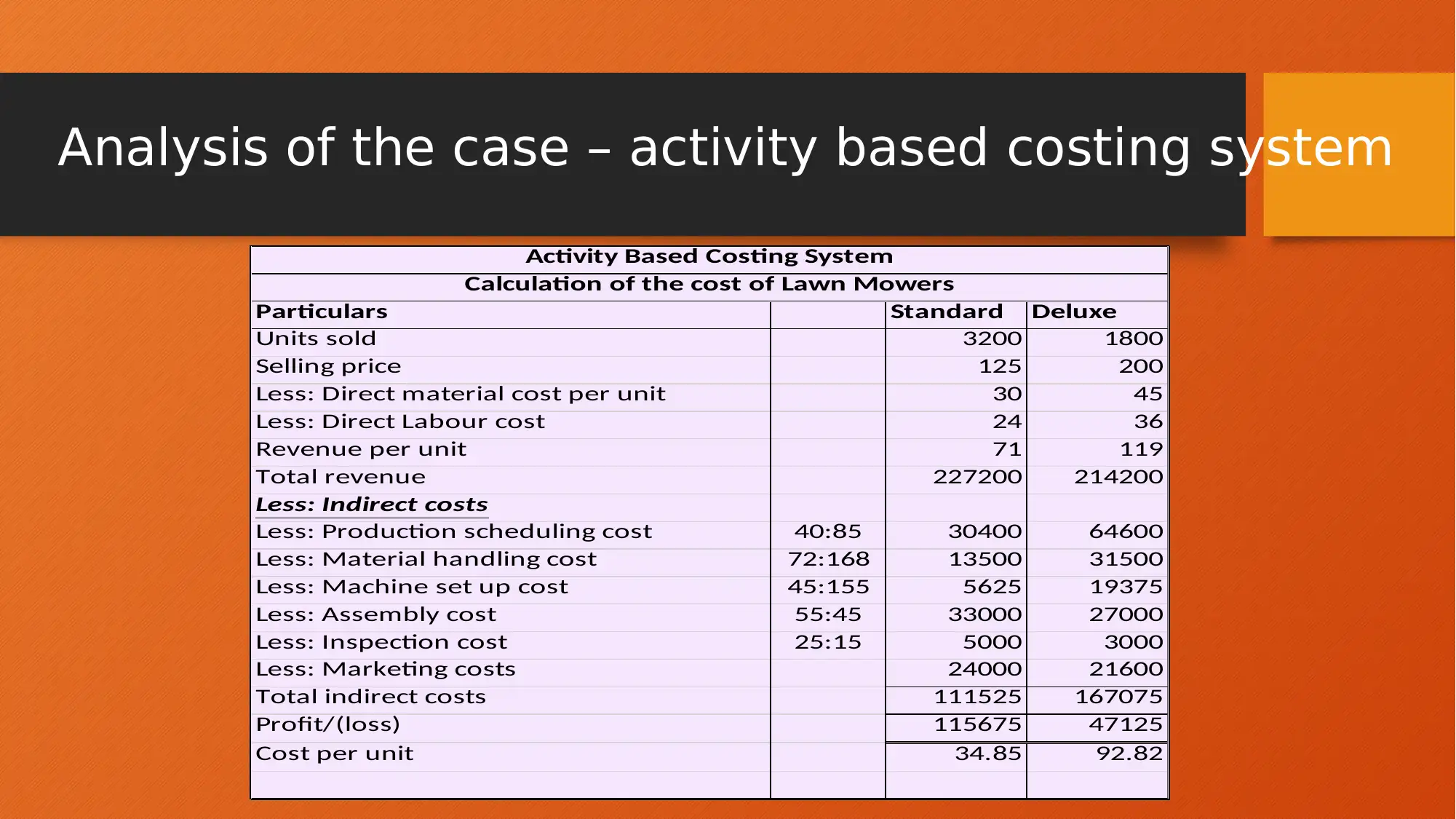

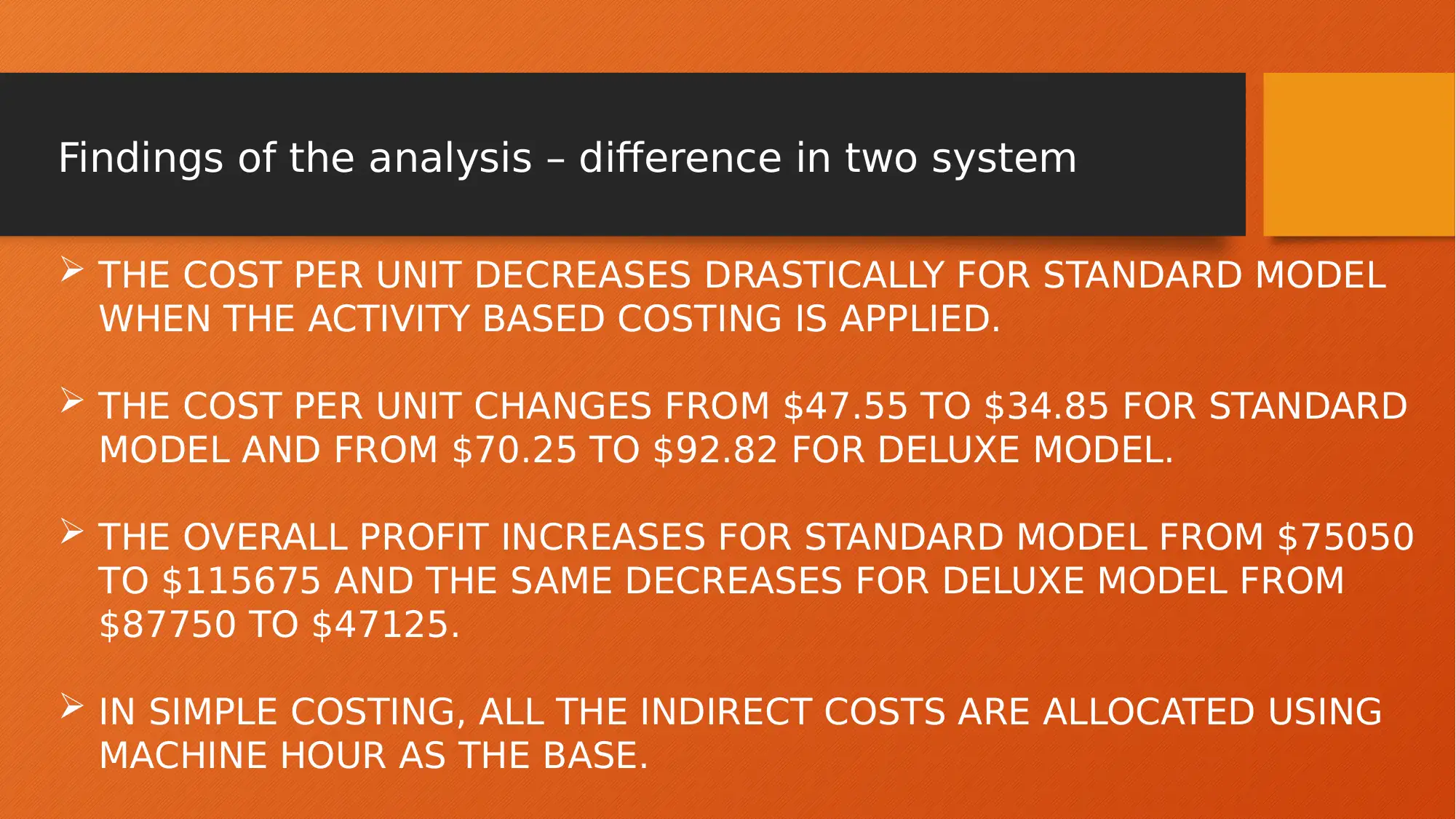

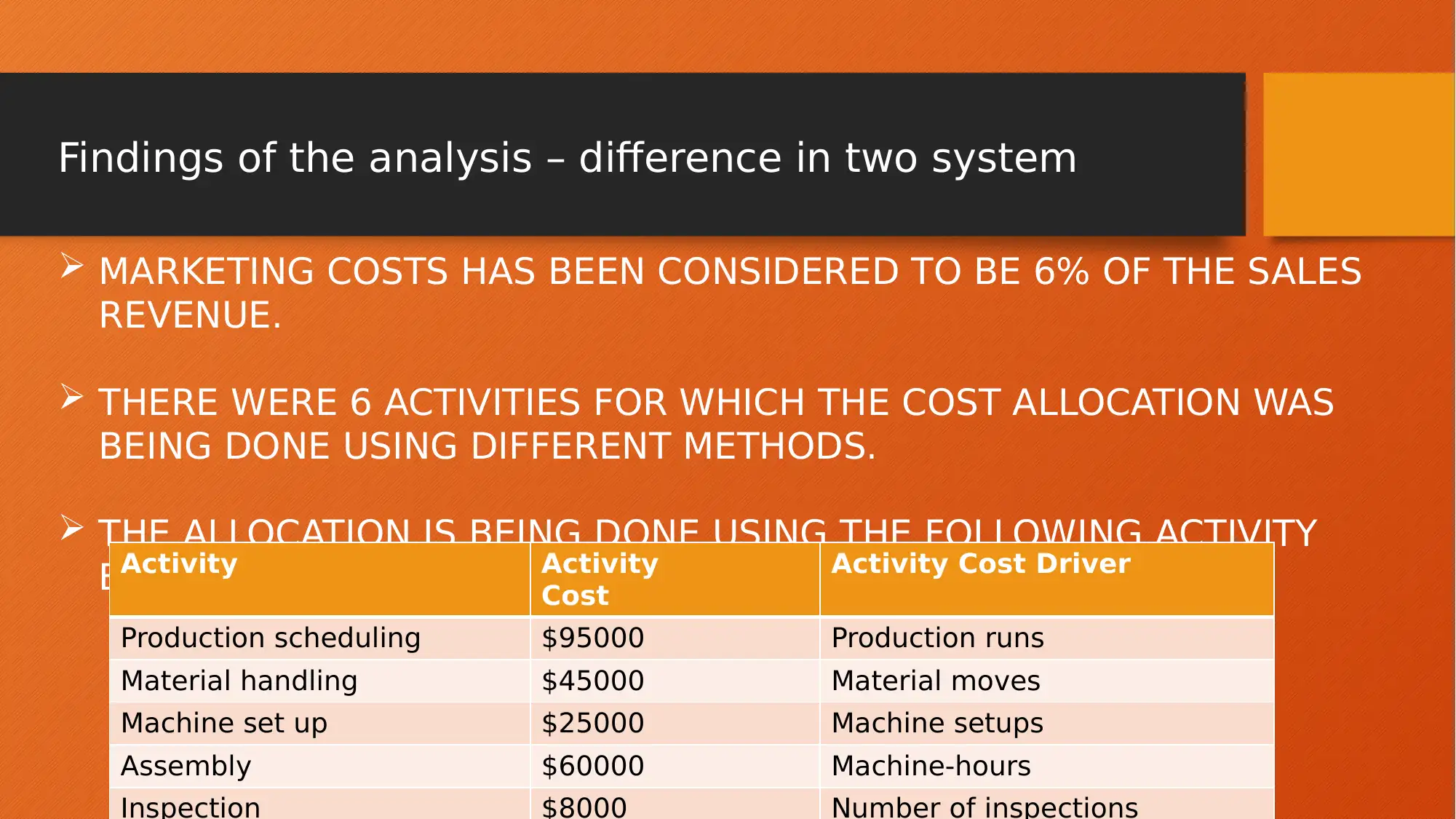

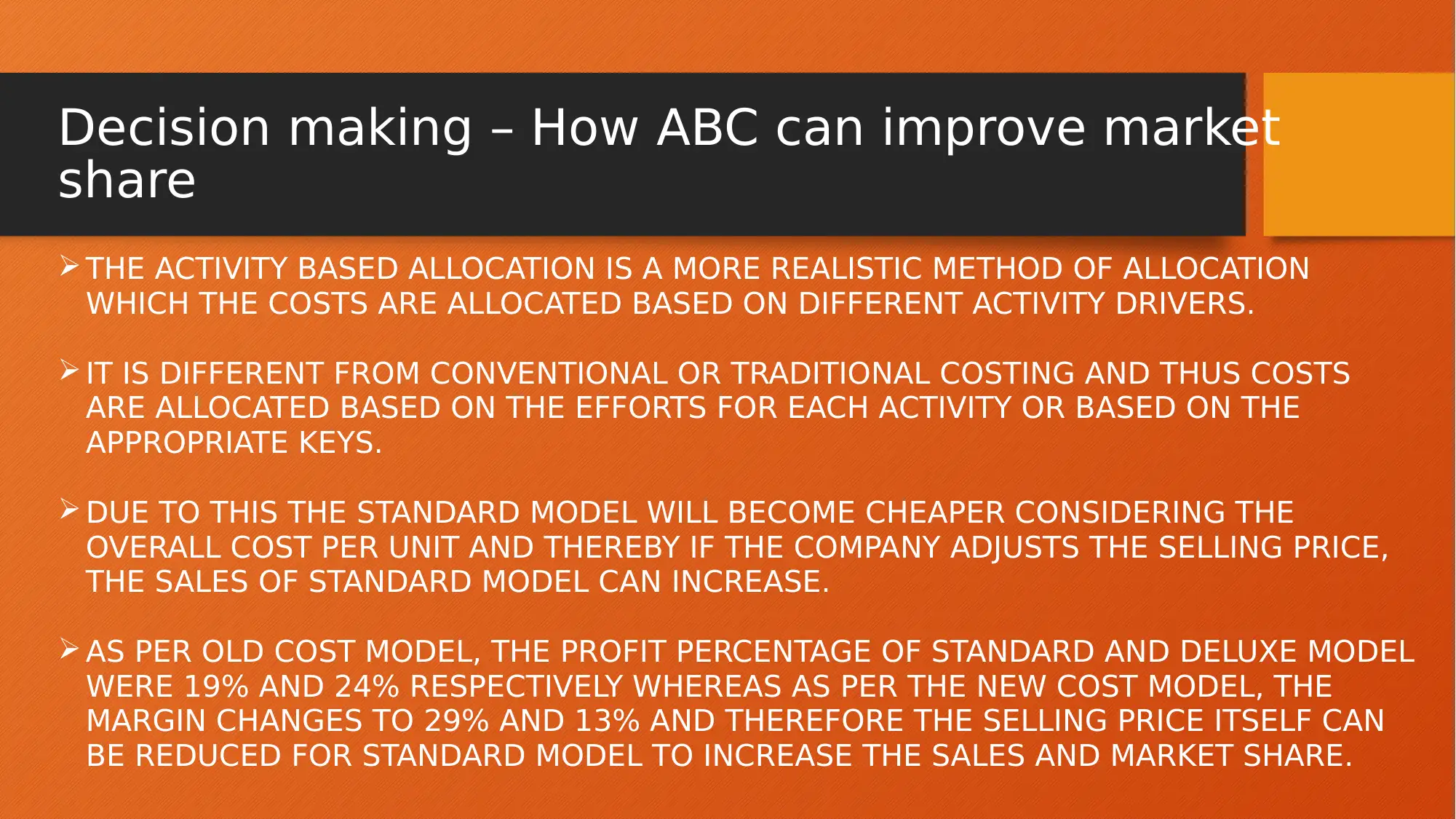

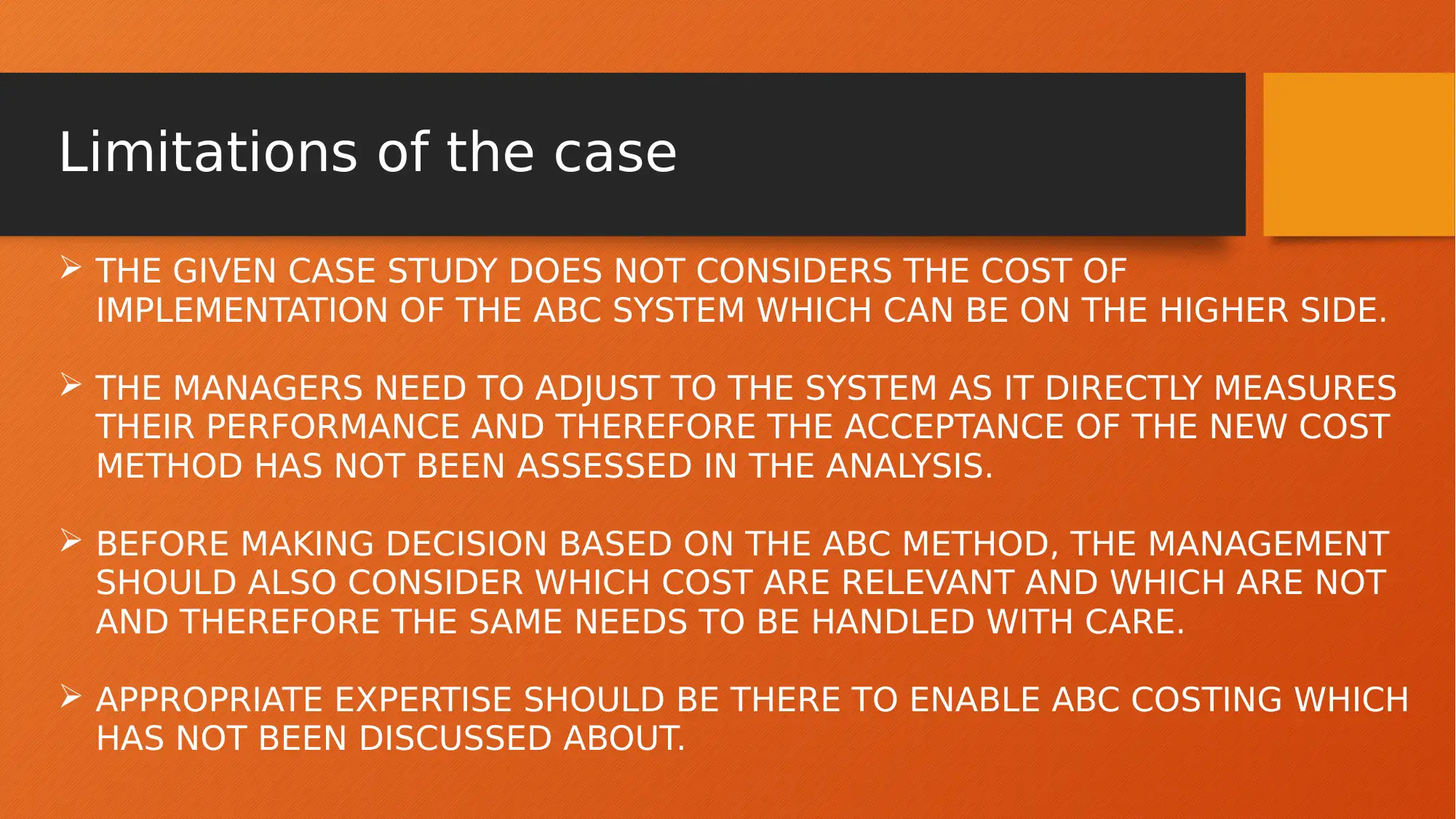

This report analyzes the cost accounting systems of Laurie Manufacturing Ltd., a company that manufactures lawn mowers. The report compares the simple costing system, currently used by the company, with an activity-based costing (ABC) system. The analysis includes detailed calculations of product costs under both systems, considering direct materials, direct labor, and various indirect costs. The findings highlight significant differences in cost per unit and profitability between the two methods, particularly for the standard and deluxe mower models. The report then explores how the ABC system can improve the company's market share by providing a more accurate allocation of costs, potentially allowing for adjustments in selling prices. The report also discusses the limitations of the case, such as the cost of implementing ABC and the need for management adaptation, and provides references for further reading.

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.