HI5017 Managerial Accounting: Activity Based Costing for Lynas

VerifiedAdded on 2023/06/11

|15

|3165

|214

Report

AI Summary

This report assesses the implementation of Activity-Based Costing (ABC) within Lynas Corporation to improve cost management and align with corporate strategies. It begins by explaining ABC and its features, highlighting its role in accurate cost allocation and performance improvement. The report then examines how ABC can support Lynas Corporation's mission, objectives, and strategies, particularly in enhancing its competitiveness and financial performance. Recommendations are provided for effective ABC implementation, emphasizing communication and addressing employee concerns. An alternative management accounting tool, Activity-Based Management (ABM), is suggested. The analysis draws upon academic sources to support its arguments and recommendations, providing a comprehensive evaluation of ABC's potential benefits for Lynas Corporation. This document is available on Desklib, a platform offering a wide range of study resources.

Activity based costing 1

ACTIVITY BASED COSTING

By (Student’s Name)

Professor’s Name

College

Course

Date

ACTIVITY BASED COSTING

By (Student’s Name)

Professor’s Name

College

Course

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity based costing 2

ACTIVITY BASED COSTING

Table of Contents

ACTIVITY BASED COSTING...........................................................................................................................1

Executive summary.....................................................................................................................................3

Introduction.................................................................................................................................................3

Explanation of Activity-based costing and its features................................................................................4

How Activity based costing aligns with strategies and goals of the Lynas Corporation...............................7

Mission and objective of the Lynas Corporation.....................................................................................7

Corporate strategies of the Lynas Corporation........................................................................................7

An explanation of how Activity-based costing enables Lynas Corporation to achieve its strategies.......8

Recommendations regarding the implementation of the Activity-based costing model for Lynas

Corporation.................................................................................................................................................9

Alternative management accounting tool appropriate for Lynas Corporation..........................................10

Conclusion.................................................................................................................................................10

References.................................................................................................................................................12

ACTIVITY BASED COSTING

Table of Contents

ACTIVITY BASED COSTING...........................................................................................................................1

Executive summary.....................................................................................................................................3

Introduction.................................................................................................................................................3

Explanation of Activity-based costing and its features................................................................................4

How Activity based costing aligns with strategies and goals of the Lynas Corporation...............................7

Mission and objective of the Lynas Corporation.....................................................................................7

Corporate strategies of the Lynas Corporation........................................................................................7

An explanation of how Activity-based costing enables Lynas Corporation to achieve its strategies.......8

Recommendations regarding the implementation of the Activity-based costing model for Lynas

Corporation.................................................................................................................................................9

Alternative management accounting tool appropriate for Lynas Corporation..........................................10

Conclusion.................................................................................................................................................10

References.................................................................................................................................................12

Activity based costing 3

Executive summary

The costs perform the essential role in the development of any corporations’

particularly in the sector of industrial. A suitable management accounting system of the

company should be consistent with the commitment of the corporate. The management should

also be able to perform its underlying activities by lead time, quality and cost. The paper look at

how the Lynas Corporation should implement the use of the Activity-based costing system to

enable more identifiable and accurate cost information appropriately. The primary focus of this

paper is to discuss in detail how the application of the Activity-based costing can help the Lynas

Corporation to improve its performance. It is also clear that the use of the ABC does not allow

for the improvements of processes or reduces the expenses of the organization. The

implementation of the ABC system into the organization only lays the foundation for the

advances of a process as well as refining information on cost. The paper also presents

appropriate recommendation that the management at Lynas Corporation should apply to

ensure effective implementation process. There is also an explanation of the best alternative

model that is capable of increasing the performance of the organization.

Introduction

Lynas Corporation is a mining Company that has gone through various changes for the

past few years. The business uses a significant amount of equity funding and debt in

establishing both the processing plant and mine, but the return on the investments was still

low. The production department of the organization was also unstable. This is because there

are high costs that are associated with particular activities that the organization performs. The

Executive summary

The costs perform the essential role in the development of any corporations’

particularly in the sector of industrial. A suitable management accounting system of the

company should be consistent with the commitment of the corporate. The management should

also be able to perform its underlying activities by lead time, quality and cost. The paper look at

how the Lynas Corporation should implement the use of the Activity-based costing system to

enable more identifiable and accurate cost information appropriately. The primary focus of this

paper is to discuss in detail how the application of the Activity-based costing can help the Lynas

Corporation to improve its performance. It is also clear that the use of the ABC does not allow

for the improvements of processes or reduces the expenses of the organization. The

implementation of the ABC system into the organization only lays the foundation for the

advances of a process as well as refining information on cost. The paper also presents

appropriate recommendation that the management at Lynas Corporation should apply to

ensure effective implementation process. There is also an explanation of the best alternative

model that is capable of increasing the performance of the organization.

Introduction

Lynas Corporation is a mining Company that has gone through various changes for the

past few years. The business uses a significant amount of equity funding and debt in

establishing both the processing plant and mine, but the return on the investments was still

low. The production department of the organization was also unstable. This is because there

are high costs that are associated with particular activities that the organization performs. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity based costing 4

current market price of its products also kept on fluctuating in the market. The organization

experiences all these changes because the organization’s ways of operation and corporate

structure were not in line with the modern market settings. Also, production and some of the

activities that the organization performs were hindered by legal challenges and operating

challenges. Therefore, to ensure that all the problems that face the organization are solved, the

management has to developed appropriate model that will help in resetting the cost base of

the Company as well as improving their functional performance while trading in the market.

The management should also ensure that the traditional strategic framework that is in place

support the financial house of the organization. Most of the issues that affect the Lynas

Corporation relate to decisions regarding allocation of costs to activities. I will advise the

management to implement and use the Activity-based costing model. This model will enable

the organization cut the operations cost and increase the efficiency of the business. All these

processes will ensure that there is the effective decision-making process in the organization. To

help explain how Activity-based costing will enhance the performance of the Lynas Corporation;

the paper is separated into different sections with each part narrates issues that deal with the

implementation process. There is an indication of accounting tool that can be used together

with the ABC to facilitate the performance of the organization.

Explanation of Activity-based costing and its features

ABC is the method of accounting that allocates costs to commodities, and the allocation

process depends on the resources that are used in the process of production. Kaplan and

Cooper introduced the concept of ABC system in the year of 1987. Activity-based costing is an

current market price of its products also kept on fluctuating in the market. The organization

experiences all these changes because the organization’s ways of operation and corporate

structure were not in line with the modern market settings. Also, production and some of the

activities that the organization performs were hindered by legal challenges and operating

challenges. Therefore, to ensure that all the problems that face the organization are solved, the

management has to developed appropriate model that will help in resetting the cost base of

the Company as well as improving their functional performance while trading in the market.

The management should also ensure that the traditional strategic framework that is in place

support the financial house of the organization. Most of the issues that affect the Lynas

Corporation relate to decisions regarding allocation of costs to activities. I will advise the

management to implement and use the Activity-based costing model. This model will enable

the organization cut the operations cost and increase the efficiency of the business. All these

processes will ensure that there is the effective decision-making process in the organization. To

help explain how Activity-based costing will enhance the performance of the Lynas Corporation;

the paper is separated into different sections with each part narrates issues that deal with the

implementation process. There is an indication of accounting tool that can be used together

with the ABC to facilitate the performance of the organization.

Explanation of Activity-based costing and its features

ABC is the method of accounting that allocates costs to commodities, and the allocation

process depends on the resources that are used in the process of production. Kaplan and

Cooper introduced the concept of ABC system in the year of 1987. Activity-based costing is an

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity based costing 5

approach that helps in the accurate allocation of overhead to the activities that use it (Taticchi,

Tonelli and Cagnazzo 2010). The use of the ABC brings about the improvement in performance

of all the organization. It causes an increase in the Organization’s financial performance

explicitly. This approach is mostly being used to assign costs to services and products which

depend on the resources and activities used. This approach uses cost drivers to apportion the

value of different commodities (services as well as products). Activity-based costing model not

only enhances the accuracy of various services and products, but it can also assist managers to

have a good understanding on how to use the unlimited resources through financial

performance, for example, the use of bottom line statement (BLI) and return on investment

(ROI). ABC is the approach that will provide the organization with the accurate method of

managing costs (Bauer et al. 2018). Activity-based costing uses innovative techniques to

measure values of business activities as well as processes to allow for the cost saving of the

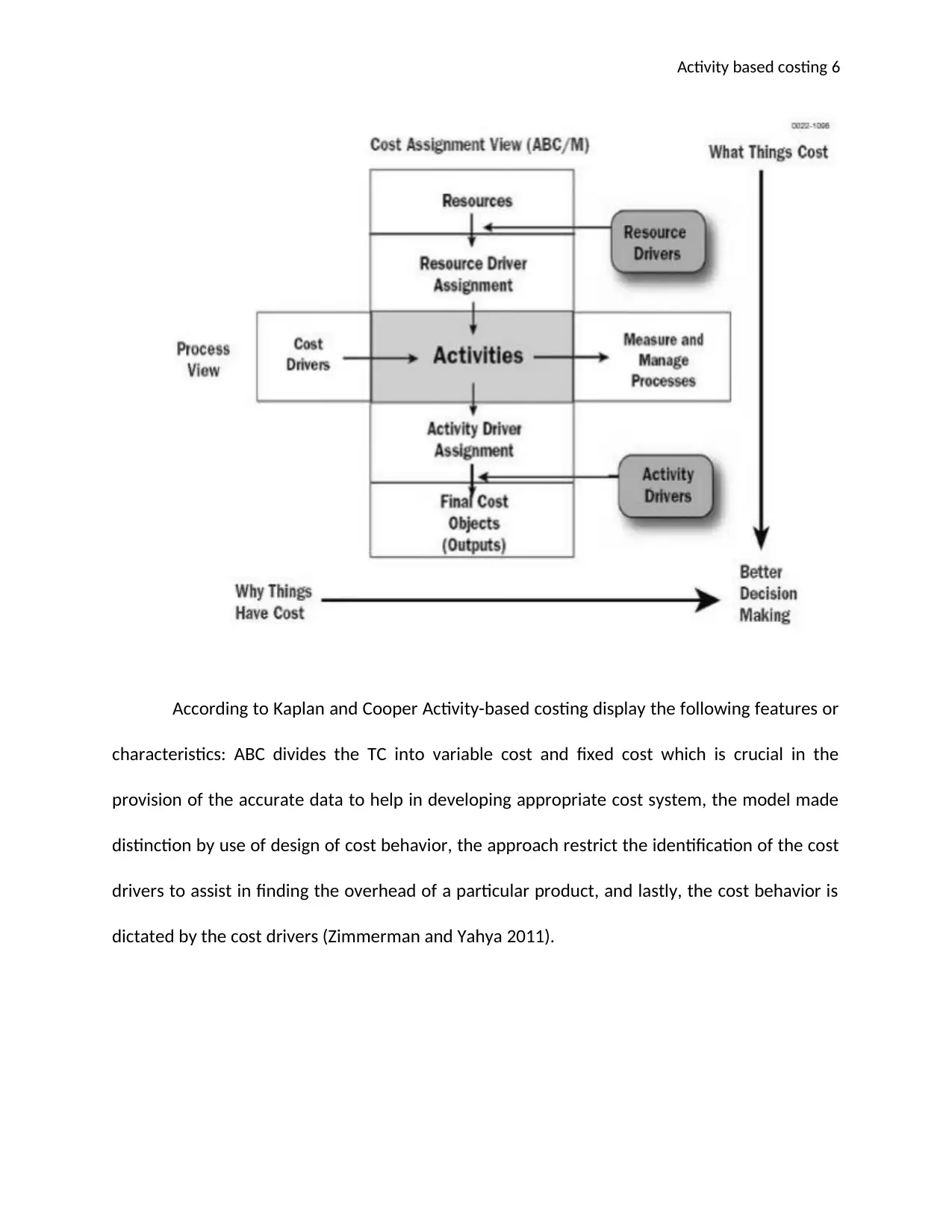

individual organizations as well as the overall supply chain. Activity-based costing can be viewed

in different ways. It can be considered to be in process view as well as cost assignment view.

The cost assignment view offers information on activities, cost object, and resources (Amid,

Ghodsypour and Brien 2011). The process view provides nonfinancial information about the

events that are for the business as well as the business process.

The figure below shows a representation of the two views

approach that helps in the accurate allocation of overhead to the activities that use it (Taticchi,

Tonelli and Cagnazzo 2010). The use of the ABC brings about the improvement in performance

of all the organization. It causes an increase in the Organization’s financial performance

explicitly. This approach is mostly being used to assign costs to services and products which

depend on the resources and activities used. This approach uses cost drivers to apportion the

value of different commodities (services as well as products). Activity-based costing model not

only enhances the accuracy of various services and products, but it can also assist managers to

have a good understanding on how to use the unlimited resources through financial

performance, for example, the use of bottom line statement (BLI) and return on investment

(ROI). ABC is the approach that will provide the organization with the accurate method of

managing costs (Bauer et al. 2018). Activity-based costing uses innovative techniques to

measure values of business activities as well as processes to allow for the cost saving of the

individual organizations as well as the overall supply chain. Activity-based costing can be viewed

in different ways. It can be considered to be in process view as well as cost assignment view.

The cost assignment view offers information on activities, cost object, and resources (Amid,

Ghodsypour and Brien 2011). The process view provides nonfinancial information about the

events that are for the business as well as the business process.

The figure below shows a representation of the two views

Activity based costing 6

According to Kaplan and Cooper Activity-based costing display the following features or

characteristics: ABC divides the TC into variable cost and fixed cost which is crucial in the

provision of the accurate data to help in developing appropriate cost system, the model made

distinction by use of design of cost behavior, the approach restrict the identification of the cost

drivers to assist in finding the overhead of a particular product, and lastly, the cost behavior is

dictated by the cost drivers (Zimmerman and Yahya 2011).

According to Kaplan and Cooper Activity-based costing display the following features or

characteristics: ABC divides the TC into variable cost and fixed cost which is crucial in the

provision of the accurate data to help in developing appropriate cost system, the model made

distinction by use of design of cost behavior, the approach restrict the identification of the cost

drivers to assist in finding the overhead of a particular product, and lastly, the cost behavior is

dictated by the cost drivers (Zimmerman and Yahya 2011).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity based costing 7

How Activity based costing aligns with strategies and goals of the Lynas

Corporation

Mission and objective of the Lynas Corporation

Lynas Corporation strives to be a universal leader in RE (Rare Earths) for a maintainable

future (Hellman and Duncan 2018). Lynas Corporation fulfills this by seeking for the workforce

and then meeting the requirements of their customers (Phua and Velu 2012). The company also

aims at investing in the communities where it operates as well as protecting the environments

where the operation of its activities takes place. The vision of the Lynas Corporation is to be the

best in the industry.

The main objectives of the company include: development and exploration of Rare

Earths deposits, The Company also aim at survey for other mineral resources, and designing,

planning as well as the construction of the plant in the western parts of Australia. Another

objective of the company is to facilitate the development of the modern processing plant to be

used in the distribution and production of REO (Rare Earth Oxide). The company has a goal of

committing zero damage in their workplace (Du and Graedel 2011).

Corporate strategies of the Lynas Corporation

Lynas Corporation has a policy of creating reliable, as well as becoming number one

supplier of Rare Earths in the market. The Company also focuses on growing the benchmark for

environmental standards and distributor of security in the global market. The company also

makes debt and structured agreement with its lenders (Meyer and Bras 2011). This kind of deal

will take the company to the next level. Lynas has a framework useful in concentrating

workforce, and this process will ensure that there is a rise in revenues and ensure profitability

How Activity based costing aligns with strategies and goals of the Lynas

Corporation

Mission and objective of the Lynas Corporation

Lynas Corporation strives to be a universal leader in RE (Rare Earths) for a maintainable

future (Hellman and Duncan 2018). Lynas Corporation fulfills this by seeking for the workforce

and then meeting the requirements of their customers (Phua and Velu 2012). The company also

aims at investing in the communities where it operates as well as protecting the environments

where the operation of its activities takes place. The vision of the Lynas Corporation is to be the

best in the industry.

The main objectives of the company include: development and exploration of Rare

Earths deposits, The Company also aim at survey for other mineral resources, and designing,

planning as well as the construction of the plant in the western parts of Australia. Another

objective of the company is to facilitate the development of the modern processing plant to be

used in the distribution and production of REO (Rare Earth Oxide). The company has a goal of

committing zero damage in their workplace (Du and Graedel 2011).

Corporate strategies of the Lynas Corporation

Lynas Corporation has a policy of creating reliable, as well as becoming number one

supplier of Rare Earths in the market. The Company also focuses on growing the benchmark for

environmental standards and distributor of security in the global market. The company also

makes debt and structured agreement with its lenders (Meyer and Bras 2011). This kind of deal

will take the company to the next level. Lynas has a framework useful in concentrating

workforce, and this process will ensure that there is a rise in revenues and ensure profitability

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity based costing 8

of the production. There is also diversity in the organization. This type of strategy provides that

the organization received varied experience to enrich the discussion process of different issues

in the organization (Long, Van Gosen, Foley and Cordier 2012).

An explanation of how Activity-based costing enables Lynas Corporation to

achieve its strategies

Lynas Corporation will depend on the inventive and strategic method of accounting as

used by the Activity-based costing to remain profitable in the competitive industry. This method

of cost accounting will enable the Company assess, analyze, evaluate and collect the overall

investing as well as spending habit, with the intention of informing the management of ways of

reducing the operational costs (Relich and Pawlewski 2018). The model will enable the Lynas

Corporation a good understanding of its values as well as the actual factors that initiatives these

costs. When both the employees and the Managers can identify the correct costs of activities,

they should then use them in the decision-making process. Due to the rising competition in the

market, the use of the model will assist the organization to improve or maintain their

competitiveness in the market through the use of information on costs that will always be

correct and accurate when the ABC model is used in the production process (Tavana, Yazdani

and Caprio 2017). The approach will enable the organization to use more suitable accounting

information (ABC) to control and planned its operations which will always reflect the actual

costs of the services as well as the product of the company. When the company employs the

use of the model, the costing system will provide accurate information which essential for

managing the decision is making (John, Cullen, Jülicher and Price 2018). ABC will assist the

Company to fulfill its target because the management will be able to increase its profit by

of the production. There is also diversity in the organization. This type of strategy provides that

the organization received varied experience to enrich the discussion process of different issues

in the organization (Long, Van Gosen, Foley and Cordier 2012).

An explanation of how Activity-based costing enables Lynas Corporation to

achieve its strategies

Lynas Corporation will depend on the inventive and strategic method of accounting as

used by the Activity-based costing to remain profitable in the competitive industry. This method

of cost accounting will enable the Company assess, analyze, evaluate and collect the overall

investing as well as spending habit, with the intention of informing the management of ways of

reducing the operational costs (Relich and Pawlewski 2018). The model will enable the Lynas

Corporation a good understanding of its values as well as the actual factors that initiatives these

costs. When both the employees and the Managers can identify the correct costs of activities,

they should then use them in the decision-making process. Due to the rising competition in the

market, the use of the model will assist the organization to improve or maintain their

competitiveness in the market through the use of information on costs that will always be

correct and accurate when the ABC model is used in the production process (Tavana, Yazdani

and Caprio 2017). The approach will enable the organization to use more suitable accounting

information (ABC) to control and planned its operations which will always reflect the actual

costs of the services as well as the product of the company. When the company employs the

use of the model, the costing system will provide accurate information which essential for

managing the decision is making (John, Cullen, Jülicher and Price 2018). ABC will assist the

Company to fulfill its target because the management will be able to increase its profit by

Activity based costing 9

saving the resources, time, and money of the business. This approach will significantly assist the

organization in this environment where Lynas Corporation operates costs is the significant

factor that the organization needs to consider during their daily operation. The use of the

approach will also enable the organization to improve its financial performance (Brogi et al.

2018). The adoption will help the Company in making precise cost analysis, thereby assisting in

the specification of constraints and reducing unnecessary costs. The technique will allow the

organization to enhance their work process and perform according to the ISO 9000. This will

give their customers enough confidence which then lead to increase profitability. The

customers will be sure of getting quality products (Ahmadi, Ghahramani, Becerik and Soibelman

2018).

Recommendations regarding the implementation of the Activity-based

costing model for Lynas Corporation

Effective communication is essential at all the departmental level of the organization.

The firm should ensure that it communicates the deficits of the costing system that they are

using, the effect of this alteration in the decision making by the management. The organization

should also explain how the new approach can be used to offer accurate information on costs

of particular activities in the organization. The organization should also state the effect of the

new model on the rewarding and valuation of all the employees. Because communication

involves getting feedback, the concerns of the employees should be addressed (Zhuang and

Chang 2017).

The management should also look at the issues of the people particularly the employees

that they will raise concerning the implementation of the Activity-based costing system as the

saving the resources, time, and money of the business. This approach will significantly assist the

organization in this environment where Lynas Corporation operates costs is the significant

factor that the organization needs to consider during their daily operation. The use of the

approach will also enable the organization to improve its financial performance (Brogi et al.

2018). The adoption will help the Company in making precise cost analysis, thereby assisting in

the specification of constraints and reducing unnecessary costs. The technique will allow the

organization to enhance their work process and perform according to the ISO 9000. This will

give their customers enough confidence which then lead to increase profitability. The

customers will be sure of getting quality products (Ahmadi, Ghahramani, Becerik and Soibelman

2018).

Recommendations regarding the implementation of the Activity-based

costing model for Lynas Corporation

Effective communication is essential at all the departmental level of the organization.

The firm should ensure that it communicates the deficits of the costing system that they are

using, the effect of this alteration in the decision making by the management. The organization

should also explain how the new approach can be used to offer accurate information on costs

of particular activities in the organization. The organization should also state the effect of the

new model on the rewarding and valuation of all the employees. Because communication

involves getting feedback, the concerns of the employees should be addressed (Zhuang and

Chang 2017).

The management should also look at the issues of the people particularly the employees

that they will raise concerning the implementation of the Activity-based costing system as the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity based costing 10

new costing system (Leahy et al. 2017). This may include looking into the issues that the

managers may forward that may prevent them from facilitating the changing process. It is also

essential for the organization to address the influence of the new model on compensation

system and measurement of performance. The existing performance metrics need to be

revised, or new one devised, based on the data collected during the activity-based costing

implementation (April and Murray 2017).

Alternative management accounting tool appropriate for Lynas

Corporation

The most suitable management tool that the Lynas Corporation should use instead of

the Activity-based costing is the Activity-based management. The organization can even use the

two management tool at the same time since the approaches work best together. ABC system

will perform the arithmetic of costs with the intention of providing precise cost information,

while the focus of activity-based management (ABM) will be on using the information provided

by the ABC system to manage different activities in the organization (Wang et al. 2018).

Conclusion

The implementation of the Activity-based costing can solve the challenges that the

Lynas Corporation are facing. The approach will provide precise cost information to the

management thereby improving the decision-making process. The paper also discusses some of

the advantages that ABC system will offer to the organization. Some of the benefits conferred

are the improvement of the decision-making process as well as increasing the profitability of

new costing system (Leahy et al. 2017). This may include looking into the issues that the

managers may forward that may prevent them from facilitating the changing process. It is also

essential for the organization to address the influence of the new model on compensation

system and measurement of performance. The existing performance metrics need to be

revised, or new one devised, based on the data collected during the activity-based costing

implementation (April and Murray 2017).

Alternative management accounting tool appropriate for Lynas

Corporation

The most suitable management tool that the Lynas Corporation should use instead of

the Activity-based costing is the Activity-based management. The organization can even use the

two management tool at the same time since the approaches work best together. ABC system

will perform the arithmetic of costs with the intention of providing precise cost information,

while the focus of activity-based management (ABM) will be on using the information provided

by the ABC system to manage different activities in the organization (Wang et al. 2018).

Conclusion

The implementation of the Activity-based costing can solve the challenges that the

Lynas Corporation are facing. The approach will provide precise cost information to the

management thereby improving the decision-making process. The paper also discusses some of

the advantages that ABC system will offer to the organization. Some of the benefits conferred

are the improvement of the decision-making process as well as increasing the profitability of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity based costing 11

the Company. Activity-based costing is more suitable for all the organization as it helps in the

allocation of activity costs.

the Company. Activity-based costing is more suitable for all the organization as it helps in the

allocation of activity costs.

Activity based costing 12

References

Ahmadi-Karvigh, S., Ghahramani, A., Becerik-Gerber, B. and Soibelman, L., 2018. Real-time

activity recognition for energy efficiency in buildings. Applied Energy, 211, pp.146-160.

Amid, A., Ghodsypour, S.H. and O’Brien, C., 2011. A weighted max–min model for fuzzy multi-

objective supplier selection in a supply chain. International Journal of Production

Economics, 131(1), pp.139-145.

April, M.D. and Murray, B.P., 2017. Cost effectiveness Analysis Appraisal and Application: An‐

Emergency Medicine Perspective. Academic Emergency Medicine, 24(6), pp.754-768.

Bauer-Nilsen, K., Hill, C., Trifiletti, D.M., Libby, B., Lash, D.H., Lain, M., Christodoulou, D., Hodge,

C. and Showalter, T.N., 2018. Evaluation of delivery costs for external beam radiation therapy

and brachytherapy for locally advanced cervical cancer using time-driven activity-based

costing. International Journal of Radiation Oncology• Biology• Physics, 100(1), pp.88-94.

Brogi, A., Danelutto, M., De Sensi, D., Ibrahim, A., Soldani, J. and Torquati, M., 2018. Analysing

Multiple QoS Attributes in Parallel Design Patterns-Based Applications. International Journal of

Parallel Programming, 46(1), pp.81-100.

References

Ahmadi-Karvigh, S., Ghahramani, A., Becerik-Gerber, B. and Soibelman, L., 2018. Real-time

activity recognition for energy efficiency in buildings. Applied Energy, 211, pp.146-160.

Amid, A., Ghodsypour, S.H. and O’Brien, C., 2011. A weighted max–min model for fuzzy multi-

objective supplier selection in a supply chain. International Journal of Production

Economics, 131(1), pp.139-145.

April, M.D. and Murray, B.P., 2017. Cost effectiveness Analysis Appraisal and Application: An‐

Emergency Medicine Perspective. Academic Emergency Medicine, 24(6), pp.754-768.

Bauer-Nilsen, K., Hill, C., Trifiletti, D.M., Libby, B., Lash, D.H., Lain, M., Christodoulou, D., Hodge,

C. and Showalter, T.N., 2018. Evaluation of delivery costs for external beam radiation therapy

and brachytherapy for locally advanced cervical cancer using time-driven activity-based

costing. International Journal of Radiation Oncology• Biology• Physics, 100(1), pp.88-94.

Brogi, A., Danelutto, M., De Sensi, D., Ibrahim, A., Soldani, J. and Torquati, M., 2018. Analysing

Multiple QoS Attributes in Parallel Design Patterns-Based Applications. International Journal of

Parallel Programming, 46(1), pp.81-100.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.