Evolution Mining: Activity-Based Costing (ABC) Implementation

VerifiedAdded on 2024/05/31

|9

|2290

|431

Report

AI Summary

This report provides an in-depth analysis of the Activity-Based Costing (ABC) method and its potential implementation within Evolution Mining Ltd, a gold mining firm operating in Australia and New Zealand. The report begins by introducing the ABC accounting method, highlighting its key features such as simplicity, cost-effectiveness, and comprehensive cost evaluation across functional departments. It then discusses Evolution Mining Ltd's objectives and mission, emphasizing the need for a more accurate costing system to track costs effectively and price products fairly. The report outlines the company's strategy to adopt the ABC system, detailing the steps involved in its implementation, including identifying activities, determining costs, and computing activity cost driver rates. Furthermore, the report explores alternative costing options for the company, such as job costing, and concludes by summarizing the potential benefits of ABC implementation for Evolution Mining Ltd, including improved cost management, profitability, and waste reduction. The document is available on Desklib, a platform offering a range of study tools and solved assignments for students.

ABC ACCOUNTING METHOD

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction......................................................................................................................................2

Objectives and Mission of the company..........................................................................................3

Strategy of the company..................................................................................................................3

Implementation of ABC Model.......................................................................................................3

Other options for the company........................................................................................................6

Conclusion.......................................................................................................................................6

Reference.........................................................................................................................................7

1

Introduction......................................................................................................................................2

Objectives and Mission of the company..........................................................................................3

Strategy of the company..................................................................................................................3

Implementation of ABC Model.......................................................................................................3

Other options for the company........................................................................................................6

Conclusion.......................................................................................................................................6

Reference.........................................................................................................................................7

1

Introduction

The ABC accounting method is the methodology of identifying the activities of a firm and then

assigning costs to them. This cost is also accompanied with the resource allocation to know the

cost of resources that come into play in the activities. The ABC method also shows the relevance

of each activity on the end result and the final output. The ABC method is mainly useful to

understand which activity has the most and least influence of the total production of goods and

services.

Evolution mining Ltd is essentially a gold mining firm. It was formed in the year 2011 by the

merger of Catalpa Resources Ltd and Conquest Mining Ltd. The firm of Evolution Mining Ltd

has a record of being consistent and reliable in their production and the cash cost guidance as

well. Evolution Mining Ltd is a firm that identifies, develops and then operates gold related

mining in Australia and New Zealand. The company operates a total of 6 gold mines. They also

deal with the mining of silver and copper along with the gold mining. They have their head

office in Sydney, Australia.

ABC model and its features

The ABC model of accounting identifies all the direct and indirect costs of all the activities that

are involved in the operations of the firm. For a perfect fit into the existing accounting system,

the ABC method needs to analyze the resources that are being utilized and the activities and their

associated costs.

The main features of the ABC model are many. It is a very simple method that can be

implemented with ease. It is one of the most cost effective methods of accounting as it analyzes

the activities being performed in the organization that will help in the development of the goods

and services. With the implementation of the ABC accounting method, all direct and indirect

costs that are related to the activities in all functional departments can be evaluated. This will

help the production and sales teams to understand the cost of resources that are needed for the

completion of the goods and services. The costs that get divided are done in tow categories,

namely

- Fixed costs

- Variable costs

2

The ABC accounting method is the methodology of identifying the activities of a firm and then

assigning costs to them. This cost is also accompanied with the resource allocation to know the

cost of resources that come into play in the activities. The ABC method also shows the relevance

of each activity on the end result and the final output. The ABC method is mainly useful to

understand which activity has the most and least influence of the total production of goods and

services.

Evolution mining Ltd is essentially a gold mining firm. It was formed in the year 2011 by the

merger of Catalpa Resources Ltd and Conquest Mining Ltd. The firm of Evolution Mining Ltd

has a record of being consistent and reliable in their production and the cash cost guidance as

well. Evolution Mining Ltd is a firm that identifies, develops and then operates gold related

mining in Australia and New Zealand. The company operates a total of 6 gold mines. They also

deal with the mining of silver and copper along with the gold mining. They have their head

office in Sydney, Australia.

ABC model and its features

The ABC model of accounting identifies all the direct and indirect costs of all the activities that

are involved in the operations of the firm. For a perfect fit into the existing accounting system,

the ABC method needs to analyze the resources that are being utilized and the activities and their

associated costs.

The main features of the ABC model are many. It is a very simple method that can be

implemented with ease. It is one of the most cost effective methods of accounting as it analyzes

the activities being performed in the organization that will help in the development of the goods

and services. With the implementation of the ABC accounting method, all direct and indirect

costs that are related to the activities in all functional departments can be evaluated. This will

help the production and sales teams to understand the cost of resources that are needed for the

completion of the goods and services. The costs that get divided are done in tow categories,

namely

- Fixed costs

- Variable costs

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The firm can analyze the behavior patterns in the costs of the resources that are required in the

activities of the firm. This method helps in providing a clear picture of the total cost of the

resources and activities all the way from the procurement to the delivery of finished goods to the

client. With this cost method in place, the management can see which activity has what

percentage of representation in the final product. Unlike the traditional costing methods in

accounting. The ABC method does not account for the man hours or machine hours that has been

used. It takes into account the activities that have been implemented for the various resources

(Chen, 2000).

Objectives and Mission of the company

The company is in the mining industry where the costing has been done on the basis of total

mined output to the total cost however this is inefficient process as different mineral takes

different time in mining hence the cost of mining is also different.

The objective and the mission of the company is to adapt a costing system that allow company to

track cost in a better manner there by allowing it to price the product fairly. If the cost of gold

mining is higher than cost of coal mining should not bear additional cost of gold mining.

Strategy of the company

The strategy adopted by the company is to use activity-based costing system. This costing

system will help company to track cost of each mined ore there by allowing it to price the same

in better way than that of traditional costing system. This is the best way forward for company

like Evolution as it allows it to have efficient pricing of many products.

Implementation of ABC Model

An activity-based cost bookkeeping framework underlines following over distribution. The part

of driver following is essentially extended by recognizing drivers disconnected to the volume of

item created (called non-unit-based activity drivers). The utilization of both unit-and non-unit-

based activity drivers expands the precision of cost assignments and the general quality and

importance of cost data. A cost bookkeeping framework that utilizations both unit-and non-unit-

based activity drivers to allot expenses to cost objects is called an activity-based cost (ABC)

framework.

3

activities of the firm. This method helps in providing a clear picture of the total cost of the

resources and activities all the way from the procurement to the delivery of finished goods to the

client. With this cost method in place, the management can see which activity has what

percentage of representation in the final product. Unlike the traditional costing methods in

accounting. The ABC method does not account for the man hours or machine hours that has been

used. It takes into account the activities that have been implemented for the various resources

(Chen, 2000).

Objectives and Mission of the company

The company is in the mining industry where the costing has been done on the basis of total

mined output to the total cost however this is inefficient process as different mineral takes

different time in mining hence the cost of mining is also different.

The objective and the mission of the company is to adapt a costing system that allow company to

track cost in a better manner there by allowing it to price the product fairly. If the cost of gold

mining is higher than cost of coal mining should not bear additional cost of gold mining.

Strategy of the company

The strategy adopted by the company is to use activity-based costing system. This costing

system will help company to track cost of each mined ore there by allowing it to price the same

in better way than that of traditional costing system. This is the best way forward for company

like Evolution as it allows it to have efficient pricing of many products.

Implementation of ABC Model

An activity-based cost bookkeeping framework underlines following over distribution. The part

of driver following is essentially extended by recognizing drivers disconnected to the volume of

item created (called non-unit-based activity drivers). The utilization of both unit-and non-unit-

based activity drivers expands the precision of cost assignments and the general quality and

importance of cost data. A cost bookkeeping framework that utilizations both unit-and non-unit-

based activity drivers to allot expenses to cost objects is called an activity-based cost (ABC)

framework.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity based administration is the essence of a contemporary operational control framework.

Activity based administration (ABM) centers around the administration of exercises with the

target of enhancing the esteem got by the client and the benefit got by the organization in giving

this esteem. It incorporates driver investigation, activity examination, and execution assessment

and draws on ABC as a noteworthy wellspring of data. Decide the exercises that go into creating

every item and the cost drivers for estimating them.

2. Decide the expenses related with every activity.

3. Decide the level of time workers spend on these exercises for every item - through meetings,

perception, or logs.

4. Compute activity cost driver rates.

5. Allot expenses to items or clients by isolating these activity costs by the yield of every

activity.

The principle reason for cost bookkeeping (rather than monetary bookkeeping) in administration

is to give information to supervisors. Administrators can utilize cost information to settle on

choices that will at last enhance the organization's money related execution. A considerable lot of

these choices identify with which items to publicize, which to extend, and which to cease.

Different choices endeavor to enhance tasks, bring down cost, or permit more aggressive

estimating. Since these choices depend vigorously on cost bookkeeping information, having

exact information are basic for an organization in recognizing wellsprings of benefit and

boosting potential productivity (Chaney, 2011).

As product offerings have turned out to be more mind boggling and advertises have turned out to

be more sectioned, organizations have grown more items for littler markets. Deals and benefits

for these business sectors are littler than for the already massed created items. This adjustment in

the aggressive condition has made the need for more precise costing data considerably more

grounded.

Activity based costing completes a superior employment of allotting overhead cost since it

doesn't aggregate costs that are spread out crosswise over a wide range of exercises. Pundits of

conventional cost bookkeeping frameworks contend that overhead costs are being designated

erroneously, prompting poor administration choices with respect to item continuation and

4

Activity based administration (ABM) centers around the administration of exercises with the

target of enhancing the esteem got by the client and the benefit got by the organization in giving

this esteem. It incorporates driver investigation, activity examination, and execution assessment

and draws on ABC as a noteworthy wellspring of data. Decide the exercises that go into creating

every item and the cost drivers for estimating them.

2. Decide the expenses related with every activity.

3. Decide the level of time workers spend on these exercises for every item - through meetings,

perception, or logs.

4. Compute activity cost driver rates.

5. Allot expenses to items or clients by isolating these activity costs by the yield of every

activity.

The principle reason for cost bookkeeping (rather than monetary bookkeeping) in administration

is to give information to supervisors. Administrators can utilize cost information to settle on

choices that will at last enhance the organization's money related execution. A considerable lot of

these choices identify with which items to publicize, which to extend, and which to cease.

Different choices endeavor to enhance tasks, bring down cost, or permit more aggressive

estimating. Since these choices depend vigorously on cost bookkeeping information, having

exact information are basic for an organization in recognizing wellsprings of benefit and

boosting potential productivity (Chaney, 2011).

As product offerings have turned out to be more mind boggling and advertises have turned out to

be more sectioned, organizations have grown more items for littler markets. Deals and benefits

for these business sectors are littler than for the already massed created items. This adjustment in

the aggressive condition has made the need for more precise costing data considerably more

grounded.

Activity based costing completes a superior employment of allotting overhead cost since it

doesn't aggregate costs that are spread out crosswise over a wide range of exercises. Pundits of

conventional cost bookkeeping frameworks contend that overhead costs are being designated

erroneously, prompting poor administration choices with respect to item continuation and

4

evaluating. In circumstances where an aggressive offer or cost-in addition to valuing is required,

the real cost of the item is basic for estimating of an item or administration. Choices in view of

mistaken cost information can directly affect the benefit of the organization in these

circumstances.

At the point when backhanded cost is a substantial bit of the general cost of the item, activity-

based costing is better than conventional costing in giving information to legitimate valuing

choices. In past decades, coordinate work has been around 25-half of the aggregate cost of an

item, yet since the 1960s, it has fallen drastically. The prevailing item cost is currently aberrant

cost.

Customary costing frameworks tend to utilize a solitary rate increased by a solitary factor to

decide the overhead designation for an item, administration, or task. This can prompt off base

costing, particularly when the incurrence of overhead cost isn't relative to that factor. In a

circumstance where a representative sets up a machine and gives it a chance to run while doing

other work, utilizing direct work as the factor for distributing overhead would prompt off base

costing. The machine hours, which are regularly overhead serious, are essentially disregarded,

while different exercises, gathering for instance, are charged high measures of overhead while

utilizing not very many assets separated from coordinate work. Utilizing a solitary rate for

allotting overhead in light of one factor will misallocate overhead in light of the fact that the

distinctive activities inside a solitary shop fluctuate generally. Overhead-serious ventures,

specifically, have a tendency to be underpriced (Boynton, 2009).

5

the real cost of the item is basic for estimating of an item or administration. Choices in view of

mistaken cost information can directly affect the benefit of the organization in these

circumstances.

At the point when backhanded cost is a substantial bit of the general cost of the item, activity-

based costing is better than conventional costing in giving information to legitimate valuing

choices. In past decades, coordinate work has been around 25-half of the aggregate cost of an

item, yet since the 1960s, it has fallen drastically. The prevailing item cost is currently aberrant

cost.

Customary costing frameworks tend to utilize a solitary rate increased by a solitary factor to

decide the overhead designation for an item, administration, or task. This can prompt off base

costing, particularly when the incurrence of overhead cost isn't relative to that factor. In a

circumstance where a representative sets up a machine and gives it a chance to run while doing

other work, utilizing direct work as the factor for distributing overhead would prompt off base

costing. The machine hours, which are regularly overhead serious, are essentially disregarded,

while different exercises, gathering for instance, are charged high measures of overhead while

utilizing not very many assets separated from coordinate work. Utilizing a solitary rate for

allotting overhead in light of one factor will misallocate overhead in light of the fact that the

distinctive activities inside a solitary shop fluctuate generally. Overhead-serious ventures,

specifically, have a tendency to be underpriced (Boynton, 2009).

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

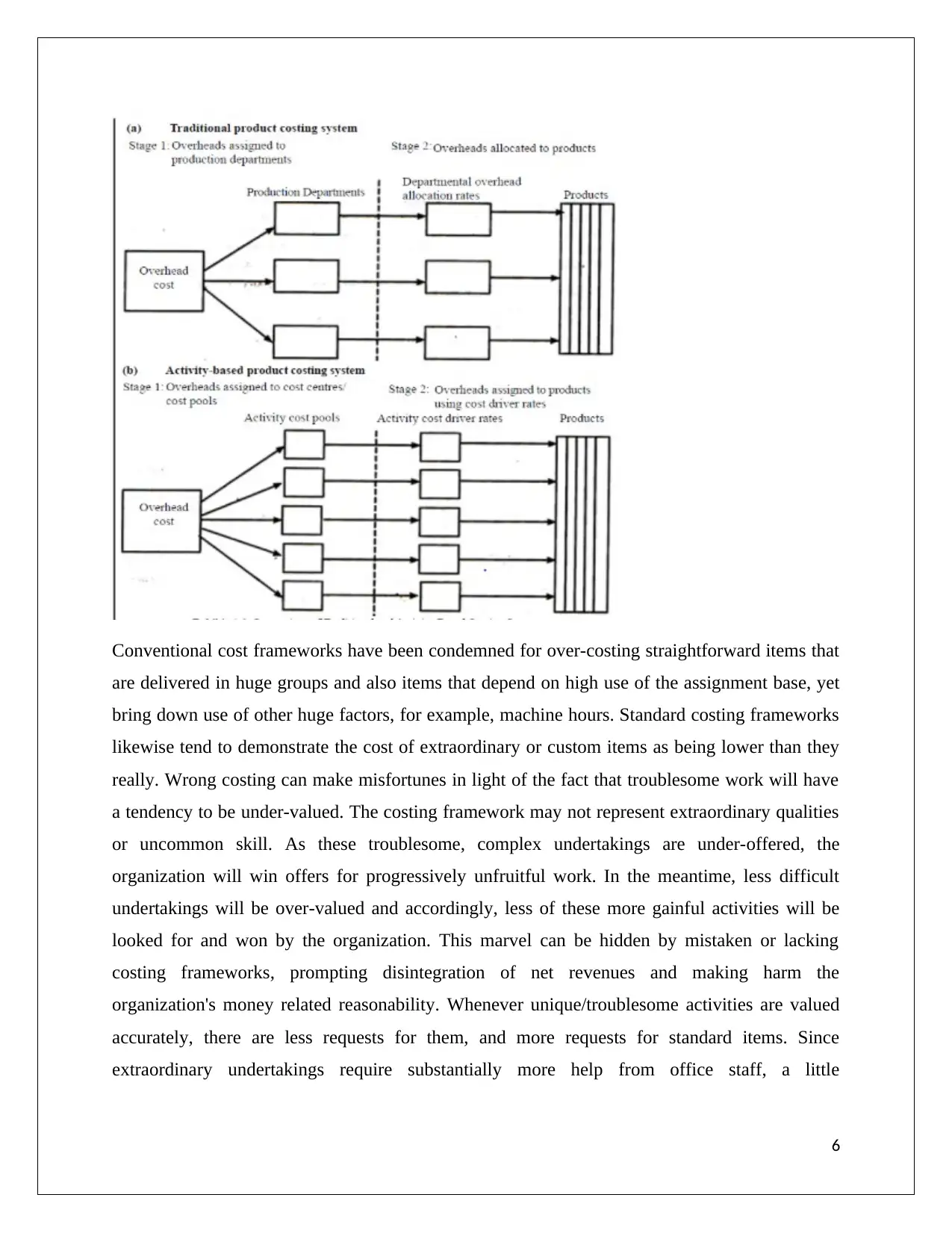

Conventional cost frameworks have been condemned for over-costing straightforward items that

are delivered in huge groups and also items that depend on high use of the assignment base, yet

bring down use of other huge factors, for example, machine hours. Standard costing frameworks

likewise tend to demonstrate the cost of extraordinary or custom items as being lower than they

really. Wrong costing can make misfortunes in light of the fact that troublesome work will have

a tendency to be under-valued. The costing framework may not represent extraordinary qualities

or uncommon skill. As these troublesome, complex undertakings are under-offered, the

organization will win offers for progressively unfruitful work. In the meantime, less difficult

undertakings will be over-valued and accordingly, less of these more gainful activities will be

looked for and won by the organization. This marvel can be hidden by mistaken or lacking

costing frameworks, prompting disintegration of net revenues and making harm the

organization's money related reasonability. Whenever unique/troublesome activities are valued

accurately, there are less requests for them, and more requests for standard items. Since

extraordinary undertakings require substantially more help from office staff, a little

6

are delivered in huge groups and also items that depend on high use of the assignment base, yet

bring down use of other huge factors, for example, machine hours. Standard costing frameworks

likewise tend to demonstrate the cost of extraordinary or custom items as being lower than they

really. Wrong costing can make misfortunes in light of the fact that troublesome work will have

a tendency to be under-valued. The costing framework may not represent extraordinary qualities

or uncommon skill. As these troublesome, complex undertakings are under-offered, the

organization will win offers for progressively unfruitful work. In the meantime, less difficult

undertakings will be over-valued and accordingly, less of these more gainful activities will be

looked for and won by the organization. This marvel can be hidden by mistaken or lacking

costing frameworks, prompting disintegration of net revenues and making harm the

organization's money related reasonability. Whenever unique/troublesome activities are valued

accurately, there are less requests for them, and more requests for standard items. Since

extraordinary undertakings require substantially more help from office staff, a little

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

diminishment in the level of unique requests versus the level of standard requests can

significantly affect the staff assets required for a similar level of request activity (Blouin, 2007).

Other options for the company

An approach for costing in which value of every 'employment' is resolved is known as job

Costing. Right here employment alludes to specific paintings or task or a settlement wherein the

work is finished via the client's guidelines and stipulations. The yield of every interest

accommodates commonly one or less of units. In this method, each hobby is taken into

consideration as an unmistakable substance, for which fee is decided. Occupation Costing is

connected while:

The execution of the employment is based on client's particular. Every one of the employments

heterogeneous in several regards and each activity requires isolating treatment. There is a

difference in WIP (paintings earlier), of each length.

Employment Costing is maximum suitable for the ventures wherein unique items are fabricated

in step with patron desires and requests. A few instances of those companies are fixtures, ship

constructing, Printing Press, interior decoration, and so on.

Conclusion

At the end evolution mining can be benefitted as:

1. Making doable unbiased and logical evaluating with the aid of diminishing charges of items

that utilisation fewer action assets and increment expenses of objects that burn up a greater

amount of the organisation's movement assets.

2. assisting institutions to offer a few incentives covered administrations or "exceptional ups"

to current gadgets on authentic fee acquired premise. Three. Killing unrewarding things from

the product presenting, alongside these strains increasing gainfulness without increasing prices, a

good opportunity in recessionary situations.

4. Killing the price of retaining up or going for walks non-gainful exercises, increasing the

preferred advantage.

5. enabling designation of assets to gainful things or things that use less assets.

7

significantly affect the staff assets required for a similar level of request activity (Blouin, 2007).

Other options for the company

An approach for costing in which value of every 'employment' is resolved is known as job

Costing. Right here employment alludes to specific paintings or task or a settlement wherein the

work is finished via the client's guidelines and stipulations. The yield of every interest

accommodates commonly one or less of units. In this method, each hobby is taken into

consideration as an unmistakable substance, for which fee is decided. Occupation Costing is

connected while:

The execution of the employment is based on client's particular. Every one of the employments

heterogeneous in several regards and each activity requires isolating treatment. There is a

difference in WIP (paintings earlier), of each length.

Employment Costing is maximum suitable for the ventures wherein unique items are fabricated

in step with patron desires and requests. A few instances of those companies are fixtures, ship

constructing, Printing Press, interior decoration, and so on.

Conclusion

At the end evolution mining can be benefitted as:

1. Making doable unbiased and logical evaluating with the aid of diminishing charges of items

that utilisation fewer action assets and increment expenses of objects that burn up a greater

amount of the organisation's movement assets.

2. assisting institutions to offer a few incentives covered administrations or "exceptional ups"

to current gadgets on authentic fee acquired premise. Three. Killing unrewarding things from

the product presenting, alongside these strains increasing gainfulness without increasing prices, a

good opportunity in recessionary situations.

4. Killing the price of retaining up or going for walks non-gainful exercises, increasing the

preferred advantage.

5. enabling designation of assets to gainful things or things that use less assets.

7

6. guaranteeing similarity with execution management scorecards by using uncovering

according to character dedication to the item value, and as a consequence, blessings.

7. Uncovering waste and wastefulness that provides to boosting efficiency.

8. recognizing and wiping out non-esteem which includes exercises, or sporting activities that do

not upload to the remaining estimation of the item or system. instances of non-esteem along with

exercises incorporate additional exams and replica paperwork.

Reference

Blouin, J., (2007). What can we learn about uncertain tax benefits from FIN 48? National Tax

Journal , 60 (3), 521-535.

Boynton, C., (2009). Earnings management and the corporate alternative minimum tax. Journal

of Accounting Research , 30 (Supplement), 131-153.

Bryant-Kutcher, L., (2007). Earnings persistence and the value of changes in firms'

effective tax rates. University of Oregon working paper.

Chaney, P., (2011). The effect of deferred taxes on security prices. Journal of Accounting,

Auditing and Finance , 9, 91-116.

Chen, K., (2000). The 1993 tax rate increase and deferred tax adjustments: a test of functional

fixation. Journal of Accounting Research , 38, 23-44.

8

according to character dedication to the item value, and as a consequence, blessings.

7. Uncovering waste and wastefulness that provides to boosting efficiency.

8. recognizing and wiping out non-esteem which includes exercises, or sporting activities that do

not upload to the remaining estimation of the item or system. instances of non-esteem along with

exercises incorporate additional exams and replica paperwork.

Reference

Blouin, J., (2007). What can we learn about uncertain tax benefits from FIN 48? National Tax

Journal , 60 (3), 521-535.

Boynton, C., (2009). Earnings management and the corporate alternative minimum tax. Journal

of Accounting Research , 30 (Supplement), 131-153.

Bryant-Kutcher, L., (2007). Earnings persistence and the value of changes in firms'

effective tax rates. University of Oregon working paper.

Chaney, P., (2011). The effect of deferred taxes on security prices. Journal of Accounting,

Auditing and Finance , 9, 91-116.

Chen, K., (2000). The 1993 tax rate increase and deferred tax adjustments: a test of functional

fixation. Journal of Accounting Research , 38, 23-44.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.