ABC Model Report: Corporate Social Responsibilities and Sustainability

VerifiedAdded on 2021/06/17

|22

|3832

|108

Report

AI Summary

This report examines the Activity Based Costing (ABC) model and its application to Mondeleze International. The introduction explains the purpose of cost systems and the significance of ABC. Part 2 delves into the ABC model, contrasting it with traditional costing methods, and detailing its advantages, such as providing accurate cost information for informed decision-making and identifying value-adding activities. It also addresses the model's limitations, like its complexity and high implementation costs. The report includes detailed examples of activity cost pools, allocation of overhead costs, and identification of cost drivers. Part 3 explores the social and environmental issues relevant to Mondeleze International, including digital information, sustainable development, raw material sourcing, and waste management. The report concludes with an analysis of the company's environmental and social indicators, outlining objectives, plans, and targets for sustainability and social responsibility. The report emphasizes the importance of aligning business practices with environmental and social considerations for long-term success.

Running Head: ACTIVITY BASED COSTING MODEL 0

Activity Based Model

Corporate Social responsibilities and Sustainability

Activity Based Model

Corporate Social responsibilities and Sustainability

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACTIVITY BASED COSTING MODEL 1

Table of Contents

Introduction................................................................................................................................2

Part 2..........................................................................................................................................2

Answer to question no-A........................................................................................................2

Answer to question no-B........................................................................................................5

Answer to question no-C........................................................................................................7

Answer to question no-D........................................................................................................9

Part-3..........................................................................................................................................9

Answer to question no-A........................................................................................................9

Answer to question no-B......................................................................................................10

Answer to question no-C......................................................................................................17

Answer to question no-D......................................................................................................18

Answer to question no-E......................................................................................................18

Answer to question no-F......................................................................................................19

Conclusion................................................................................................................................19

References................................................................................................................................20

Table of Contents

Introduction................................................................................................................................2

Part 2..........................................................................................................................................2

Answer to question no-A........................................................................................................2

Answer to question no-B........................................................................................................5

Answer to question no-C........................................................................................................7

Answer to question no-D........................................................................................................9

Part-3..........................................................................................................................................9

Answer to question no-A........................................................................................................9

Answer to question no-B......................................................................................................10

Answer to question no-C......................................................................................................17

Answer to question no-D......................................................................................................18

Answer to question no-E......................................................................................................18

Answer to question no-F......................................................................................................19

Conclusion................................................................................................................................19

References................................................................................................................................20

ACTIVITY BASED COSTING MODEL 2

Introduction

Cost systems are generally designed to provide the reliable information to the

managers, investors, suppliers to understand the mechanism of control and decision making.

Cost systems are generally designed to provide an insight on how particular objects consume

resources of the organisation. Every organisation has its own type of costing system and

cannot settle for a universal system.

Part 2

Answer to question no-A

Activity based costing system also known as ABC is a method of costing that

interprets the activities in an organisation and individual costs are assigned to each activity

with resources to all the products and services according to their actual consumption. Indirect

costs are assigned more into the direct costs in comparison to the traditional costing method.

According to Chartered Institute of Management Accounts ABC is an approach of managing

the costs. The activities are monitored, the resource consumption is traced and costs are

designed according to the final output (Anderson, Hesford, and Young, 2012).

The activity based cost method and the traditional costing method, both calculates the

overhead costs associated to the production and then the costs are assigned to the products on

the basis of cost driver rate. The major differences are lined up as follows

Particulars ABC COSTING CONVENTIONAL COSTING

POOLING OF

COST

The costs are accumulated into the

homogeneous activities. These activities

Under this method the costs are

accumulated either via plant-wide

Introduction

Cost systems are generally designed to provide the reliable information to the

managers, investors, suppliers to understand the mechanism of control and decision making.

Cost systems are generally designed to provide an insight on how particular objects consume

resources of the organisation. Every organisation has its own type of costing system and

cannot settle for a universal system.

Part 2

Answer to question no-A

Activity based costing system also known as ABC is a method of costing that

interprets the activities in an organisation and individual costs are assigned to each activity

with resources to all the products and services according to their actual consumption. Indirect

costs are assigned more into the direct costs in comparison to the traditional costing method.

According to Chartered Institute of Management Accounts ABC is an approach of managing

the costs. The activities are monitored, the resource consumption is traced and costs are

designed according to the final output (Anderson, Hesford, and Young, 2012).

The activity based cost method and the traditional costing method, both calculates the

overhead costs associated to the production and then the costs are assigned to the products on

the basis of cost driver rate. The major differences are lined up as follows

Particulars ABC COSTING CONVENTIONAL COSTING

POOLING OF

COST

The costs are accumulated into the

homogeneous activities. These activities

Under this method the costs are

accumulated either via plant-wide

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACTIVITY BASED COSTING MODEL 3

are also associated with the major

activities or processes.

method or through the departmental

cost method, where the cost is

driven by the heterogeneous factors

and are not determined by the

single key drivers.

Basis of

allocation

The costs are allocated to the specific

objects using the cost drivers.

With the help of volume based

allocation procedure the costs are

allocated.

Ranking of

costs

Not every cost is occurred during the

output therefore, costs are ranked on the

basis of non-linear accumulation

method (Anderson, Hesford, and

Young, 2012).

Generally under this method all the

costs are taken into consideration

which is driven by the volume or

the product.

Cost Objects The focus is mainly on evaluating the

costs of a variety of the objects

On the other hand under this

method the focus is very narrow

and revolves around the single

product.

Decision

Making

The information provided the ABC

model is more accurate and relevant in

nature. The procedure is easy to

understand and operate on to.

At times the costs are either

overvalued or undervalued which

ultimately results into the wrong

information and also becomes

are also associated with the major

activities or processes.

method or through the departmental

cost method, where the cost is

driven by the heterogeneous factors

and are not determined by the

single key drivers.

Basis of

allocation

The costs are allocated to the specific

objects using the cost drivers.

With the help of volume based

allocation procedure the costs are

allocated.

Ranking of

costs

Not every cost is occurred during the

output therefore, costs are ranked on the

basis of non-linear accumulation

method (Anderson, Hesford, and

Young, 2012).

Generally under this method all the

costs are taken into consideration

which is driven by the volume or

the product.

Cost Objects The focus is mainly on evaluating the

costs of a variety of the objects

On the other hand under this

method the focus is very narrow

and revolves around the single

product.

Decision

Making

The information provided the ABC

model is more accurate and relevant in

nature. The procedure is easy to

understand and operate on to.

At times the costs are either

overvalued or undervalued which

ultimately results into the wrong

information and also becomes

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACTIVITY BASED COSTING MODEL 4

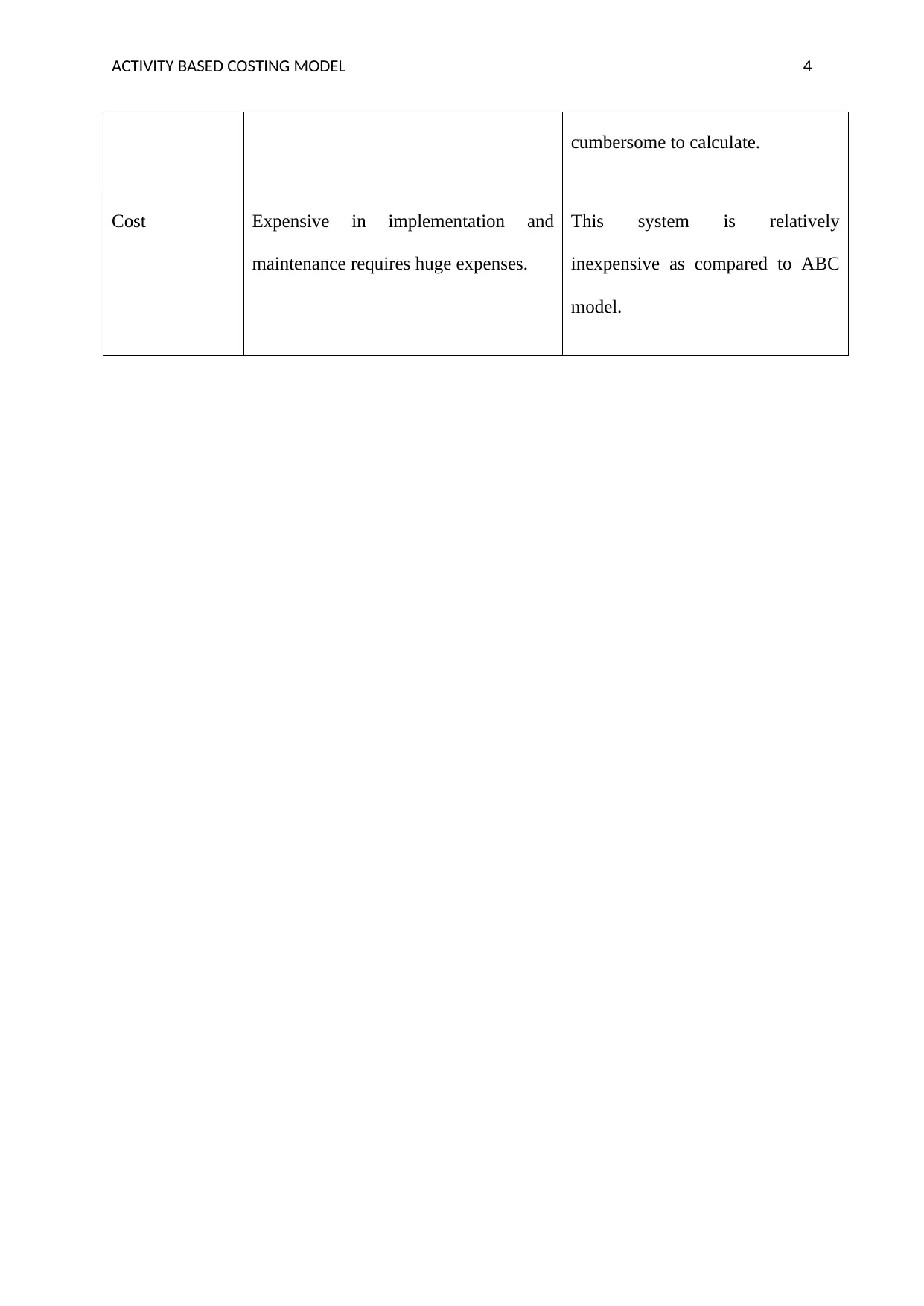

cumbersome to calculate.

Cost Expensive in implementation and

maintenance requires huge expenses.

This system is relatively

inexpensive as compared to ABC

model.

cumbersome to calculate.

Cost Expensive in implementation and

maintenance requires huge expenses.

This system is relatively

inexpensive as compared to ABC

model.

ACTIVITY BASED COSTING MODEL 5

Answer to question no-B.

One of the basic advantages of the ABC model is it provides reliable information

which helps in reducing the cost for prevailing opportunities available for Mondeleze

International. Due to the relevant information the managers are able to control many costs of

fixed nature. This happens because in the conventional method the costs were not visible

clearly whereas under this method the costs are more visible and clear.

Activity based costing system works only on the activities. Therefore, it will become

easy for the management of the Mondeleze International to decide quickly without

comprising on the quality front on each activity carefully. ABC helps in improving the

decision power of the company. ABC is also helpful in fixation of the selling prices as more

accurate data is available and a better understanding is developed. Due to this factor the

decision making process has become quite easy and sustainable (Tsai, 2016).

Further, the activities can be bifurcated into activities which add some value and

activities which do not add any kind of value or worth in general. The ABC model will help

the Mondeleze International Company to focus on the activities which creates force on value

adding activities. The ABC model though focuses on all the activities which are underlying to

trace more overheads (Hicks, 2012).

There are some costs which are categorised as non-manufacturing costs for example

advertising. Even though the advertising cost does not form the part of the major cost yet

contributes majorly in the business of Mondeleze International. With the help of the

advertising the company can reach at altogether new level. It can attract more number of

customers automatically.

Answer to question no-B.

One of the basic advantages of the ABC model is it provides reliable information

which helps in reducing the cost for prevailing opportunities available for Mondeleze

International. Due to the relevant information the managers are able to control many costs of

fixed nature. This happens because in the conventional method the costs were not visible

clearly whereas under this method the costs are more visible and clear.

Activity based costing system works only on the activities. Therefore, it will become

easy for the management of the Mondeleze International to decide quickly without

comprising on the quality front on each activity carefully. ABC helps in improving the

decision power of the company. ABC is also helpful in fixation of the selling prices as more

accurate data is available and a better understanding is developed. Due to this factor the

decision making process has become quite easy and sustainable (Tsai, 2016).

Further, the activities can be bifurcated into activities which add some value and

activities which do not add any kind of value or worth in general. The ABC model will help

the Mondeleze International Company to focus on the activities which creates force on value

adding activities. The ABC model though focuses on all the activities which are underlying to

trace more overheads (Hicks, 2012).

There are some costs which are categorised as non-manufacturing costs for example

advertising. Even though the advertising cost does not form the part of the major cost yet

contributes majorly in the business of Mondeleze International. With the help of the

advertising the company can reach at altogether new level. It can attract more number of

customers automatically.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACTIVITY BASED COSTING MODEL 6

The cost of allocation if done accurately, leads to proper pricing policy. Therefore

with the help of proper pricing policy the company can maintain the additional products

which may also leads to profit. It has been recognized that the costs are created by activities

more than the products. In an environment where the advanced manufacturing takes place

and the support functions are forming the major portion of the cost ABC model of Mondeleze

can provide more realistic costs (Innes, and Mitchell, 2015).

The statement of expenditure is prepared on the basis of the activities and the cost of

every activity is compared amongst other to find out the variances if any. If there are any

variances proper steps are undertaken to ensure on going stability of the process.

Having analysed the positive effects of the ABC model there are some negative

effects as well.

Since ABC has a numerous cost pools and a range of drivers of cost it becomes

complex to implement in comparison to the traditional product costing systems. It involves a

high amount of expenditure to implement and maintain the model for a long period of time.

Therefore, Mondeleze can cease to work if the on-going process becomes cumbersome.

Mondeleze International faces certain difficulties like cost selection, apportionment of the

common costs and lastly varying cost driver’s rates.

One of the biggest disadvantages is the complex measurements that need to be taken

to implement the same model practically. ABC requires proper management system to

evaluate the costs of the activity pools and to identify the best possible measure to act as a

driver for the purpose of the allocation (Anderson, Hesford, and Young, 2012).

If in later stage Mondeleze is left with only one product in the market than the ABC

model will be redundant and will not be relatively useful. Therefore corrective measures shall

The cost of allocation if done accurately, leads to proper pricing policy. Therefore

with the help of proper pricing policy the company can maintain the additional products

which may also leads to profit. It has been recognized that the costs are created by activities

more than the products. In an environment where the advanced manufacturing takes place

and the support functions are forming the major portion of the cost ABC model of Mondeleze

can provide more realistic costs (Innes, and Mitchell, 2015).

The statement of expenditure is prepared on the basis of the activities and the cost of

every activity is compared amongst other to find out the variances if any. If there are any

variances proper steps are undertaken to ensure on going stability of the process.

Having analysed the positive effects of the ABC model there are some negative

effects as well.

Since ABC has a numerous cost pools and a range of drivers of cost it becomes

complex to implement in comparison to the traditional product costing systems. It involves a

high amount of expenditure to implement and maintain the model for a long period of time.

Therefore, Mondeleze can cease to work if the on-going process becomes cumbersome.

Mondeleze International faces certain difficulties like cost selection, apportionment of the

common costs and lastly varying cost driver’s rates.

One of the biggest disadvantages is the complex measurements that need to be taken

to implement the same model practically. ABC requires proper management system to

evaluate the costs of the activity pools and to identify the best possible measure to act as a

driver for the purpose of the allocation (Anderson, Hesford, and Young, 2012).

If in later stage Mondeleze is left with only one product in the market than the ABC

model will be redundant and will not be relatively useful. Therefore corrective measures shall

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACTIVITY BASED COSTING MODEL 7

be taken by the company to avoid the effects of limitations to a certain extent (Jung, and

Choi, 2009).

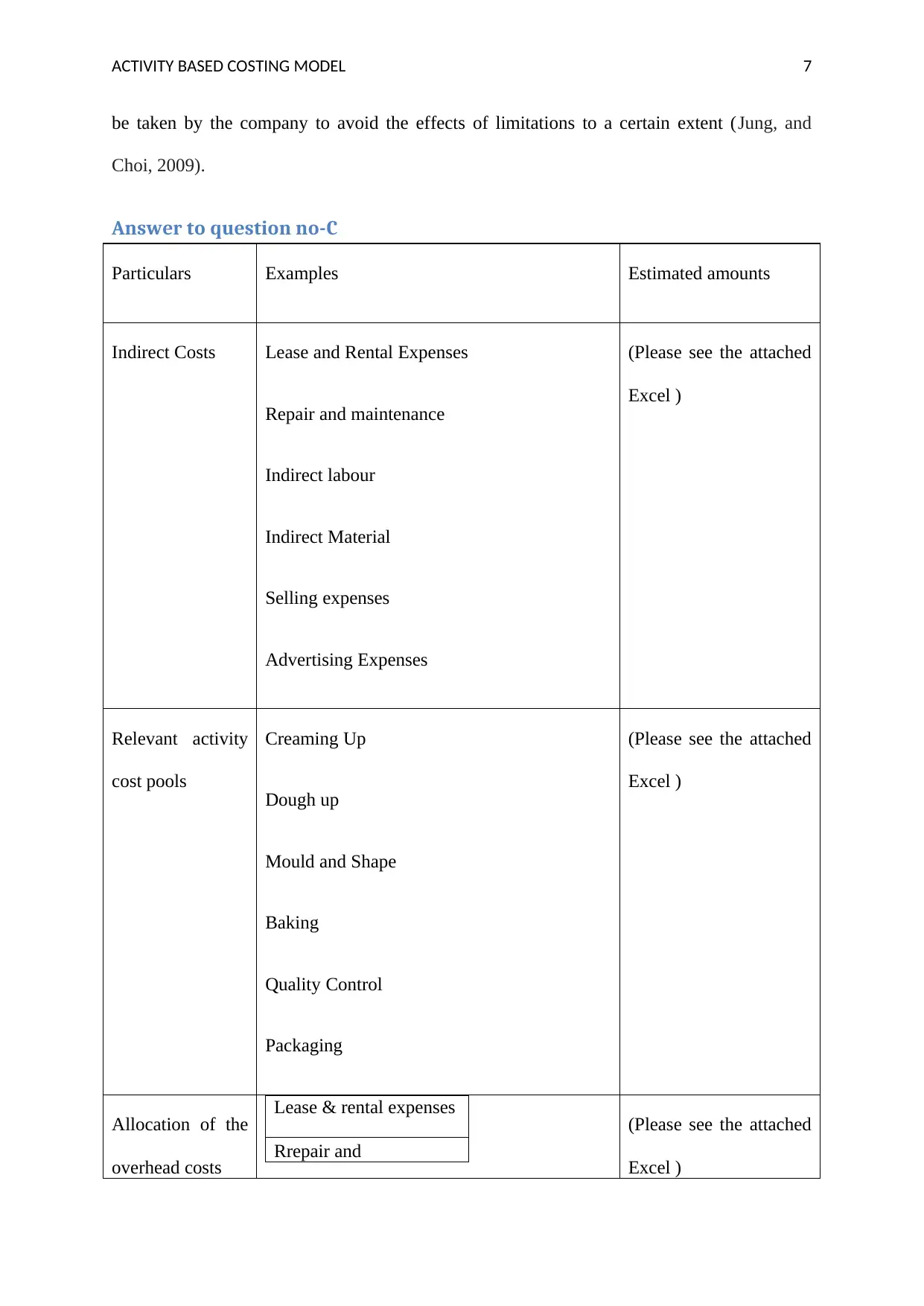

Answer to question no-C

Particulars Examples Estimated amounts

Indirect Costs Lease and Rental Expenses

Repair and maintenance

Indirect labour

Indirect Material

Selling expenses

Advertising Expenses

(Please see the attached

Excel )

Relevant activity

cost pools

Creaming Up

Dough up

Mould and Shape

Baking

Quality Control

Packaging

(Please see the attached

Excel )

Allocation of the

overhead costs

Lease & rental expenses

Rrepair and

(Please see the attached

Excel )

be taken by the company to avoid the effects of limitations to a certain extent (Jung, and

Choi, 2009).

Answer to question no-C

Particulars Examples Estimated amounts

Indirect Costs Lease and Rental Expenses

Repair and maintenance

Indirect labour

Indirect Material

Selling expenses

Advertising Expenses

(Please see the attached

Excel )

Relevant activity

cost pools

Creaming Up

Dough up

Mould and Shape

Baking

Quality Control

Packaging

(Please see the attached

Excel )

Allocation of the

overhead costs

Lease & rental expenses

Rrepair and

(Please see the attached

Excel )

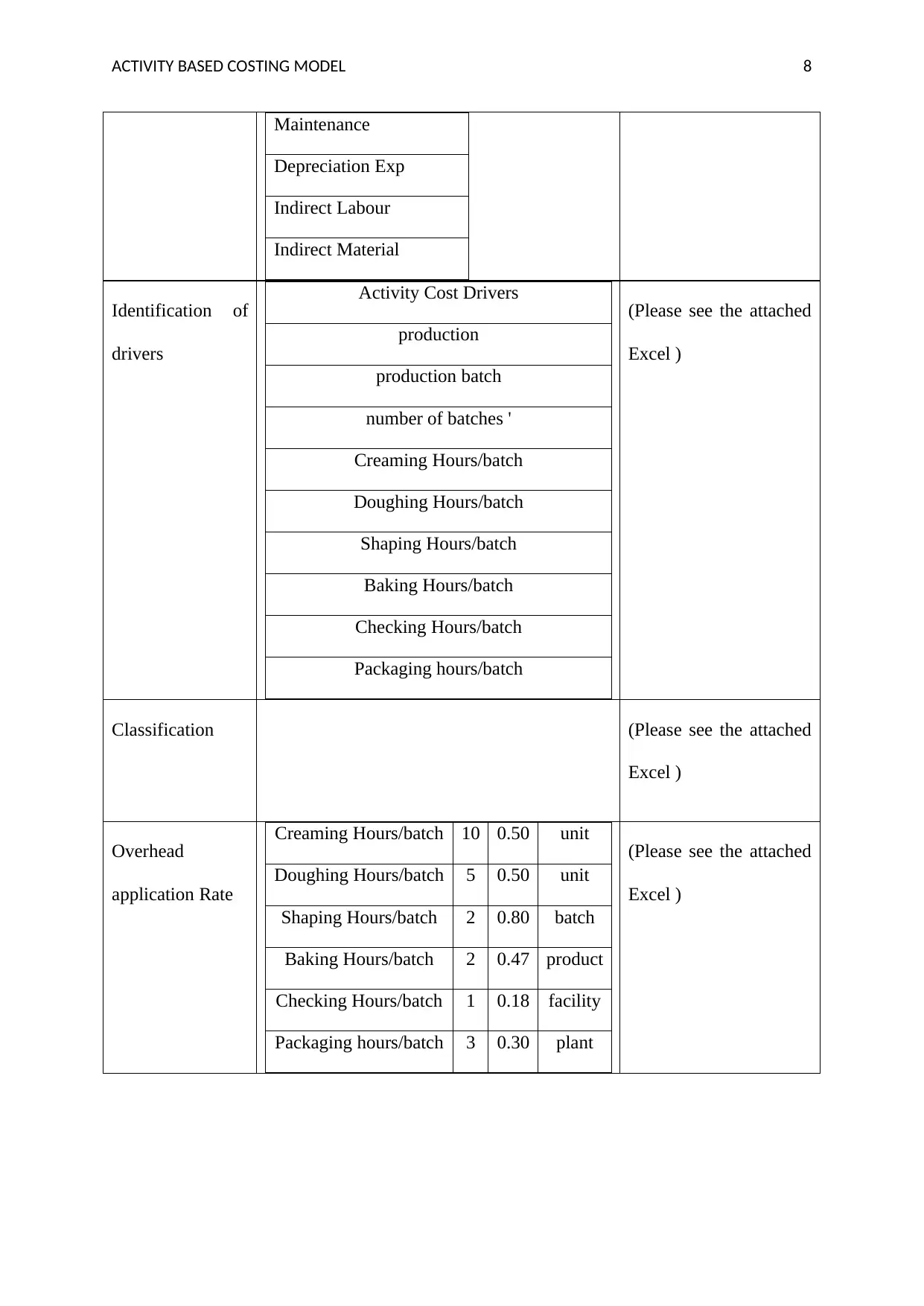

ACTIVITY BASED COSTING MODEL 8

Maintenance

Depreciation Exp

Indirect Labour

Indirect Material

Identification of

drivers

Activity Cost Drivers

production

production batch

number of batches '

Creaming Hours/batch

Doughing Hours/batch

Shaping Hours/batch

Baking Hours/batch

Checking Hours/batch

Packaging hours/batch

(Please see the attached

Excel )

Classification (Please see the attached

Excel )

Overhead

application Rate

Creaming Hours/batch 10 0.50 unit

Doughing Hours/batch 5 0.50 unit

Shaping Hours/batch 2 0.80 batch

Baking Hours/batch 2 0.47 product

Checking Hours/batch 1 0.18 facility

Packaging hours/batch 3 0.30 plant

(Please see the attached

Excel )

Maintenance

Depreciation Exp

Indirect Labour

Indirect Material

Identification of

drivers

Activity Cost Drivers

production

production batch

number of batches '

Creaming Hours/batch

Doughing Hours/batch

Shaping Hours/batch

Baking Hours/batch

Checking Hours/batch

Packaging hours/batch

(Please see the attached

Excel )

Classification (Please see the attached

Excel )

Overhead

application Rate

Creaming Hours/batch 10 0.50 unit

Doughing Hours/batch 5 0.50 unit

Shaping Hours/batch 2 0.80 batch

Baking Hours/batch 2 0.47 product

Checking Hours/batch 1 0.18 facility

Packaging hours/batch 3 0.30 plant

(Please see the attached

Excel )

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACTIVITY BASED COSTING MODEL 9

Answer to question no-D

The indirect costs like lease and rental payments, depreciation, repair and

maintenance, indirect labour and material of Mondeleze International have been allocated

using the activity cost drivers which have been discussed above. The costs which are publicly

available are cost to employees, cost of indirect material or indirect labour. Whereas there are

some costs which are meant to be assumed. The overhead costs are calculated on the basis of

the overhead rates and further the classification is done on the basis of corporate level

activity, plant margin, product margin or unit margin to understand the activities individually.

This cost hierarchy is important to determine the activity cost analysis.

Part-3

Answer to question no-A

SOCIAL AND ENVIRONMENTAL ISSUES

In the article published in economic times on 3rd May 2018, the paper talked about

how Mondeleze International, the company behind the Cadbury milk and Oreo cookies was

able to generate double the Revenue at the end of the March quarter. The company posted a

5% global increase in the volumes of sales. It is said to be reported to have sold more cookies

and chocolates than expected. Considering the above article the major social issues that are

important are as follow (Jung, and Choi, 2009).

Digital and Social Information: The biggest challenge for the company is to promote

the product through social media front. The food industry runs on the basis of advertising of

the products Ethical and social issues are raised only to improve the existing food production

procedure. It is the responsibility of the company to deliver the right information about the

Answer to question no-D

The indirect costs like lease and rental payments, depreciation, repair and

maintenance, indirect labour and material of Mondeleze International have been allocated

using the activity cost drivers which have been discussed above. The costs which are publicly

available are cost to employees, cost of indirect material or indirect labour. Whereas there are

some costs which are meant to be assumed. The overhead costs are calculated on the basis of

the overhead rates and further the classification is done on the basis of corporate level

activity, plant margin, product margin or unit margin to understand the activities individually.

This cost hierarchy is important to determine the activity cost analysis.

Part-3

Answer to question no-A

SOCIAL AND ENVIRONMENTAL ISSUES

In the article published in economic times on 3rd May 2018, the paper talked about

how Mondeleze International, the company behind the Cadbury milk and Oreo cookies was

able to generate double the Revenue at the end of the March quarter. The company posted a

5% global increase in the volumes of sales. It is said to be reported to have sold more cookies

and chocolates than expected. Considering the above article the major social issues that are

important are as follow (Jung, and Choi, 2009).

Digital and Social Information: The biggest challenge for the company is to promote

the product through social media front. The food industry runs on the basis of advertising of

the products Ethical and social issues are raised only to improve the existing food production

procedure. It is the responsibility of the company to deliver the right information about the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACTIVITY BASED COSTING MODEL 10

product to its customers. The customers are also quality conscious and therefore they value

the money in terms of worth of the product. Hence it is important to nurture the digital and

information sector to ultimately grow the business to a next level (Jung, and Choi, 2009).

Sustainable development the second major social issue is the stability of the product. The

concept of stability covers a wide range of aspects. Stability can be a grey area but it can also

come up with benefits. Stability decides the market share of the company and the ability to

stay among the competitors (Tsai, 2016).

The major environmental issues that are important are natural and Industrial

environment at times do not coincide with each other. There are certain factors which play an

important role in determining the environmental issues. The first is the undesirable

component in the raw materials to increase the production level and quantity of the product

can be a major issue. Next are the additives and preservatives used in the processing and

preservation which may create the adverse impact on the heath of the users. The emission of

waste effluents from the processing plants which can create several diseases and have a worse

impact on the health. The forces of demand and supply also play a pivotal role in the category

of the environmental factors. The company has to adjust its strength and weaknesses

according to the opportunities and threats present in the environment. Therefore both the

factors are reasonably important to determine the position and overall working of the

Mondelze International (Hicks, 2012).

Answer to question no-B

Column1 Particulars Objective Plan Target

Sr no.

Environmental

Indicators

product to its customers. The customers are also quality conscious and therefore they value

the money in terms of worth of the product. Hence it is important to nurture the digital and

information sector to ultimately grow the business to a next level (Jung, and Choi, 2009).

Sustainable development the second major social issue is the stability of the product. The

concept of stability covers a wide range of aspects. Stability can be a grey area but it can also

come up with benefits. Stability decides the market share of the company and the ability to

stay among the competitors (Tsai, 2016).

The major environmental issues that are important are natural and Industrial

environment at times do not coincide with each other. There are certain factors which play an

important role in determining the environmental issues. The first is the undesirable

component in the raw materials to increase the production level and quantity of the product

can be a major issue. Next are the additives and preservatives used in the processing and

preservation which may create the adverse impact on the heath of the users. The emission of

waste effluents from the processing plants which can create several diseases and have a worse

impact on the health. The forces of demand and supply also play a pivotal role in the category

of the environmental factors. The company has to adjust its strength and weaknesses

according to the opportunities and threats present in the environment. Therefore both the

factors are reasonably important to determine the position and overall working of the

Mondelze International (Hicks, 2012).

Answer to question no-B

Column1 Particulars Objective Plan Target

Sr no.

Environmental

Indicators

ACTIVITY BASED COSTING MODEL 11

1

Packaging Quality To assess new

packaging

designs, to drive

less material

Reduction in

energy and

greenhouse

gases.

By

eliminating

the shipper

box during

packaging,

By reducing

the number

of pouches

and

cardboard

consumption

is set at low.

Lastly by

replacing the

Oreo cookie

tray with the

film wrap.

To exceed by

78% in

overall

market.

2

Water Generation To reduce the

wastage of

water through

factories up to

30%.

By making

aware about

the

importance

of water

reuse and

process

systems

Additional

reduction of

water

consumption

in the

manufacturin

g plants by

15%

1

Packaging Quality To assess new

packaging

designs, to drive

less material

Reduction in

energy and

greenhouse

gases.

By

eliminating

the shipper

box during

packaging,

By reducing

the number

of pouches

and

cardboard

consumption

is set at low.

Lastly by

replacing the

Oreo cookie

tray with the

film wrap.

To exceed by

78% in

overall

market.

2

Water Generation To reduce the

wastage of

water through

factories up to

30%.

By making

aware about

the

importance

of water

reuse and

process

systems

Additional

reduction of

water

consumption

in the

manufacturin

g plants by

15%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.