Applying Activity-Based Costing to MYOB Group Ltd: A Financial Report

VerifiedAdded on 2021/05/31

|11

|2552

|29

Report

AI Summary

This report provides a comprehensive analysis of Activity-Based Costing (ABC) and its application to MYOB Group Ltd, a technology company providing software solutions. The report begins with an introduction to ABC, explaining its use in resource utilization and efficiency, particularly in manufacturing, and its applicability to the service industry. The study examines MYOB's mission, objectives, and strategies, including increasing market growth and penetration. It details how the ABC model assists in achieving these strategies by assessing indirect costs and identifying cost drivers. The report includes financial data, recommendations for adopting ABC, and a discussion of another management accounting tool, Life Cycle Costing. The conclusion emphasizes the benefits of ABC for MYOB's future growth and effective resource utilization.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction......................................................................................................................................4

Activity based Cost Model..............................................................................................................5

ABC Model in accordance with the goals and strategies of MYOB Group Ltd. Mission and

objective of MYOB Group Limited................................................................................................6

Recommendations-..........................................................................................................................9

Another Management Accounting Tool suitable for the use of MYOB Group Ltd......................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

2

Introduction......................................................................................................................................4

Activity based Cost Model..............................................................................................................5

ABC Model in accordance with the goals and strategies of MYOB Group Ltd. Mission and

objective of MYOB Group Limited................................................................................................6

Recommendations-..........................................................................................................................9

Another Management Accounting Tool suitable for the use of MYOB Group Ltd......................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

2

Introduction

Activity-based costing is a technique that has been widely used by many businesses in

order to find out the actual utilization of resources, It is mostly used in the manufacturing

businesses. It has been proved as very beneficial in increasing the efficiency of the business. It

deals with the utilization of the resources in the production activities. It can give good results in

service industry too if it is applicable in an efficient way. Below study is based on an

organization named MYOB Group Ltd. It is a big Australia based multinational company and it

belongs to the technology industry. This company is involved in providing software-related

services to small, mid-size as well as big companies. It provides different software that helps in

business management like management of payroll, payments, retail, tax solutions and CRM.

There are different benefits of ABC model that has been described in the below study. It

provides benefits by assessing the vision, mission, objectives and strategies of MYOB. It also

provides some recommendations for the benefit of the organization.

3

Activity-based costing is a technique that has been widely used by many businesses in

order to find out the actual utilization of resources, It is mostly used in the manufacturing

businesses. It has been proved as very beneficial in increasing the efficiency of the business. It

deals with the utilization of the resources in the production activities. It can give good results in

service industry too if it is applicable in an efficient way. Below study is based on an

organization named MYOB Group Ltd. It is a big Australia based multinational company and it

belongs to the technology industry. This company is involved in providing software-related

services to small, mid-size as well as big companies. It provides different software that helps in

business management like management of payroll, payments, retail, tax solutions and CRM.

There are different benefits of ABC model that has been described in the below study. It

provides benefits by assessing the vision, mission, objectives and strategies of MYOB. It also

provides some recommendations for the benefit of the organization.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity-based Cost Model

ABC costing refers to Activity-based costing. It basically deals with costing of different

things in a production process. It basically helps in keep a tracking of resources used and the cost

of the production. There are different activities involved in the production process and a

particular cost is assigned to each of them. This costing has been widely used in calculating all

the overhead expenses and the cost to the extent of revenue. It starts with identifying the

activities involved in the business and then allocates a cost and resources to each of them. It

assists in the initiation of activity to produce the outputs. The effective cost that has been utilized

in the production process in a particular time period is known as activity cost. It basically deals

with indirect costs. ABC costing only works when the model is totally based on the business

activities and the cost involved in the same. These costs are incurred in the manufacturing or

production process of goods or services. It is necessary to find out the estimation of the funds

requires in production activities, so this model is perfectly suitable for the same (Wink and

Corradino, 2011).

Features of Activity-based costing

There are mainly two types of cost involved in the business activities according to

activity-based costing. These two costs are fixed costs and variable costs. Fixed costs are the cost

that remains fixed irrespective of the units of production and it is incurred on a fixed basis for a

particular business. Even if there is no production activities are going on, this fixed cost will

remain the same. E.g. Rent, electricity bill and wages of labour. Variable cost is a cost that

totally depends upon the production activities and a number of units produced. This cost varies

according to the production activities like maintenance cost and diversification costs. This cost

helps in the improvement of the quality of the products as well as the design of the product

(Mohamed EL-Shishini and Upadhyaya, 2018).

It helps in the identification of cost drivers for each type of activity. A cost driver is a part

of the activity that utilizes the maximum cost in the manufacturing process. This model provides

a tracking support for the cost involved in the activities that are very beneficial for the business

4

ABC costing refers to Activity-based costing. It basically deals with costing of different

things in a production process. It basically helps in keep a tracking of resources used and the cost

of the production. There are different activities involved in the production process and a

particular cost is assigned to each of them. This costing has been widely used in calculating all

the overhead expenses and the cost to the extent of revenue. It starts with identifying the

activities involved in the business and then allocates a cost and resources to each of them. It

assists in the initiation of activity to produce the outputs. The effective cost that has been utilized

in the production process in a particular time period is known as activity cost. It basically deals

with indirect costs. ABC costing only works when the model is totally based on the business

activities and the cost involved in the same. These costs are incurred in the manufacturing or

production process of goods or services. It is necessary to find out the estimation of the funds

requires in production activities, so this model is perfectly suitable for the same (Wink and

Corradino, 2011).

Features of Activity-based costing

There are mainly two types of cost involved in the business activities according to

activity-based costing. These two costs are fixed costs and variable costs. Fixed costs are the cost

that remains fixed irrespective of the units of production and it is incurred on a fixed basis for a

particular business. Even if there is no production activities are going on, this fixed cost will

remain the same. E.g. Rent, electricity bill and wages of labour. Variable cost is a cost that

totally depends upon the production activities and a number of units produced. This cost varies

according to the production activities like maintenance cost and diversification costs. This cost

helps in the improvement of the quality of the products as well as the design of the product

(Mohamed EL-Shishini and Upadhyaya, 2018).

It helps in the identification of cost drivers for each type of activity. A cost driver is a part

of the activity that utilizes the maximum cost in the manufacturing process. This model provides

a tracking support for the cost involved in the activities that are very beneficial for the business

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organization. It is necessary to create budgets for the business operation and do a proper

planning. When there is an observation related to increasing cost then this approach has been

used to reduce the cost of the planning and budgeting stage (RUAN and ZHOU, 2017).

After the introduction of this model, people have started using the same and replace it with the

previously used methods. The previously used methods consist of so many hassles and involve

difficult and lengthy calculations. They were more time consuming too. So, this method has been

proved very beneficial in reducing the time as well as the cost involved in the process of

calculating activity cost.

ABC Model in accordance with the goals and strategies of MYOB Group Ltd. Mission and

objective of MYOB Group Limited.

Every company has its pre-defined vision and missions. The major mission of MYOB Group is

to grow with the growth of the clients. It always focused on the retention of the customers by

providing them with the best business solutions. They want to provide a good level of

satisfaction to the clients and resolve their issues in an effective way. There are various

categories of the services that are provided to the clients that can satisfy their needs on different

levels (Gille, 2010).

The main objective of this organization is to increase the number of clients by providing them

online as well as offline services to all type of businesses. They do not focus on a particular

client size as the main motive is to create a solution that is compatible with all types of

businesses.

There are three types of strategies set by MYOB Group Ltd-

1. Increase the growth in existing market- This is an important objective of the organization. In

order to achieve the same, they are targeting their online subscribers that results in increasing the

subscription too.

5

planning. When there is an observation related to increasing cost then this approach has been

used to reduce the cost of the planning and budgeting stage (RUAN and ZHOU, 2017).

After the introduction of this model, people have started using the same and replace it with the

previously used methods. The previously used methods consist of so many hassles and involve

difficult and lengthy calculations. They were more time consuming too. So, this method has been

proved very beneficial in reducing the time as well as the cost involved in the process of

calculating activity cost.

ABC Model in accordance with the goals and strategies of MYOB Group Ltd. Mission and

objective of MYOB Group Limited.

Every company has its pre-defined vision and missions. The major mission of MYOB Group is

to grow with the growth of the clients. It always focused on the retention of the customers by

providing them with the best business solutions. They want to provide a good level of

satisfaction to the clients and resolve their issues in an effective way. There are various

categories of the services that are provided to the clients that can satisfy their needs on different

levels (Gille, 2010).

The main objective of this organization is to increase the number of clients by providing them

online as well as offline services to all type of businesses. They do not focus on a particular

client size as the main motive is to create a solution that is compatible with all types of

businesses.

There are three types of strategies set by MYOB Group Ltd-

1. Increase the growth in existing market- This is an important objective of the organization. In

order to achieve the same, they are targeting their online subscribers that results in increasing the

subscription too.

5

2. Penetrate the new market option- This strategy basically focuses on increasing the accessibility

of the market with the help of payments and increase the shares and the total market size.

3. Strengthen the working base and new market opportunities- It is important to grab all the

upcoming opportunities for the growth of the organization. MYOB has focused on the strategies

that help them in gain the available opportunities (Marsh, 2012).

They have the vision to provide the best technical support to the business. It has also created

strategies to maintain a good focus on the deliverables that have been transferred to its partners

and clients. It also wants to participate in the community level things as a member and would

create a good relationship with the shareholders of the company (Keuper, 2011).

How ABC model assists in achieving the strategies of MYOB Group Ltd.

All the strategies of an organization and Activity Based Costing always work together.

Strategies help a business organization to create plans for the future expansion of the

organization. Expansion plans involved different types of costs. A budget or estimation has

been created for the expansion plan when activity-based costing takes place.

MYOB belongs to service sector and ABC model basically works for manufacturing industries.

But it has been analysed in case of MYOB that this model can be used in the service industry

or technology-based industry. ABC tool is mainly used for assessing the indirect cost of the

operations belongs to a company. In the case of MYOB, a major part of the cost incurred is the

part of the indirect cost (Activity-based costing study, 2007).

ABC model has been used in the analysis of MYOB. The benefits or advantages due to the

same are-

The main focus of MYOB is to increase its customer ways in an efficient way. It has provided

online services for an increase in online subscriptions. All the allocation of resources and

analysis of cost have been done for the same by doing ABC costing. This helps in identifying

the ultimate cost of the product. It helps BYOD to understand the utility of each activity and

the advantage gain through that. ABC model provides assistance to know the estimated prices

of the services that are offered to tier 3 clients (Budgeting, 2013).

6

of the market with the help of payments and increase the shares and the total market size.

3. Strengthen the working base and new market opportunities- It is important to grab all the

upcoming opportunities for the growth of the organization. MYOB has focused on the strategies

that help them in gain the available opportunities (Marsh, 2012).

They have the vision to provide the best technical support to the business. It has also created

strategies to maintain a good focus on the deliverables that have been transferred to its partners

and clients. It also wants to participate in the community level things as a member and would

create a good relationship with the shareholders of the company (Keuper, 2011).

How ABC model assists in achieving the strategies of MYOB Group Ltd.

All the strategies of an organization and Activity Based Costing always work together.

Strategies help a business organization to create plans for the future expansion of the

organization. Expansion plans involved different types of costs. A budget or estimation has

been created for the expansion plan when activity-based costing takes place.

MYOB belongs to service sector and ABC model basically works for manufacturing industries.

But it has been analysed in case of MYOB that this model can be used in the service industry

or technology-based industry. ABC tool is mainly used for assessing the indirect cost of the

operations belongs to a company. In the case of MYOB, a major part of the cost incurred is the

part of the indirect cost (Activity-based costing study, 2007).

ABC model has been used in the analysis of MYOB. The benefits or advantages due to the

same are-

The main focus of MYOB is to increase its customer ways in an efficient way. It has provided

online services for an increase in online subscriptions. All the allocation of resources and

analysis of cost have been done for the same by doing ABC costing. This helps in identifying

the ultimate cost of the product. It helps BYOD to understand the utility of each activity and

the advantage gain through that. ABC model provides assistance to know the estimated prices

of the services that are offered to tier 3 clients (Budgeting, 2013).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The annual report shows the basic elements that identify the position of an organization. AN

observation has been done with the help of the annual report of BYOD. It has been defining

that the working if the organization has been divided into four parts. These four parts are-

Clients and partners

Enterprise solution

Operation and services

Cooperates (Hoozze and Hansen, 2014)

An analysis of cost has been done for BYOD according to the costing techniques used by the

organization. It was considered a common base for different activities of all the segments and

the cost for four segments are allocated according to the same. So, it results in the improper

allocation of costs. With the help of ABC model, the actual and real analysis can be done as it

considered the actual resources involved in each segment and cost involved in the same can be

calculated. This model helps in understanding the allocation of cost as well as the resources. It

also creates an understanding of different cost drivers (THORPE, 2015).

7

observation has been done with the help of the annual report of BYOD. It has been defining

that the working if the organization has been divided into four parts. These four parts are-

Clients and partners

Enterprise solution

Operation and services

Cooperates (Hoozze and Hansen, 2014)

An analysis of cost has been done for BYOD according to the costing techniques used by the

organization. It was considered a common base for different activities of all the segments and

the cost for four segments are allocated according to the same. So, it results in the improper

allocation of costs. With the help of ABC model, the actual and real analysis can be done as it

considered the actual resources involved in each segment and cost involved in the same can be

calculated. This model helps in understanding the allocation of cost as well as the resources. It

also creates an understanding of different cost drivers (THORPE, 2015).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

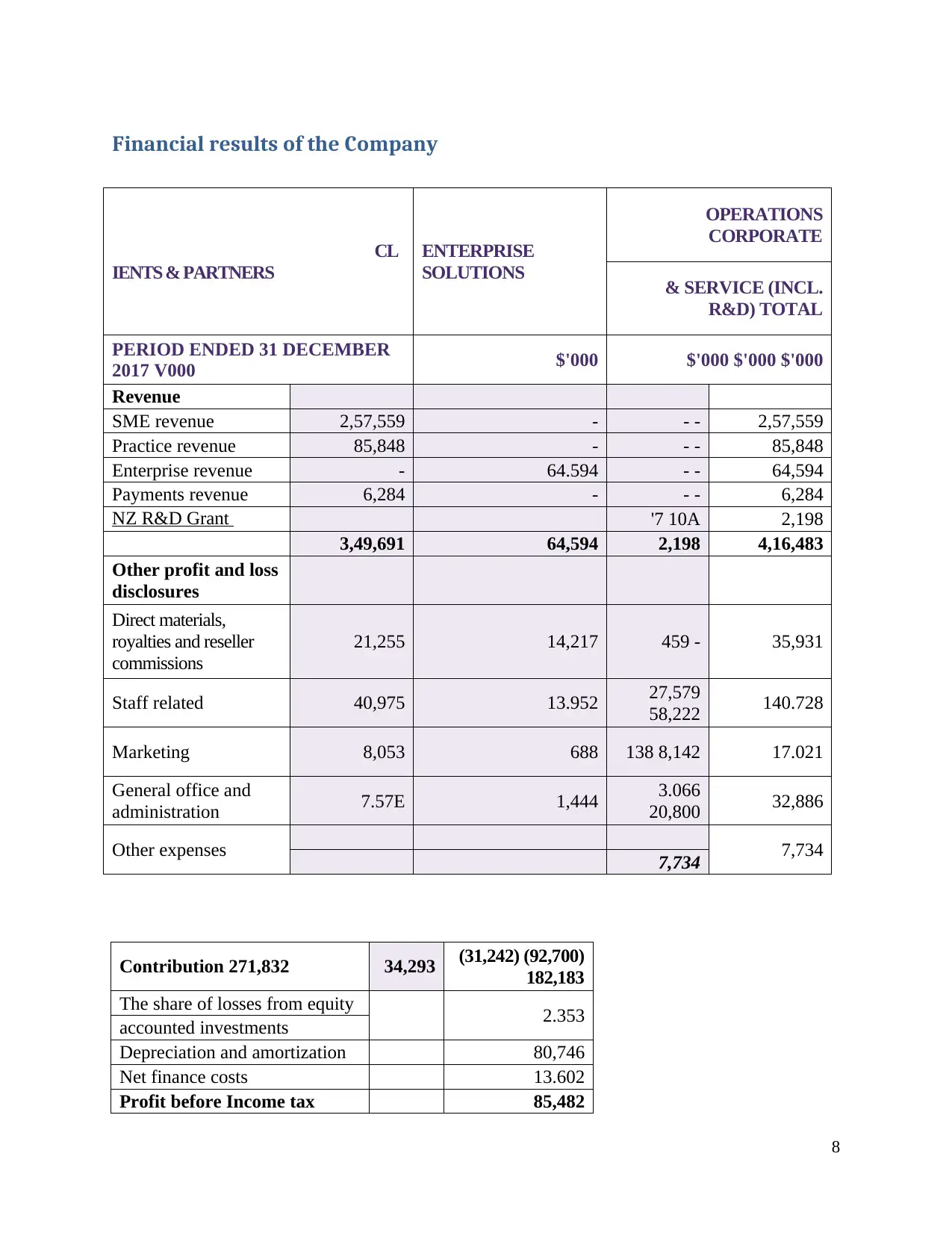

Financial results of the Company

CL

IENTS & PARTNERS

ENTERPRISE

SOLUTIONS

OPERATIONS

CORPORATE

& SERVICE (INCL.

R&D) TOTAL

PERIOD ENDED 31 DECEMBER

2017 V000 $'000 $'000 $'000 $'000

Revenue

SME revenue 2,57,559 - - - 2,57,559

Practice revenue 85,848 - - - 85,848

Enterprise revenue - 64.594 - - 64,594

Payments revenue 6,284 - - - 6,284

NZ R&D Grant

revenue

'7 10A 2,198

3,49,691 64,594 2,198 4,16,483

Other profit and loss

disclosures

Direct materials,

royalties and reseller

commissions

21,255 14,217 459 - 35,931

Staff related 40,975 13.952 27,579

58,222 140.728

Marketing 8,053 688 138 8,142 17.021

General office and

administration 7.57E 1,444 3.066

20,800 32,886

Other expenses 7,734

7,734

Contribution 271,832 34,293 (31,242) (92,700)

182,183

The share of losses from equity 2.353

accounted investments

Depreciation and amortization 80,746

Net finance costs 13.602

Profit before Income tax 85,482

8

CL

IENTS & PARTNERS

ENTERPRISE

SOLUTIONS

OPERATIONS

CORPORATE

& SERVICE (INCL.

R&D) TOTAL

PERIOD ENDED 31 DECEMBER

2017 V000 $'000 $'000 $'000 $'000

Revenue

SME revenue 2,57,559 - - - 2,57,559

Practice revenue 85,848 - - - 85,848

Enterprise revenue - 64.594 - - 64,594

Payments revenue 6,284 - - - 6,284

NZ R&D Grant

revenue

'7 10A 2,198

3,49,691 64,594 2,198 4,16,483

Other profit and loss

disclosures

Direct materials,

royalties and reseller

commissions

21,255 14,217 459 - 35,931

Staff related 40,975 13.952 27,579

58,222 140.728

Marketing 8,053 688 138 8,142 17.021

General office and

administration 7.57E 1,444 3.066

20,800 32,886

Other expenses 7,734

7,734

Contribution 271,832 34,293 (31,242) (92,700)

182,183

The share of losses from equity 2.353

accounted investments

Depreciation and amortization 80,746

Net finance costs 13.602

Profit before Income tax 85,482

8

Interpretation

These financial statements have shown that company has created value on the

investment. It is observed that company has a good amount to cash inflow from its enterprise's

solution business. The increased profit has shown that company increased its business efficiency

by using the advance costing system.

Recommendations-

MYOB has used an older model for analysis of cost that is not providing the correct

results. Use of ABC costing has been recommended to MYOB as it can create different benefits

for the company. Cost of each and every segment can be analysed properly that create a

convenience in finding out the maximum cost for each activity. The existing technique is not

worth and should be removed properly. ABC model is a modern way of analysing the cost and

staff can easily understand the same.

Another Management Accounting Tool suitable for the use of MYOB Group Ltd.

MYOB Group Ltd. can also use another method for analysis of cost other than Activity-Based

Costing. The model is Life Cycle Costing. Basically, it selects the different options that can

create an impact on the current as well as the future cost of the company. It compares the current

options available for investments and then provides the cost options for next 20 years after doing

a proper identification. It is considered as a long-term approach. The benefits of using this

approach are-

Evaluating the policies of the company- This model helps in doing the evaluation of the policies

of the company. It consists of a long term approach that BYOD needs for its expansion plan

(Nowack, Hoppe and Guenther, 2012).

Ensuring Regulatory Compliance- There are different compliances for the service industry and

regulatory authorities handle it. There are heavy penalties for the non- compliance. Life cycle

costing method helps in the reporting and documentation in a very good at that assists the

manager to follow all those compliances (Mittmann and De Oliveira, 2016).

9

These financial statements have shown that company has created value on the

investment. It is observed that company has a good amount to cash inflow from its enterprise's

solution business. The increased profit has shown that company increased its business efficiency

by using the advance costing system.

Recommendations-

MYOB has used an older model for analysis of cost that is not providing the correct

results. Use of ABC costing has been recommended to MYOB as it can create different benefits

for the company. Cost of each and every segment can be analysed properly that create a

convenience in finding out the maximum cost for each activity. The existing technique is not

worth and should be removed properly. ABC model is a modern way of analysing the cost and

staff can easily understand the same.

Another Management Accounting Tool suitable for the use of MYOB Group Ltd.

MYOB Group Ltd. can also use another method for analysis of cost other than Activity-Based

Costing. The model is Life Cycle Costing. Basically, it selects the different options that can

create an impact on the current as well as the future cost of the company. It compares the current

options available for investments and then provides the cost options for next 20 years after doing

a proper identification. It is considered as a long-term approach. The benefits of using this

approach are-

Evaluating the policies of the company- This model helps in doing the evaluation of the policies

of the company. It consists of a long term approach that BYOD needs for its expansion plan

(Nowack, Hoppe and Guenther, 2012).

Ensuring Regulatory Compliance- There are different compliances for the service industry and

regulatory authorities handle it. There are heavy penalties for the non- compliance. Life cycle

costing method helps in the reporting and documentation in a very good at that assists the

manager to follow all those compliances (Mittmann and De Oliveira, 2016).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Conclusion

It has been concluded with the help of above analysis that Activity-based costing model

is very helpful for the future growth of BYOD. It also works in the service industry. Activity-

based costing is used according to the utilization of resources in the activities of business

organizations. This helps in assessing the estimated cost and resources involved in a particular

set of activities. Implementation of this model becomes more effective by describing the goals,

objectives and missions of the organization. If it is difficult for any company to implement ABC

model then it can also apply Life Cycle Costing model. This tool is also useful for long term

growth of MYOB. So, the best option for MYOB is to implement ABC Model.

10

It has been concluded with the help of above analysis that Activity-based costing model

is very helpful for the future growth of BYOD. It also works in the service industry. Activity-

based costing is used according to the utilization of resources in the activities of business

organizations. This helps in assessing the estimated cost and resources involved in a particular

set of activities. Implementation of this model becomes more effective by describing the goals,

objectives and missions of the organization. If it is difficult for any company to implement ABC

model then it can also apply Life Cycle Costing model. This tool is also useful for long term

growth of MYOB. So, the best option for MYOB is to implement ABC Model.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Activity-based costing study. (2007). Vancouver, B.C.: The Committee.

Budgeting. (2013). London: BPP Learning Media Ltd.

Gille, C. (2010). Life Cycle Costing. Controlling, 22(1), pp.31-33.

Hoozze, S. and Hansen, S. (2014). A Comparison of Activity-Based Costing and Time-Driven

Activity-Based Costing. SSRN Electronic Journal.

Keuper, F. (2011). Life Cycle Costing. Business + Innovation, 2(3), pp.3-3.

Marsh, C. (2012). Financial management for non-financial managers. London: Kogan Page.

Mittmann, N. and De Oliveira, C. (2016). Importance of cost estimates and cost studies. Current

Oncology, 23(0), p.6.

Mohamed EL-Shishini, H. and Upadhyaya, M. (2018). The Relationships Between Contextual

Variables and Perceived Importance and Bene-fits of Environmental Management

Accounting (EMA) Techniques. Journal of Environmental Accounting and Management,

6(1), pp.17-32.

Nowack, M., Hoppe, H. and Guenther, E. (2012). Review and downscaling of life cycle decision

support tools for the procurement of low-value products. The International Journal of Life

Cycle Assessment, 17(6), pp.655-665.

RUAN, Y. and ZHOU, L. (2017). The Research on Management Accounting Tools—Based on

the Comparison Between Activity-based Costing and Traditional Costing. DEStech

Transactions on Engineering and Technology Research, (amsm).

THORPE, R. (2015). PERFORMANCE MANAGEMENT. [Place of publication not identified]:

PALGRAVE MACMILLAN.

Wink, G. and Corradino, L. (2011). Intermediate accounting demystified. New York, NY:

McGraw-Hill.

11

Activity-based costing study. (2007). Vancouver, B.C.: The Committee.

Budgeting. (2013). London: BPP Learning Media Ltd.

Gille, C. (2010). Life Cycle Costing. Controlling, 22(1), pp.31-33.

Hoozze, S. and Hansen, S. (2014). A Comparison of Activity-Based Costing and Time-Driven

Activity-Based Costing. SSRN Electronic Journal.

Keuper, F. (2011). Life Cycle Costing. Business + Innovation, 2(3), pp.3-3.

Marsh, C. (2012). Financial management for non-financial managers. London: Kogan Page.

Mittmann, N. and De Oliveira, C. (2016). Importance of cost estimates and cost studies. Current

Oncology, 23(0), p.6.

Mohamed EL-Shishini, H. and Upadhyaya, M. (2018). The Relationships Between Contextual

Variables and Perceived Importance and Bene-fits of Environmental Management

Accounting (EMA) Techniques. Journal of Environmental Accounting and Management,

6(1), pp.17-32.

Nowack, M., Hoppe, H. and Guenther, E. (2012). Review and downscaling of life cycle decision

support tools for the procurement of low-value products. The International Journal of Life

Cycle Assessment, 17(6), pp.655-665.

RUAN, Y. and ZHOU, L. (2017). The Research on Management Accounting Tools—Based on

the Comparison Between Activity-based Costing and Traditional Costing. DEStech

Transactions on Engineering and Technology Research, (amsm).

THORPE, R. (2015). PERFORMANCE MANAGEMENT. [Place of publication not identified]:

PALGRAVE MACMILLAN.

Wink, G. and Corradino, L. (2011). Intermediate accounting demystified. New York, NY:

McGraw-Hill.

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.