HI5017: Activity Based Costing Model for Origin Energy Analysis

VerifiedAdded on 2023/06/11

|14

|2995

|453

Report

AI Summary

This report provides an analysis of the Activity Based Costing (ABC) model and its application to Origin Energy, an Australian energy company. It discusses how ABC can be used to allocate energy costs, identify cost drivers, and improve decision-making. The report aligns ABC with Origin Energy's strategic objectives, such as customer focus and cost reduction. It recommends the implementation of ABC with effective change management and resource allocation. Furthermore, it suggests Enterprise Risk Management (ERM) as an additional management tool to address risk factors and achieve strategic goals, ultimately enhancing the company's financial performance and competitiveness.

Activity Based Costing Model 1

ACTIVITY BASED COSTING MODEL

By (Student’s Name)

Professor’s Name

College

Course

Date

ACTIVITY BASED COSTING MODEL

By (Student’s Name)

Professor’s Name

College

Course

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity Based Costing Model 2

ACTIVITY BASED COSTING MODEL

Table of Contents

Executive Summary.....................................................................................................................................3

Introduction.................................................................................................................................................3

Explanation Activity-based model and its features......................................................................................4

Explanation of how Activity-based costing aligns with the goals as well as strategies of the Origin Energy

.................................................................................................................................................................... 6

Objectives and mission of the Origin Energy...........................................................................................6

Corporate strategies of the Origin Energy...............................................................................................6

Explanation of how Activity-based costing system enables Origin Energy in achieving their strategies. 7

Recommendation about the implementation of Activity-based costing model for Origin Energy..............8

Appropriate management tool suitable for Origin Energy apart from Activity-based costing model..........9

Conclusion...................................................................................................................................................9

References.................................................................................................................................................11

ACTIVITY BASED COSTING MODEL

Table of Contents

Executive Summary.....................................................................................................................................3

Introduction.................................................................................................................................................3

Explanation Activity-based model and its features......................................................................................4

Explanation of how Activity-based costing aligns with the goals as well as strategies of the Origin Energy

.................................................................................................................................................................... 6

Objectives and mission of the Origin Energy...........................................................................................6

Corporate strategies of the Origin Energy...............................................................................................6

Explanation of how Activity-based costing system enables Origin Energy in achieving their strategies. 7

Recommendation about the implementation of Activity-based costing model for Origin Energy..............8

Appropriate management tool suitable for Origin Energy apart from Activity-based costing model..........9

Conclusion...................................................................................................................................................9

References.................................................................................................................................................11

Activity Based Costing Model 3

Executive Summary

This paper discusses a modern approach to apportioning the exact cost of energy to a

given cost center or product in the Company known as the Origin Company. Activity-based

costing which is useful in the identification of particular cost drivers and after that assigns costs

depending on the details of the product mix, facility’s equipment, and operation. The paper will

use ABC method to allocate the values of energy in the chosen manufacturing environment.

This approach can also help the organization to predict and analyze the amount of energy used

in the industry. The costs of energy at Origin Energy located in Australia are applied as an

illustration of this modern model. This paper uses the principle of ABC system explicitly to

comprehensive energy management and energy costing in the organization. This paper also

discusses the recommendation that the Origin Energy should put in place to ensure that this

management accounting tool is appropriately implemented in the organization. Lastly, the

paper enlightens another model that can also help the Origin Company to achieve most of its

strategies.

Introduction

Origin Energy is one of the Listed Company in Australia. The Company undertakes the

energy business. The organization consumes the massive amount of resources, and the cost of

energy is also increasing, and the prediction is that the trend will continue even to the future

years to come. The constant changes that happened in the sector of energy and necessitate

them to acquire relevant information useful in decision making, need a rethinking on the type

of the costing system that the Company should apply to be active in the industry. Due to the

Executive Summary

This paper discusses a modern approach to apportioning the exact cost of energy to a

given cost center or product in the Company known as the Origin Company. Activity-based

costing which is useful in the identification of particular cost drivers and after that assigns costs

depending on the details of the product mix, facility’s equipment, and operation. The paper will

use ABC method to allocate the values of energy in the chosen manufacturing environment.

This approach can also help the organization to predict and analyze the amount of energy used

in the industry. The costs of energy at Origin Energy located in Australia are applied as an

illustration of this modern model. This paper uses the principle of ABC system explicitly to

comprehensive energy management and energy costing in the organization. This paper also

discusses the recommendation that the Origin Energy should put in place to ensure that this

management accounting tool is appropriately implemented in the organization. Lastly, the

paper enlightens another model that can also help the Origin Company to achieve most of its

strategies.

Introduction

Origin Energy is one of the Listed Company in Australia. The Company undertakes the

energy business. The organization consumes the massive amount of resources, and the cost of

energy is also increasing, and the prediction is that the trend will continue even to the future

years to come. The constant changes that happened in the sector of energy and necessitate

them to acquire relevant information useful in decision making, need a rethinking on the type

of the costing system that the Company should apply to be active in the industry. Due to the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity Based Costing Model 4

financial and economic manifested in the sector, Origin Energy must discover ways to stay

strong as well as reducing costs; ensure that its activities continue as usual in the industry with

the role of becoming best of the best in the industry. Therefore, the company requires different

measures to enhance the information system as well as ensuring that the operational track

most of the costs in the company. The complexity of the organization and other different

challenges such as ways to monitor the energy within the processes necessitate the

organization to model the systems, but the system Complexity will make the organization to

suffer more costs regarding information and time to facilitate the creation of the model. At the

same, most of the organization such as the Utility Companies begins to implement modern

technologies to facilitate the distribution of energy. The most favorable management

accounting tool that will enable the Origin Energy to solve most of the issues that affect its

operations and be relevant in the industry is the adoption of the Activity-based costing model.

This approach will enable the management to verify whether a particular Response and

Demand is viable to the organization. The method will also assist in modeling how the facility

uses the energy. It will also offer the required structure to be used in evaluating the product

and processes costs in the organization. The paper is separated into parts with each part

discusses the issues relating to the Activity-based costing.

Explanation Activity-based model and its features

ABC is the management accounting tool used to find costs to process or product of the

Company. Rather than apportioning costs directly to specific products and services, they are

allocated to the Company’s activities (Dalci, Tanis and Kosan 2010). Then, the products cost are

financial and economic manifested in the sector, Origin Energy must discover ways to stay

strong as well as reducing costs; ensure that its activities continue as usual in the industry with

the role of becoming best of the best in the industry. Therefore, the company requires different

measures to enhance the information system as well as ensuring that the operational track

most of the costs in the company. The complexity of the organization and other different

challenges such as ways to monitor the energy within the processes necessitate the

organization to model the systems, but the system Complexity will make the organization to

suffer more costs regarding information and time to facilitate the creation of the model. At the

same, most of the organization such as the Utility Companies begins to implement modern

technologies to facilitate the distribution of energy. The most favorable management

accounting tool that will enable the Origin Energy to solve most of the issues that affect its

operations and be relevant in the industry is the adoption of the Activity-based costing model.

This approach will enable the management to verify whether a particular Response and

Demand is viable to the organization. The method will also assist in modeling how the facility

uses the energy. It will also offer the required structure to be used in evaluating the product

and processes costs in the organization. The paper is separated into parts with each part

discusses the issues relating to the Activity-based costing.

Explanation Activity-based model and its features

ABC is the management accounting tool used to find costs to process or product of the

Company. Rather than apportioning costs directly to specific products and services, they are

allocated to the Company’s activities (Dalci, Tanis and Kosan 2010). Then, the products cost are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity Based Costing Model 5

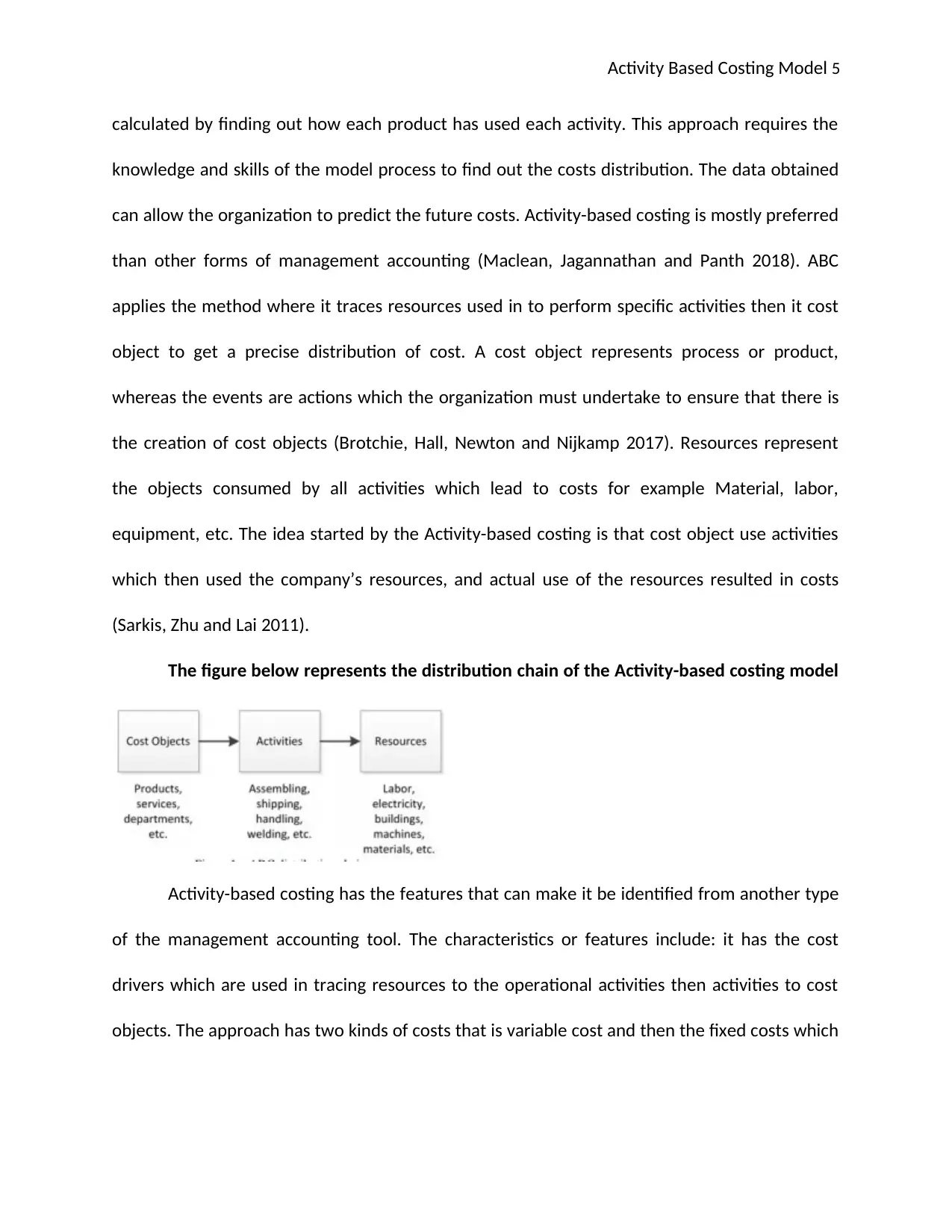

calculated by finding out how each product has used each activity. This approach requires the

knowledge and skills of the model process to find out the costs distribution. The data obtained

can allow the organization to predict the future costs. Activity-based costing is mostly preferred

than other forms of management accounting (Maclean, Jagannathan and Panth 2018). ABC

applies the method where it traces resources used in to perform specific activities then it cost

object to get a precise distribution of cost. A cost object represents process or product,

whereas the events are actions which the organization must undertake to ensure that there is

the creation of cost objects (Brotchie, Hall, Newton and Nijkamp 2017). Resources represent

the objects consumed by all activities which lead to costs for example Material, labor,

equipment, etc. The idea started by the Activity-based costing is that cost object use activities

which then used the company’s resources, and actual use of the resources resulted in costs

(Sarkis, Zhu and Lai 2011).

The figure below represents the distribution chain of the Activity-based costing model

Activity-based costing has the features that can make it be identified from another type

of the management accounting tool. The characteristics or features include: it has the cost

drivers which are used in tracing resources to the operational activities then activities to cost

objects. The approach has two kinds of costs that is variable cost and then the fixed costs which

calculated by finding out how each product has used each activity. This approach requires the

knowledge and skills of the model process to find out the costs distribution. The data obtained

can allow the organization to predict the future costs. Activity-based costing is mostly preferred

than other forms of management accounting (Maclean, Jagannathan and Panth 2018). ABC

applies the method where it traces resources used in to perform specific activities then it cost

object to get a precise distribution of cost. A cost object represents process or product,

whereas the events are actions which the organization must undertake to ensure that there is

the creation of cost objects (Brotchie, Hall, Newton and Nijkamp 2017). Resources represent

the objects consumed by all activities which lead to costs for example Material, labor,

equipment, etc. The idea started by the Activity-based costing is that cost object use activities

which then used the company’s resources, and actual use of the resources resulted in costs

(Sarkis, Zhu and Lai 2011).

The figure below represents the distribution chain of the Activity-based costing model

Activity-based costing has the features that can make it be identified from another type

of the management accounting tool. The characteristics or features include: it has the cost

drivers which are used in tracing resources to the operational activities then activities to cost

objects. The approach has two kinds of costs that is variable cost and then the fixed costs which

Activity Based Costing Model 6

are used in the provision of quality information in the organization (Rajemi, Mativenga and

Aramcharoen 2010). The cost driver of the model also helps in dictating cost behavior design.

Explanation of how Activity-based costing aligns with the goals as well as

strategies of the Origin Energy

Objectives and mission of the Origin Energy

The mission of the Origin is to lead in the transition of smarter, customer-centric, and

cleaner energy to their customers (Moriarty 2018). The objectives of the Origin Energy include

establishing the closer focus on their customers, building trust and loyalty and delivering

different products to their customers, for example, predictable plan. The Company ensures to

use Analytic as they continue to offer different products as well as achieving their customer-

centric goals. Another objective of the origin is providing electricity products and natural gas to

all of their customers in the market (Amiri and Weinberger 2018).

Corporate strategies of the Origin Energy

Origin Energy focuses on being one of a successful organization in the market among the

competing firms that offer the same products. The primary strategy of the Origin Energy is to

ensure the connection of energy resources to its market (Imteaz and Ahsan 2018). It has the

following strategic priorities: To deliver leading customer solutions and experience, create

resources to balance the increasing demand of gas, ensure that there is disciplined in the

management of capital, and embrace digital and a decentralized future (Filapek 2018). Other

strategies include moving toward the production of clean energy and also being one of the

lower cost operators. The Origin Energy mainly focuses on what matters to their customers.

are used in the provision of quality information in the organization (Rajemi, Mativenga and

Aramcharoen 2010). The cost driver of the model also helps in dictating cost behavior design.

Explanation of how Activity-based costing aligns with the goals as well as

strategies of the Origin Energy

Objectives and mission of the Origin Energy

The mission of the Origin is to lead in the transition of smarter, customer-centric, and

cleaner energy to their customers (Moriarty 2018). The objectives of the Origin Energy include

establishing the closer focus on their customers, building trust and loyalty and delivering

different products to their customers, for example, predictable plan. The Company ensures to

use Analytic as they continue to offer different products as well as achieving their customer-

centric goals. Another objective of the origin is providing electricity products and natural gas to

all of their customers in the market (Amiri and Weinberger 2018).

Corporate strategies of the Origin Energy

Origin Energy focuses on being one of a successful organization in the market among the

competing firms that offer the same products. The primary strategy of the Origin Energy is to

ensure the connection of energy resources to its market (Imteaz and Ahsan 2018). It has the

following strategic priorities: To deliver leading customer solutions and experience, create

resources to balance the increasing demand of gas, ensure that there is disciplined in the

management of capital, and embrace digital and a decentralized future (Filapek 2018). Other

strategies include moving toward the production of clean energy and also being one of the

lower cost operators. The Origin Energy mainly focuses on what matters to their customers.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity Based Costing Model 7

The company aims at improving each day to be better in the future (Merkenich 2018). This will

motivate them to build and grow the business, connect their customers to the technologies and

energy of the future. These strategies help to set the path and give direction to the Company. It

informs the company what they have to deliver based on the on the opportunity cost and

priorities. The strategies can also tell the organization where it is headed to regarding fulfilling

the set goals (Amiri and Weinberger 2018).

Explanation of how Activity-based costing system enables Origin Energy in

achieving their strategies

ABC system will allow the organization to apportion all the costs of resources to

functions or activities. Nevertheless, the Activity-based costing model can be applied in the

organization to find the allocation of a particular price of resources all over the Company, for

example, the cost of energy. With the distribution of energy cost, management will be able to

find out which activities, as well as cost centers or products, are incurring the highest value of

energy and consuming the highest amount of energy (Govindan, Khodaverdi and Jafarian 2013).

This information will then enable the organization to detect the probable energy waste.

Management can then put its efforts on the departmental areas where there is a significant

amount of energy which is being used and then evaluates them with the intention of finding

out whether a redesign is capable of reducing waste as well as increasing the efficiency of

energy. Activity-based costing will also offer actual cost information that the organization can

use to ensure that there is energy saving in specific functions or areas (Maclean, Jagannathan

and Panth 2018). The approach will, therefore, be useful in the organization in that it will

facilitate the management decision making relating cost issues. The organization will improve

The company aims at improving each day to be better in the future (Merkenich 2018). This will

motivate them to build and grow the business, connect their customers to the technologies and

energy of the future. These strategies help to set the path and give direction to the Company. It

informs the company what they have to deliver based on the on the opportunity cost and

priorities. The strategies can also tell the organization where it is headed to regarding fulfilling

the set goals (Amiri and Weinberger 2018).

Explanation of how Activity-based costing system enables Origin Energy in

achieving their strategies

ABC system will allow the organization to apportion all the costs of resources to

functions or activities. Nevertheless, the Activity-based costing model can be applied in the

organization to find the allocation of a particular price of resources all over the Company, for

example, the cost of energy. With the distribution of energy cost, management will be able to

find out which activities, as well as cost centers or products, are incurring the highest value of

energy and consuming the highest amount of energy (Govindan, Khodaverdi and Jafarian 2013).

This information will then enable the organization to detect the probable energy waste.

Management can then put its efforts on the departmental areas where there is a significant

amount of energy which is being used and then evaluates them with the intention of finding

out whether a redesign is capable of reducing waste as well as increasing the efficiency of

energy. Activity-based costing will also offer actual cost information that the organization can

use to ensure that there is energy saving in specific functions or areas (Maclean, Jagannathan

and Panth 2018). The approach will, therefore, be useful in the organization in that it will

facilitate the management decision making relating cost issues. The organization will improve

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity Based Costing Model 8

their performance hence leading to the profitability in the long-run (Drury 2013). The use of

Activity-based costing will also enable the organization to improve their financial performance.

The will increase the profitability and improve the performance in the following ways: It will

identify the exact cost drivers as well as overhead costs leading to active business processes

(Catherine, Soundarrajan and Louis 2018). The manager will be able to develop a hint of the

business processes that perform well and those that are wasteful through the allocation of both

the indirect and direct costs of their products. The costs data of the Activity-based costing is

equally important because it will help the management to come up with optimal choices about

how they should assign the limited resources of the organization. Therefore, effective

implementation of this approach of management accounting into the system of the Origin

Energy will enable them to achieve most of their strategic priorities (Tejera, Rios, Martínez and

Palacios 2018).

Recommendation about the implementation of Activity-based costing

model for Origin Energy

The application of ABC will necessitate the establishment of the process of effective

change management. The process will have the responsibility of ensuring that the organization

supports the system. It will involve putting in place the top manager to fight for the initiative

and the issues that affect all the employees regarding the implementation of the Activity-based

costing system (Fang, Ma and Luo 2018).

The implementation of Activity-based costing will necessitate the organization to put in

place enough resources, such as time, competent team, hardware, software as well as the

human support (people). So, the organization needs to provide enough people and material to

their performance hence leading to the profitability in the long-run (Drury 2013). The use of

Activity-based costing will also enable the organization to improve their financial performance.

The will increase the profitability and improve the performance in the following ways: It will

identify the exact cost drivers as well as overhead costs leading to active business processes

(Catherine, Soundarrajan and Louis 2018). The manager will be able to develop a hint of the

business processes that perform well and those that are wasteful through the allocation of both

the indirect and direct costs of their products. The costs data of the Activity-based costing is

equally important because it will help the management to come up with optimal choices about

how they should assign the limited resources of the organization. Therefore, effective

implementation of this approach of management accounting into the system of the Origin

Energy will enable them to achieve most of their strategic priorities (Tejera, Rios, Martínez and

Palacios 2018).

Recommendation about the implementation of Activity-based costing

model for Origin Energy

The application of ABC will necessitate the establishment of the process of effective

change management. The process will have the responsibility of ensuring that the organization

supports the system. It will involve putting in place the top manager to fight for the initiative

and the issues that affect all the employees regarding the implementation of the Activity-based

costing system (Fang, Ma and Luo 2018).

The implementation of Activity-based costing will necessitate the organization to put in

place enough resources, such as time, competent team, hardware, software as well as the

human support (people). So, the organization needs to provide enough people and material to

Activity Based Costing Model 9

help in completing the implementation process of Activity-based costing. All the stages that the

model through require enough resources. Such as, the implementation stage needs enough

funds and knowledge, skilled personnel’s (García, Istrate and Iribarren 2018).

Appropriate management tool suitable for Origin Energy apart from

Activity-based costing model

The proper management accounting that the organization should develop is the (ERM)

Enterprise risk management. This will enable the organization to identify the risk as well as

providing a suitable method of addressing the risk factors for the achievement of the set

strategic objectives (Etges, Souza, Kliemann and Felix, 2018). It will also enable the organization

to be ahead of its competitors. The process of managing risk is an important factor used in the

strategic management of any form of organization. Therefore, Origin Energy should include

Enterprise risk management in its ongoing activities. This approach will offer awareness of the

various risks that affect the organization as well as providing suitable methods of solving them

effectively. It will also enhance the confidence of the management and the entire employees

about the accomplishment of the company’s strategic objectives.

Conclusion

This paper provides ways in which the Origin Energy can use Activity-based costing to

improve the decision-making process. The management can use the model to solve most of the

problems faced by Origin Energy. Being that the organization is related to the sector of energy,

the volume of fixed costs is high, and the only model that can help to reduce the costs is the

Activity-based costing model. The approach will not only increase the profit of the entity but

help in completing the implementation process of Activity-based costing. All the stages that the

model through require enough resources. Such as, the implementation stage needs enough

funds and knowledge, skilled personnel’s (García, Istrate and Iribarren 2018).

Appropriate management tool suitable for Origin Energy apart from

Activity-based costing model

The proper management accounting that the organization should develop is the (ERM)

Enterprise risk management. This will enable the organization to identify the risk as well as

providing a suitable method of addressing the risk factors for the achievement of the set

strategic objectives (Etges, Souza, Kliemann and Felix, 2018). It will also enable the organization

to be ahead of its competitors. The process of managing risk is an important factor used in the

strategic management of any form of organization. Therefore, Origin Energy should include

Enterprise risk management in its ongoing activities. This approach will offer awareness of the

various risks that affect the organization as well as providing suitable methods of solving them

effectively. It will also enhance the confidence of the management and the entire employees

about the accomplishment of the company’s strategic objectives.

Conclusion

This paper provides ways in which the Origin Energy can use Activity-based costing to

improve the decision-making process. The management can use the model to solve most of the

problems faced by Origin Energy. Being that the organization is related to the sector of energy,

the volume of fixed costs is high, and the only model that can help to reduce the costs is the

Activity-based costing model. The approach will not only increase the profit of the entity but

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity Based Costing Model 10

also increased the perceived value of the customers. Therefore, any organization wishing to

increase their profitability and improve their decision-making process should use ABC model.

also increased the perceived value of the customers. Therefore, any organization wishing to

increase their profitability and improve their decision-making process should use ABC model.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity Based Costing Model 11

References

Amiri, S. and Weinberger, G., 2018. Increased cogeneration of renewable electricity through

energy cooperation in a Swedish district heating system-A case study. Renewable energy, 116,

pp.866-877.

Brotchie, J., Hall, P., Newton, P. and Nijkamp, P., 2017. The future of urban form: the impact of

new technology. Routledge.

Catherine, R.L.H., Soundarrajan, A. and Louis, J.R., 2018. Cost Optimization of a Ring Frame Unit.

In Advances in Power Systems and Energy Management (pp. 107-117). Springer, Singapore.

Dalci, I., Tanis, V. and Kosan, L., 2010. Customer profitability analysis with time-driven activity-

based costing: a case study in a hotel. International Journal of contemporary hospitality

Management, 22(5), pp.609-637.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Etges, A.P.B.D.S., de Souza, J.S., Kliemann Neto, F.J. and Felix, E.A., 2018. A proposed enterprise

risk management model for health organizations. Journal of Risk Research, pp.1-19.

References

Amiri, S. and Weinberger, G., 2018. Increased cogeneration of renewable electricity through

energy cooperation in a Swedish district heating system-A case study. Renewable energy, 116,

pp.866-877.

Brotchie, J., Hall, P., Newton, P. and Nijkamp, P., 2017. The future of urban form: the impact of

new technology. Routledge.

Catherine, R.L.H., Soundarrajan, A. and Louis, J.R., 2018. Cost Optimization of a Ring Frame Unit.

In Advances in Power Systems and Energy Management (pp. 107-117). Springer, Singapore.

Dalci, I., Tanis, V. and Kosan, L., 2010. Customer profitability analysis with time-driven activity-

based costing: a case study in a hotel. International Journal of contemporary hospitality

Management, 22(5), pp.609-637.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Etges, A.P.B.D.S., de Souza, J.S., Kliemann Neto, F.J. and Felix, E.A., 2018. A proposed enterprise

risk management model for health organizations. Journal of Risk Research, pp.1-19.

Activity Based Costing Model 12

Fang, Y., Ma, Z.D. and Luo, Y.Z., 2018. Carbon Emission Modelling for Construction Logistics

Process Through Activity-Based Method. In Proceedings of the 21st International Symposium on

Advancement of Construction Management and Real Estate (pp. 413-424). Springer, Singapore.

Filapek-Vandyck, R., 2018. A three pronged investment strategy. Equity, 32(2), p.6.

García-Gusano, D., Istrate, I.R. and Iribarren, D., 2018. Life-cycle consequences of internalising

socio-environmental externalities of power generation. Science of the Total Environment, 612,

pp.386-391.

Govindan, K., Khodaverdi, R. and Jafarian, A., 2013. A fuzzy multi criteria approach for

measuring sustainability performance of a supplier based on triple bottom line

approach. Journal of Cleaner Production, 47, pp.345-354.

Imteaz, M.A. and Ahsan, A., 2018. Solar panels: Real efficiencies, potential productions and

payback periods for major Australian cities. Sustainable Energy Technologies and

Assessments, 25, pp.119-125.

Maclean, R., Jagannathan, S. and Panth, B., 2018. Introduction. In Education and Skills for

Inclusive Growth, Green Jobs and the Greening of Economies in Asia (pp. 19-40). Springer,

Singapore.

Fang, Y., Ma, Z.D. and Luo, Y.Z., 2018. Carbon Emission Modelling for Construction Logistics

Process Through Activity-Based Method. In Proceedings of the 21st International Symposium on

Advancement of Construction Management and Real Estate (pp. 413-424). Springer, Singapore.

Filapek-Vandyck, R., 2018. A three pronged investment strategy. Equity, 32(2), p.6.

García-Gusano, D., Istrate, I.R. and Iribarren, D., 2018. Life-cycle consequences of internalising

socio-environmental externalities of power generation. Science of the Total Environment, 612,

pp.386-391.

Govindan, K., Khodaverdi, R. and Jafarian, A., 2013. A fuzzy multi criteria approach for

measuring sustainability performance of a supplier based on triple bottom line

approach. Journal of Cleaner Production, 47, pp.345-354.

Imteaz, M.A. and Ahsan, A., 2018. Solar panels: Real efficiencies, potential productions and

payback periods for major Australian cities. Sustainable Energy Technologies and

Assessments, 25, pp.119-125.

Maclean, R., Jagannathan, S. and Panth, B., 2018. Introduction. In Education and Skills for

Inclusive Growth, Green Jobs and the Greening of Economies in Asia (pp. 19-40). Springer,

Singapore.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.