Activity Based Costing Implementation for TILT Renewables Limited

VerifiedAdded on 2021/05/27

|16

|3267

|279

Report

AI Summary

This report provides a comprehensive analysis of Activity Based Costing (ABC) and its potential implementation within TILT Renewables Limited. The paper begins with an executive summary outlining the benefits of ABC, including improved cost allocation, product pricing, and strategic decision-making. It then introduces the concept of ABC, detailing its features and contrasting it with traditional costing methods, followed by a diagram showcasing the ABC process. The report examines how ABC aligns with TILT Renewables' mission, objectives, and corporate strategies, particularly in the context of the renewable energy sector. It offers recommendations for successful ABC implementation, emphasizing employee training and management support. Finally, the report suggests Just-in-Time inventory system as a complementary tool, providing a holistic approach to enhance the organization's efficiency and reduce costs.

Activity Based Costing 1

ACTIVITY BASED COSTING

By (Student’s Name)

Professor’s Name

College

Course

Date

ACTIVITY BASED COSTING

By (Student’s Name)

Professor’s Name

College

Course

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity Based Costing 2

ACTIVITY BASED COSTING

Table of Contents

Executive summary.....................................................................................................................................3

Introduction.................................................................................................................................................3

Description of Activity based costing and its features.................................................................................4

Description of how Activity based costing supports the current strategies and goals of the organization. 5

The mission and objectives of the TILT Renewables Limited...................................................................5

Corporate strategy of the TILT Renewable Limited.................................................................................6

How Activity based costing can help TILT Renewables Limited to attain its strategies............................6

Recommendation about the implementation of Activity Based Costing in the organization......................7

The management tool apart from Activity based costing that is more appropriate to TILT Renewables

Limited.........................................................................................................................................................8

Conclusion...................................................................................................................................................9

References.................................................................................................................................................10

ACTIVITY BASED COSTING

Table of Contents

Executive summary.....................................................................................................................................3

Introduction.................................................................................................................................................3

Description of Activity based costing and its features.................................................................................4

Description of how Activity based costing supports the current strategies and goals of the organization. 5

The mission and objectives of the TILT Renewables Limited...................................................................5

Corporate strategy of the TILT Renewable Limited.................................................................................6

How Activity based costing can help TILT Renewables Limited to attain its strategies............................6

Recommendation about the implementation of Activity Based Costing in the organization......................7

The management tool apart from Activity based costing that is more appropriate to TILT Renewables

Limited.........................................................................................................................................................8

Conclusion...................................................................................................................................................9

References.................................................................................................................................................10

Activity Based Costing 3

Executive Summary

This paper discusses how Activity-based costing can help the accounting information of

the management in TILT Renewables Limited. The control of The TILT Renewable Limited

should apply the use of the sophisticated cost information that can make them quick decisions in

the organisation. Given the high rate of competition in the industry and the need to reduce the

costs, the management of TILT Renewable Limited needs to implement ABC system (Anguita et

al. 2012). This type of the model will help the administration to allocate various costs of the

administration to the services and products that the organisation provides. The main advantages

that the ABC system will contribute to the management at TILT Renewable Limited are as

follows: It will enable the administration to identify costs provided by various departments of the

organisation as well as efficient use of services that are more costly. The product managers will

also make use of the information that relates to cost to design products more cost-effectively.

Cost information will also improve product pricing in the organisation (Amid, Ghodsypour and

O’Brien 2011). Activity-based costing system can also help the management in fixing the prices

of most of their products (setting selling prices). The implementation process of the model to the

organisation requires proper planning before and after the implementation process. The

management should also teach all the employees on how the Model will function. The teaching

process will enable every employee to understand the implementation process of the model.

Activity Based Costing can provide solutions to the problems that the organisations are facing

(Pinto 2010).

Executive Summary

This paper discusses how Activity-based costing can help the accounting information of

the management in TILT Renewables Limited. The control of The TILT Renewable Limited

should apply the use of the sophisticated cost information that can make them quick decisions in

the organisation. Given the high rate of competition in the industry and the need to reduce the

costs, the management of TILT Renewable Limited needs to implement ABC system (Anguita et

al. 2012). This type of the model will help the administration to allocate various costs of the

administration to the services and products that the organisation provides. The main advantages

that the ABC system will contribute to the management at TILT Renewable Limited are as

follows: It will enable the administration to identify costs provided by various departments of the

organisation as well as efficient use of services that are more costly. The product managers will

also make use of the information that relates to cost to design products more cost-effectively.

Cost information will also improve product pricing in the organisation (Amid, Ghodsypour and

O’Brien 2011). Activity-based costing system can also help the management in fixing the prices

of most of their products (setting selling prices). The implementation process of the model to the

organisation requires proper planning before and after the implementation process. The

management should also teach all the employees on how the Model will function. The teaching

process will enable every employee to understand the implementation process of the model.

Activity Based Costing can provide solutions to the problems that the organisations are facing

(Pinto 2010).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity Based Costing 4

Introduction

The paper discusses how the management can apply the ABC system to improve the

performance of the TILT Renewables Limited. The company is well known in the provision

of the energy generation, and it also tries to be the leading owner, developer as well as the

manager of the production of the renewable energy in both New Zealand and Australia.

Over the past few years, the TLT has reduced its level of return; this is due to the problem

in financial leverage which in turn impact Return on equity which then affects the overall

profits of the Company. The organisation can only improve the performance by

implementing Activity Based Costing system. To help explained how ABC could enhance

the performance of the TILT Renewable Limited; the paper is divided into sections with

each part illustrating the Activity-based costing method. The paper explains Activity-based

costing system as well as its features; also, it also discusses the benefits that are associated

with the model in the TILT Renewables Limited. It also describes how activity-based

costing supports the current strategies and goals of the institution and then provides a

recommendation that should be put in place to ensure effective implementation of the ABC

system (Lin et al. 2017). Lastly, the paper proposes the alternative accounting tool that is

appropriate for TILT Renewables Limited.

Description of Activity-based costing and its features

Introduction

The paper discusses how the management can apply the ABC system to improve the

performance of the TILT Renewables Limited. The company is well known in the provision

of the energy generation, and it also tries to be the leading owner, developer as well as the

manager of the production of the renewable energy in both New Zealand and Australia.

Over the past few years, the TLT has reduced its level of return; this is due to the problem

in financial leverage which in turn impact Return on equity which then affects the overall

profits of the Company. The organisation can only improve the performance by

implementing Activity Based Costing system. To help explained how ABC could enhance

the performance of the TILT Renewable Limited; the paper is divided into sections with

each part illustrating the Activity-based costing method. The paper explains Activity-based

costing system as well as its features; also, it also discusses the benefits that are associated

with the model in the TILT Renewables Limited. It also describes how activity-based

costing supports the current strategies and goals of the institution and then provides a

recommendation that should be put in place to ensure effective implementation of the ABC

system (Lin et al. 2017). Lastly, the paper proposes the alternative accounting tool that is

appropriate for TILT Renewables Limited.

Description of Activity-based costing and its features

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity Based Costing 5

ABC system is accounting tool that helps in assigning the organization’s overhead to

those specific items that uses it. The model assists in identification of activities in the

institution and then apportions each cost of every activity with all the resources to all

services and products according to how each have been used. Usually, the model allocates

more overhead (indirect cost) into direct cost than the Traditional Costing method. It is

also an approach to the monitoring and costing of activities that involves finding the

consumption of resources as well as costing the final output. ABC was developed to provide

solution to the problems that are related to traditional cost management. The system can

be used as a method of reducing the costs of the overhead (Verhagen, Bermell, van and

Curran 2012). The model performs well in a complex environment, that contains many

products and machines, as well as tangled processes that cannot be sorted out efficiently

(Tavana, Yazdani and Caprio 2017). ABC model cannot efficiently perform well in a

streamlined environment that is made up of production processes that are abbreviated

(Nguyen and Aiello 2013). This model is mostly applied in the manufacturing companies

because it improves the consistency of cost data. This can make the Company to easily

classify all the costs that are incurred as well as producing exact expenses during the

production process. The model is performing its function by arranging the machines for

designing products, production, and distributing operating devices or finished goods

(DRURY 2013). The activity-based costing enhances costing process in the organisation in

three Main ways. The first way is that it increases the actual total of the costs pool that is

being used to accumulate overhead costs. Instead of assembling all expenses that are

associated with the production in one basin, it apportions costs by activity. It also helps in

creating bases for allocating overhead costs to those items. Lastly, Activity-based costing

ABC system is accounting tool that helps in assigning the organization’s overhead to

those specific items that uses it. The model assists in identification of activities in the

institution and then apportions each cost of every activity with all the resources to all

services and products according to how each have been used. Usually, the model allocates

more overhead (indirect cost) into direct cost than the Traditional Costing method. It is

also an approach to the monitoring and costing of activities that involves finding the

consumption of resources as well as costing the final output. ABC was developed to provide

solution to the problems that are related to traditional cost management. The system can

be used as a method of reducing the costs of the overhead (Verhagen, Bermell, van and

Curran 2012). The model performs well in a complex environment, that contains many

products and machines, as well as tangled processes that cannot be sorted out efficiently

(Tavana, Yazdani and Caprio 2017). ABC model cannot efficiently perform well in a

streamlined environment that is made up of production processes that are abbreviated

(Nguyen and Aiello 2013). This model is mostly applied in the manufacturing companies

because it improves the consistency of cost data. This can make the Company to easily

classify all the costs that are incurred as well as producing exact expenses during the

production process. The model is performing its function by arranging the machines for

designing products, production, and distributing operating devices or finished goods

(DRURY 2013). The activity-based costing enhances costing process in the organisation in

three Main ways. The first way is that it increases the actual total of the costs pool that is

being used to accumulate overhead costs. Instead of assembling all expenses that are

associated with the production in one basin, it apportions costs by activity. It also helps in

creating bases for allocating overhead costs to those items. Lastly, Activity-based costing

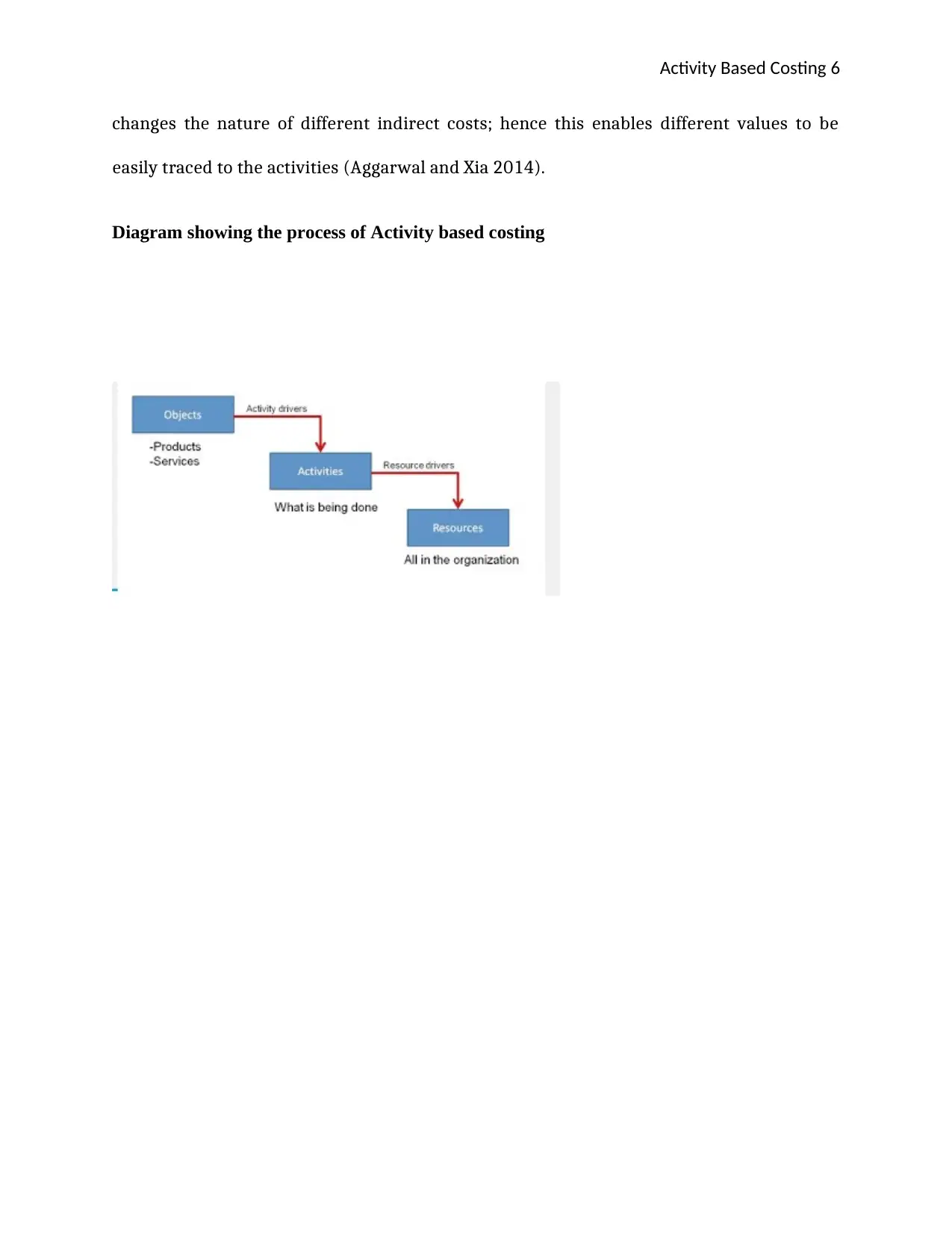

Activity Based Costing 6

changes the nature of different indirect costs; hence this enables different values to be

easily traced to the activities (Aggarwal and Xia 2014).

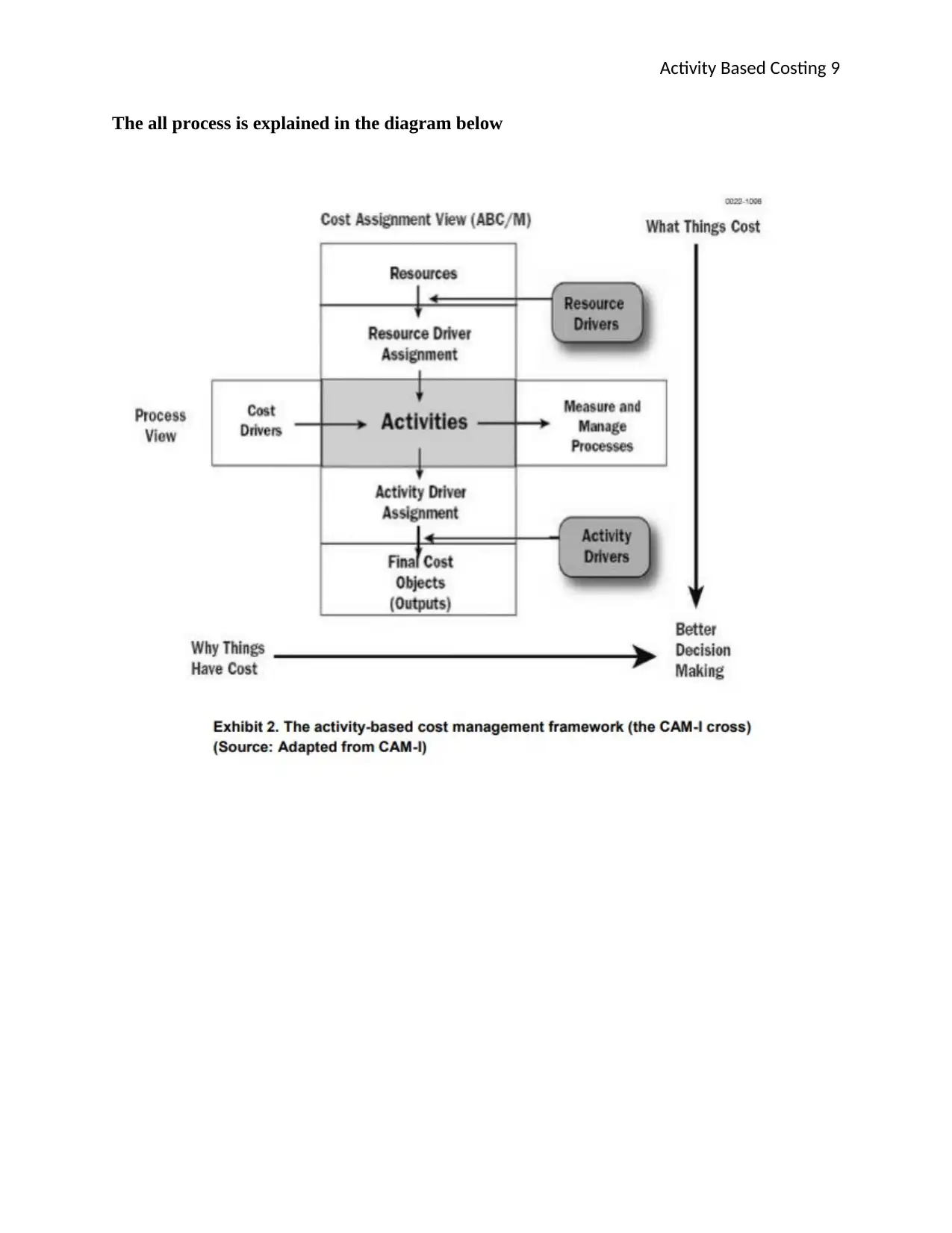

Diagram showing the process of Activity based costing

changes the nature of different indirect costs; hence this enables different values to be

easily traced to the activities (Aggarwal and Xia 2014).

Diagram showing the process of Activity based costing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity Based Costing 7

Description of how Activity-based costing supports the current strategies and

goals of the organisation.

The mission and objectives of the TILT Renewables Limited

The purpose of the company is to provide enough renewable capacity of energy to

all the people in Australia and New Zealand.

The objective of the organisation is to double the total amount of energy being

offered in Australia. The next aim of the organisation is to produce a large quantity of the

renewable energy to both Australia and New Zealand.

Corporate strategy of the TILT Renewable Limited

The primary strategic objective is to create an existing New Zealand and Australian

experience in wind development to help in the implementation of its established pipeline.

The next strategy is to secure market a large of its products both in Australia and New

Zealand. It also tries to acquire development sites and operational wind assets as well the

generation of solar in Australia. The company also attempts to enhance the operational

performance of the available asset base as well as repowering opportunities for any assets.

The company even tries to be number one producer of energy by giving out quality

products to its customers in the market.

How Activity-based costing can help TILT Renewables Limited to attain its

strategies

Description of how Activity-based costing supports the current strategies and

goals of the organisation.

The mission and objectives of the TILT Renewables Limited

The purpose of the company is to provide enough renewable capacity of energy to

all the people in Australia and New Zealand.

The objective of the organisation is to double the total amount of energy being

offered in Australia. The next aim of the organisation is to produce a large quantity of the

renewable energy to both Australia and New Zealand.

Corporate strategy of the TILT Renewable Limited

The primary strategic objective is to create an existing New Zealand and Australian

experience in wind development to help in the implementation of its established pipeline.

The next strategy is to secure market a large of its products both in Australia and New

Zealand. It also tries to acquire development sites and operational wind assets as well the

generation of solar in Australia. The company also attempts to enhance the operational

performance of the available asset base as well as repowering opportunities for any assets.

The company even tries to be number one producer of energy by giving out quality

products to its customers in the market.

How Activity-based costing can help TILT Renewables Limited to attain its

strategies

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity Based Costing 8

Activity-based costing will add value to the company when it uses it as the source of

information for improving and managing the business. It will provide the organisation with

a valuable tool probably the most powerful tool that will enhance the performance of the

organisation. The model will provide the methods and ways of improving the profitability

of the organisation (Taticchi, Tonelli and Cagnazzo 2010). When the management

combined other alternatives accounting tools such as just-in-time, BPR, total quality

management and financial management system must be used together with the ABC

system for TILT Company to, improve business performance (Ding, Zhou and Akinci 2014).

The management will attain the strategies put in place since it will be able to identify how

different costs of activities are being consumed as well as understanding the composition

of their output. With the use of the model, the Company will respond very first with the

changing business environment that requires quick responsive to the expectation of the

customers. The Company will be able to provide appropriate products to its Customers that

are in Australia and other parts of the world. Activity-based costing will also enable the

strategic management decisions, for example, product mix and pricing (Shander et al.

2010). The accuracy of the of the cost of output will help the Managers to come up with

better decisions on process improvements, customer mix, product design and market

segment. The company will be capable of determining accurate measurements of its

performance with the intention of finding out departments within the organization that

needs still needs improvements for the better performance of all the Organization. The

model will help the organization to find out accurate costs and then developed ways of how

to control those costs to ensure that there is improvement in the organization

(Chiadamrong 2017).

Activity-based costing will add value to the company when it uses it as the source of

information for improving and managing the business. It will provide the organisation with

a valuable tool probably the most powerful tool that will enhance the performance of the

organisation. The model will provide the methods and ways of improving the profitability

of the organisation (Taticchi, Tonelli and Cagnazzo 2010). When the management

combined other alternatives accounting tools such as just-in-time, BPR, total quality

management and financial management system must be used together with the ABC

system for TILT Company to, improve business performance (Ding, Zhou and Akinci 2014).

The management will attain the strategies put in place since it will be able to identify how

different costs of activities are being consumed as well as understanding the composition

of their output. With the use of the model, the Company will respond very first with the

changing business environment that requires quick responsive to the expectation of the

customers. The Company will be able to provide appropriate products to its Customers that

are in Australia and other parts of the world. Activity-based costing will also enable the

strategic management decisions, for example, product mix and pricing (Shander et al.

2010). The accuracy of the of the cost of output will help the Managers to come up with

better decisions on process improvements, customer mix, product design and market

segment. The company will be capable of determining accurate measurements of its

performance with the intention of finding out departments within the organization that

needs still needs improvements for the better performance of all the Organization. The

model will help the organization to find out accurate costs and then developed ways of how

to control those costs to ensure that there is improvement in the organization

(Chiadamrong 2017).

Activity Based Costing 9

The all process is explained in the diagram below

The all process is explained in the diagram below

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity Based Costing 10

Recommendation about the implementation of Activity Based Costing in the

organisation

Training of all the employees and the general manager is the essential factor as the

training process will assist the employees to have a good understanding of how Activity-

based costing system varies from the existing accounting cost being used by the

organisation or from the traditional accounting costs (Garrison, Noreen, Brewer and

McGowan 2010). The employees should also be given training on the processes, goals and

benefits of the Activity-based costing implementation. This remains important since it

improves the confidence as well as helping them to a positive outlook concerning

implementation process. TILT Renewables Limited should allocate enough funds to

facilitate the training process of all the employees who have to gain the knowledge and

skills about the Activity-based costing implementation. The training process should not be

made up of the measurements and review procedures but should also include methods of

solving problems for example effect and causes analysis. The analysis will assist in

identification of the correlation between different costs in the organisation.

Recommendation about the implementation of Activity Based Costing in the

organisation

Training of all the employees and the general manager is the essential factor as the

training process will assist the employees to have a good understanding of how Activity-

based costing system varies from the existing accounting cost being used by the

organisation or from the traditional accounting costs (Garrison, Noreen, Brewer and

McGowan 2010). The employees should also be given training on the processes, goals and

benefits of the Activity-based costing implementation. This remains important since it

improves the confidence as well as helping them to a positive outlook concerning

implementation process. TILT Renewables Limited should allocate enough funds to

facilitate the training process of all the employees who have to gain the knowledge and

skills about the Activity-based costing implementation. The training process should not be

made up of the measurements and review procedures but should also include methods of

solving problems for example effect and causes analysis. The analysis will assist in

identification of the correlation between different costs in the organisation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity Based Costing 11

Active support of the management is vital in the effective implementation of

Activity-based costing (ABC) system. The administration should provide means of

application and enough resources that can facilitate all process of ABC implementation. The

resources mainly include the commitment and time of the accountants, operating

employees, top management, external consultant and software. The implementation

process also consume a lot of time. The amount of time take to fully complete all the stages

of the ABC system will depend on the size of the organization. TILT Renewable Limited is a

large organization hence it will take a lot of time for the implementation process to be

completed. One of the most essential factors that will lead to the success of the ABC system

is having enough employees in the organization. Other resources, for example custom-

made or commercial software as well as external consultants are not so essential to the

effective implementation of the ABC (Dale and Plunkett 2017). The management should

also offer enough support to staff to ensure smooth implementation of the Activity-based

costing into the organisation. The support may be in the form of monetary or advice. They

should respond to the need of any employee in the organisation by giving them the

necessary relating to the Activity-based costing. This is because the employees are the

cornerstones of any successful organization. Therefore, the management should respond to

their problems for smooth implementation of the model

The management tool apart from Activity-based costing that is more appropriate to

TILT Renewables Limited

Active support of the management is vital in the effective implementation of

Activity-based costing (ABC) system. The administration should provide means of

application and enough resources that can facilitate all process of ABC implementation. The

resources mainly include the commitment and time of the accountants, operating

employees, top management, external consultant and software. The implementation

process also consume a lot of time. The amount of time take to fully complete all the stages

of the ABC system will depend on the size of the organization. TILT Renewable Limited is a

large organization hence it will take a lot of time for the implementation process to be

completed. One of the most essential factors that will lead to the success of the ABC system

is having enough employees in the organization. Other resources, for example custom-

made or commercial software as well as external consultants are not so essential to the

effective implementation of the ABC (Dale and Plunkett 2017). The management should

also offer enough support to staff to ensure smooth implementation of the Activity-based

costing into the organisation. The support may be in the form of monetary or advice. They

should respond to the need of any employee in the organisation by giving them the

necessary relating to the Activity-based costing. This is because the employees are the

cornerstones of any successful organization. Therefore, the management should respond to

their problems for smooth implementation of the model

The management tool apart from Activity-based costing that is more appropriate to

TILT Renewables Limited

Activity Based Costing 12

TILT Renewable Limited should adopt the use of the Just-in-time inventory system

to assist in the improvements of the efficiency of the organisation as well as reducing the

costs. The system will require the Tilt Renewable Limited to purchase the products when

there is a demand in the market (Lange et al. 2011). It will enable the organization to

establish a correlation with sellers to ensure that products reach the organization in time

for the preparation according to the needs of the customers. It will also ensure that

production is made according to the orders of the customers and this will help to eliminate

wastage. This model will not allow TILT Company to store or generate excess products. It

will also require the management and other members of the organization to work as a team

with the aim of delivering according to the goals of the organization. It will enable the

administration to find simple solutions for any problems that the organisation might

encounter in the future. Just-in-time will also allow all the members of the organisation to

concentrate only on the tasks that every member performs. It also motivates every worker

to analyze the processes and then provide suggestions that can improve the performance of

the organization (Chen, Hoey, Nugent, Cook and Yu 2012).

Conclusion

TILT Renewable Limited should adopt the use of the Just-in-time inventory system

to assist in the improvements of the efficiency of the organisation as well as reducing the

costs. The system will require the Tilt Renewable Limited to purchase the products when

there is a demand in the market (Lange et al. 2011). It will enable the organization to

establish a correlation with sellers to ensure that products reach the organization in time

for the preparation according to the needs of the customers. It will also ensure that

production is made according to the orders of the customers and this will help to eliminate

wastage. This model will not allow TILT Company to store or generate excess products. It

will also require the management and other members of the organization to work as a team

with the aim of delivering according to the goals of the organization. It will enable the

administration to find simple solutions for any problems that the organisation might

encounter in the future. Just-in-time will also allow all the members of the organisation to

concentrate only on the tasks that every member performs. It also motivates every worker

to analyze the processes and then provide suggestions that can improve the performance of

the organization (Chen, Hoey, Nugent, Cook and Yu 2012).

Conclusion

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.