HI5017 Managerial Accounting Report: ABC Analysis and Implications

VerifiedAdded on 2023/06/04

|17

|3704

|134

Report

AI Summary

This report examines the implications of Activity Based Costing (ABC) in managerial accounting. It analyzes two journal articles focusing on ABC's application and benefits in different business contexts. The report evaluates the articles, identifying similarities and differences, and extracts key outcomes applicable to Australian management accountants. The analysis covers the process of ABC, its advantages over traditional costing methods, and its role in improving cost reporting and decision-making. The report highlights how ABC can enhance cost allocation, improve cost structure, and provide more accurate cost information, ultimately aiding businesses in effective cost management and strategic planning. Furthermore, the report addresses how ABC can be implemented in various sectors, including service and public sector organizations, and provides practical insights for improving cost management practices.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGERIAL ACCOUNTING

Executive Summary

The main purpose of this report is to analyze the implications of Activity based costing

techniques in a business. In order to effective analyze the topic, the assessment considers two

journal articles which are ion different companies on which the analysis are to be conducted.

The journal articles which are considered are on Activity based costing application in a business

and how the same helps a business to improve the reporting of costs of the business. The key

outcomes which are derived from the analysis are suggested to management professionals in

Australia in order to make improvement there.

MANAGERIAL ACCOUNTING

Executive Summary

The main purpose of this report is to analyze the implications of Activity based costing

techniques in a business. In order to effective analyze the topic, the assessment considers two

journal articles which are ion different companies on which the analysis are to be conducted.

The journal articles which are considered are on Activity based costing application in a business

and how the same helps a business to improve the reporting of costs of the business. The key

outcomes which are derived from the analysis are suggested to management professionals in

Australia in order to make improvement there.

2

MANAGERIAL ACCOUNTING

Table of Contents

Introduction.....................................................................................................................................3

Process of Activity Based Costing....................................................................................................4

Analysis of Two Journal Articles......................................................................................................5

Evaluation of Journal Article 1.....................................................................................................5

Evaluation of Journal Article 2.....................................................................................................7

Similarities and Dissimilarities between the two Articles.............................................................10

Four Specific Outcomes from the Research Papers which can Help Australian Management

Accountants...................................................................................................................................11

Conclusion......................................................................................................................................13

Reference.......................................................................................................................................15

MANAGERIAL ACCOUNTING

Table of Contents

Introduction.....................................................................................................................................3

Process of Activity Based Costing....................................................................................................4

Analysis of Two Journal Articles......................................................................................................5

Evaluation of Journal Article 1.....................................................................................................5

Evaluation of Journal Article 2.....................................................................................................7

Similarities and Dissimilarities between the two Articles.............................................................10

Four Specific Outcomes from the Research Papers which can Help Australian Management

Accountants...................................................................................................................................11

Conclusion......................................................................................................................................13

Reference.......................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGERIAL ACCOUNTING

Introduction

In todays world’s, the business environment is going at an increasing pace and most of

the business are focusing on making more and more profits. In such a situation, as the sales of

the business increase so does the variable costs which are associated with the sale. Therefore,

it is very important for the business to choose an appropriate costing technique which can

effectively record and analyze the costs of the business. The treatment of overhead costs of the

business are important aspects which needs to be considered by the management and

appropriate allocation of such costs are also important. In the new era of modernization, most

of the business are utilizing activity-based costing techniques for the purpose of identifying and

allocating costs of the business (Stefano and Casarotto Filho 2013). Traditional costing

techniques are unable to keep up with the changing environment of businesses and therefore

activity-based costing techniques helps businesses to overcome the deficiencies of traditional

costing techniques and also helps in decision making process of the business.

Activity based costing techniques allows business to effectively apportion the costs of

the business which are indirect in nature on the basis of the activities which are undertaken by

the business for production the products of the business. Activity based costing is also

applicable for organizations which are engaged in the manufacture of multiple products of a

business (Estampe et al. 2013). Activity based costing techniques of a business allows the

management of companies to identify the costs and its respective activity and allocate on the

basis of the same (Kaplan 2014). The working process of activity-based costing technique is

unique in nature than traditional costing techniques which only considers machine hour as the

MANAGERIAL ACCOUNTING

Introduction

In todays world’s, the business environment is going at an increasing pace and most of

the business are focusing on making more and more profits. In such a situation, as the sales of

the business increase so does the variable costs which are associated with the sale. Therefore,

it is very important for the business to choose an appropriate costing technique which can

effectively record and analyze the costs of the business. The treatment of overhead costs of the

business are important aspects which needs to be considered by the management and

appropriate allocation of such costs are also important. In the new era of modernization, most

of the business are utilizing activity-based costing techniques for the purpose of identifying and

allocating costs of the business (Stefano and Casarotto Filho 2013). Traditional costing

techniques are unable to keep up with the changing environment of businesses and therefore

activity-based costing techniques helps businesses to overcome the deficiencies of traditional

costing techniques and also helps in decision making process of the business.

Activity based costing techniques allows business to effectively apportion the costs of

the business which are indirect in nature on the basis of the activities which are undertaken by

the business for production the products of the business. Activity based costing is also

applicable for organizations which are engaged in the manufacture of multiple products of a

business (Estampe et al. 2013). Activity based costing techniques of a business allows the

management of companies to identify the costs and its respective activity and allocate on the

basis of the same (Kaplan 2014). The working process of activity-based costing technique is

unique in nature than traditional costing techniques which only considers machine hour as the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGERIAL ACCOUNTING

basis for allocating the costs of the business. In case of activity-based costing the nature if

activity is considered and then the respective cost unit is identified by the business.

Process of Activity Based Costing

Activity based costing is an efficient way of allocating costs to respective cost drivers of

the business and also helps in the decision-making process of the business. Activity based

costing techniques also plays a vital role in setting the selling price of the products which are

manufactured by the business. In details, Activity based costing the costs which are incurred by

the business are classified on the basis of short term costs and long-term costs of the business

(Frazier 2014). The short term costs of the business are generally allocated on the basis of the

volume related cost drivers of the business. Some of the examples which can be provided for

volume related cost drivers are machine hours, labour hours and direct material cost. In case of

long-term variable costs, the first step is to identify and analyze the nature of the costs and the

activity which incurs such costs (Donovan et al. 2014).

The objectives of Activity based costing in a business environment are listed below in

details:

The new costing system aims to rectify the inaccuracies of the traditional costing system

which is related to recording a cost of the business.

The method aims to improve the allocation of costs of the business which can be done

by linking the costs which is incurred by a business to its respective activity.

MANAGERIAL ACCOUNTING

basis for allocating the costs of the business. In case of activity-based costing the nature if

activity is considered and then the respective cost unit is identified by the business.

Process of Activity Based Costing

Activity based costing is an efficient way of allocating costs to respective cost drivers of

the business and also helps in the decision-making process of the business. Activity based

costing techniques also plays a vital role in setting the selling price of the products which are

manufactured by the business. In details, Activity based costing the costs which are incurred by

the business are classified on the basis of short term costs and long-term costs of the business

(Frazier 2014). The short term costs of the business are generally allocated on the basis of the

volume related cost drivers of the business. Some of the examples which can be provided for

volume related cost drivers are machine hours, labour hours and direct material cost. In case of

long-term variable costs, the first step is to identify and analyze the nature of the costs and the

activity which incurs such costs (Donovan et al. 2014).

The objectives of Activity based costing in a business environment are listed below in

details:

The new costing system aims to rectify the inaccuracies of the traditional costing system

which is related to recording a cost of the business.

The method aims to improve the allocation of costs of the business which can be done

by linking the costs which is incurred by a business to its respective activity.

5

MANAGERIAL ACCOUNTING

The method also focuses on helping the management of a company to effectively take

decisions regarding the costs of the business and also deciding the selling price of the

product (Laguna and Marklund 2013).

Activity based costing brings about more effective disclosures of costs of the business

and also improve the costs structure of the business.

Analysis of Two Journal Articles

In order to effectively analyze the system of Activity based costing, research papers

written by different authors are considered. The journal article will further explain the

application and usefulness of Activity based costing in a business. The journal article which are

considered for this assessment are listed below:

Article 1: “Activity Based Costing in Services Industry: A Conceptual Framework for

Entrepreneurs”

Article 2: “Activity based costing (ABC) in the public sector: Benefits and challenges”

The above journal deals with organization which operates in different sector entirely.

The journal article portrays and gives more insights into the process of Activity based costing.

Evaluation of Journal Article 1

As per the journal paper, the focus of the researcher is on a service sector industry. Just

as the business engaged in manufacturing industry has attained growth in recent years so has

the service sector industries in the country. The author has effectively identified that in the

changing environment, the overall increase in the scale of operations results in tremendous

MANAGERIAL ACCOUNTING

The method also focuses on helping the management of a company to effectively take

decisions regarding the costs of the business and also deciding the selling price of the

product (Laguna and Marklund 2013).

Activity based costing brings about more effective disclosures of costs of the business

and also improve the costs structure of the business.

Analysis of Two Journal Articles

In order to effectively analyze the system of Activity based costing, research papers

written by different authors are considered. The journal article will further explain the

application and usefulness of Activity based costing in a business. The journal article which are

considered for this assessment are listed below:

Article 1: “Activity Based Costing in Services Industry: A Conceptual Framework for

Entrepreneurs”

Article 2: “Activity based costing (ABC) in the public sector: Benefits and challenges”

The above journal deals with organization which operates in different sector entirely.

The journal article portrays and gives more insights into the process of Activity based costing.

Evaluation of Journal Article 1

As per the journal paper, the focus of the researcher is on a service sector industry. Just

as the business engaged in manufacturing industry has attained growth in recent years so has

the service sector industries in the country. The author has effectively identified that in the

changing environment, the overall increase in the scale of operations results in tremendous

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MANAGERIAL ACCOUNTING

increase in the costs which are associated with the business. Most of the businesses suffer from

problems in managing the profit margins and cost of the business (Ross 2016). Therefore, it is

an essential requirement of businesses to select an appropriate cost management system

which can effectively and accurately show the costs which re incurred by the business during

the year.

The research paper shows the costing techniques which are used in a business

environment and how the same can reported and used for the decision-making process of the

business. The journal paper effectively describes the Activity based costing and the key steps

which are followed by businesses for identifying the cost components and also the key cost

drivers of the business. The research paper further shows that the points of difference between

t6raditional costing system and Activity based costing system (Onat, Anitsal and Anitsal 2014).

The main deficiencies of the traditional costing system which can be identified is that the

costing process is unable to detect non-financial factors which can affect a business, inaccurate

cost information which is generated by the traditional system. The journal paper specifically

identifies that traditional costing system is inappropriate for a business which is engaged in

service industry. Therefore, the researcher is of the opinion that Activity based costing is best

available option for service sector business in order to effectively treat the costs which are

incurred in a service sector business. The journal paper highlights certain advantages which is

related to application of Activity based costing in a service sector business which are brings

about better presentation of the costs of the business, cost reductions, improve the costing for

the product and also helps in the decision-making process of the business.

MANAGERIAL ACCOUNTING

increase in the costs which are associated with the business. Most of the businesses suffer from

problems in managing the profit margins and cost of the business (Ross 2016). Therefore, it is

an essential requirement of businesses to select an appropriate cost management system

which can effectively and accurately show the costs which re incurred by the business during

the year.

The research paper shows the costing techniques which are used in a business

environment and how the same can reported and used for the decision-making process of the

business. The journal paper effectively describes the Activity based costing and the key steps

which are followed by businesses for identifying the cost components and also the key cost

drivers of the business. The research paper further shows that the points of difference between

t6raditional costing system and Activity based costing system (Onat, Anitsal and Anitsal 2014).

The main deficiencies of the traditional costing system which can be identified is that the

costing process is unable to detect non-financial factors which can affect a business, inaccurate

cost information which is generated by the traditional system. The journal paper specifically

identifies that traditional costing system is inappropriate for a business which is engaged in

service industry. Therefore, the researcher is of the opinion that Activity based costing is best

available option for service sector business in order to effectively treat the costs which are

incurred in a service sector business. The journal paper highlights certain advantages which is

related to application of Activity based costing in a service sector business which are brings

about better presentation of the costs of the business, cost reductions, improve the costing for

the product and also helps in the decision-making process of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGERIAL ACCOUNTING

Thus, the above discussion effectively shows the superiority of Activity based costing in

comparison to traditional costing system. The advantages of Activity based costing are

effectively shown by the researcher in the journal paper and outline the reasons due to which

service sector enterprises can effectively implement such a process (Dumas et al. 2013). The

analysis also reveals the process which is applied while following Activity based costing in a

business. The further research question which arises from the analysis of the journal paper are

listed below:

1. How does Activity based costing helps in a decision making process?

2. Detailed analysis of the difference which exist in a business which is using traditional

costing system and a business which is using Activity based costing

3. What are the relevant cost drivers which can be identified in a service sector industry?

Evaluation of Journal Article 2

As per the Journal which is shown in the research paper clearly shows the comparation

which is shown between traditional costing system and Activity based costing system when

applied in a business. The journal also lists out the advantages which are associated with the

method of Activity based costing. The journal shows the implementation of Activity based

costing technique in a public sector enterprise.

The problem statement of the research paper shows that many of the researchers and

academician are of the opinion that Activity based costing are only useful in businesses which

have large business size and has a large scale of operations or on a business which is engaged in

the production of multiple goods or products or offer various services to the customers.

MANAGERIAL ACCOUNTING

Thus, the above discussion effectively shows the superiority of Activity based costing in

comparison to traditional costing system. The advantages of Activity based costing are

effectively shown by the researcher in the journal paper and outline the reasons due to which

service sector enterprises can effectively implement such a process (Dumas et al. 2013). The

analysis also reveals the process which is applied while following Activity based costing in a

business. The further research question which arises from the analysis of the journal paper are

listed below:

1. How does Activity based costing helps in a decision making process?

2. Detailed analysis of the difference which exist in a business which is using traditional

costing system and a business which is using Activity based costing

3. What are the relevant cost drivers which can be identified in a service sector industry?

Evaluation of Journal Article 2

As per the Journal which is shown in the research paper clearly shows the comparation

which is shown between traditional costing system and Activity based costing system when

applied in a business. The journal also lists out the advantages which are associated with the

method of Activity based costing. The journal shows the implementation of Activity based

costing technique in a public sector enterprise.

The problem statement of the research paper shows that many of the researchers and

academician are of the opinion that Activity based costing are only useful in businesses which

have large business size and has a large scale of operations or on a business which is engaged in

the production of multiple goods or products or offer various services to the customers.

8

MANAGERIAL ACCOUNTING

However, the use of Activity based costing is much more extensive than what is initially

portrayed. The assessment considers a public-sector enterprise which is engaged in providing

services to the general public and the services which are provided are mainly overhead

intensive and therefore the researcher is of the opinion that Activity based costing is a best

option for such sector (Oseifuah 2014). The researcher further states that implementation of

such costing practice will bring about transparency and accountability of the enterprise. The

research is conducted considering the public-sector enterprises which are operating in South

Africa and which are the grass root for service delivery in South Africa. The research aims to

analyze how Activity based costing can be effectively implemented in the public-sector

enterprises in South Africa.

The journal paper explains the process of traditional costing and how the same is

applied in business. The traditional system of costing is often developed and implemented in

businesses which has either a job process or a process costing system in place. The costs are

allocated and divided on the basis of product which are direct expenses in nature and on the

basis of period which are generally indirect in nature (Warren, Reeve and Duchac 2013). The

apportion of cost is done on the basis of volume-based cost driver which may be machine

hours. The deficiencies which are present in the traditional costing system are also highlighted

in the journal paper.

MANAGERIAL ACCOUNTING

However, the use of Activity based costing is much more extensive than what is initially

portrayed. The assessment considers a public-sector enterprise which is engaged in providing

services to the general public and the services which are provided are mainly overhead

intensive and therefore the researcher is of the opinion that Activity based costing is a best

option for such sector (Oseifuah 2014). The researcher further states that implementation of

such costing practice will bring about transparency and accountability of the enterprise. The

research is conducted considering the public-sector enterprises which are operating in South

Africa and which are the grass root for service delivery in South Africa. The research aims to

analyze how Activity based costing can be effectively implemented in the public-sector

enterprises in South Africa.

The journal paper explains the process of traditional costing and how the same is

applied in business. The traditional system of costing is often developed and implemented in

businesses which has either a job process or a process costing system in place. The costs are

allocated and divided on the basis of product which are direct expenses in nature and on the

basis of period which are generally indirect in nature (Warren, Reeve and Duchac 2013). The

apportion of cost is done on the basis of volume-based cost driver which may be machine

hours. The deficiencies which are present in the traditional costing system are also highlighted

in the journal paper.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MANAGERIAL ACCOUNTING

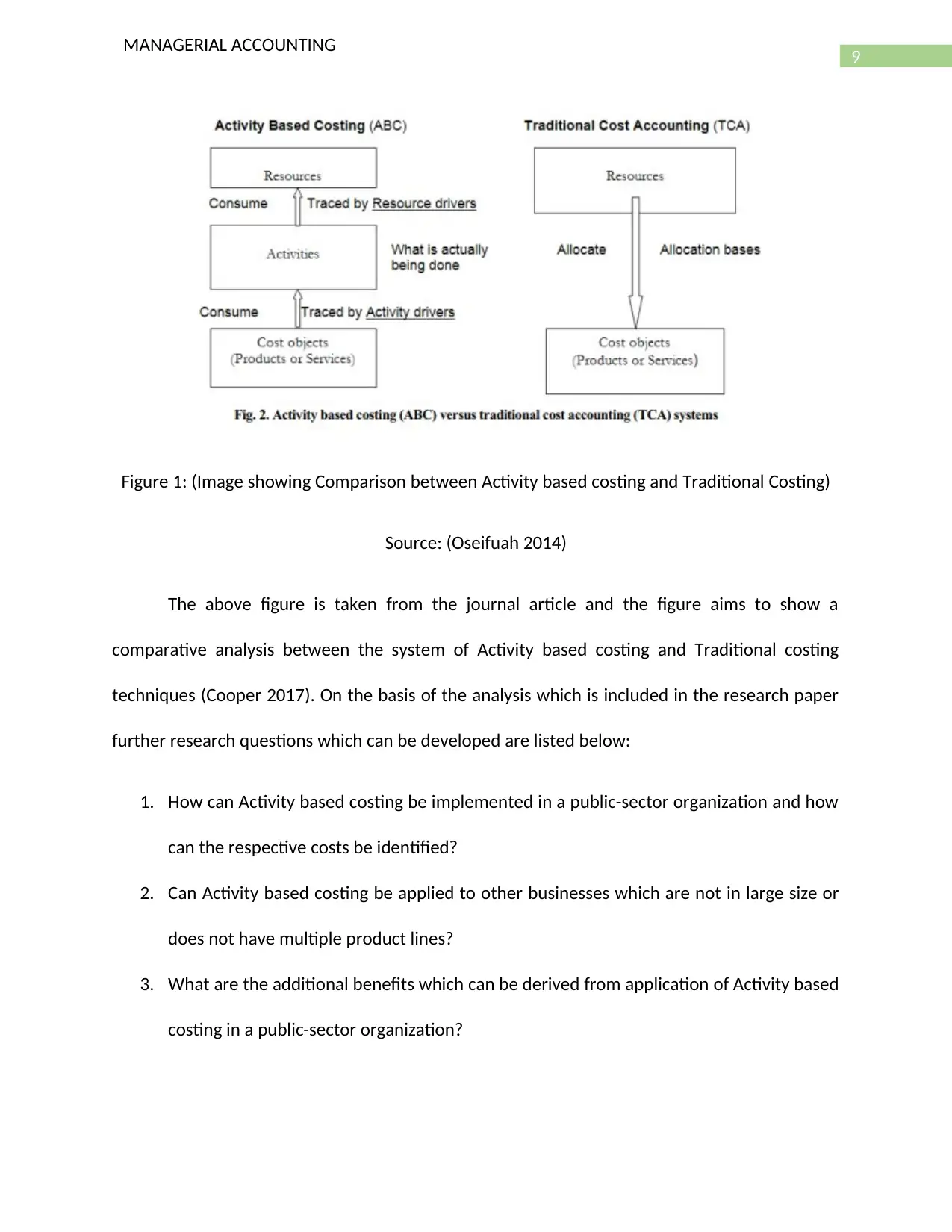

Figure 1: (Image showing Comparison between Activity based costing and Traditional Costing)

Source: (Oseifuah 2014)

The above figure is taken from the journal article and the figure aims to show a

comparative analysis between the system of Activity based costing and Traditional costing

techniques (Cooper 2017). On the basis of the analysis which is included in the research paper

further research questions which can be developed are listed below:

1. How can Activity based costing be implemented in a public-sector organization and how

can the respective costs be identified?

2. Can Activity based costing be applied to other businesses which are not in large size or

does not have multiple product lines?

3. What are the additional benefits which can be derived from application of Activity based

costing in a public-sector organization?

MANAGERIAL ACCOUNTING

Figure 1: (Image showing Comparison between Activity based costing and Traditional Costing)

Source: (Oseifuah 2014)

The above figure is taken from the journal article and the figure aims to show a

comparative analysis between the system of Activity based costing and Traditional costing

techniques (Cooper 2017). On the basis of the analysis which is included in the research paper

further research questions which can be developed are listed below:

1. How can Activity based costing be implemented in a public-sector organization and how

can the respective costs be identified?

2. Can Activity based costing be applied to other businesses which are not in large size or

does not have multiple product lines?

3. What are the additional benefits which can be derived from application of Activity based

costing in a public-sector organization?

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MANAGERIAL ACCOUNTING

Similarities and Dissimilarities between the two Articles

The analysis of the two articles which is shown above reveals certain similarities and

dissimilarities which are present which are listed below in details:

Similarities

Both the articles which are considered for the assessment deals with the application of

Activity based costing in different sector and how the same can bring about

improvements in the reporting framework of the business. The application of Activity

based costing in the organization or sector can bring about improvements and accurate

estimation are justified in the assessment.

The articles which are considered in the assessment both show the deficiencies which

are present in the traditional costing system and also how the application of Activity

based costing can remove such deficiencies. Both the article makes comparison

between the traditional costing system and the modern Activity based costing system

which can bring about improvements in a business.

The advantages of using Activity based costing as a costing technique in the business are

listed out by both the articles. Both the article focuses on strengthening the analysis

which is shown in the research papers with the benefits which are associated with the

use of Activity based costing.

Dissimilarities

MANAGERIAL ACCOUNTING

Similarities and Dissimilarities between the two Articles

The analysis of the two articles which is shown above reveals certain similarities and

dissimilarities which are present which are listed below in details:

Similarities

Both the articles which are considered for the assessment deals with the application of

Activity based costing in different sector and how the same can bring about

improvements in the reporting framework of the business. The application of Activity

based costing in the organization or sector can bring about improvements and accurate

estimation are justified in the assessment.

The articles which are considered in the assessment both show the deficiencies which

are present in the traditional costing system and also how the application of Activity

based costing can remove such deficiencies. Both the article makes comparison

between the traditional costing system and the modern Activity based costing system

which can bring about improvements in a business.

The advantages of using Activity based costing as a costing technique in the business are

listed out by both the articles. Both the article focuses on strengthening the analysis

which is shown in the research papers with the benefits which are associated with the

use of Activity based costing.

Dissimilarities

11

MANAGERIAL ACCOUNTING

In both the paper the company which are considered belong to entirely different

industry and this is the biggest difference between the two articles as the business

structure or even the cost items might not be the same for both the companies or

sector considered. In the first article, the company which is considered is engaged in

service sector industry and so basically the author emphasizes more on service sector

businesses. In case of second article, the emphasis is more on the public-sector

enterprise.

The analysis in both the articles considers different businesses which are engaged in

different service rendering and even the country in which the business operate are also

different.

Four Specific Outcomes from the Research Papers which can Help Australian Management

Accountants

The analysis of the two research papers which is shown above effectively demonstrate

the usefulness of Activity based costing in a business. The positives which are derived from the

journal papers can be suggested to the management professionals who are working in Australia

so that they can also bring about the desired improvement in the business structure of the

companies. The specific outcomes are listed below in details:

Superiority of Activity based costing over Traditional Costing System: The traditional

costing system which is followed in Australia needs to be revised and replaced with

Activity based costing system as the same can bring about significant changes in the

reporting framework which is followed in Australia. It is especially recommended for

MANAGERIAL ACCOUNTING

In both the paper the company which are considered belong to entirely different

industry and this is the biggest difference between the two articles as the business

structure or even the cost items might not be the same for both the companies or

sector considered. In the first article, the company which is considered is engaged in

service sector industry and so basically the author emphasizes more on service sector

businesses. In case of second article, the emphasis is more on the public-sector

enterprise.

The analysis in both the articles considers different businesses which are engaged in

different service rendering and even the country in which the business operate are also

different.

Four Specific Outcomes from the Research Papers which can Help Australian Management

Accountants

The analysis of the two research papers which is shown above effectively demonstrate

the usefulness of Activity based costing in a business. The positives which are derived from the

journal papers can be suggested to the management professionals who are working in Australia

so that they can also bring about the desired improvement in the business structure of the

companies. The specific outcomes are listed below in details:

Superiority of Activity based costing over Traditional Costing System: The traditional

costing system which is followed in Australia needs to be revised and replaced with

Activity based costing system as the same can bring about significant changes in the

reporting framework which is followed in Australia. It is especially recommended for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.