Introduction to Management Accounting: Costing System Analysis Report

VerifiedAdded on 2021/06/14

|12

|2712

|463

Report

AI Summary

This report analyzes the costing methods employed by Sewing Easy Ltd., a company manufacturing sewing machines. The report begins by comparing the traditional costing system with activity-based costing (ABC) to determine why an overseas buyer prefers the advanced model. The analysis includes calculations of cost per unit under both systems, demonstrating the impact of different costing methods on profit and loss. The report highlights the importance of accurate product costing for informed decision-making, including pricing strategies and product introduction or removal. It also addresses the handling of over- and under-applied overheads. Furthermore, the report outlines the benefits and limitations of the ABC system, emphasizing its advantages in accurate costing, effective overhead management, and improved decision-making, while acknowledging its complexity and implementation costs. The report concludes by showcasing how ABC can improve product and customer profitability analysis, aiding in better allocation of overheads, and helping in identifying spare capacity.

INTRODUCTION TO

MANAGEMENT

ACCOUNTING

ASSIGNMENT

MANAGEMENT

ACCOUNTING

ASSIGNMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

2

Executive Summary

In the given assignment, a report has been prepared on the costing of the products, where the

company is currently using the traditional costing system and the same has been compared with

activity based costing in terms of costing of the 2 products. The difference between the two has

been analysed theoretically as well as practically and importance of the accurate costing has been

shown in the report. The ways of dealing with the under and over application of the overhead has

also been shown in the report. Finally the main benefits and the limitations of the ABC system

has also been shown at the end.

2 | P a g e

Executive Summary

In the given assignment, a report has been prepared on the costing of the products, where the

company is currently using the traditional costing system and the same has been compared with

activity based costing in terms of costing of the 2 products. The difference between the two has

been analysed theoretically as well as practically and importance of the accurate costing has been

shown in the report. The ways of dealing with the under and over application of the overhead has

also been shown in the report. Finally the main benefits and the limitations of the ABC system

has also been shown at the end.

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Contents

Background..................................................................................................................................................4

Analysis........................................................................................................................................................4

References.................................................................................................................................................10

3 | P a g e

Contents

Background..................................................................................................................................................4

Analysis........................................................................................................................................................4

References.................................................................................................................................................10

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

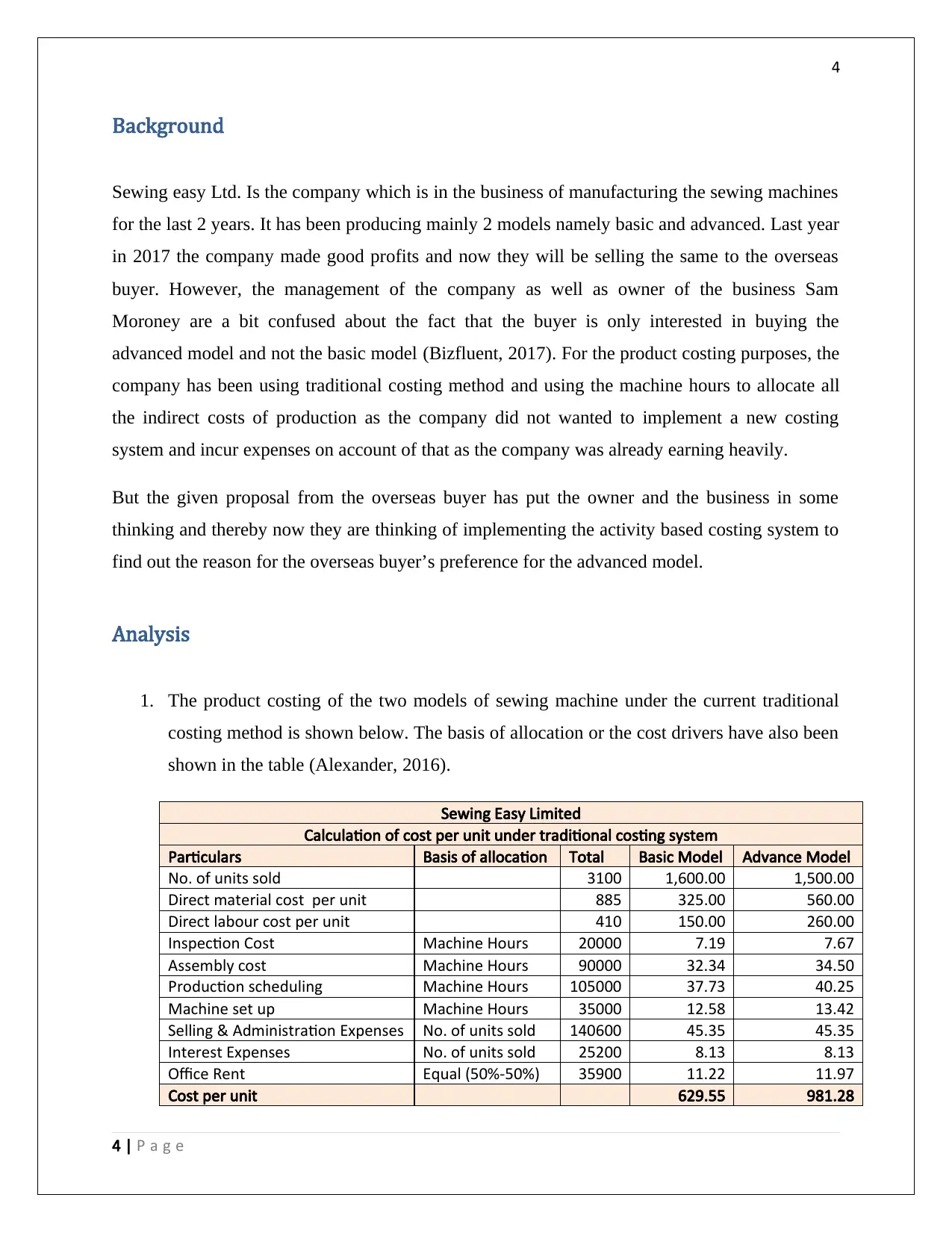

Background

Sewing easy Ltd. Is the company which is in the business of manufacturing the sewing machines

for the last 2 years. It has been producing mainly 2 models namely basic and advanced. Last year

in 2017 the company made good profits and now they will be selling the same to the overseas

buyer. However, the management of the company as well as owner of the business Sam

Moroney are a bit confused about the fact that the buyer is only interested in buying the

advanced model and not the basic model (Bizfluent, 2017). For the product costing purposes, the

company has been using traditional costing method and using the machine hours to allocate all

the indirect costs of production as the company did not wanted to implement a new costing

system and incur expenses on account of that as the company was already earning heavily.

But the given proposal from the overseas buyer has put the owner and the business in some

thinking and thereby now they are thinking of implementing the activity based costing system to

find out the reason for the overseas buyer’s preference for the advanced model.

Analysis

1. The product costing of the two models of sewing machine under the current traditional

costing method is shown below. The basis of allocation or the cost drivers have also been

shown in the table (Alexander, 2016).

Sewing Easy Limited

Calculation of cost per unit under traditional costing system

Particulars Basis of allocation Total Basic Model Advance Model

No. of units sold 3100 1,600.00 1,500.00

Direct material cost per unit 885 325.00 560.00

Direct labour cost per unit 410 150.00 260.00

Inspection Cost Machine Hours 20000 7.19 7.67

Assembly cost Machine Hours 90000 32.34 34.50

Production scheduling Machine Hours 105000 37.73 40.25

Machine set up Machine Hours 35000 12.58 13.42

Selling & Administration Expenses No. of units sold 140600 45.35 45.35

Interest Expenses No. of units sold 25200 8.13 8.13

Office Rent Equal (50%-50%) 35900 11.22 11.97

Cost per unit 629.55 981.28

4 | P a g e

Background

Sewing easy Ltd. Is the company which is in the business of manufacturing the sewing machines

for the last 2 years. It has been producing mainly 2 models namely basic and advanced. Last year

in 2017 the company made good profits and now they will be selling the same to the overseas

buyer. However, the management of the company as well as owner of the business Sam

Moroney are a bit confused about the fact that the buyer is only interested in buying the

advanced model and not the basic model (Bizfluent, 2017). For the product costing purposes, the

company has been using traditional costing method and using the machine hours to allocate all

the indirect costs of production as the company did not wanted to implement a new costing

system and incur expenses on account of that as the company was already earning heavily.

But the given proposal from the overseas buyer has put the owner and the business in some

thinking and thereby now they are thinking of implementing the activity based costing system to

find out the reason for the overseas buyer’s preference for the advanced model.

Analysis

1. The product costing of the two models of sewing machine under the current traditional

costing method is shown below. The basis of allocation or the cost drivers have also been

shown in the table (Alexander, 2016).

Sewing Easy Limited

Calculation of cost per unit under traditional costing system

Particulars Basis of allocation Total Basic Model Advance Model

No. of units sold 3100 1,600.00 1,500.00

Direct material cost per unit 885 325.00 560.00

Direct labour cost per unit 410 150.00 260.00

Inspection Cost Machine Hours 20000 7.19 7.67

Assembly cost Machine Hours 90000 32.34 34.50

Production scheduling Machine Hours 105000 37.73 40.25

Machine set up Machine Hours 35000 12.58 13.42

Selling & Administration Expenses No. of units sold 140600 45.35 45.35

Interest Expenses No. of units sold 25200 8.13 8.13

Office Rent Equal (50%-50%) 35900 11.22 11.97

Cost per unit 629.55 981.28

4 | P a g e

5

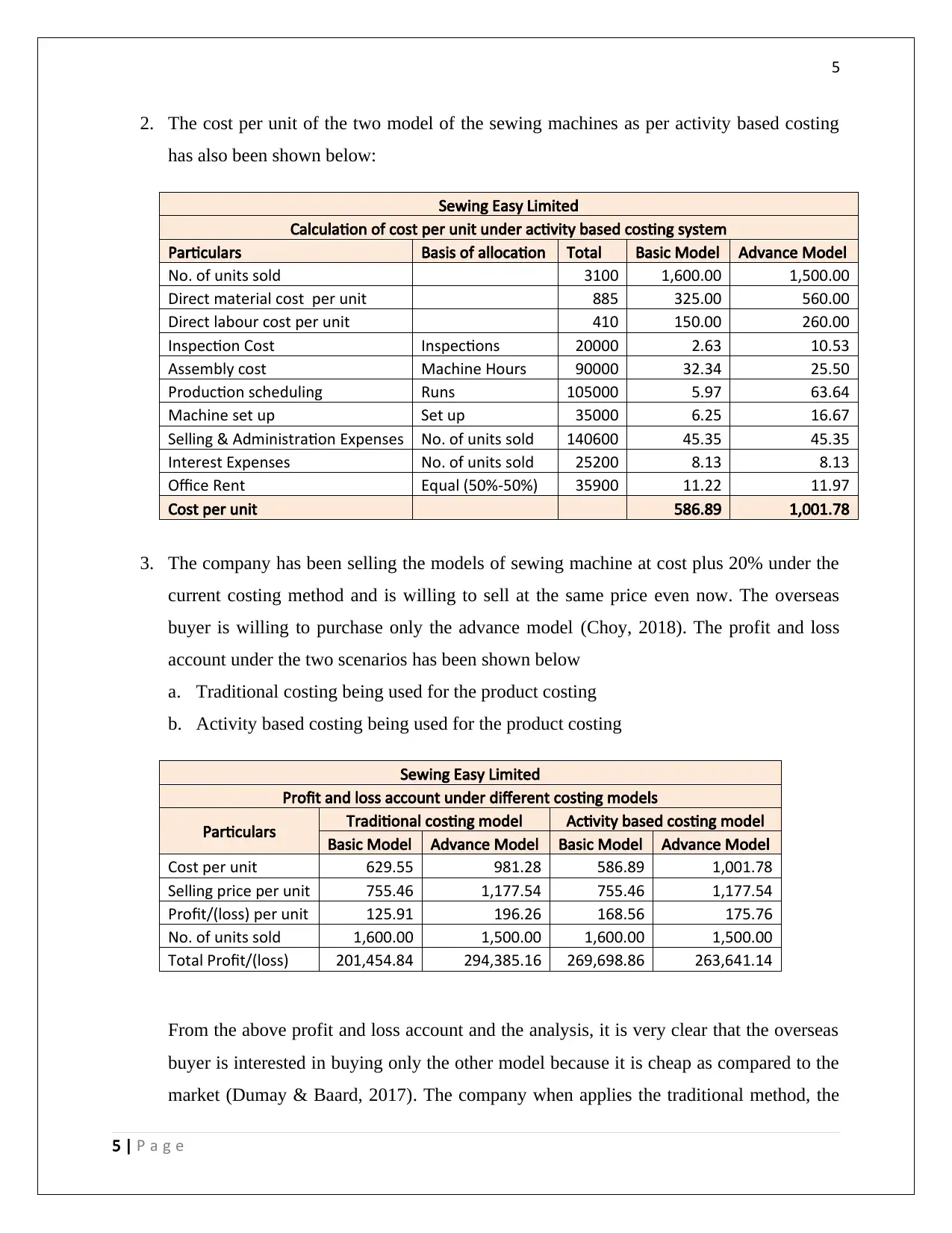

2. The cost per unit of the two model of the sewing machines as per activity based costing

has also been shown below:

Sewing Easy Limited

Calculation of cost per unit under activity based costing system

Particulars Basis of allocation Total Basic Model Advance Model

No. of units sold 3100 1,600.00 1,500.00

Direct material cost per unit 885 325.00 560.00

Direct labour cost per unit 410 150.00 260.00

Inspection Cost Inspections 20000 2.63 10.53

Assembly cost Machine Hours 90000 32.34 25.50

Production scheduling Runs 105000 5.97 63.64

Machine set up Set up 35000 6.25 16.67

Selling & Administration Expenses No. of units sold 140600 45.35 45.35

Interest Expenses No. of units sold 25200 8.13 8.13

Office Rent Equal (50%-50%) 35900 11.22 11.97

Cost per unit 586.89 1,001.78

3. The company has been selling the models of sewing machine at cost plus 20% under the

current costing method and is willing to sell at the same price even now. The overseas

buyer is willing to purchase only the advance model (Choy, 2018). The profit and loss

account under the two scenarios has been shown below

a. Traditional costing being used for the product costing

b. Activity based costing being used for the product costing

Sewing Easy Limited

Profit and loss account under different costing models

Particulars Traditional costing model Activity based costing model

Basic Model Advance Model Basic Model Advance Model

Cost per unit 629.55 981.28 586.89 1,001.78

Selling price per unit 755.46 1,177.54 755.46 1,177.54

Profit/(loss) per unit 125.91 196.26 168.56 175.76

No. of units sold 1,600.00 1,500.00 1,600.00 1,500.00

Total Profit/(loss) 201,454.84 294,385.16 269,698.86 263,641.14

From the above profit and loss account and the analysis, it is very clear that the overseas

buyer is interested in buying only the other model because it is cheap as compared to the

market (Dumay & Baard, 2017). The company when applies the traditional method, the

5 | P a g e

2. The cost per unit of the two model of the sewing machines as per activity based costing

has also been shown below:

Sewing Easy Limited

Calculation of cost per unit under activity based costing system

Particulars Basis of allocation Total Basic Model Advance Model

No. of units sold 3100 1,600.00 1,500.00

Direct material cost per unit 885 325.00 560.00

Direct labour cost per unit 410 150.00 260.00

Inspection Cost Inspections 20000 2.63 10.53

Assembly cost Machine Hours 90000 32.34 25.50

Production scheduling Runs 105000 5.97 63.64

Machine set up Set up 35000 6.25 16.67

Selling & Administration Expenses No. of units sold 140600 45.35 45.35

Interest Expenses No. of units sold 25200 8.13 8.13

Office Rent Equal (50%-50%) 35900 11.22 11.97

Cost per unit 586.89 1,001.78

3. The company has been selling the models of sewing machine at cost plus 20% under the

current costing method and is willing to sell at the same price even now. The overseas

buyer is willing to purchase only the advance model (Choy, 2018). The profit and loss

account under the two scenarios has been shown below

a. Traditional costing being used for the product costing

b. Activity based costing being used for the product costing

Sewing Easy Limited

Profit and loss account under different costing models

Particulars Traditional costing model Activity based costing model

Basic Model Advance Model Basic Model Advance Model

Cost per unit 629.55 981.28 586.89 1,001.78

Selling price per unit 755.46 1,177.54 755.46 1,177.54

Profit/(loss) per unit 125.91 196.26 168.56 175.76

No. of units sold 1,600.00 1,500.00 1,600.00 1,500.00

Total Profit/(loss) 201,454.84 294,385.16 269,698.86 263,641.14

From the above profit and loss account and the analysis, it is very clear that the overseas

buyer is interested in buying only the other model because it is cheap as compared to the

market (Dumay & Baard, 2017). The company when applies the traditional method, the

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

cost of the advanced model is $ 981.28 per unit whereas when the company applies the

activity based costing technique then the cost becomes $ 1001.78, now in both the

scenarios the company is getting the model at the $ 1188.54. On the other hand if we

analyse the cost per unit for the basic model under the traditional costing and the activity

based costing, we see that the profit attributable under the latter system is much more

than the former hence the buyer will be at loss purchasing the product at more than as

compared to the market (Heminway, 2017).

The above is one of the instances which shows the importance of the accurate product

costing.

This shows that if the products are being appropriately and correctly costed then the

correct profit would be revealed and the business would not be losing the revenue as

well as the customers.

Also, the competitors would not be able to make use of the same and thereby

increasing their sales. In case the correct costing is not being done, the business

would not be able to take decision relating to the introduction of the new products in

the market, removal of the old products from the catalogue as they are no more

profitable and also not being able to decide when to increase or decrease the price of

the product in the market (Goldmann, 2016).

In case there is any project tracking related with the costing of the product then in the

absence of the accurate costing, there would always be a deviation as compared to the

expectation and the project tracking would all go wrong.

If the company is planning for the project development meaning the introduction of

the new product in the market basis the old product then the costing can be an

invaluable resource therefore it needs to be accurate (Jefferson, 2017).

Finally, if the product is not costed accurately, it gives rise to inefficiency and

ineffective results in terms of budget, the income statement, the transfer prices and

thereby the overall financial statements of the company.

4. We hardly see that the actual overhead costs and the applied overhead costs would match.

It is usually the difference between the manufacturing overhead applied to the work in

6 | P a g e

cost of the advanced model is $ 981.28 per unit whereas when the company applies the

activity based costing technique then the cost becomes $ 1001.78, now in both the

scenarios the company is getting the model at the $ 1188.54. On the other hand if we

analyse the cost per unit for the basic model under the traditional costing and the activity

based costing, we see that the profit attributable under the latter system is much more

than the former hence the buyer will be at loss purchasing the product at more than as

compared to the market (Heminway, 2017).

The above is one of the instances which shows the importance of the accurate product

costing.

This shows that if the products are being appropriately and correctly costed then the

correct profit would be revealed and the business would not be losing the revenue as

well as the customers.

Also, the competitors would not be able to make use of the same and thereby

increasing their sales. In case the correct costing is not being done, the business

would not be able to take decision relating to the introduction of the new products in

the market, removal of the old products from the catalogue as they are no more

profitable and also not being able to decide when to increase or decrease the price of

the product in the market (Goldmann, 2016).

In case there is any project tracking related with the costing of the product then in the

absence of the accurate costing, there would always be a deviation as compared to the

expectation and the project tracking would all go wrong.

If the company is planning for the project development meaning the introduction of

the new product in the market basis the old product then the costing can be an

invaluable resource therefore it needs to be accurate (Jefferson, 2017).

Finally, if the product is not costed accurately, it gives rise to inefficiency and

ineffective results in terms of budget, the income statement, the transfer prices and

thereby the overall financial statements of the company.

4. We hardly see that the actual overhead costs and the applied overhead costs would match.

It is usually the difference between the manufacturing overhead applied to the work in

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

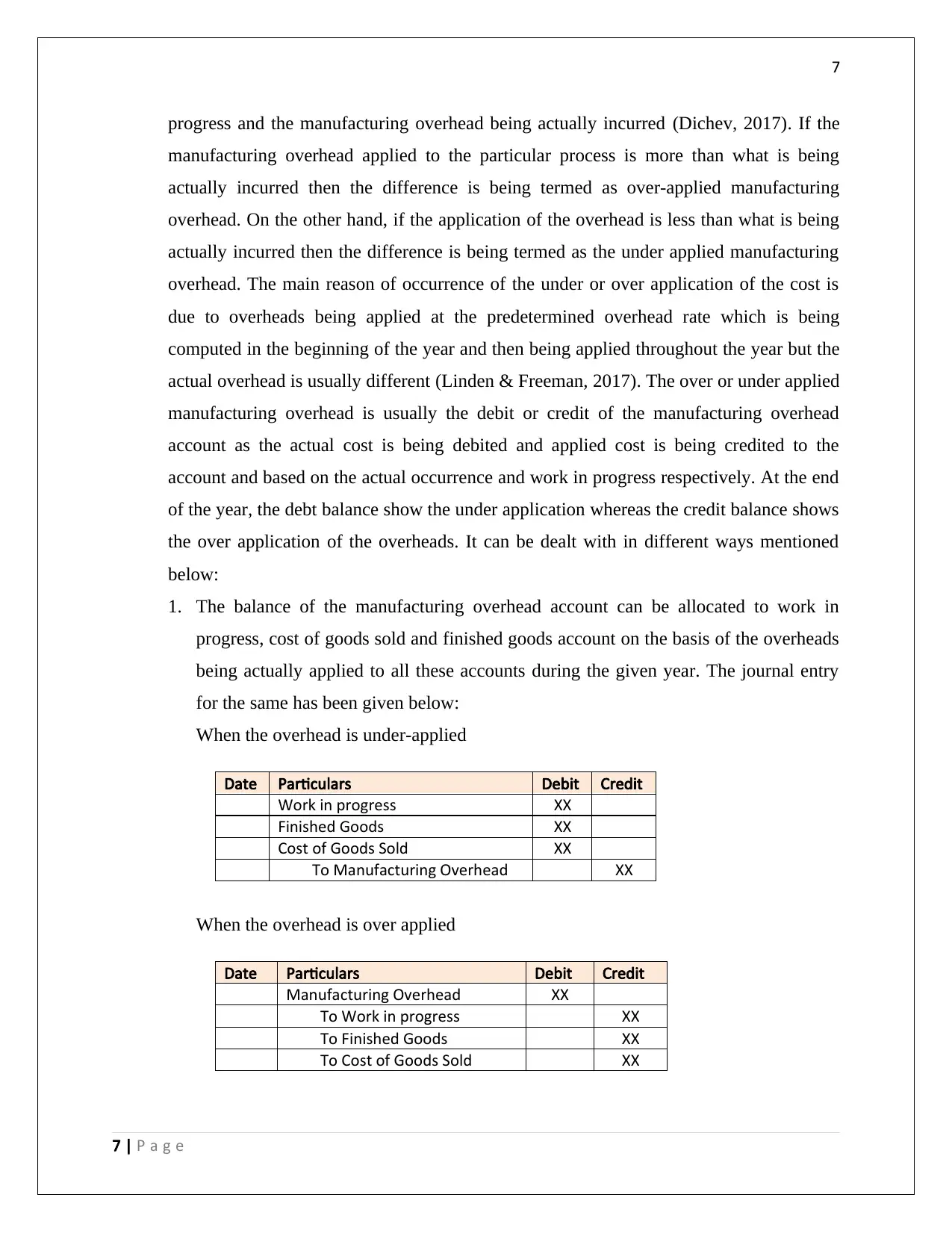

progress and the manufacturing overhead being actually incurred (Dichev, 2017). If the

manufacturing overhead applied to the particular process is more than what is being

actually incurred then the difference is being termed as over-applied manufacturing

overhead. On the other hand, if the application of the overhead is less than what is being

actually incurred then the difference is being termed as the under applied manufacturing

overhead. The main reason of occurrence of the under or over application of the cost is

due to overheads being applied at the predetermined overhead rate which is being

computed in the beginning of the year and then being applied throughout the year but the

actual overhead is usually different (Linden & Freeman, 2017). The over or under applied

manufacturing overhead is usually the debit or credit of the manufacturing overhead

account as the actual cost is being debited and applied cost is being credited to the

account and based on the actual occurrence and work in progress respectively. At the end

of the year, the debt balance show the under application whereas the credit balance shows

the over application of the overheads. It can be dealt with in different ways mentioned

below:

1. The balance of the manufacturing overhead account can be allocated to work in

progress, cost of goods sold and finished goods account on the basis of the overheads

being actually applied to all these accounts during the given year. The journal entry

for the same has been given below:

When the overhead is under-applied

Date Particulars Debit Credit

Work in progress XX

Finished Goods XX

Cost of Goods Sold XX

To Manufacturing Overhead XX

When the overhead is over applied

Date Particulars Debit Credit

Manufacturing Overhead XX

To Work in progress XX

To Finished Goods XX

To Cost of Goods Sold XX

7 | P a g e

progress and the manufacturing overhead being actually incurred (Dichev, 2017). If the

manufacturing overhead applied to the particular process is more than what is being

actually incurred then the difference is being termed as over-applied manufacturing

overhead. On the other hand, if the application of the overhead is less than what is being

actually incurred then the difference is being termed as the under applied manufacturing

overhead. The main reason of occurrence of the under or over application of the cost is

due to overheads being applied at the predetermined overhead rate which is being

computed in the beginning of the year and then being applied throughout the year but the

actual overhead is usually different (Linden & Freeman, 2017). The over or under applied

manufacturing overhead is usually the debit or credit of the manufacturing overhead

account as the actual cost is being debited and applied cost is being credited to the

account and based on the actual occurrence and work in progress respectively. At the end

of the year, the debt balance show the under application whereas the credit balance shows

the over application of the overheads. It can be dealt with in different ways mentioned

below:

1. The balance of the manufacturing overhead account can be allocated to work in

progress, cost of goods sold and finished goods account on the basis of the overheads

being actually applied to all these accounts during the given year. The journal entry

for the same has been given below:

When the overhead is under-applied

Date Particulars Debit Credit

Work in progress XX

Finished Goods XX

Cost of Goods Sold XX

To Manufacturing Overhead XX

When the overhead is over applied

Date Particulars Debit Credit

Manufacturing Overhead XX

To Work in progress XX

To Finished Goods XX

To Cost of Goods Sold XX

7 | P a g e

8

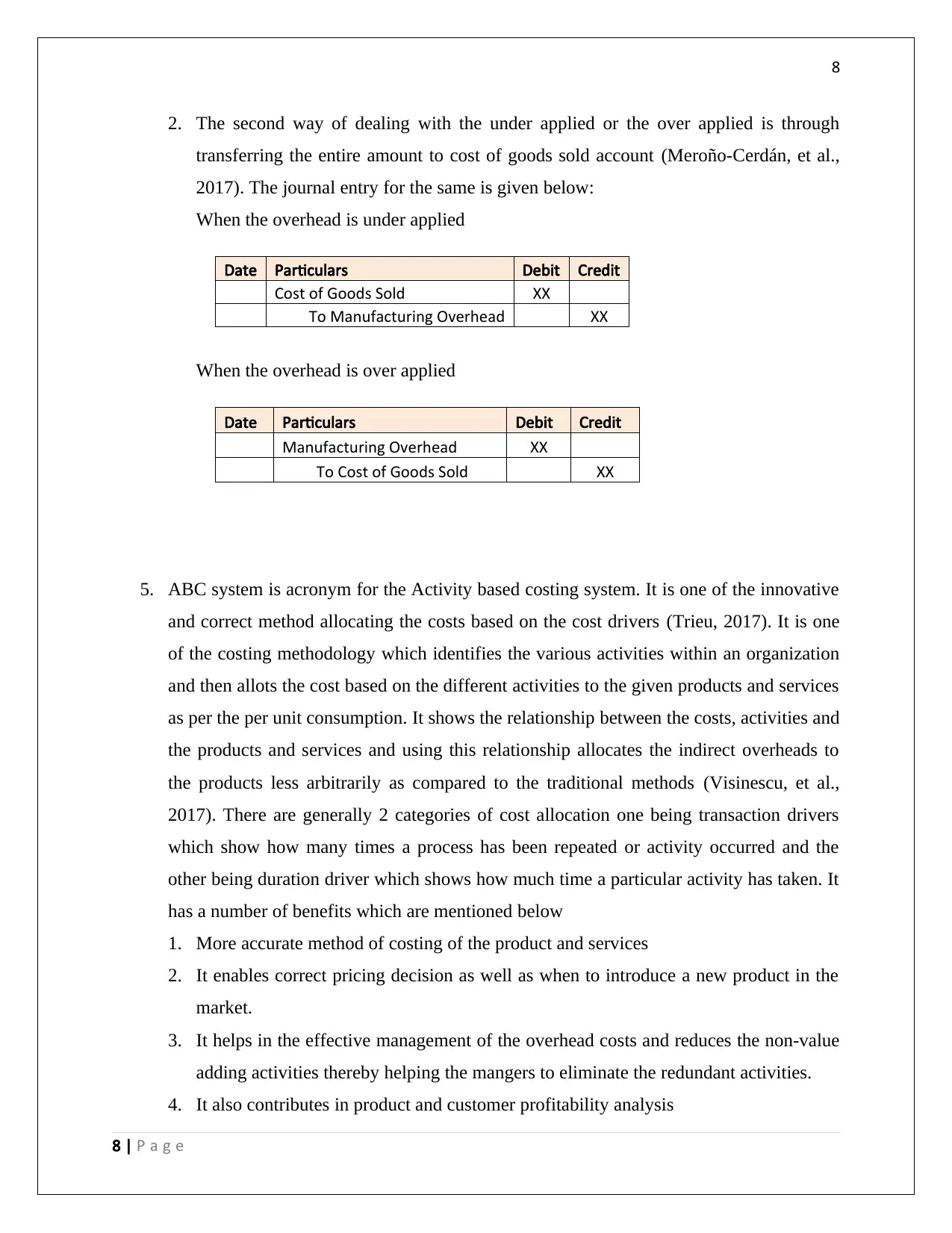

2. The second way of dealing with the under applied or the over applied is through

transferring the entire amount to cost of goods sold account (Meroño-Cerdán, et al.,

2017). The journal entry for the same is given below:

When the overhead is under applied

Date Particulars Debit Credit

Cost of Goods Sold XX

To Manufacturing Overhead XX

When the overhead is over applied

Date Particulars Debit Credit

Manufacturing Overhead XX

To Cost of Goods Sold XX

5. ABC system is acronym for the Activity based costing system. It is one of the innovative

and correct method allocating the costs based on the cost drivers (Trieu, 2017). It is one

of the costing methodology which identifies the various activities within an organization

and then allots the cost based on the different activities to the given products and services

as per the per unit consumption. It shows the relationship between the costs, activities and

the products and services and using this relationship allocates the indirect overheads to

the products less arbitrarily as compared to the traditional methods (Visinescu, et al.,

2017). There are generally 2 categories of cost allocation one being transaction drivers

which show how many times a process has been repeated or activity occurred and the

other being duration driver which shows how much time a particular activity has taken. It

has a number of benefits which are mentioned below

1. More accurate method of costing of the product and services

2. It enables correct pricing decision as well as when to introduce a new product in the

market.

3. It helps in the effective management of the overhead costs and reduces the non-value

adding activities thereby helping the mangers to eliminate the redundant activities.

4. It also contributes in product and customer profitability analysis

8 | P a g e

2. The second way of dealing with the under applied or the over applied is through

transferring the entire amount to cost of goods sold account (Meroño-Cerdán, et al.,

2017). The journal entry for the same is given below:

When the overhead is under applied

Date Particulars Debit Credit

Cost of Goods Sold XX

To Manufacturing Overhead XX

When the overhead is over applied

Date Particulars Debit Credit

Manufacturing Overhead XX

To Cost of Goods Sold XX

5. ABC system is acronym for the Activity based costing system. It is one of the innovative

and correct method allocating the costs based on the cost drivers (Trieu, 2017). It is one

of the costing methodology which identifies the various activities within an organization

and then allots the cost based on the different activities to the given products and services

as per the per unit consumption. It shows the relationship between the costs, activities and

the products and services and using this relationship allocates the indirect overheads to

the products less arbitrarily as compared to the traditional methods (Visinescu, et al.,

2017). There are generally 2 categories of cost allocation one being transaction drivers

which show how many times a process has been repeated or activity occurred and the

other being duration driver which shows how much time a particular activity has taken. It

has a number of benefits which are mentioned below

1. More accurate method of costing of the product and services

2. It enables correct pricing decision as well as when to introduce a new product in the

market.

3. It helps in the effective management of the overhead costs and reduces the non-value

adding activities thereby helping the mangers to eliminate the redundant activities.

4. It also contributes in product and customer profitability analysis

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

5. It helps in tracing the activities for the given cost object and also in tracing of the

overhead costs (Sithole, et al., 2017).

6. It helps in better decision making by the mangers as more accurate data is present to

see what product and activities to be focused upon to improve the profitability.

7. ABC analysis involves pooling of the costs, identification of the cost drivers and

range of applications. Thereby it can help the company in identifying the spare

capacity if any help in the reduction of the cost.

8. It helps the service industry mostly to allocate its cost as there are no direct cost

drivers which can be used to allocate the overheads (Werner, 2017).

Along with the benefits, ABC costing also comes with the some limitations as well which

has been listed below:

1. It is quite expensive to implement as it needs to be driven as a separate activity all

together and an extra manpower may be required. It is also complex as compared to

the other processes and traditional costing systems.

2. There may also be several difficulties in the selection of the cost drivers and

assignment of the common costs (Vieira, et al., 2017).

3. It may be that beneficial to the smaller firms as they may not require this level of

technology. Furthermore, it is beneficial to those who use cost plus mark-up method

for pricing but not for those who using the market price based method.

4. If the amount of the overheads is small, then the ABC costing analysis may not be of

much use (Raiborn, et al., 2016).

5. It is not a substitute to the monthly profit and loss statements, neither should it be

used to prepare the profit and loss account.

9 | P a g e

5. It helps in tracing the activities for the given cost object and also in tracing of the

overhead costs (Sithole, et al., 2017).

6. It helps in better decision making by the mangers as more accurate data is present to

see what product and activities to be focused upon to improve the profitability.

7. ABC analysis involves pooling of the costs, identification of the cost drivers and

range of applications. Thereby it can help the company in identifying the spare

capacity if any help in the reduction of the cost.

8. It helps the service industry mostly to allocate its cost as there are no direct cost

drivers which can be used to allocate the overheads (Werner, 2017).

Along with the benefits, ABC costing also comes with the some limitations as well which

has been listed below:

1. It is quite expensive to implement as it needs to be driven as a separate activity all

together and an extra manpower may be required. It is also complex as compared to

the other processes and traditional costing systems.

2. There may also be several difficulties in the selection of the cost drivers and

assignment of the common costs (Vieira, et al., 2017).

3. It may be that beneficial to the smaller firms as they may not require this level of

technology. Furthermore, it is beneficial to those who use cost plus mark-up method

for pricing but not for those who using the market price based method.

4. If the amount of the overheads is small, then the ABC costing analysis may not be of

much use (Raiborn, et al., 2016).

5. It is not a substitute to the monthly profit and loss statements, neither should it be

used to prepare the profit and loss account.

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

References

Alexander, F., 2016. The Changing Face of Accountability. The Journal of Higher Education, 71(4), pp.

411-431.

Bizfluent, 2017. Advantages & Disadvantages of Internal Control. [Online]

Available at: https://bizfluent.com/info-8064250-advantages-disadvantages-internal-control.html

[Accessed 07 december 2017].

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview Analysis.

Ecological Economics, p. 145.

Dichev, I., 2017. On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), pp. 617-632.

Dumay, J. & Baard, V., 2017. An introduction to interventionist research in accounting.. The Routledge

Companion to Qualitative Accounting Research Methods, p. 265.

Goldmann, K., 2016. Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, Volume 4, pp. 103-112.

Heminway, J., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, pp. 1-35.

Jefferson, M., 2017. Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland.

Technological Forecasting and Social Change, pp. 353-354.

Linden, B. & Freeman, R., 2017. Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), pp. 353-379.

Meroño-Cerdán, A., Lopez-Nicolas, C. & Molina-Castillo, F., 2017. Risk aversion, innovation and

performance in family firms. Economics of Innovation and new technology, pp. 1-15.

Raiborn, C., Butler, J. & Martin, K., 2016. The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), pp. 10-21.

Sithole, S., Chandler, P., Abeysekera, I. & Paas, F., 2017. Benefits of guided self-management of attention

on learning accounting. Journal of Educational Psychology, 109(2), p. 220.

Trieu, V., 2017. Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, Volume 93, pp. 111-124.

Vieira, R., O’Dwyer, B. & Schneider, R., 2017. Aligning Strategy and Performance Management Systems.

SAGE Journals, 30(1).

10 | P a g e

References

Alexander, F., 2016. The Changing Face of Accountability. The Journal of Higher Education, 71(4), pp.

411-431.

Bizfluent, 2017. Advantages & Disadvantages of Internal Control. [Online]

Available at: https://bizfluent.com/info-8064250-advantages-disadvantages-internal-control.html

[Accessed 07 december 2017].

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview Analysis.

Ecological Economics, p. 145.

Dichev, I., 2017. On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), pp. 617-632.

Dumay, J. & Baard, V., 2017. An introduction to interventionist research in accounting.. The Routledge

Companion to Qualitative Accounting Research Methods, p. 265.

Goldmann, K., 2016. Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, Volume 4, pp. 103-112.

Heminway, J., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, pp. 1-35.

Jefferson, M., 2017. Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland.

Technological Forecasting and Social Change, pp. 353-354.

Linden, B. & Freeman, R., 2017. Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), pp. 353-379.

Meroño-Cerdán, A., Lopez-Nicolas, C. & Molina-Castillo, F., 2017. Risk aversion, innovation and

performance in family firms. Economics of Innovation and new technology, pp. 1-15.

Raiborn, C., Butler, J. & Martin, K., 2016. The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), pp. 10-21.

Sithole, S., Chandler, P., Abeysekera, I. & Paas, F., 2017. Benefits of guided self-management of attention

on learning accounting. Journal of Educational Psychology, 109(2), p. 220.

Trieu, V., 2017. Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, Volume 93, pp. 111-124.

Vieira, R., O’Dwyer, B. & Schneider, R., 2017. Aligning Strategy and Performance Management Systems.

SAGE Journals, 30(1).

10 | P a g e

11

Visinescu, L., Jones, M. & Sidorova, A., 2017. Improving Decision Quality: The Role of Business

Intelligence. Journal of Computer Information Systems, 57(1), pp. 58-66.

Werner, M., 2017. Financial process mining - Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems, Volume 25, pp. 57-80.

11 | P a g e

Visinescu, L., Jones, M. & Sidorova, A., 2017. Improving Decision Quality: The Role of Business

Intelligence. Journal of Computer Information Systems, 57(1), pp. 58-66.

Werner, M., 2017. Financial process mining - Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems, Volume 25, pp. 57-80.

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.