Business Accounting Report: Costing Methods for Sewing Easy Ltd.

VerifiedAdded on 2021/05/30

|15

|3157

|29

Report

AI Summary

This report provides a comprehensive analysis of activity-based costing (ABC) compared to traditional costing methods within the context of Sewing Easy Ltd., a sewing machine manufacturer. The report begins by calculating the cost per unit for two sewing machine models using the traditional costing system, where overhead costs are allocated based on machine hours. It then proceeds to calculate the cost per unit using ABC, which identifies different cost centers for overhead allocation based on specific activities. The report highlights the advantages of ABC, such as improved accuracy in product costing and better decision-making capabilities. Furthermore, the report explores the reasons for under or over-applied overhead costs and suggests ways to address these issues. Finally, it discusses the merits and demerits of the ABC system, including its ability to trace overhead costs and provide cost behavior information, as well as its potentially high implementation costs and complexity.

qwertyuiopasdfghjklzxcvbnmqw

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiop

asdfghjklzxcvbnmqwertyuiopasd

fghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmqwertyuiopasdfghjkl

zxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbnm

qwertyuiopasdfghjklzxcvbnmqw

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiop

asdfghjklzxcvbnmqwertyuiopasd

fghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmrtyuiopasdfghjklzxcv

Business Accounting

Report

5/13/2018

Student Name

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiop

asdfghjklzxcvbnmqwertyuiopasd

fghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmqwertyuiopasdfghjkl

zxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbnm

qwertyuiopasdfghjklzxcvbnmqw

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiop

asdfghjklzxcvbnmqwertyuiopasd

fghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmrtyuiopasdfghjklzxcv

Business Accounting

Report

5/13/2018

Student Name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 | P a g e Business Accounting

Contents

Introduction................................................................................................................................2

Task 1.........................................................................................................................................2

Task 2.........................................................................................................................................3

Task 3.........................................................................................................................................4

Task 4.........................................................................................................................................6

Task 5.........................................................................................................................................7

Merits of ABC system............................................................................................................7

Demerits of ABC system........................................................................................................9

References................................................................................................................................12

Contents

Introduction................................................................................................................................2

Task 1.........................................................................................................................................2

Task 2.........................................................................................................................................3

Task 3.........................................................................................................................................4

Task 4.........................................................................................................................................6

Task 5.........................................................................................................................................7

Merits of ABC system............................................................................................................7

Demerits of ABC system........................................................................................................9

References................................................................................................................................12

2 | P a g e Business Accounting

Introduction

Activity based costing can be defined as the costing in which the activities are identified by

the firm and accordingly its indirect cost of the product. These indirect costs includes the

management and office staff salaries, rent etc. these costs are find allocate to assign in the

manufacturing sector. From ABC costing, allocation of indirect cost can be made easily. The

company Sewing Easy Ltd. is dealing in providing the manufacturing of sewing machines. At

present company is using the traditional costing system and machine hours for assigning the

indirect cost. The Company can allocate its cost accurately and can reduce its per unit cost of

machines using ABC costing. ABC costing establishes the relationship between the cost,

activities, indirect cost and its products. The cost assigned in the ABC costing is low as

compared to the traditional costing.

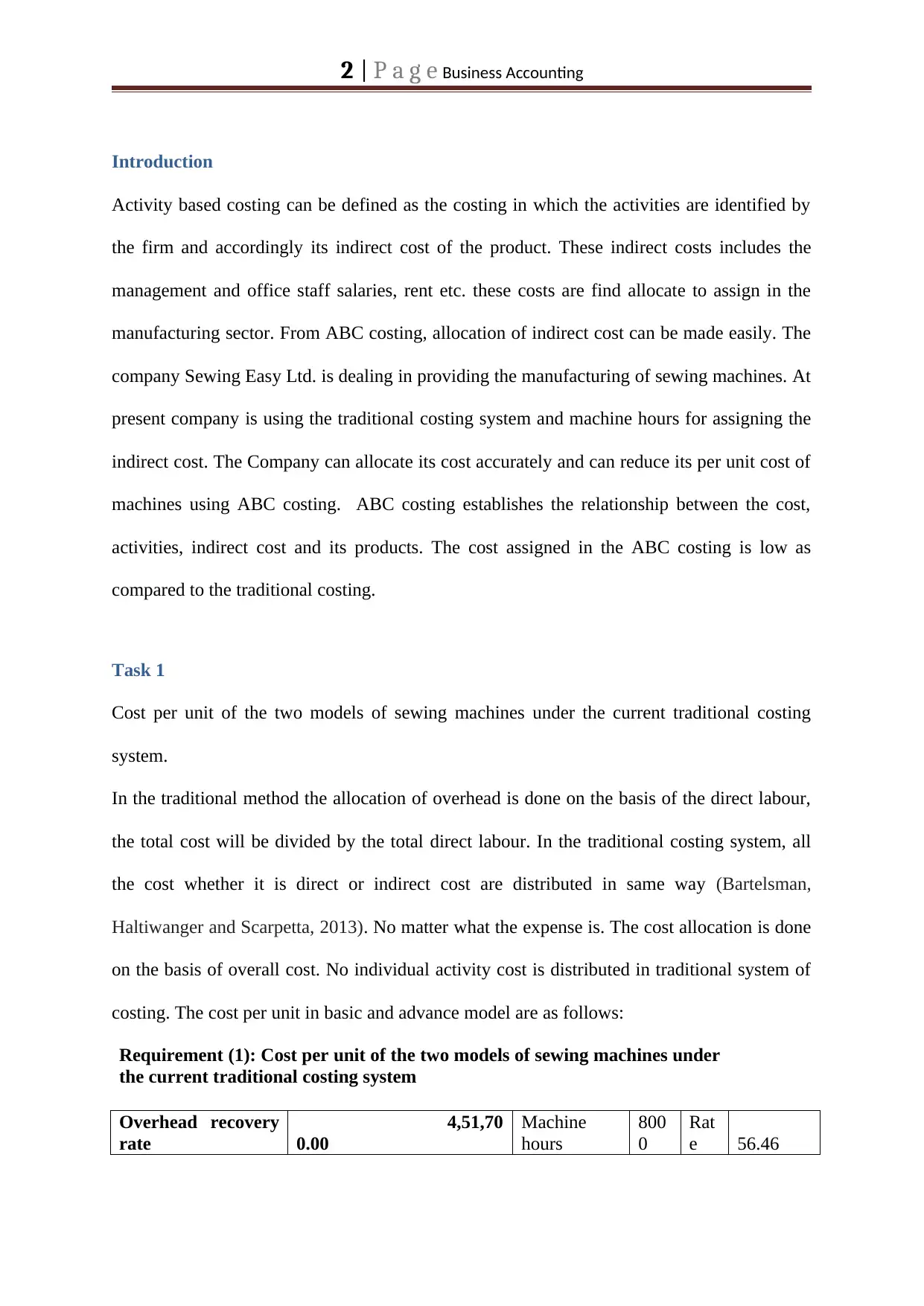

Task 1

Cost per unit of the two models of sewing machines under the current traditional costing

system.

In the traditional method the allocation of overhead is done on the basis of the direct labour,

the total cost will be divided by the total direct labour. In the traditional costing system, all

the cost whether it is direct or indirect cost are distributed in same way (Bartelsman,

Haltiwanger and Scarpetta, 2013). No matter what the expense is. The cost allocation is done

on the basis of overall cost. No individual activity cost is distributed in traditional system of

costing. The cost per unit in basic and advance model are as follows:

Requirement (1): Cost per unit of the two models of sewing machines under

the current traditional costing system

Overhead recovery

rate

4,51,70

0.00

Machine

hours

800

0

Rat

e 56.46

Introduction

Activity based costing can be defined as the costing in which the activities are identified by

the firm and accordingly its indirect cost of the product. These indirect costs includes the

management and office staff salaries, rent etc. these costs are find allocate to assign in the

manufacturing sector. From ABC costing, allocation of indirect cost can be made easily. The

company Sewing Easy Ltd. is dealing in providing the manufacturing of sewing machines. At

present company is using the traditional costing system and machine hours for assigning the

indirect cost. The Company can allocate its cost accurately and can reduce its per unit cost of

machines using ABC costing. ABC costing establishes the relationship between the cost,

activities, indirect cost and its products. The cost assigned in the ABC costing is low as

compared to the traditional costing.

Task 1

Cost per unit of the two models of sewing machines under the current traditional costing

system.

In the traditional method the allocation of overhead is done on the basis of the direct labour,

the total cost will be divided by the total direct labour. In the traditional costing system, all

the cost whether it is direct or indirect cost are distributed in same way (Bartelsman,

Haltiwanger and Scarpetta, 2013). No matter what the expense is. The cost allocation is done

on the basis of overall cost. No individual activity cost is distributed in traditional system of

costing. The cost per unit in basic and advance model are as follows:

Requirement (1): Cost per unit of the two models of sewing machines under

the current traditional costing system

Overhead recovery

rate

4,51,70

0.00

Machine

hours

800

0

Rat

e 56.46

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3 | P a g e Business Accounting

Particulars Models of machine

Basic(in $) Advance($)

Direct material

5,20,00

0.00

8,40,000.0

0

Direct labour

2,40,00

0.00

3,90,000.0

0

Overheads

Machine hours 4600 3400

Rate per hour 56.46

56.

46

Over heads allocated

2,59,72

7.50

1,91,972.5

0

Total cost

10,19,72

7.50

14,21,972.5

0

Total unit 1600 1500

Per unit cost

6

37.33

947.

98

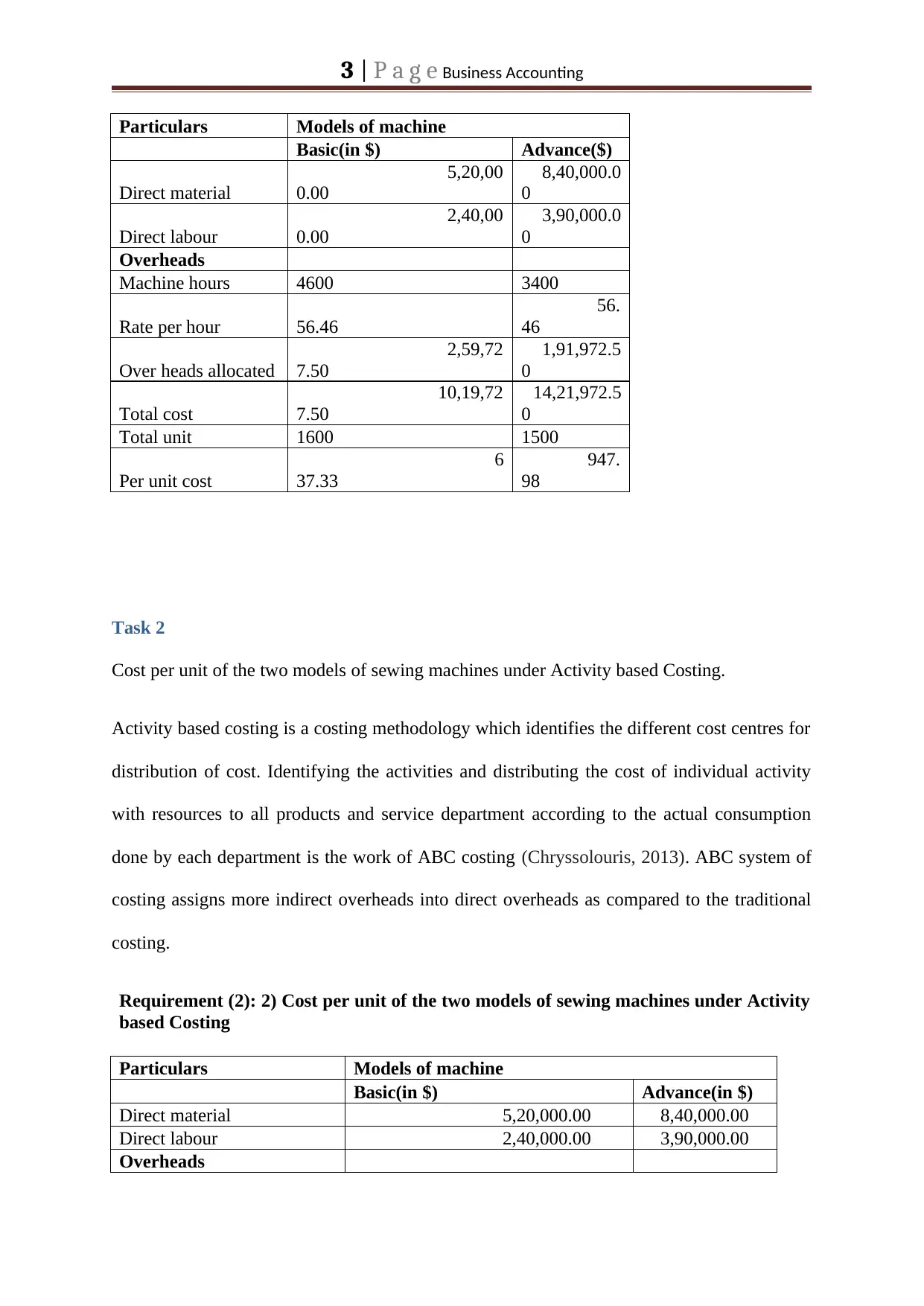

Task 2

Cost per unit of the two models of sewing machines under Activity based Costing.

Activity based costing is a costing methodology which identifies the different cost centres for

distribution of cost. Identifying the activities and distributing the cost of individual activity

with resources to all products and service department according to the actual consumption

done by each department is the work of ABC costing (Chryssolouris, 2013). ABC system of

costing assigns more indirect overheads into direct overheads as compared to the traditional

costing.

Requirement (2): 2) Cost per unit of the two models of sewing machines under Activity

based Costing

Particulars Models of machine

Basic(in $) Advance(in $)

Direct material 5,20,000.00 8,40,000.00

Direct labour 2,40,000.00 3,90,000.00

Overheads

Particulars Models of machine

Basic(in $) Advance($)

Direct material

5,20,00

0.00

8,40,000.0

0

Direct labour

2,40,00

0.00

3,90,000.0

0

Overheads

Machine hours 4600 3400

Rate per hour 56.46

56.

46

Over heads allocated

2,59,72

7.50

1,91,972.5

0

Total cost

10,19,72

7.50

14,21,972.5

0

Total unit 1600 1500

Per unit cost

6

37.33

947.

98

Task 2

Cost per unit of the two models of sewing machines under Activity based Costing.

Activity based costing is a costing methodology which identifies the different cost centres for

distribution of cost. Identifying the activities and distributing the cost of individual activity

with resources to all products and service department according to the actual consumption

done by each department is the work of ABC costing (Chryssolouris, 2013). ABC system of

costing assigns more indirect overheads into direct overheads as compared to the traditional

costing.

Requirement (2): 2) Cost per unit of the two models of sewing machines under Activity

based Costing

Particulars Models of machine

Basic(in $) Advance(in $)

Direct material 5,20,000.00 8,40,000.00

Direct labour 2,40,000.00 3,90,000.00

Overheads

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4 | P a g e Business Accounting

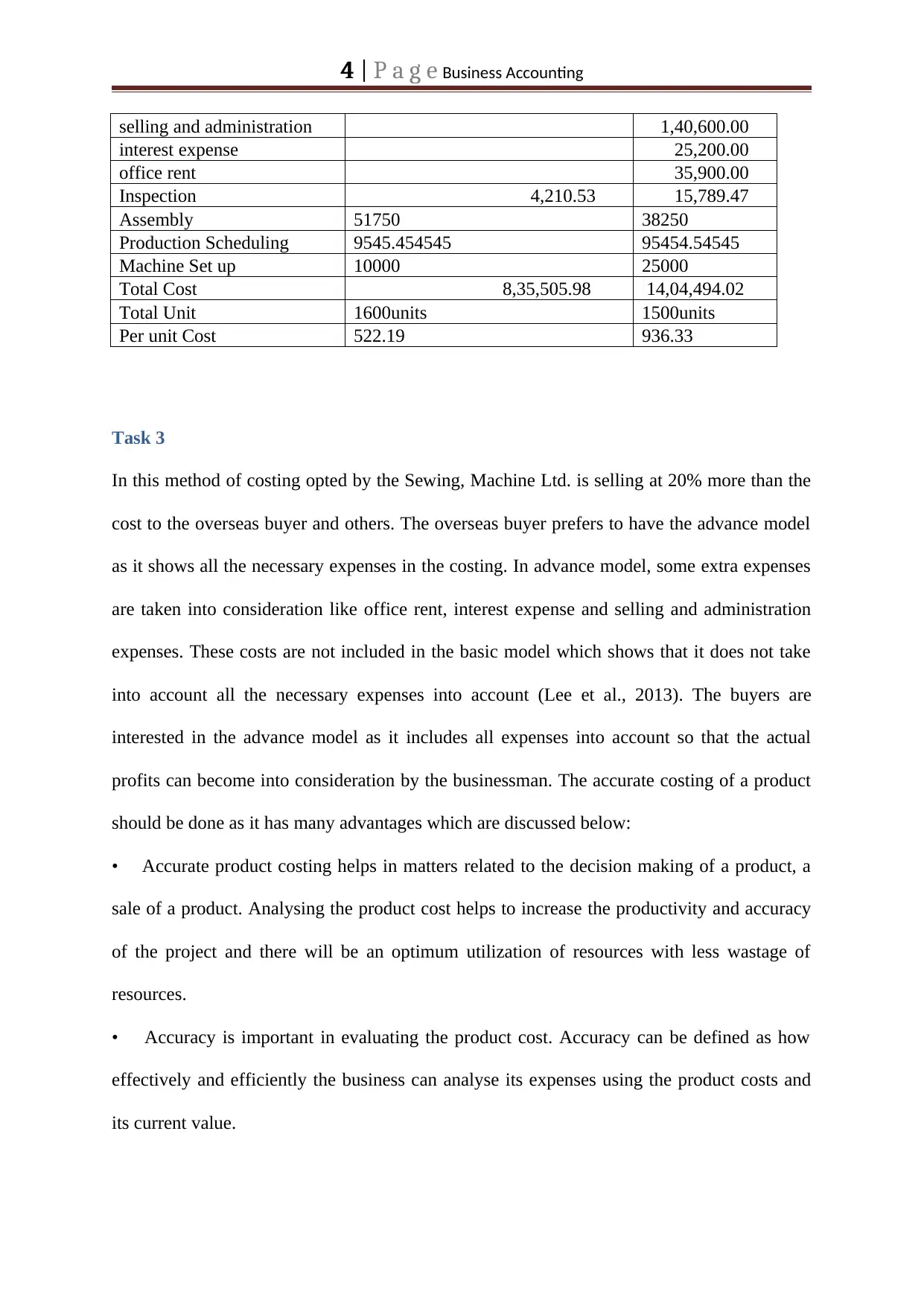

selling and administration 1,40,600.00

interest expense 25,200.00

office rent 35,900.00

Inspection 4,210.53 15,789.47

Assembly 51750 38250

Production Scheduling 9545.454545 95454.54545

Machine Set up 10000 25000

Total Cost 8,35,505.98 14,04,494.02

Total Unit 1600units 1500units

Per unit Cost 522.19 936.33

Task 3

In this method of costing opted by the Sewing, Machine Ltd. is selling at 20% more than the

cost to the overseas buyer and others. The overseas buyer prefers to have the advance model

as it shows all the necessary expenses in the costing. In advance model, some extra expenses

are taken into consideration like office rent, interest expense and selling and administration

expenses. These costs are not included in the basic model which shows that it does not take

into account all the necessary expenses into account (Lee et al., 2013). The buyers are

interested in the advance model as it includes all expenses into account so that the actual

profits can become into consideration by the businessman. The accurate costing of a product

should be done as it has many advantages which are discussed below:

• Accurate product costing helps in matters related to the decision making of a product, a

sale of a product. Analysing the product cost helps to increase the productivity and accuracy

of the project and there will be an optimum utilization of resources with less wastage of

resources.

• Accuracy is important in evaluating the product cost. Accuracy can be defined as how

effectively and efficiently the business can analyse its expenses using the product costs and

its current value.

selling and administration 1,40,600.00

interest expense 25,200.00

office rent 35,900.00

Inspection 4,210.53 15,789.47

Assembly 51750 38250

Production Scheduling 9545.454545 95454.54545

Machine Set up 10000 25000

Total Cost 8,35,505.98 14,04,494.02

Total Unit 1600units 1500units

Per unit Cost 522.19 936.33

Task 3

In this method of costing opted by the Sewing, Machine Ltd. is selling at 20% more than the

cost to the overseas buyer and others. The overseas buyer prefers to have the advance model

as it shows all the necessary expenses in the costing. In advance model, some extra expenses

are taken into consideration like office rent, interest expense and selling and administration

expenses. These costs are not included in the basic model which shows that it does not take

into account all the necessary expenses into account (Lee et al., 2013). The buyers are

interested in the advance model as it includes all expenses into account so that the actual

profits can become into consideration by the businessman. The accurate costing of a product

should be done as it has many advantages which are discussed below:

• Accurate product costing helps in matters related to the decision making of a product, a

sale of a product. Analysing the product cost helps to increase the productivity and accuracy

of the project and there will be an optimum utilization of resources with less wastage of

resources.

• Accuracy is important in evaluating the product cost. Accuracy can be defined as how

effectively and efficiently the business can analyse its expenses using the product costs and

its current value.

5 | P a g e Business Accounting

• Tracking of project or proposal can be made with effectiveness if the organization is

doing the costing of product correctly and it also keeps a focus on the budgets and estimates

of product to know whether the costs are matching the expectations or not (Tsai et al., 2014).

• Accuracy product costing is also important for making the budget. The budget includes

the calculation of all the expenses which are going to incur in the production and budget

records all the estimated incomes as well. This will help in the forecasting for the next

production to the company.

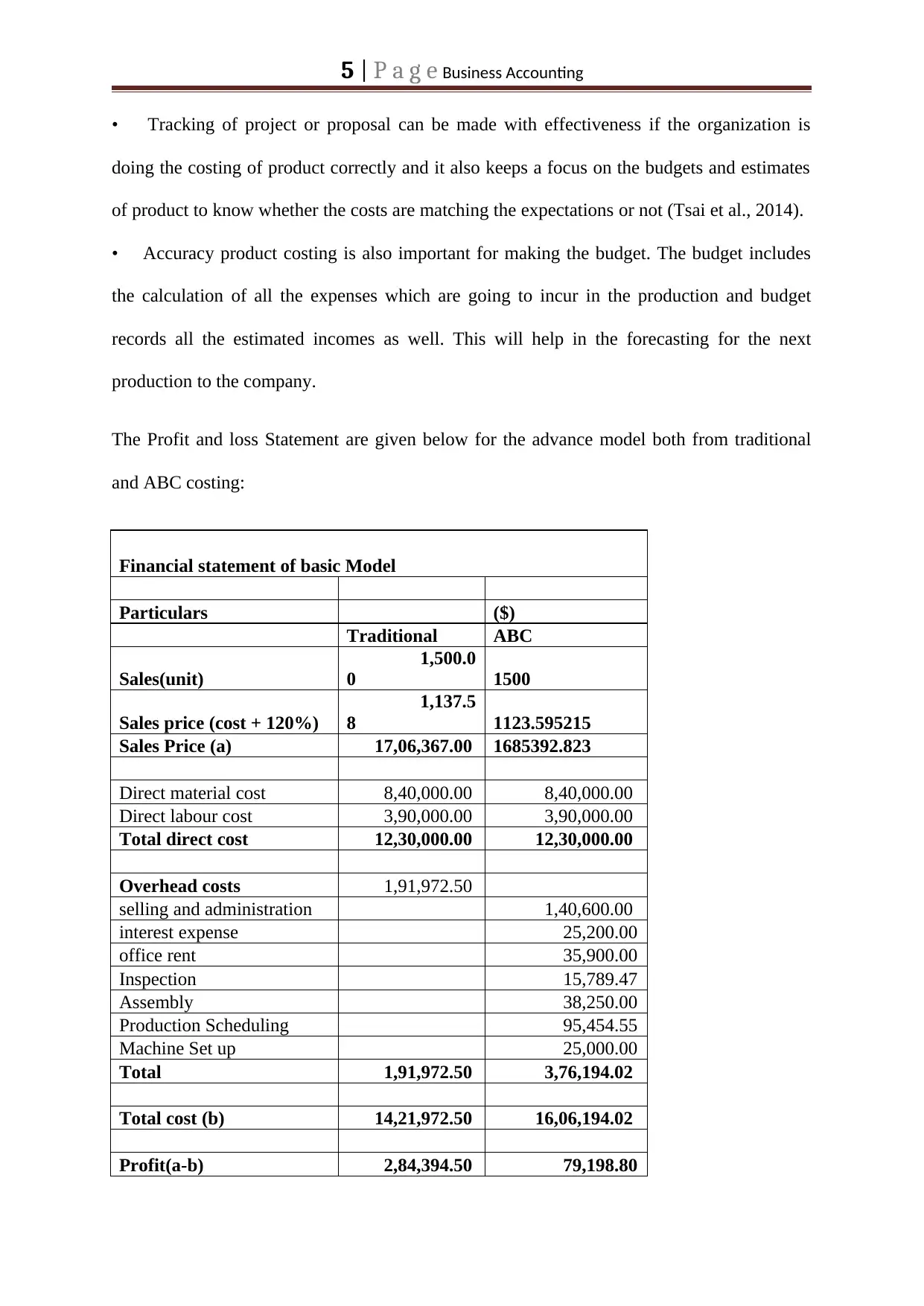

The Profit and loss Statement are given below for the advance model both from traditional

and ABC costing:

Financial statement of basic Model

Particulars ($)

Traditional ABC

Sales(unit)

1,500.0

0 1500

Sales price (cost + 120%)

1,137.5

8 1123.595215

Sales Price (a) 17,06,367.00 1685392.823

Direct material cost 8,40,000.00 8,40,000.00

Direct labour cost 3,90,000.00 3,90,000.00

Total direct cost 12,30,000.00 12,30,000.00

Overhead costs 1,91,972.50

selling and administration 1,40,600.00

interest expense 25,200.00

office rent 35,900.00

Inspection 15,789.47

Assembly 38,250.00

Production Scheduling 95,454.55

Machine Set up 25,000.00

Total 1,91,972.50 3,76,194.02

Total cost (b) 14,21,972.50 16,06,194.02

Profit(a-b) 2,84,394.50 79,198.80

• Tracking of project or proposal can be made with effectiveness if the organization is

doing the costing of product correctly and it also keeps a focus on the budgets and estimates

of product to know whether the costs are matching the expectations or not (Tsai et al., 2014).

• Accuracy product costing is also important for making the budget. The budget includes

the calculation of all the expenses which are going to incur in the production and budget

records all the estimated incomes as well. This will help in the forecasting for the next

production to the company.

The Profit and loss Statement are given below for the advance model both from traditional

and ABC costing:

Financial statement of basic Model

Particulars ($)

Traditional ABC

Sales(unit)

1,500.0

0 1500

Sales price (cost + 120%)

1,137.5

8 1123.595215

Sales Price (a) 17,06,367.00 1685392.823

Direct material cost 8,40,000.00 8,40,000.00

Direct labour cost 3,90,000.00 3,90,000.00

Total direct cost 12,30,000.00 12,30,000.00

Overhead costs 1,91,972.50

selling and administration 1,40,600.00

interest expense 25,200.00

office rent 35,900.00

Inspection 15,789.47

Assembly 38,250.00

Production Scheduling 95,454.55

Machine Set up 25,000.00

Total 1,91,972.50 3,76,194.02

Total cost (b) 14,21,972.50 16,06,194.02

Profit(a-b) 2,84,394.50 79,198.80

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6 | P a g e Business Accounting

Task 4

Actual overhead and Applied overhead

Overheads are usually the indirect cost incurred by the manufacturing companies like Sewing

Machine Ltd. These are the manufacturing cost other than the direct material and direct labor.

The actual overhead is nothing but the indirect manufacturing cost occurs in real and

recorded in the books. These overheads include the electricity, gas, water, rent etc. whereas

the applied overheads are those overheads which have been allocated to the manufactured

goods. Manufacturing overhead is usually applied, assigned or allocated according to the

annual overheads rate. Actual overhead and applied overheads are not similar to each other as

one is the actual cost and other is the cost assigned or allocated to the goods (Huang et al.,

2013).

Reasons for under/over applied overhead costs

In the organization, allocations of overheads are done. This allocation sometimes can be

under-allocated or over-allocated. If too much overhead has been applied to the jobs then it is

called the problem of over applied overheads. If too little overhead has been applying then it

is called the problem of under applied overheads. This over and under overheads are arises

because of the wrong allocation of the resources. This should be corrected and this correction

can be made through the use of the proper system of costing in the business (McIvor, 2013).

The reasons for over applied overheads are the increase in the labor cost that is not used

directly in the production of products. Another reason can be the method of absorption can be

wrong.

Ways to deal with under and over applied overheads

Task 4

Actual overhead and Applied overhead

Overheads are usually the indirect cost incurred by the manufacturing companies like Sewing

Machine Ltd. These are the manufacturing cost other than the direct material and direct labor.

The actual overhead is nothing but the indirect manufacturing cost occurs in real and

recorded in the books. These overheads include the electricity, gas, water, rent etc. whereas

the applied overheads are those overheads which have been allocated to the manufactured

goods. Manufacturing overhead is usually applied, assigned or allocated according to the

annual overheads rate. Actual overhead and applied overheads are not similar to each other as

one is the actual cost and other is the cost assigned or allocated to the goods (Huang et al.,

2013).

Reasons for under/over applied overhead costs

In the organization, allocations of overheads are done. This allocation sometimes can be

under-allocated or over-allocated. If too much overhead has been applied to the jobs then it is

called the problem of over applied overheads. If too little overhead has been applying then it

is called the problem of under applied overheads. This over and under overheads are arises

because of the wrong allocation of the resources. This should be corrected and this correction

can be made through the use of the proper system of costing in the business (McIvor, 2013).

The reasons for over applied overheads are the increase in the labor cost that is not used

directly in the production of products. Another reason can be the method of absorption can be

wrong.

Ways to deal with under and over applied overheads

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7 | P a g e Business Accounting

• This problem can be rectified by the measuring the difference between the actual and

applied overhead. This will be the amount the business has to adjust through the cost of

goods sold to bring it to the actual cost of the product. If the overhead is over applied then it

should be subtracted from the cost of goods sold to nullify the effect and if the overheads are

under applied then it should be added back to the cost of goods sold (Öker and Adıgüzel,

2016). This should be done at the end of the accounting period so that the books will show

the true and fair view.

• If the transfer is made at the end of the financial period then the under or over absorbed

cost or overhead should be carried forward to the next month. This carried forward will be

done in the month to month basis treating it as a deferred income if applied and deferred

expenses if over applied overheads are there.

• Another way to deal with the under or over applied overheads can be the use of the

supplementary rates which is calculated by dividing by the over and under-absorbed amount

by the actual base. If over recovered, then it will be adjusted by using the supplementary rate

in case of over absorption.

• The over and under overheads can be adjusted through by writing off in Profit and loss

account.

Task 5

Merits of ABC system

Accurate Product cost

Calculation of product cost is more realistic and practical by using the ABC costing in the

business operation. ABC costing brings reliability and accuracy in the calculation of the

• This problem can be rectified by the measuring the difference between the actual and

applied overhead. This will be the amount the business has to adjust through the cost of

goods sold to bring it to the actual cost of the product. If the overhead is over applied then it

should be subtracted from the cost of goods sold to nullify the effect and if the overheads are

under applied then it should be added back to the cost of goods sold (Öker and Adıgüzel,

2016). This should be done at the end of the accounting period so that the books will show

the true and fair view.

• If the transfer is made at the end of the financial period then the under or over absorbed

cost or overhead should be carried forward to the next month. This carried forward will be

done in the month to month basis treating it as a deferred income if applied and deferred

expenses if over applied overheads are there.

• Another way to deal with the under or over applied overheads can be the use of the

supplementary rates which is calculated by dividing by the over and under-absorbed amount

by the actual base. If over recovered, then it will be adjusted by using the supplementary rate

in case of over absorption.

• The over and under overheads can be adjusted through by writing off in Profit and loss

account.

Task 5

Merits of ABC system

Accurate Product cost

Calculation of product cost is more realistic and practical by using the ABC costing in the

business operation. ABC costing brings reliability and accuracy in the calculation of the

8 | P a g e Business Accounting

product cost. ABC recognizes the activities cause to root for not evaluating the right cost of

the product. It brings results when there is the high number of differentiation among the

manufactured goods such as low volume products, high-value products (Joung et al., 2013).

Tracing of overhead cost

ABC costing traces all the cost related to the areas of managerial responsibilities, processes,

customers, departments besides the product costs. It also sets the standards and benchmarks

for the other methods to calculate the cost. As ABC is a unique way of calculating the cost

(Javid et al., 2016).

Information about the cost behaviour

ABC analysis helps to know about the real nature of the costs and helps in decrease them by

analysing and knowing those activities which are not relevant or make increase in the product

value. Using ABC managers can able to reduce its fixed overhead cost by having more

control over the activities. This can be done because the cost in relation to the fixed costs are

now more visible and gives clear image to the managers (Ríos-Manríquez, Colomina and

Pastor, 2014).

Better Decision Making

The use of ABC costing in the business improves the process of decision making in the

managers as they can use the reliable product data and cost data. It also takes into

consideration the six sigma and other continuous improvements programs.

Cost Management

ABC costing provides the cost driver rates and the other information related to the cost of the

products which helps a manager to have control over the cost. This will also help firmly in

product cost. ABC recognizes the activities cause to root for not evaluating the right cost of

the product. It brings results when there is the high number of differentiation among the

manufactured goods such as low volume products, high-value products (Joung et al., 2013).

Tracing of overhead cost

ABC costing traces all the cost related to the areas of managerial responsibilities, processes,

customers, departments besides the product costs. It also sets the standards and benchmarks

for the other methods to calculate the cost. As ABC is a unique way of calculating the cost

(Javid et al., 2016).

Information about the cost behaviour

ABC analysis helps to know about the real nature of the costs and helps in decrease them by

analysing and knowing those activities which are not relevant or make increase in the product

value. Using ABC managers can able to reduce its fixed overhead cost by having more

control over the activities. This can be done because the cost in relation to the fixed costs are

now more visible and gives clear image to the managers (Ríos-Manríquez, Colomina and

Pastor, 2014).

Better Decision Making

The use of ABC costing in the business improves the process of decision making in the

managers as they can use the reliable product data and cost data. It also takes into

consideration the six sigma and other continuous improvements programs.

Cost Management

ABC costing provides the cost driver rates and the other information related to the cost of the

products which helps a manager to have control over the cost. This will also help firmly in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9 | P a g e Business Accounting

the performance appraisal of responsibility centres. In Sewing Machine Ltd, the cost drivers

are also helped to maintain the design of the new product or existing product as they indicate

the overhead costs that are likely to be applied in the costing of the product (Kastalli and Van

Looy, 2013).

Use of Excess capacity and reduction in cost

Through the process of pooling activity done in cost, helps to reduce the overhead expenses.

The cost of the activity and identification of cost, drivers can lead to a range of applications.

The cost drivers are there to reduce to identify the cost and try to find the ways for reducing

the cost. The resources are also saved from wastage by using the ABC costing. The

expenditure on unnecessary expenses can be saved by using the cost pool and cost drivers

(Goodrich et al., 2013).

Demerits of ABC system

Expensive in nature

Implementing the ABC costing in the business is quite an expensive way. It involves various

other hidden costs. As Sewing machine Ltd. Activities are analyses, they must be broken into

small tasks or jobs. This entire process can value up against the resources, as data are

collected, measured and entered into the new system. As this type of costing is not simple in

nature, the experts are hired for the same. It will also increase the cost and some training is

given to the employees of the organization so that they can use this type of cost without any

mistakes (Wittbrodt et al., 2013).

Time taken and complex

the performance appraisal of responsibility centres. In Sewing Machine Ltd, the cost drivers

are also helped to maintain the design of the new product or existing product as they indicate

the overhead costs that are likely to be applied in the costing of the product (Kastalli and Van

Looy, 2013).

Use of Excess capacity and reduction in cost

Through the process of pooling activity done in cost, helps to reduce the overhead expenses.

The cost of the activity and identification of cost, drivers can lead to a range of applications.

The cost drivers are there to reduce to identify the cost and try to find the ways for reducing

the cost. The resources are also saved from wastage by using the ABC costing. The

expenditure on unnecessary expenses can be saved by using the cost pool and cost drivers

(Goodrich et al., 2013).

Demerits of ABC system

Expensive in nature

Implementing the ABC costing in the business is quite an expensive way. It involves various

other hidden costs. As Sewing machine Ltd. Activities are analyses, they must be broken into

small tasks or jobs. This entire process can value up against the resources, as data are

collected, measured and entered into the new system. As this type of costing is not simple in

nature, the experts are hired for the same. It will also increase the cost and some training is

given to the employees of the organization so that they can use this type of cost without any

mistakes (Wittbrodt et al., 2013).

Time taken and complex

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10 | P a g e Business Accounting

ABC costing is also the time taking the process as the calculations in this required a bit more

time than the traditional as it believes in the concept of accuracy. ABC costing is also

complex in nature as it includes many cost drivers and cost pools which make the working

complex than the traditional product costing system (Kapić, 2014). This cost technique will

become time taking, costly and complex to the Sewing Machine Ltd.

Misinterpretation of the data

Reports made by an ABC costing include information which can differ from the information

given in the traditional costing system. It is the possibility that some activities are found to be

irrelevant in a certain process of decision-making.

For example:

ABC costing does not agree with the concepts of the accounting standards and they are also

not used for the external reporting.

Before ABC costing, mostly organization is using the traditional way of cost analysis. So

there are chances of misinterpretations of figures and facts that the manager can do while

interpreting the accounts. It will also lead to the bad decision making in analyzing the cost

(Monroy, Nasiri, and Peláez, 2014).

Selection of Drivers

It became a difficult task to select a driver from many drivers available. Many difficulties can

emerge from the use of ABC system of costing. Cost drivers selection, assigning of common

cost, different cost driver rates etc.

Measuring Difficulties

ABC costing is also the time taking the process as the calculations in this required a bit more

time than the traditional as it believes in the concept of accuracy. ABC costing is also

complex in nature as it includes many cost drivers and cost pools which make the working

complex than the traditional product costing system (Kapić, 2014). This cost technique will

become time taking, costly and complex to the Sewing Machine Ltd.

Misinterpretation of the data

Reports made by an ABC costing include information which can differ from the information

given in the traditional costing system. It is the possibility that some activities are found to be

irrelevant in a certain process of decision-making.

For example:

ABC costing does not agree with the concepts of the accounting standards and they are also

not used for the external reporting.

Before ABC costing, mostly organization is using the traditional way of cost analysis. So

there are chances of misinterpretations of figures and facts that the manager can do while

interpreting the accounts. It will also lead to the bad decision making in analyzing the cost

(Monroy, Nasiri, and Peláez, 2014).

Selection of Drivers

It became a difficult task to select a driver from many drivers available. Many difficulties can

emerge from the use of ABC system of costing. Cost drivers selection, assigning of common

cost, different cost driver rates etc.

Measuring Difficulties

11 | P a g e Business Accounting

Measuring difficulties in the implementation in ABC Costing is done by the management.

The management estimates the cost involved in the pooling of activity in the ABC system of

costing. To identify and measure cost drivers to serve as cost allocation base. The

measurement is also found to be costly and requires time to time updates (Petrick and

Simpson, 2013).

Measuring difficulties in the implementation in ABC Costing is done by the management.

The management estimates the cost involved in the pooling of activity in the ABC system of

costing. To identify and measure cost drivers to serve as cost allocation base. The

measurement is also found to be costly and requires time to time updates (Petrick and

Simpson, 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.