Financial Management: Activity Based Costing Application at Unilever

VerifiedAdded on 2023/06/10

|17

|1379

|456

Report

AI Summary

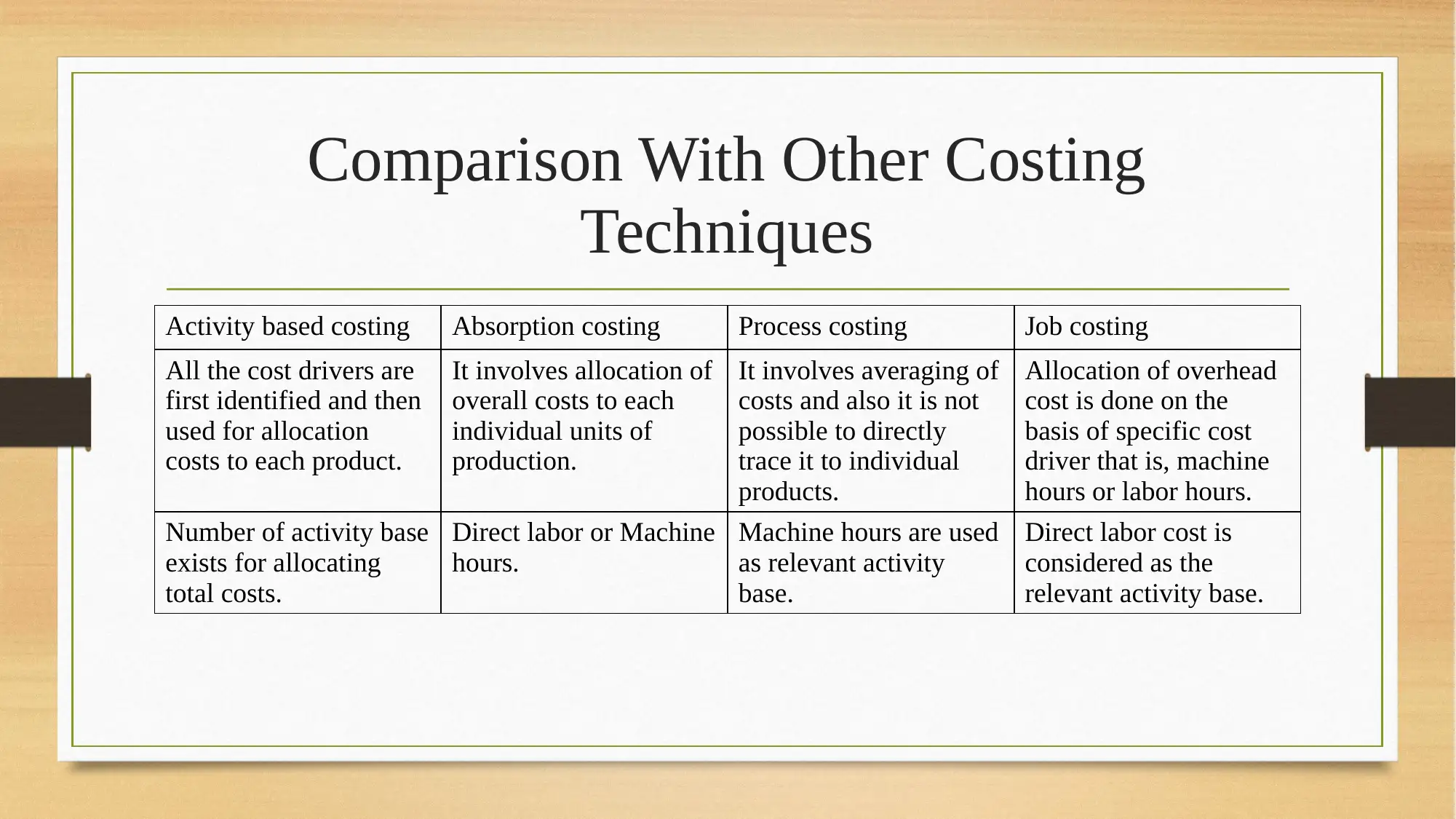

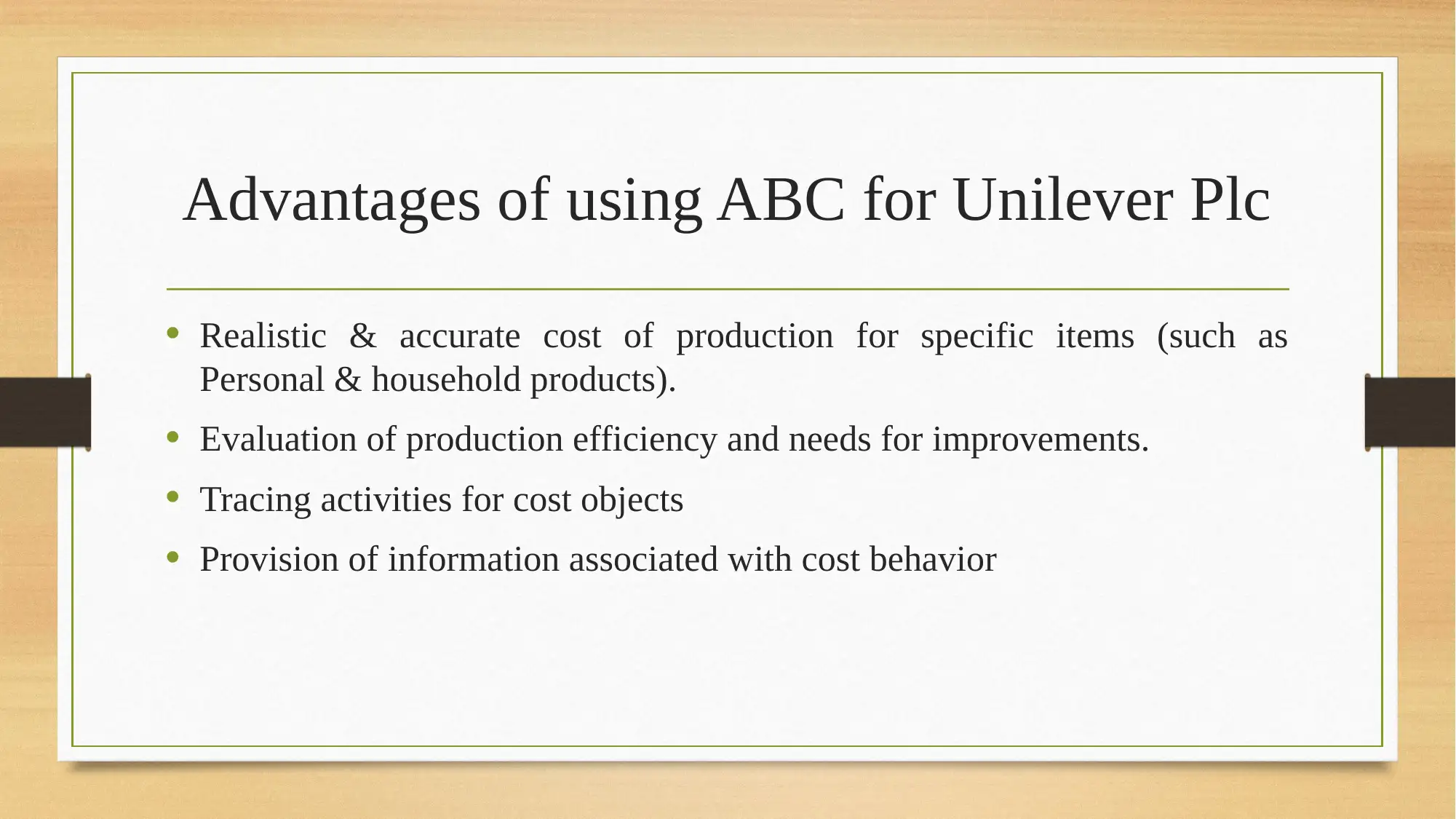

This report provides a detailed analysis of Activity Based Costing (ABC) and its application within Unilever Plc's financial management framework. It begins by defining ABC and comparing it with other costing systems like absorption, process, and job costing. The report then elaborates on how ABC can be implemented at Unilever, focusing on resource drivers, activities, activity drivers, cost objects, and activity cost drivers specific to personal and household product lines. It highlights the advantages of using ABC, such as realistic cost assessment and improved efficiency evaluation, as well as its disadvantages, including complexity and resource intensity. A comparison with traditional costing techniques is presented, emphasizing the benefits of ABC in terms of accurate cost allocation and understanding overheads. The report concludes by referencing several academic sources that support the analysis of ABC in organizational settings.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.