Activity-Based Management in Strategic Accounting - ACT302

VerifiedAdded on 2023/01/16

|12

|2787

|45

Report

AI Summary

This report delves into the intricacies of Activity-Based Management (ABM), exploring its core principles and practical applications within the realm of strategic accounting. It examines the nature of ABM, emphasizing its role in cost management and performance evaluation. The report dissects the ABM model, including cost driver analysis, activity analysis, and value-added versus non-value-added activities. Furthermore, it explores the applications of ABM in various business operations, such as cost reduction, activity-based budgeting, business process reengineering, benchmarking, and performance measurement. A significant portion of the report is dedicated to how ABM can ensure quality management and environmental sustainability, discussing its role in developing corporate strategy, making activity analysis, and improving operational processes. The report concludes by highlighting the importance of ABM in both local and public sector organizations, emphasizing the benefits of a well-designed and implemented ABM system for achieving quality management and sustainable business practices. The report fulfills the requirements of the ACT302 course, which focused on Strategic Management Accounting.

Activity-Based Management 1

Activity-Based Management

Name:

Institution:

Course:

Tutor:

Date:

Activity-Based Management

Name:

Institution:

Course:

Tutor:

Date:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity-Based Management 2

Nature of Activity-Based Management

The notion of Activity Based Management commonly abbreviated as ABM refers to the

management of cost execution of activity-based costing. It is mostly stand to be approach of

management that concentrates on efficiently together with effective management of various

activities so as to enhance the quality of services and goods being offered to the clients and also

enhance competitiveness together with revenue of the organization. ABM utilizes the Activity

Based Costing (ABC) as a device for controlling the activity stages (Taba 2017). Here, ABC also

stands out as system that stresses on operations that are conducted for producing different

products. It broadly comprises of different aspects that consist of decisions of product mix, cost

reduction together with process enhancement decisions, along with decisions of product design.

It has several ways in which it can be used efficiently to support the operations of organizations

(Kang 2015). For instance, it can be utilized to establish the total productivity of the client

founded on returns of sales, procurements of clients, and application of time of the client service

section. It can also be applied to agree on the total abundance of the advanced products rooted on

its transactions in the marketplace, mend time needed for dispatched goods. Besides, it can be

utilized to ascertain the total success of research and design section, anchored in spends fund and

result of advanced development of products around different markets (Huynh 2013). Therefore,

the primary focus of this research paper is to assess Major issues related to the execution and use

of ABM in the framework of performance evaluation, management of chain of supply, quality

administration and environmental sustainability, while satisfying an organization’s stakeholders

and ensuring long-term viability and sustainability of the organization

Major issues related to the implementation and use of Activity Based Management (ABM)

Nature of Activity-Based Management

The notion of Activity Based Management commonly abbreviated as ABM refers to the

management of cost execution of activity-based costing. It is mostly stand to be approach of

management that concentrates on efficiently together with effective management of various

activities so as to enhance the quality of services and goods being offered to the clients and also

enhance competitiveness together with revenue of the organization. ABM utilizes the Activity

Based Costing (ABC) as a device for controlling the activity stages (Taba 2017). Here, ABC also

stands out as system that stresses on operations that are conducted for producing different

products. It broadly comprises of different aspects that consist of decisions of product mix, cost

reduction together with process enhancement decisions, along with decisions of product design.

It has several ways in which it can be used efficiently to support the operations of organizations

(Kang 2015). For instance, it can be utilized to establish the total productivity of the client

founded on returns of sales, procurements of clients, and application of time of the client service

section. It can also be applied to agree on the total abundance of the advanced products rooted on

its transactions in the marketplace, mend time needed for dispatched goods. Besides, it can be

utilized to ascertain the total success of research and design section, anchored in spends fund and

result of advanced development of products around different markets (Huynh 2013). Therefore,

the primary focus of this research paper is to assess Major issues related to the execution and use

of ABM in the framework of performance evaluation, management of chain of supply, quality

administration and environmental sustainability, while satisfying an organization’s stakeholders

and ensuring long-term viability and sustainability of the organization

Major issues related to the implementation and use of Activity Based Management (ABM)

Activity-Based Management 3

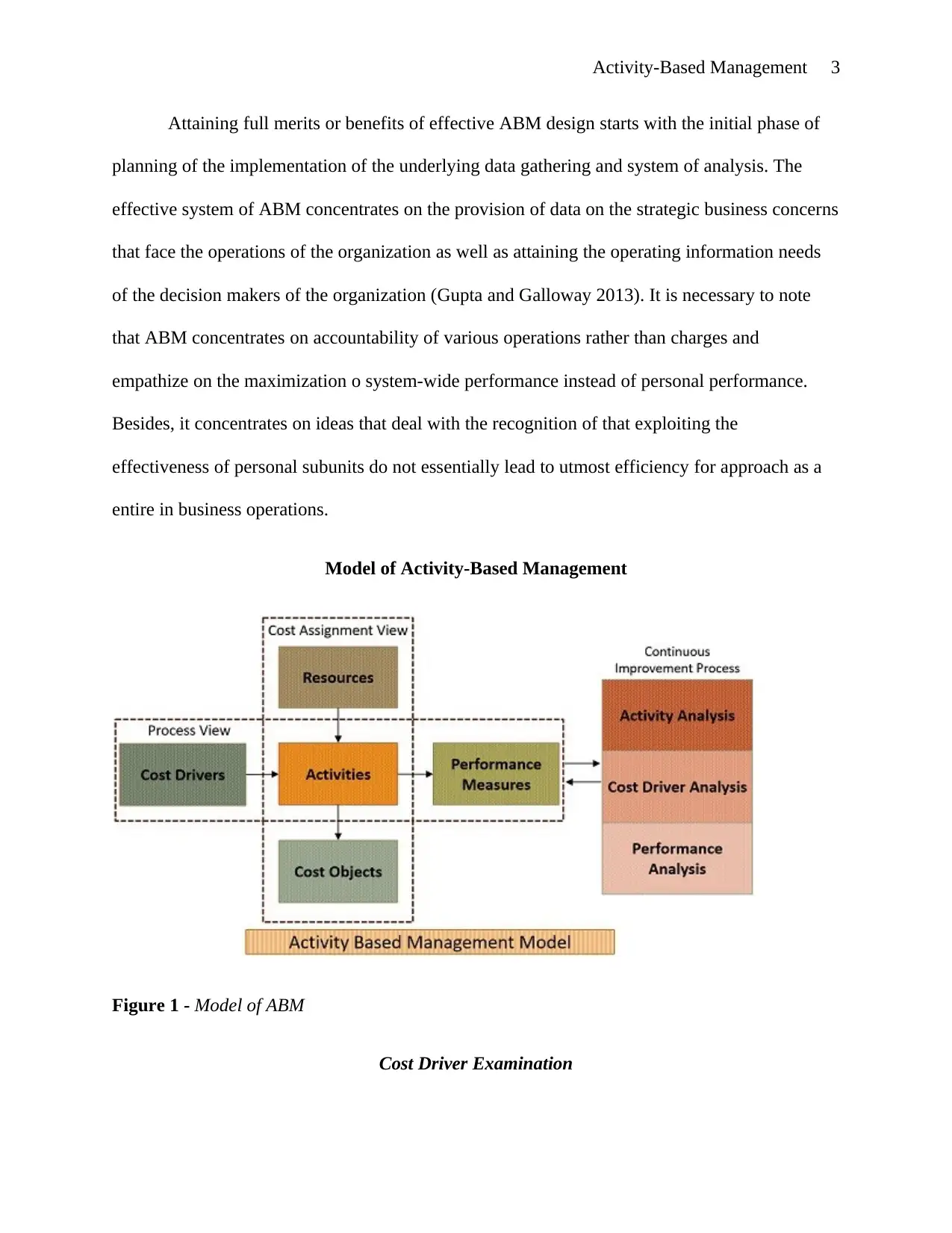

Attaining full merits or benefits of effective ABM design starts with the initial phase of

planning of the implementation of the underlying data gathering and system of analysis. The

effective system of ABM concentrates on the provision of data on the strategic business concerns

that face the operations of the organization as well as attaining the operating information needs

of the decision makers of the organization (Gupta and Galloway 2013). It is necessary to note

that ABM concentrates on accountability of various operations rather than charges and

empathize on the maximization o system-wide performance instead of personal performance.

Besides, it concentrates on ideas that deal with the recognition of that exploiting the

effectiveness of personal subunits do not essentially lead to utmost efficiency for approach as a

entire in business operations.

Model of Activity-Based Management

Figure 1 - Model of ABM

Cost Driver Examination

Attaining full merits or benefits of effective ABM design starts with the initial phase of

planning of the implementation of the underlying data gathering and system of analysis. The

effective system of ABM concentrates on the provision of data on the strategic business concerns

that face the operations of the organization as well as attaining the operating information needs

of the decision makers of the organization (Gupta and Galloway 2013). It is necessary to note

that ABM concentrates on accountability of various operations rather than charges and

empathize on the maximization o system-wide performance instead of personal performance.

Besides, it concentrates on ideas that deal with the recognition of that exploiting the

effectiveness of personal subunits do not essentially lead to utmost efficiency for approach as a

entire in business operations.

Model of Activity-Based Management

Figure 1 - Model of ABM

Cost Driver Examination

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity-Based Management 4

It is a concern with the idea of managing the activity cares, the elements that result in

actions to take in consideration are identified at the stage.

Activity analysis

It is a concern with idea of finding out the operations of the organizations together with

its centers that ought to be used in concept of Costing of Activity Based. Based on the benefits

together with benefits of the alternatives, the operations are sub-divided into the number of

activity centers (Orams 2013). Further, it ascertains value added together with activities of non-

value supplementary in actions.

Value added actions

The stage comprises of different activities that are very vital for the completion of the

processes that are categorized as value-added procedures.

Non-Value Added Operations

They submit to those activities that do not possess any value for both external and

internal clients and are a term to be Non-Vale added operations. Indeed such activities do not

improve the product quality rather they have a negative effect on the prices of the services or

products as they develop wastes, delays, and improve the overall value of different operations.

Analysis of performance

The stage comprises of discovering the appropriate measure useful in analyzing the

performance of the activity centers. Therefore, with such analysis, Activity-Based Management

concentrates at managing the organization by ascertains what directs the activities of the

company and how they can be enhanced (Udvalnorov 2018).

It is a concern with the idea of managing the activity cares, the elements that result in

actions to take in consideration are identified at the stage.

Activity analysis

It is a concern with idea of finding out the operations of the organizations together with

its centers that ought to be used in concept of Costing of Activity Based. Based on the benefits

together with benefits of the alternatives, the operations are sub-divided into the number of

activity centers (Orams 2013). Further, it ascertains value added together with activities of non-

value supplementary in actions.

Value added actions

The stage comprises of different activities that are very vital for the completion of the

processes that are categorized as value-added procedures.

Non-Value Added Operations

They submit to those activities that do not possess any value for both external and

internal clients and are a term to be Non-Vale added operations. Indeed such activities do not

improve the product quality rather they have a negative effect on the prices of the services or

products as they develop wastes, delays, and improve the overall value of different operations.

Analysis of performance

The stage comprises of discovering the appropriate measure useful in analyzing the

performance of the activity centers. Therefore, with such analysis, Activity-Based Management

concentrates at managing the organization by ascertains what directs the activities of the

company and how they can be enhanced (Udvalnorov 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity-Based Management 5

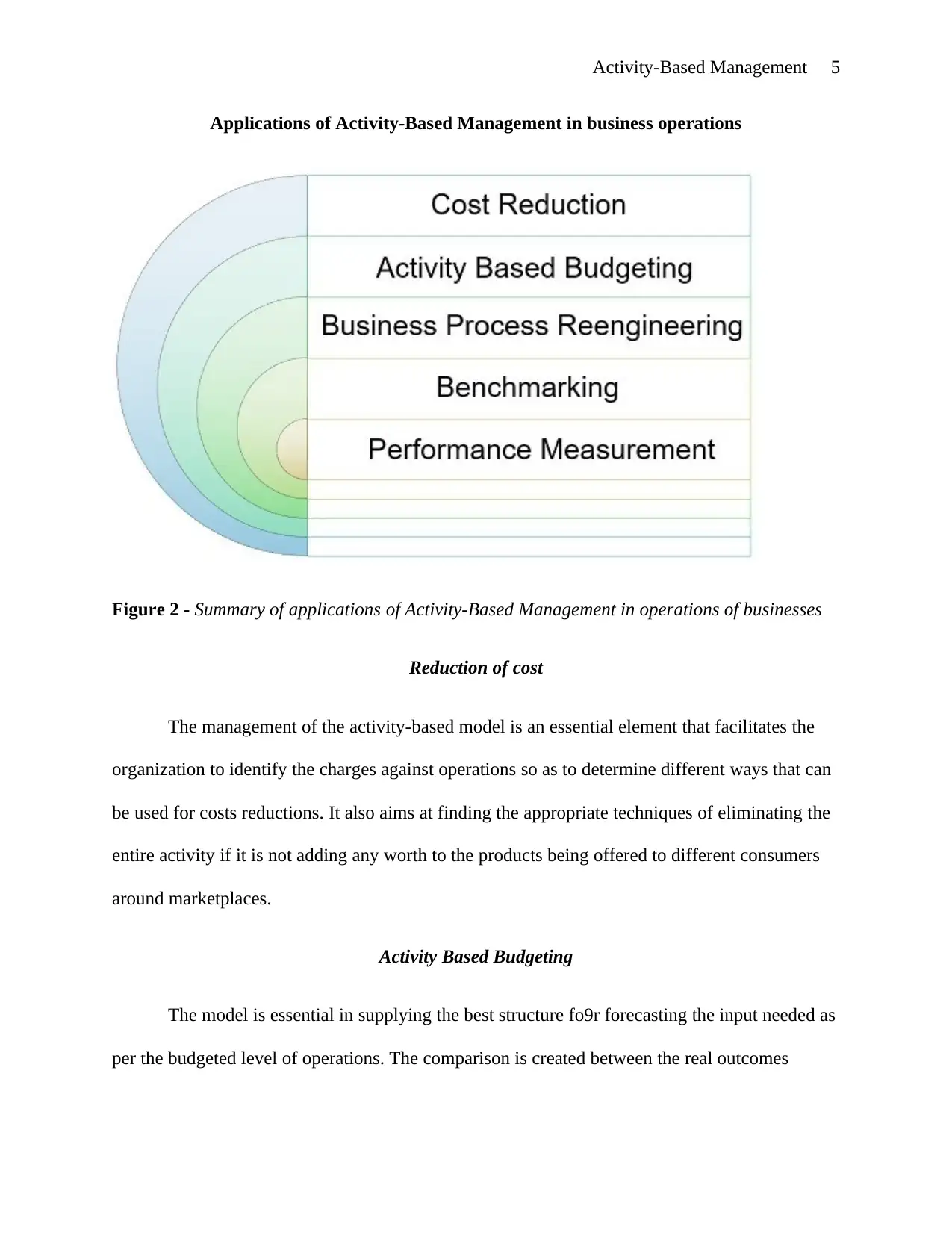

Applications of Activity-Based Management in business operations

Figure 2 - Summary of applications of Activity-Based Management in operations of businesses

Reduction of cost

The management of the activity-based model is an essential element that facilitates the

organization to identify the charges against operations so as to determine different ways that can

be used for costs reductions. It also aims at finding the appropriate techniques of eliminating the

entire activity if it is not adding any worth to the products being offered to different consumers

around marketplaces.

Activity Based Budgeting

The model is essential in supplying the best structure fo9r forecasting the input needed as

per the budgeted level of operations. The comparison is created between the real outcomes

Applications of Activity-Based Management in business operations

Figure 2 - Summary of applications of Activity-Based Management in operations of businesses

Reduction of cost

The management of the activity-based model is an essential element that facilitates the

organization to identify the charges against operations so as to determine different ways that can

be used for costs reductions. It also aims at finding the appropriate techniques of eliminating the

entire activity if it is not adding any worth to the products being offered to different consumers

around marketplaces.

Activity Based Budgeting

The model is essential in supplying the best structure fo9r forecasting the input needed as

per the budgeted level of operations. The comparison is created between the real outcomes

Activity-Based Management 6

together with estimated outcomes to help in the process of outlining the activities with the high-

level variances from the budget for the probable reduction in the input of supply (Pokorná 2016).

Reengineering of business process

The idea of using ABM entails the idea of examining as well as redesigning the processes

together with workflows of the corporation for enhancing the performance that targets at gaining

the excellence in operations of businesses. It comprises of the idea of creating significant

variations regarding how organizations operate in the present business society (Hughes 2015).

The concept of ABM concerns with the idea of creating significant shifts regarding how different

corporations operates in the current business society. Additionally, ABM assists in enhancing the

business process efficiency together with business effectiveness.

Benchmarking

It comprises of the process of creating a necessary comparison of the products together

with services offered by the organization with that of the other corporations. It concentrates at

the identification of ideal approaches to enhance the products and services of the organization

(Hasan 2017).

Measurement of performance

In present business days, several firms concentrate on activity performance by observing

the efficiency as well as operational effectiveness through the idea of concentrating on observing

the effectiveness along with the efficiency of operations. The idea of such observations is crucial

in business operations as it ensures that every business competes successfully around different

marketplaces (Chouhan, Soral, and Chandra 2017). According Kren (2018), it is necessary to

together with estimated outcomes to help in the process of outlining the activities with the high-

level variances from the budget for the probable reduction in the input of supply (Pokorná 2016).

Reengineering of business process

The idea of using ABM entails the idea of examining as well as redesigning the processes

together with workflows of the corporation for enhancing the performance that targets at gaining

the excellence in operations of businesses. It comprises of the idea of creating significant

variations regarding how organizations operate in the present business society (Hughes 2015).

The concept of ABM concerns with the idea of creating significant shifts regarding how different

corporations operates in the current business society. Additionally, ABM assists in enhancing the

business process efficiency together with business effectiveness.

Benchmarking

It comprises of the process of creating a necessary comparison of the products together

with services offered by the organization with that of the other corporations. It concentrates at

the identification of ideal approaches to enhance the products and services of the organization

(Hasan 2017).

Measurement of performance

In present business days, several firms concentrate on activity performance by observing

the efficiency as well as operational effectiveness through the idea of concentrating on observing

the effectiveness along with the efficiency of operations. The idea of such observations is crucial

in business operations as it ensures that every business competes successfully around different

marketplaces (Chouhan, Soral, and Chandra 2017). According Kren (2018), it is necessary to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity-Based Management 7

note that ABM is not a mere approach but also the management philosophy that is oriented

towards ideas of planning, measurements, together with the implementation of different activities

in business. Besides, ABM also assists in reducing costs and also provides the appropriate

foundation for management of processes of making decisions.

How Activity-Based Management (and associated performance evaluation and supply

chain management) can be used to ensure quality management and environmental

sustainability

ABM can be used as approach towards ensuring quality management and environmental

sustainability in diverse ways. It can form the approach to management that aims at maximizing

the value-adding operations while concentrating on ideas of minimizing or eliminating activities

that do not add value in the operations. It can be used to improve the efficiencies together with

the effectiveness of the organization in securing its marketplace (Joao Major 2014). The use of

ABM ca draw different data from ABC as its principal basis of data, along with this will help it in

focusing on different operations. Such operations can include minimizing costs of operations,

developing performance measures, enhancing the flow of business cash and quality products, as

well as producing improved value products. The ABM can be used in different steps to ensure

quality management and environmental sustainability (Hashim 2013). These steps can comprise

of recognition of major activities, measuring resources utilized by every business operation,

assessing the presentation or each activity, and finding ideal techniques to enhance competence

alongside effectiveness. Therefore, ABM offers idea procedure that has been in existence since

its origination in the early days of the 1980s. The procedure is useful in improving processes of

analysis of business operations that aim at improving the manner of identifying different

strengths and weaknesses during operations. The process of using ABM can seek out regions

note that ABM is not a mere approach but also the management philosophy that is oriented

towards ideas of planning, measurements, together with the implementation of different activities

in business. Besides, ABM also assists in reducing costs and also provides the appropriate

foundation for management of processes of making decisions.

How Activity-Based Management (and associated performance evaluation and supply

chain management) can be used to ensure quality management and environmental

sustainability

ABM can be used as approach towards ensuring quality management and environmental

sustainability in diverse ways. It can form the approach to management that aims at maximizing

the value-adding operations while concentrating on ideas of minimizing or eliminating activities

that do not add value in the operations. It can be used to improve the efficiencies together with

the effectiveness of the organization in securing its marketplace (Joao Major 2014). The use of

ABM ca draw different data from ABC as its principal basis of data, along with this will help it in

focusing on different operations. Such operations can include minimizing costs of operations,

developing performance measures, enhancing the flow of business cash and quality products, as

well as producing improved value products. The ABM can be used in different steps to ensure

quality management and environmental sustainability (Hashim 2013). These steps can comprise

of recognition of major activities, measuring resources utilized by every business operation,

assessing the presentation or each activity, and finding ideal techniques to enhance competence

alongside effectiveness. Therefore, ABM offers idea procedure that has been in existence since

its origination in the early days of the 1980s. The procedure is useful in improving processes of

analysis of business operations that aim at improving the manner of identifying different

strengths and weaknesses during operations. The process of using ABM can seek out regions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity-Based Management 8

where the trade is losing finances so that every activity can be abolished or enhanced to improve

success (Kashmanian 2015). Besides, ABM can be used to ensure quality management by

ensuring that it increases the process of analyzing charge of workers, equipment, amenities,

allocation, overhead, together with extra elements in business operations. The idea can be

essential in determining and allocating activity costs during operations thus leading to a

sustainable business working environment.

Most organizations can use ABM in various approaches. For instance, they can use the

approach in developing a corporate strategy as well as making activity analysis as a way of

ensuring quality management together with environmental sustainability. In the developing

corporate strategy, ABM can aid different organizations to create an appropriate strategy of the

organization by focusing on long term ideas and competitive merits by concentrating on and

managing their operations. It ensures that every operation is in line with sustainable ideas as

required by the authority (Pokorná 2016). Additionally, some organizations have competitive

merit by offering the low valued products or manage operations to decrease operational costs

hence leading to sustainable business settings — the use of ABM help in reducing operational

costs that is always necessary for changes needed in operations. By using ABM, every business

operator can be capable to decrease operational charges if the operation is closed leading to

reduced costs. Udvalnorov (2018) denoted that ABM has the aim of reducing or cutting costs of

operations to fit the environmental needs leading to a sustainable business setting. Besides, the

use of ABM has the principal objective of reducing charges while maintaining quantity along

with the quality of business output.

ABM can be used to ensure the management of quality and environmental sustainability

by improving how a business conducts its making activity analysis. ABM targets at attaining

where the trade is losing finances so that every activity can be abolished or enhanced to improve

success (Kashmanian 2015). Besides, ABM can be used to ensure quality management by

ensuring that it increases the process of analyzing charge of workers, equipment, amenities,

allocation, overhead, together with extra elements in business operations. The idea can be

essential in determining and allocating activity costs during operations thus leading to a

sustainable business working environment.

Most organizations can use ABM in various approaches. For instance, they can use the

approach in developing a corporate strategy as well as making activity analysis as a way of

ensuring quality management together with environmental sustainability. In the developing

corporate strategy, ABM can aid different organizations to create an appropriate strategy of the

organization by focusing on long term ideas and competitive merits by concentrating on and

managing their operations. It ensures that every operation is in line with sustainable ideas as

required by the authority (Pokorná 2016). Additionally, some organizations have competitive

merit by offering the low valued products or manage operations to decrease operational costs

hence leading to sustainable business settings — the use of ABM help in reducing operational

costs that is always necessary for changes needed in operations. By using ABM, every business

operator can be capable to decrease operational charges if the operation is closed leading to

reduced costs. Udvalnorov (2018) denoted that ABM has the aim of reducing or cutting costs of

operations to fit the environmental needs leading to a sustainable business setting. Besides, the

use of ABM has the principal objective of reducing charges while maintaining quantity along

with the quality of business output.

ABM can be used to ensure the management of quality and environmental sustainability

by improving how a business conducts its making activity analysis. ABM targets at attaining

Activity-Based Management 9

continuous enhancement by making activity analysis (Lee and Kashmanian 2013). They achieve

such operations y classifying every operation as value-supplementary or non-supplementary

added. Besides, value-added operation refers to operation that adds worth to service or product

from viewpoint of client. The non-value-supplemented operation remains to be operation that fails

to add any value to service or product from the point of view of the targeted or esteemed

customers (Chouhan, Soral, and Chandra 2017). Besides, the value added actions make up value

chain that ensures management of quality and sustainability of business techniques used in the

operations. The value chain is connected with different sets of value-generating actions from

sources of raw resources to the ultimate end utilization of goods or produced environment-

friendly services. Therefore, ABM usage in organizations can ensure quality management as it

helps in improving the manager management make strategic decisions, how they conduct

operation analysis, improve processes of operations, and conducting benchmarking in other

organizations (Gupta and Galloway 2013). The benchmarking plan help in ensuring that

organization work in line with other ionizations so as to attain the best working plan of

improving their day-to-day business operations.

Conclusion

Both local, as well as public sector organizations, are starting to apply the concept of

ABM for different purposes that aim at ensuring quality management in their operations and

achieving sustainable business environment. It is clear from this assessment that gaining the full

benefits of Activity Base Management lies entirely in assessment, designing, together with the

implementation of the underlying data gathered and analysis system. The effective system or

approach of ABM concentrates on offering essential data that relates to strategic business

concerns facing the organization and meeting the requirements of operating data of the makers of

continuous enhancement by making activity analysis (Lee and Kashmanian 2013). They achieve

such operations y classifying every operation as value-supplementary or non-supplementary

added. Besides, value-added operation refers to operation that adds worth to service or product

from viewpoint of client. The non-value-supplemented operation remains to be operation that fails

to add any value to service or product from the point of view of the targeted or esteemed

customers (Chouhan, Soral, and Chandra 2017). Besides, the value added actions make up value

chain that ensures management of quality and sustainability of business techniques used in the

operations. The value chain is connected with different sets of value-generating actions from

sources of raw resources to the ultimate end utilization of goods or produced environment-

friendly services. Therefore, ABM usage in organizations can ensure quality management as it

helps in improving the manager management make strategic decisions, how they conduct

operation analysis, improve processes of operations, and conducting benchmarking in other

organizations (Gupta and Galloway 2013). The benchmarking plan help in ensuring that

organization work in line with other ionizations so as to attain the best working plan of

improving their day-to-day business operations.

Conclusion

Both local, as well as public sector organizations, are starting to apply the concept of

ABM for different purposes that aim at ensuring quality management in their operations and

achieving sustainable business environment. It is clear from this assessment that gaining the full

benefits of Activity Base Management lies entirely in assessment, designing, together with the

implementation of the underlying data gathered and analysis system. The effective system or

approach of ABM concentrates on offering essential data that relates to strategic business

concerns facing the organization and meeting the requirements of operating data of the makers of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity-Based Management 10

decisions within an organization. The achievement of robust and effective design that can ensure

quality management and environmental sustainability of ABM commence with the initial phase

of planning of the implementation and continues throughout the development of ongoing

improvements and adjustments to the system as the need changes within an organization. It is

apparent from the discussion that the method of ABM is extremely vital to enhance

performances of the enterprises on different fronts. However, enterprises become the

consciousness of ABM significance only when the right individual or persons are responsible for

assessing the appropriate data for creating ideal decisions and improve the performances of the

organization.

decisions within an organization. The achievement of robust and effective design that can ensure

quality management and environmental sustainability of ABM commence with the initial phase

of planning of the implementation and continues throughout the development of ongoing

improvements and adjustments to the system as the need changes within an organization. It is

apparent from the discussion that the method of ABM is extremely vital to enhance

performances of the enterprises on different fronts. However, enterprises become the

consciousness of ABM significance only when the right individual or persons are responsible for

assessing the appropriate data for creating ideal decisions and improve the performances of the

organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity-Based Management 11

List of References

Chouhan, V., Soral, G. and Chandra, B. (2017). Activity based costing model for inventory

valuation. Management Science Letters, pp.135-144.

Gupta, M. and Galloway, K. (2013). Activity-based costing/management and its implications for

operations management. Technovation, 23(2), pp.131-138.

Hasan, A. (2017). Implementation Problems of Activity Based Costing: A Study of Companies

in Jordan. British Journal of Economics, Management & Trade, 17(1), pp.1-9.

Hashim, J. (2013). Activity-based costing (ABC) Model for Public Higher Education Institutions

(PHEI) : A guide for a Model development. International Journal Of Management &

Information Technology, 7(3), pp.1089-1100.

Hoozée, S. and Hansen, S. (2018). A Comparison of Activity-Based Costing and Time-Driven

Activity-Based Costing. Journal of Management Accounting Research, 30(1), pp.143-167.

Hughes, A. (2015). ABC/ABM – activity‐based costing and activity‐based management. Journal

of Fashion Marketing and Management: An International Journal, 9(1), pp.8-19.

Huynh, T. (2013). Integration of Activity-Based Budgeting and Activity-Based Management.

International Journal of Economics, Finance and Management Sciences, 1(4), p.181.

Joao Major, M. (2014). Implementing Activity-Based Costing in the Telecommunications

Sector: A Case Study. Journal of Telecommunications System & Management, 03(01).

List of References

Chouhan, V., Soral, G. and Chandra, B. (2017). Activity based costing model for inventory

valuation. Management Science Letters, pp.135-144.

Gupta, M. and Galloway, K. (2013). Activity-based costing/management and its implications for

operations management. Technovation, 23(2), pp.131-138.

Hasan, A. (2017). Implementation Problems of Activity Based Costing: A Study of Companies

in Jordan. British Journal of Economics, Management & Trade, 17(1), pp.1-9.

Hashim, J. (2013). Activity-based costing (ABC) Model for Public Higher Education Institutions

(PHEI) : A guide for a Model development. International Journal Of Management &

Information Technology, 7(3), pp.1089-1100.

Hoozée, S. and Hansen, S. (2018). A Comparison of Activity-Based Costing and Time-Driven

Activity-Based Costing. Journal of Management Accounting Research, 30(1), pp.143-167.

Hughes, A. (2015). ABC/ABM – activity‐based costing and activity‐based management. Journal

of Fashion Marketing and Management: An International Journal, 9(1), pp.8-19.

Huynh, T. (2013). Integration of Activity-Based Budgeting and Activity-Based Management.

International Journal of Economics, Finance and Management Sciences, 1(4), p.181.

Joao Major, M. (2014). Implementing Activity-Based Costing in the Telecommunications

Sector: A Case Study. Journal of Telecommunications System & Management, 03(01).

Activity-Based Management 12

Kang, M. (2015). Activity-based Costing Research on Enterprise Logistics Cost Management.

Business and Management Research, 4(2), pp.1.

Kashmanian, R. (2015). Building a Sustainable Supply Chain: Key Elements. Environmental

Quality Management, 24(3), pp.17-41.

Kren, L. (2018). Activity Based Management (ABM) and Control System design. Accounting

and Finance Research, 7(2), p.61.

Lee, T. and Kashmanian, R. (2013). Supply Chain Sustainability: Compliance- and Performance-

Based Tools. Environmental Quality Management, 22(4), pp.1-23.

Orams, M. (2013). Economic Activity Derived from Whale-Based Tourism in Vava'u, Tonga.

Coastal Management, 41(6), pp.481-500.

Pokorná, J. (2016). The Expansion of Activity-Based Costing/Management in the Czech

Republic. Central European Journal of Management, 2(1,2), pp.5.

Taba, M. (2017). The Smooth Implementation of Activity Based Cost Management (ABCM) in

the Public Service Organisation (PSO) in South Africa. SSRN Electronic Journal, 1(3), pp.21-52.

Udvalnorov, C. (2018). Technological management of rational nature management (based on the

datas from coal deposits in Mongolia). Economics and Environmental Management, pp.110-121.

Kang, M. (2015). Activity-based Costing Research on Enterprise Logistics Cost Management.

Business and Management Research, 4(2), pp.1.

Kashmanian, R. (2015). Building a Sustainable Supply Chain: Key Elements. Environmental

Quality Management, 24(3), pp.17-41.

Kren, L. (2018). Activity Based Management (ABM) and Control System design. Accounting

and Finance Research, 7(2), p.61.

Lee, T. and Kashmanian, R. (2013). Supply Chain Sustainability: Compliance- and Performance-

Based Tools. Environmental Quality Management, 22(4), pp.1-23.

Orams, M. (2013). Economic Activity Derived from Whale-Based Tourism in Vava'u, Tonga.

Coastal Management, 41(6), pp.481-500.

Pokorná, J. (2016). The Expansion of Activity-Based Costing/Management in the Czech

Republic. Central European Journal of Management, 2(1,2), pp.5.

Taba, M. (2017). The Smooth Implementation of Activity Based Cost Management (ABCM) in

the Public Service Organisation (PSO) in South Africa. SSRN Electronic Journal, 1(3), pp.21-52.

Udvalnorov, C. (2018). Technological management of rational nature management (based on the

datas from coal deposits in Mongolia). Economics and Environmental Management, pp.110-121.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.