Comparative Costing Methods: Conventional vs. Activity-Based Costing

VerifiedAdded on 2020/04/07

|4

|930

|73

AI Summary

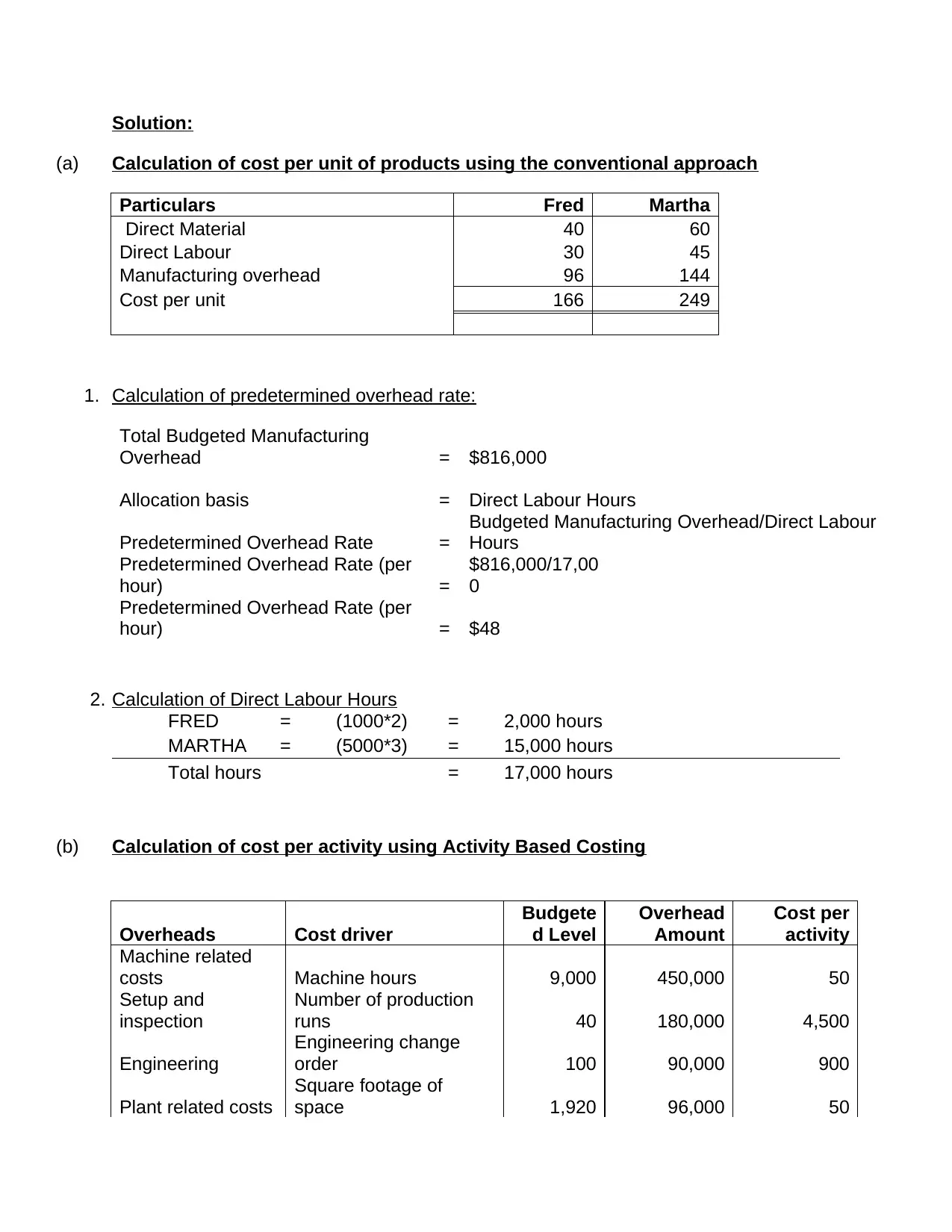

The assignment investigates two costing methodologies: Conventional Costing and Activity-Based Costing (ABC). It begins with calculating unit costs for products Fred and Martha using conventional costing, which allocates overhead based on direct labor hours. Here, Fred is priced at $166 per unit, while Martha is $249 per unit. The predetermined overhead rate is calculated as $48 per hour, based on a total budgeted manufacturing overhead of $816,000 divided by 17,000 direct labor hours. However, this approach may inaccurately distribute costs due to its reliance on direct labor hours alone.

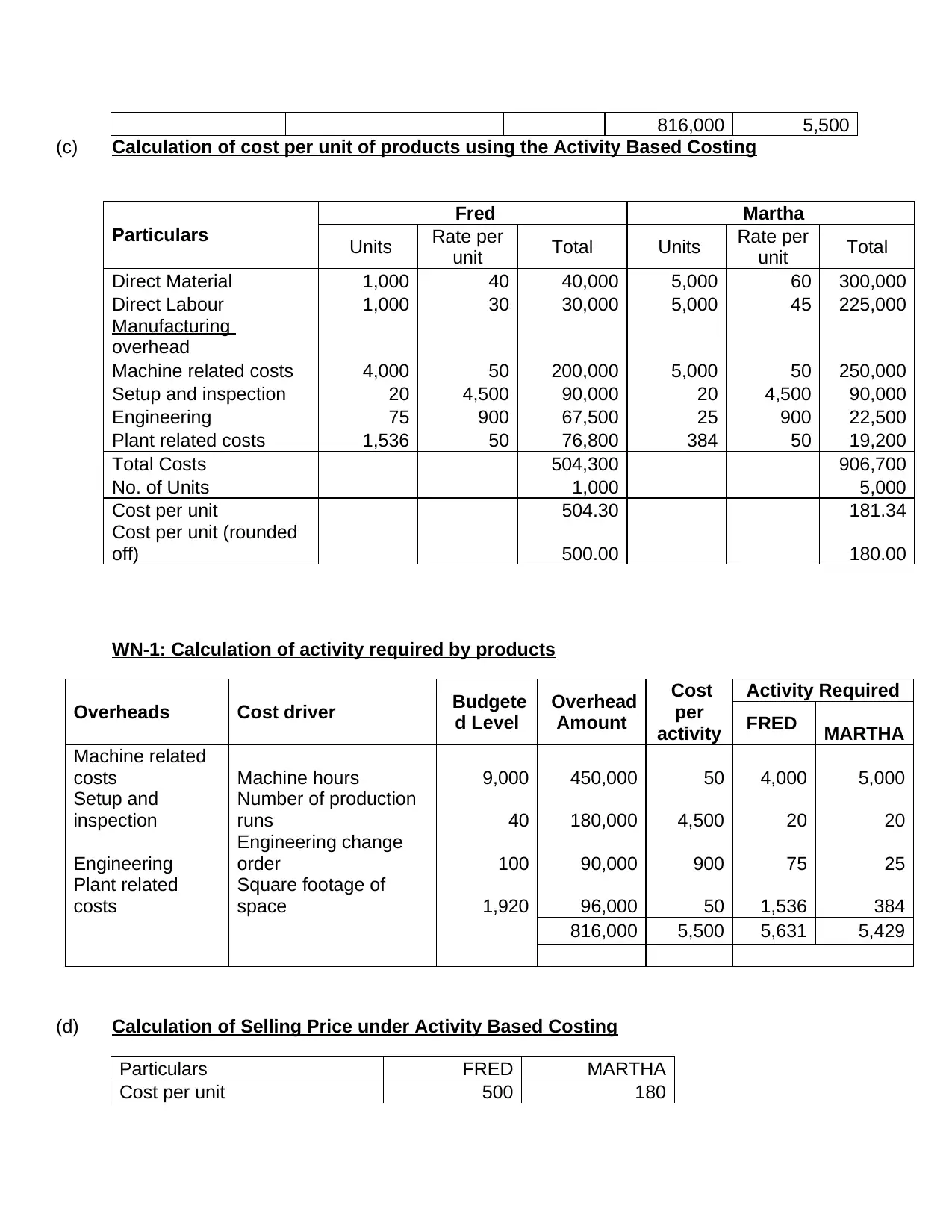

In contrast, the assignment introduces ABC, which allocates overhead based on specific activities and their respective cost drivers such as machine hours, production runs, engineering changes, and plant space utilization. This method yields different unit costs: $500 for Fred and $180 for Martha, providing a more precise reflection of resource consumption.

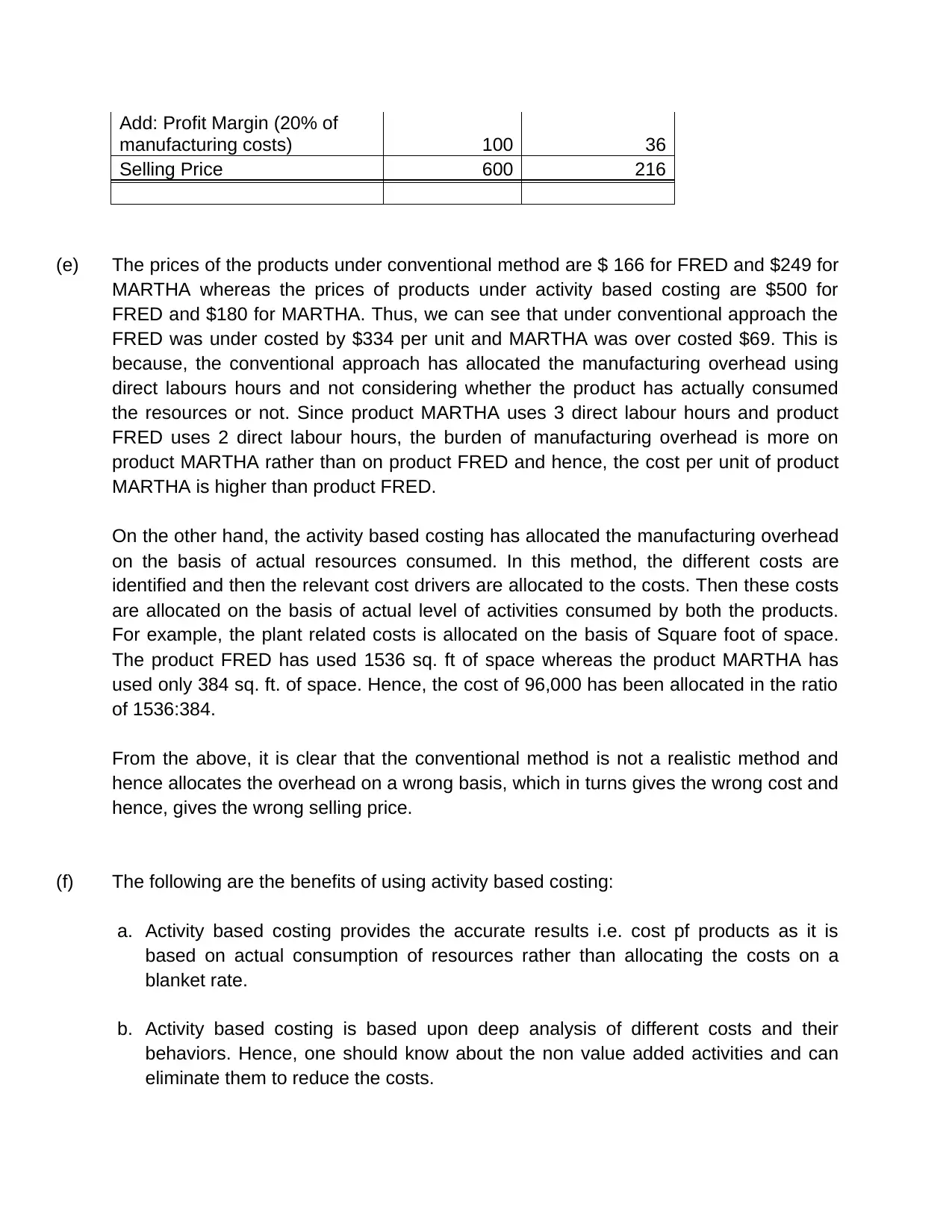

The analysis reveals that under conventional costing, Fred was significantly under-costed by $334 per unit while Martha was over-costed by $69. ABC addresses these discrepancies by aligning overhead allocation with actual activities consumed. This method enhances cost accuracy and informs better pricing strategies, though it comes with higher implementation costs and time-consuming data requirements. Ultimately, the assignment underscores the benefits of ABC in achieving competitive product pricing through more accurate cost analysis while acknowledging its limitations for smaller enterprises.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.