ACTST861 - Risk Theory: Assignment 1 - Weibull, Pareto, Lognormal

VerifiedAdded on 2023/04/07

|6

|677

|238

Homework Assignment

AI Summary

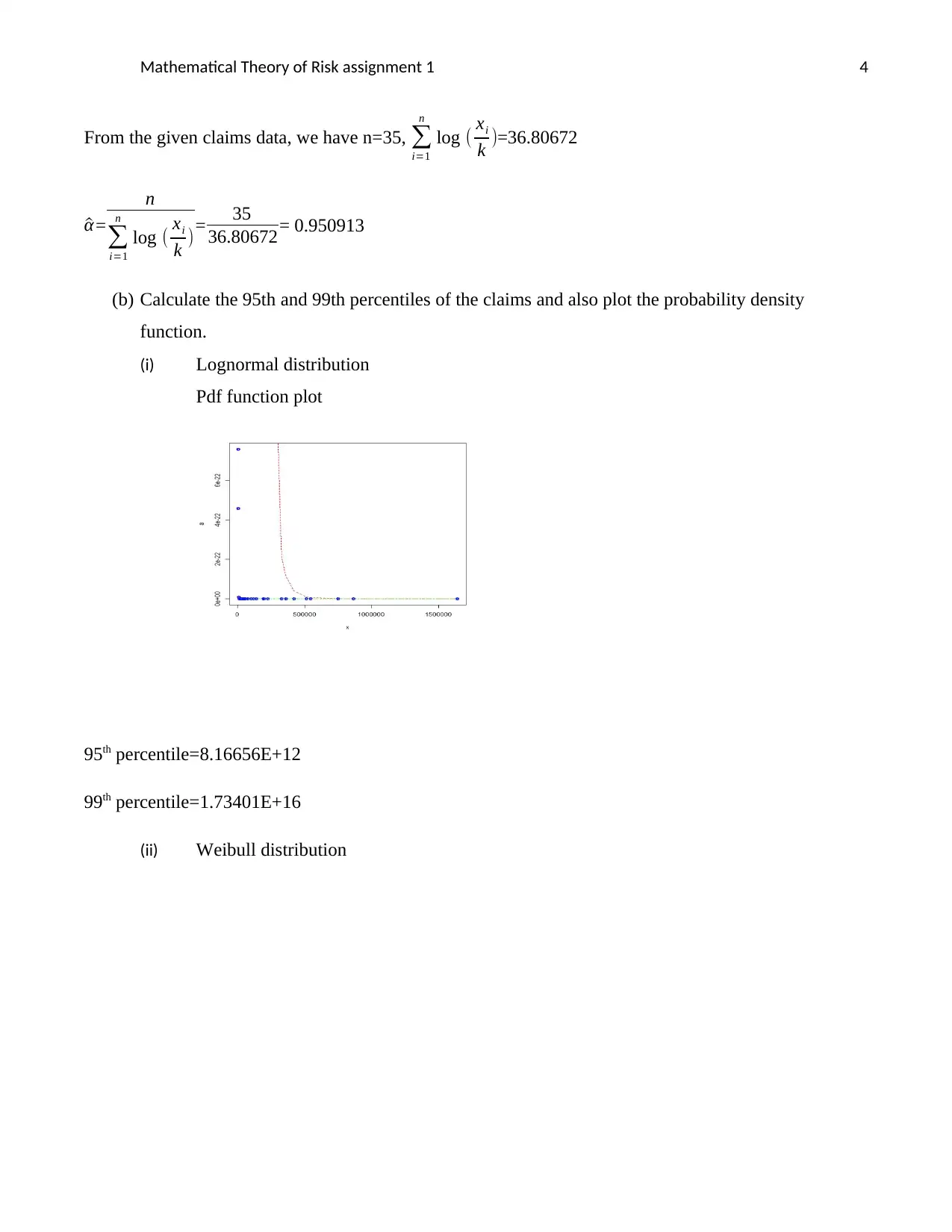

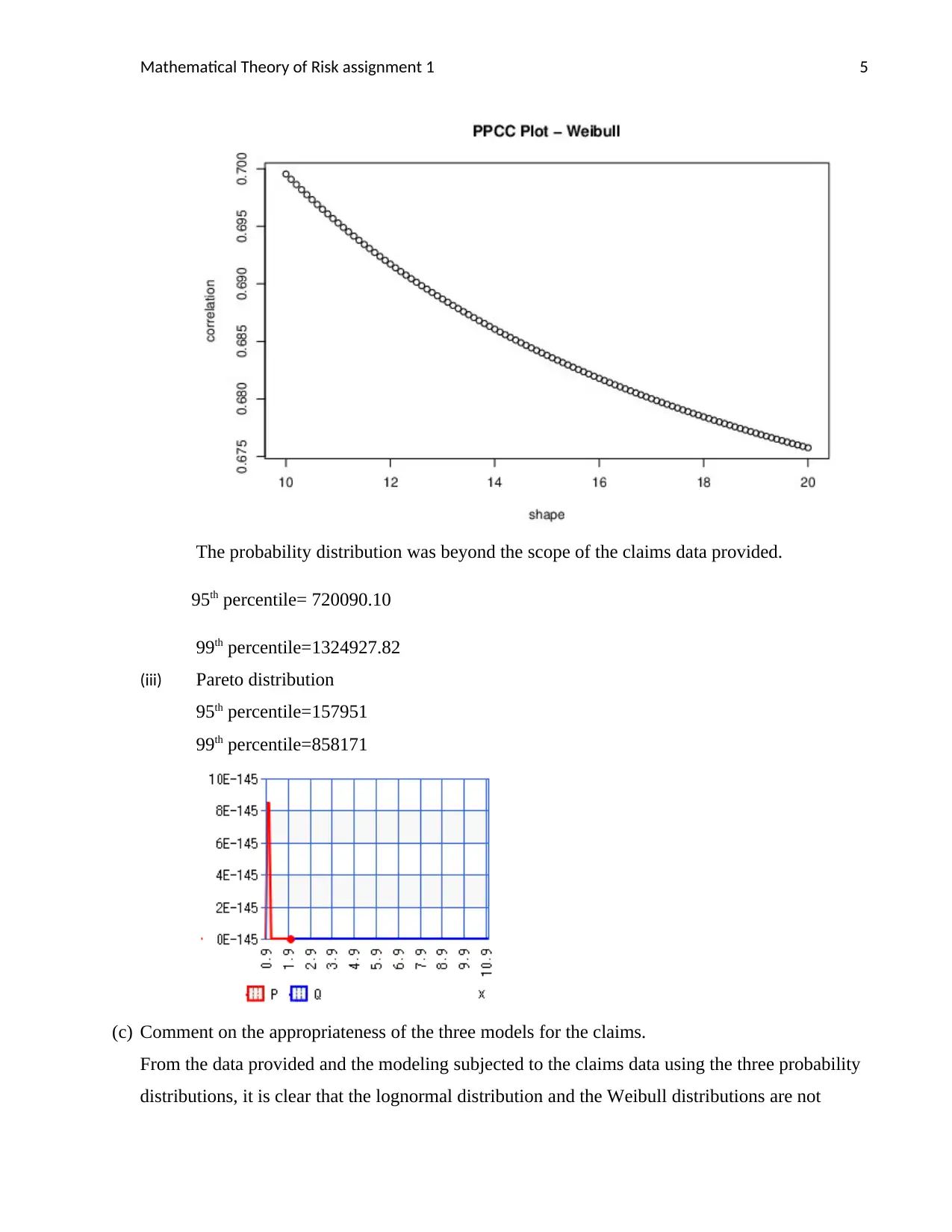

This assignment solution focuses on the mathematical theory of risk, specifically addressing parameter estimation for the Weibull, Pareto, and Lognormal distributions using the maximum likelihood method. The solution involves estimating parameters for each distribution using a given claims dataset, calculating the 95th and 99th percentiles of the claims, plotting the probability density functions, and commenting on the appropriateness of each model for the claims data. The analysis concludes that the Pareto distribution is the most appropriate model due to the outlier parameters produced by the data for lognormal and Weibull distributions, making it hard for the two probability distributions to fit the data. Desklib offers a range of study tools and resources, including solved assignments and past papers, to support students in their academic endeavors.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.