Case Study: Evaluating Adam & Co's Accounting Information System

VerifiedAdded on 2022/12/27

|12

|2892

|83

Case Study

AI Summary

This case study examines Adam & Co's accounting information system, focusing on its expenditure cycle which includes purchase, payroll, and cash disbursement systems. The analysis involves creating system flowcharts for each department, detailing the processes from purchase order generation to cash disbursement. The assignment identifies internal control weaknesses, such as manual processes and lack of segregation of duties, and assesses the associated risks, including potential inaccuracies, fraud, and misappropriation of funds. The study highlights the importance of a robust internal control system to ensure accurate financial records and prevent operational inefficiencies. The case study concludes with an overview of the identified weaknesses and their impact on the company's financial health and operational integrity, emphasizing the need for improved monitoring and verification processes.

Running head: CASE STUDY- ADAM & CO

CASE STUDY- ADAM & CO

Name of the Student

Name of the University

Author Note

CASE STUDY- ADAM & CO

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CASE STUDY- ADAM & CO

Executive Summary:

In this paper, the role of accounting information system in the context of operating

policies and structure of organization has been presented. For such analysis, the

case on Adam and Co explaining its different system of the procedure of expenditure

cycle has been evaluated. The assignment states the evaluation of the method of

risk and internal control based on strength and the weakness of the organization.

This process of analyzing the risk and internal control is explained with the help of a

case study of a renowned company named Adam and Co. There are three different

departments in Adam and Co, which have been engaged in determining the total

amount of purchase, payroll, and the amount of cash disbursed. The remaining part

of the assessment represents the flaws of internal control system arises in each

department.

Executive Summary:

In this paper, the role of accounting information system in the context of operating

policies and structure of organization has been presented. For such analysis, the

case on Adam and Co explaining its different system of the procedure of expenditure

cycle has been evaluated. The assignment states the evaluation of the method of

risk and internal control based on strength and the weakness of the organization.

This process of analyzing the risk and internal control is explained with the help of a

case study of a renowned company named Adam and Co. There are three different

departments in Adam and Co, which have been engaged in determining the total

amount of purchase, payroll, and the amount of cash disbursed. The remaining part

of the assessment represents the flaws of internal control system arises in each

department.

CASE STUDY- ADAM & CO

Table of Contents

Introduction:..................................................................................................................3

Discussion:...................................................................................................................3

System flowchart of purchase system:.........................................................................3

System flowchart of cash disbursement system:.........................................................5

System flowchart of payroll system:.............................................................................5

Identification of the internal control weakness and the risk associated with the

system:..........................................................................................................................6

Conclusion:...................................................................................................................7

Reference list:...............................................................................................................9

Table of Contents

Introduction:..................................................................................................................3

Discussion:...................................................................................................................3

System flowchart of purchase system:.........................................................................3

System flowchart of cash disbursement system:.........................................................5

System flowchart of payroll system:.............................................................................5

Identification of the internal control weakness and the risk associated with the

system:..........................................................................................................................6

Conclusion:...................................................................................................................7

Reference list:...............................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CASE STUDY- ADAM & CO

Introduction:

The aim of this assignment is to establish a concrete a framework on

evaluation of risk, process and method of internal control on expenditure cycle of the

company. Therefore, it can be said that the framework will assist the managing

directors of Adam & Co for growth and development. Adam & Co is engaged in

wholesale business and the company collects its resources from Thailand, China

and Vietnam. The process of expenditure cycle of Adam & Co consists of purchase

system, payroll and cash disbursement system. The process of expenditure cycle

can be defined with a flow chart, which provides an overview of evaluating the state

of transactions concerning present situation for further development and growth

(Farkas and Hirsch, 2015).

Discussion:

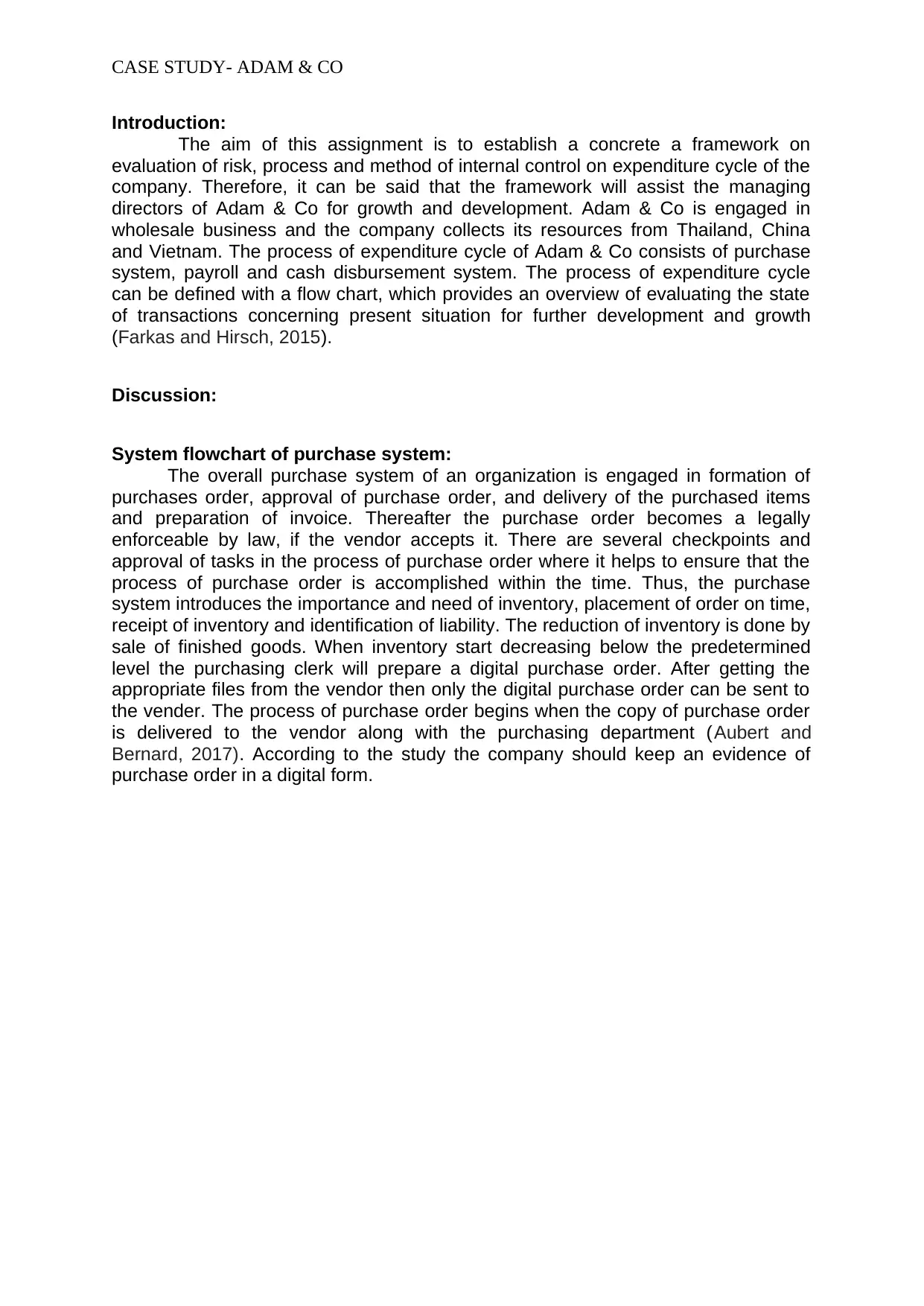

System flowchart of purchase system:

The overall purchase system of an organization is engaged in formation of

purchases order, approval of purchase order, and delivery of the purchased items

and preparation of invoice. Thereafter the purchase order becomes a legally

enforceable by law, if the vendor accepts it. There are several checkpoints and

approval of tasks in the process of purchase order where it helps to ensure that the

process of purchase order is accomplished within the time. Thus, the purchase

system introduces the importance and need of inventory, placement of order on time,

receipt of inventory and identification of liability. The reduction of inventory is done by

sale of finished goods. When inventory start decreasing below the predetermined

level the purchasing clerk will prepare a digital purchase order. After getting the

appropriate files from the vendor then only the digital purchase order can be sent to

the vender. The process of purchase order begins when the copy of purchase order

is delivered to the vendor along with the purchasing department (Aubert and

Bernard, 2017). According to the study the company should keep an evidence of

purchase order in a digital form.

Introduction:

The aim of this assignment is to establish a concrete a framework on

evaluation of risk, process and method of internal control on expenditure cycle of the

company. Therefore, it can be said that the framework will assist the managing

directors of Adam & Co for growth and development. Adam & Co is engaged in

wholesale business and the company collects its resources from Thailand, China

and Vietnam. The process of expenditure cycle of Adam & Co consists of purchase

system, payroll and cash disbursement system. The process of expenditure cycle

can be defined with a flow chart, which provides an overview of evaluating the state

of transactions concerning present situation for further development and growth

(Farkas and Hirsch, 2015).

Discussion:

System flowchart of purchase system:

The overall purchase system of an organization is engaged in formation of

purchases order, approval of purchase order, and delivery of the purchased items

and preparation of invoice. Thereafter the purchase order becomes a legally

enforceable by law, if the vendor accepts it. There are several checkpoints and

approval of tasks in the process of purchase order where it helps to ensure that the

process of purchase order is accomplished within the time. Thus, the purchase

system introduces the importance and need of inventory, placement of order on time,

receipt of inventory and identification of liability. The reduction of inventory is done by

sale of finished goods. When inventory start decreasing below the predetermined

level the purchasing clerk will prepare a digital purchase order. After getting the

appropriate files from the vendor then only the digital purchase order can be sent to

the vender. The process of purchase order begins when the copy of purchase order

is delivered to the vendor along with the purchasing department (Aubert and

Bernard, 2017). According to the study the company should keep an evidence of

purchase order in a digital form.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CASE STUDY- ADAM & CO

The company can implement the process of purchase order effectively if the

purchase department is updated through regular information of purchase order from

valid vendor file and the information of supplier of inventory. In the subsequent stage

of this process, the receiving department receives the previously ordered goods.

Therefore, to maintain transparency the officials reconciles the information recorder

in digital form and purchasing slip based on goods accepted by the clerk after

investigating the situation properly. The receiving clerk undertakes the responsibility

of preparing hard copies of manually maintained reports. The responsible clerk has

to keep two copies of the receiving report as evidence (Albring et al. 2016).

Therefore, the clerk would file the receiving report after the subsidiary ledger account

of the inventory is updated with current information and the stocks of finished goods

are set aside properly. Therefore, according to the assessment the completion of

The company can implement the process of purchase order effectively if the

purchase department is updated through regular information of purchase order from

valid vendor file and the information of supplier of inventory. In the subsequent stage

of this process, the receiving department receives the previously ordered goods.

Therefore, to maintain transparency the officials reconciles the information recorder

in digital form and purchasing slip based on goods accepted by the clerk after

investigating the situation properly. The receiving clerk undertakes the responsibility

of preparing hard copies of manually maintained reports. The responsible clerk has

to keep two copies of the receiving report as evidence (Albring et al. 2016).

Therefore, the clerk would file the receiving report after the subsidiary ledger account

of the inventory is updated with current information and the stocks of finished goods

are set aside properly. Therefore, according to the assessment the completion of

CASE STUDY- ADAM & CO

purchase process depends on delivering the copies of receipt report, invoice and

purchase order to the department of cash disbursement (Bressler and Bressler,

2017).

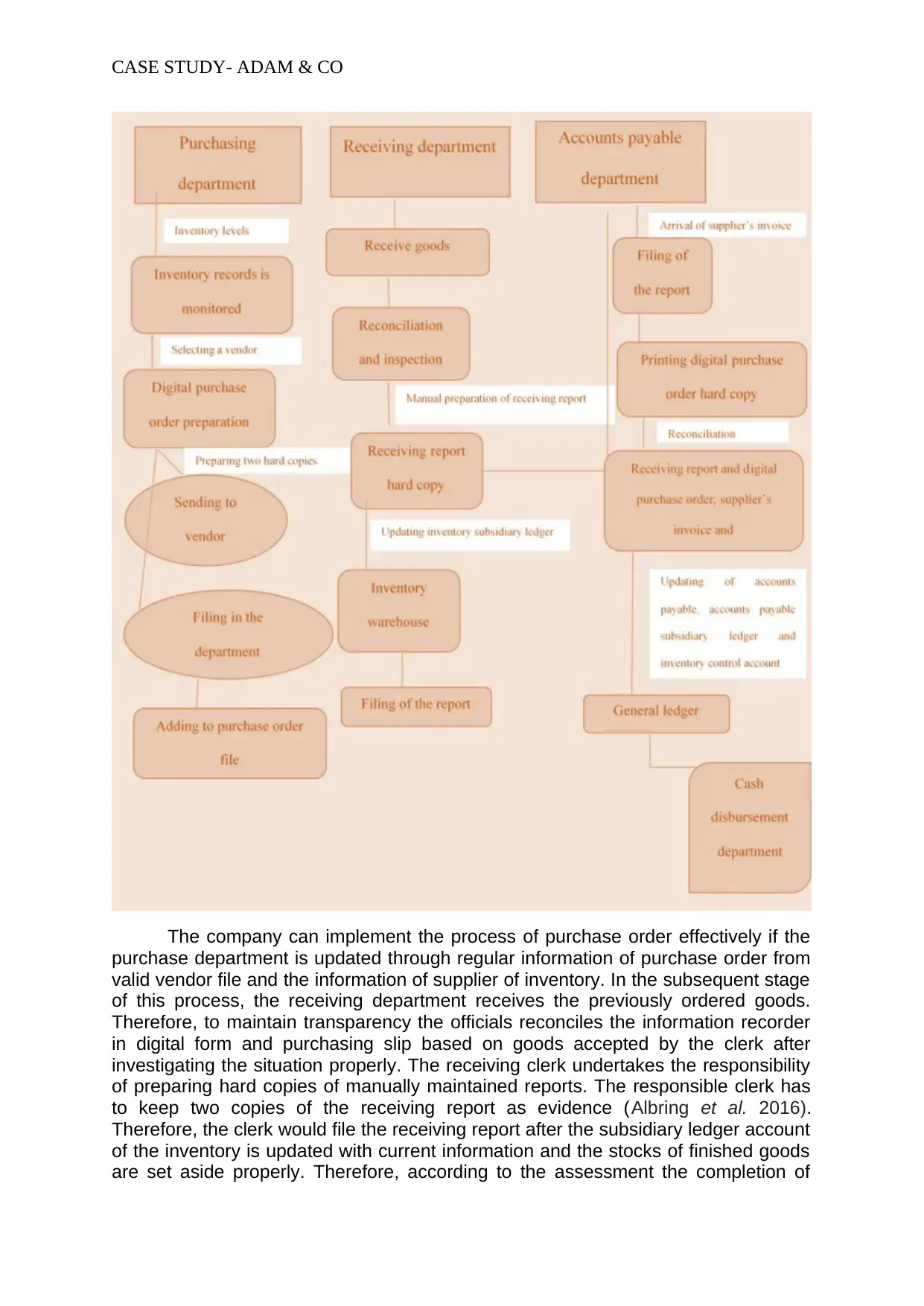

System flowchart of cash disbursement system:

The basic concept of cash disbursement system reflects the outflow of cash

due to purchase of goods or services. Usually the process of cash disbursement is

accomplished through the system of account payable .Every organization whether it

is small or large needs to imply the system of cash disbursement system effectively

to maintain a proper cash balance and to detect that the cash is paid for legitimate

reason (Wilford 2016). An effective framework of cash disbursement system requires

proper internal control system since the internal control system helps to detect the

fraud and misrepresentation of cash transaction within the company. Thus it can be

said that cash disbursement system helps to maintain the liquidity position of the

particular business since the organisation can able to meet the short term liabilities

without any disruption. According to the study the department of accounts payable

should aware of all the information and maintain all the relevant documents of

purchase order, invoice and receipt of report. These documents should be

maintained by the clerk of accounts receivable department till the due date of

payment. Then the responsible clerk would issue a cheque on the due date and the

treasurer would sign the cheque and send a copy of the cheque to vendor via mail

(Stafievskaya et al. 2015). After that, the officials of cash disbursement department

would update the balance of accounts payable subsidiary ledger, register of cheque

and accounts payable control account. Finally the overall cash disbursement

process comes to an end after filing the relevant copy of purchase order, copy of

invoice and report of receipt by the clerk.

purchase process depends on delivering the copies of receipt report, invoice and

purchase order to the department of cash disbursement (Bressler and Bressler,

2017).

System flowchart of cash disbursement system:

The basic concept of cash disbursement system reflects the outflow of cash

due to purchase of goods or services. Usually the process of cash disbursement is

accomplished through the system of account payable .Every organization whether it

is small or large needs to imply the system of cash disbursement system effectively

to maintain a proper cash balance and to detect that the cash is paid for legitimate

reason (Wilford 2016). An effective framework of cash disbursement system requires

proper internal control system since the internal control system helps to detect the

fraud and misrepresentation of cash transaction within the company. Thus it can be

said that cash disbursement system helps to maintain the liquidity position of the

particular business since the organisation can able to meet the short term liabilities

without any disruption. According to the study the department of accounts payable

should aware of all the information and maintain all the relevant documents of

purchase order, invoice and receipt of report. These documents should be

maintained by the clerk of accounts receivable department till the due date of

payment. Then the responsible clerk would issue a cheque on the due date and the

treasurer would sign the cheque and send a copy of the cheque to vendor via mail

(Stafievskaya et al. 2015). After that, the officials of cash disbursement department

would update the balance of accounts payable subsidiary ledger, register of cheque

and accounts payable control account. Finally the overall cash disbursement

process comes to an end after filing the relevant copy of purchase order, copy of

invoice and report of receipt by the clerk.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CASE STUDY- ADAM & CO

System flowchart of payroll system:

The term payroll refers to the amount of compensation to be paid to by the

company for the welfare of the employees for a specific period. Payroll is one of the

most crucial parts of a company. The concept of payroll mainly explains the process

of paying wages and salaries to the employees according to hours worked for the

day. Therefore, it can be said that the payroll process indirectly monitors the

employee performance and track their activities. The case study of Adam & Co

identifies the basic factors of payroll system. The essential factors of payroll system

include the number of hours worked by the employees and the total hours worked

registered in the time card. The workers are paid according to the data recorded in

the time card. Therefore, time card acts as an indicator of overall employee

performance. The responsible supervisor of the company verifies the data recorded

in time card thoroughly to rectify the discrepancies or loopholes in the given

information. Then the verified time card should be presented to the department of

payroll system. Thereafter, all the information of time card is to be transferred to the

processing department by the clerk. Therefore, the in charge the department should

insert two copies of the register of the payroll system along with the hard copies of

cheque to the records of employee in digital form. Further, the time card is filed by

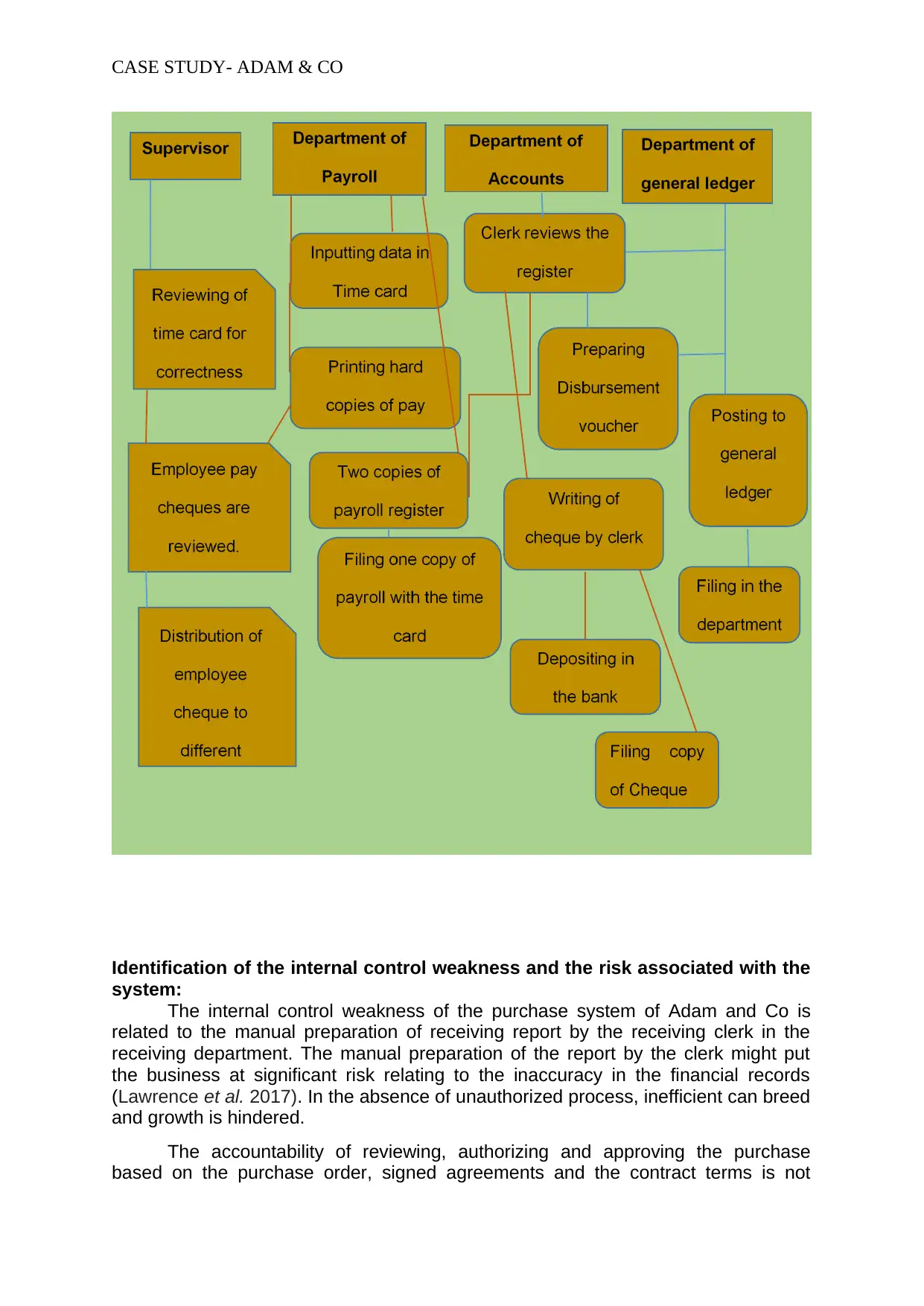

System flowchart of payroll system:

The term payroll refers to the amount of compensation to be paid to by the

company for the welfare of the employees for a specific period. Payroll is one of the

most crucial parts of a company. The concept of payroll mainly explains the process

of paying wages and salaries to the employees according to hours worked for the

day. Therefore, it can be said that the payroll process indirectly monitors the

employee performance and track their activities. The case study of Adam & Co

identifies the basic factors of payroll system. The essential factors of payroll system

include the number of hours worked by the employees and the total hours worked

registered in the time card. The workers are paid according to the data recorded in

the time card. Therefore, time card acts as an indicator of overall employee

performance. The responsible supervisor of the company verifies the data recorded

in time card thoroughly to rectify the discrepancies or loopholes in the given

information. Then the verified time card should be presented to the department of

payroll system. Thereafter, all the information of time card is to be transferred to the

processing department by the clerk. Therefore, the in charge the department should

insert two copies of the register of the payroll system along with the hard copies of

cheque to the records of employee in digital form. Further, the time card is filed by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CASE STUDY- ADAM & CO

the payroll clerk of the payroll department. There are a lot of supervisors who

accepts the employee pay cheque for further analysis and thereafter these are

distributed among the employees of different departments. One duplicate copy of the

payroll register is to be filed with the department of payroll for further evidence and

other relevant documents is to be transferred to the departments of accounts

payable. The subsequent step is inspection of the register of payroll by the

responsible assistant of the department of accounts payable. The same person of

the account payable department takes the responsibility of preparing the voucher of

disbursement (O’Grady et al. 2016). There after the responsible clerk transfers the

register of payroll and the relevant documents of voucher to the department of

general ledger. Then the clerk of account payable department prepares a cheque for

the overall payroll and deposits the same in the bank account. Finally the clerk of the

department of account payable asks for a duplicate copy of the cheque as evidence.

Therefore, in this way the payroll system comes to an end. As per the study on

Adam & Co the clerk of general ledger department delivers the register of payroll and

the vouchers to the general ledger department.

the payroll clerk of the payroll department. There are a lot of supervisors who

accepts the employee pay cheque for further analysis and thereafter these are

distributed among the employees of different departments. One duplicate copy of the

payroll register is to be filed with the department of payroll for further evidence and

other relevant documents is to be transferred to the departments of accounts

payable. The subsequent step is inspection of the register of payroll by the

responsible assistant of the department of accounts payable. The same person of

the account payable department takes the responsibility of preparing the voucher of

disbursement (O’Grady et al. 2016). There after the responsible clerk transfers the

register of payroll and the relevant documents of voucher to the department of

general ledger. Then the clerk of account payable department prepares a cheque for

the overall payroll and deposits the same in the bank account. Finally the clerk of the

department of account payable asks for a duplicate copy of the cheque as evidence.

Therefore, in this way the payroll system comes to an end. As per the study on

Adam & Co the clerk of general ledger department delivers the register of payroll and

the vouchers to the general ledger department.

CASE STUDY- ADAM & CO

Identification of the internal control weakness and the risk associated with the

system:

The internal control weakness of the purchase system of Adam and Co is

related to the manual preparation of receiving report by the receiving clerk in the

receiving department. The manual preparation of the report by the clerk might put

the business at significant risk relating to the inaccuracy in the financial records

(Lawrence et al. 2017). In the absence of unauthorized process, inefficient can breed

and growth is hindered.

The accountability of reviewing, authorizing and approving the purchase

based on the purchase order, signed agreements and the contract terms is not

Identification of the internal control weakness and the risk associated with the

system:

The internal control weakness of the purchase system of Adam and Co is

related to the manual preparation of receiving report by the receiving clerk in the

receiving department. The manual preparation of the report by the clerk might put

the business at significant risk relating to the inaccuracy in the financial records

(Lawrence et al. 2017). In the absence of unauthorized process, inefficient can breed

and growth is hindered.

The accountability of reviewing, authorizing and approving the purchase

based on the purchase order, signed agreements and the contract terms is not

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CASE STUDY- ADAM & CO

ordered. In the absence of accountability, there is the possibility of unnecessary and

fraudulent purchases and unauthorization of the work performed by the suppliers. In

addition to this, there can be the misappropriation of funds due to the improper

charges made to the incorrect fund and accounts (Mohapatra et al. 2015).

Some of the internal control weakness of the cash disbursement system of the

company and the risks associated with such weakness are listed below:

The probability of an employee being able to cover up the theft and stealing of

the assets is minimized because of segregating the duties to employees. It

can be observed from the case that the one or more tasks related to the

system of purchase is performed by one staff. This also causes the

employees to share the responsibility so that they are able to serve the check

on the work of other employees (Richardson, 2017).

Lack of reliability- In the absence of accurate monitoring, there exist the

possibility that the produced documents supporting the transactions might not

be reliable. The accounting transactions should be supported by producing

suitable documents as the documentary evidence forms an important part of

the structure of internal control system (Berthelot and Morrill, 2016).

Some of the internal control weakness of the payroll system of the company

and the risks associated with such weakness are listed below:

It can be observed from the analysis of the work of payroll department that a

single person that is the accounting clerk is responsible for inputting the data

in the time card, preparing hard copies, payroll register and positing in the

general ledger. This implies that there do not exist the assigning of one

particular job by one specific employee. The safeguarding of the assets

cannot be done in the absence of such segregation (Wilford, 2016).

In addition to above, it has been found that the disbursement voucher is

prepared manually. This might results in occurrence of error and furthermore,

the company doe snit have any verification process in place for burying the

information contained therein.

Conclusion:

The analysis of the case study depicts the evaluation of the processes, risk

and the internal control system of the procedure cycle of Adam and Co. It has been

found from the evaluation of the facts that the internal control system of the systems

suffers from some weaknesses which has caused some of the assertions related to

different accounts at risk. The evaluation of the payroll system, purchase system and

the cash disbursement system has been done for measuring the efficiency and

effectiveness. From the overall analysis of the facts presented, it is inferred that

there exist a lack of monitoring and adequate verification process for verifying and

cross checking the accounting transactions. The disadvantages in the process of

expenditure cycle of Adam and Co is that most of the transactions are recorded

manually in the different departments such as payroll and purchase systems.

Furthermore, the data pertaining to the accounts become less reliable and accurate

in the absence of appropriate segregation of duties.

ordered. In the absence of accountability, there is the possibility of unnecessary and

fraudulent purchases and unauthorization of the work performed by the suppliers. In

addition to this, there can be the misappropriation of funds due to the improper

charges made to the incorrect fund and accounts (Mohapatra et al. 2015).

Some of the internal control weakness of the cash disbursement system of the

company and the risks associated with such weakness are listed below:

The probability of an employee being able to cover up the theft and stealing of

the assets is minimized because of segregating the duties to employees. It

can be observed from the case that the one or more tasks related to the

system of purchase is performed by one staff. This also causes the

employees to share the responsibility so that they are able to serve the check

on the work of other employees (Richardson, 2017).

Lack of reliability- In the absence of accurate monitoring, there exist the

possibility that the produced documents supporting the transactions might not

be reliable. The accounting transactions should be supported by producing

suitable documents as the documentary evidence forms an important part of

the structure of internal control system (Berthelot and Morrill, 2016).

Some of the internal control weakness of the payroll system of the company

and the risks associated with such weakness are listed below:

It can be observed from the analysis of the work of payroll department that a

single person that is the accounting clerk is responsible for inputting the data

in the time card, preparing hard copies, payroll register and positing in the

general ledger. This implies that there do not exist the assigning of one

particular job by one specific employee. The safeguarding of the assets

cannot be done in the absence of such segregation (Wilford, 2016).

In addition to above, it has been found that the disbursement voucher is

prepared manually. This might results in occurrence of error and furthermore,

the company doe snit have any verification process in place for burying the

information contained therein.

Conclusion:

The analysis of the case study depicts the evaluation of the processes, risk

and the internal control system of the procedure cycle of Adam and Co. It has been

found from the evaluation of the facts that the internal control system of the systems

suffers from some weaknesses which has caused some of the assertions related to

different accounts at risk. The evaluation of the payroll system, purchase system and

the cash disbursement system has been done for measuring the efficiency and

effectiveness. From the overall analysis of the facts presented, it is inferred that

there exist a lack of monitoring and adequate verification process for verifying and

cross checking the accounting transactions. The disadvantages in the process of

expenditure cycle of Adam and Co is that most of the transactions are recorded

manually in the different departments such as payroll and purchase systems.

Furthermore, the data pertaining to the accounts become less reliable and accurate

in the absence of appropriate segregation of duties.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CASE STUDY- ADAM & CO

Reference list:

Albring, S.M., Elder, R.J. and Xu, X., 2018. Unexpected fees and the prediction of

material weaknesses in internal control over financial reporting. Journal of

Accounting, Auditing & Finance, 33(4), pp.485-505.

Aubert, B. and Bernard, J.G., 2017. Outsourcing of accounting information systems.

In The Routledge Companion to Accounting Information Systems (pp. 120-132).

Routledge.

Berthelot, S. and Morrill, J., 2016. Management Control Systems and the Presence

of a Full-Time Accountant: An Empirical Study of Small-and Medium-Sized

Enterprises (SMEs). In Advances in Management Accounting (pp. 207-242).

Emerald Group Publishing Limited.

Bressler, L.A. and Bressler, M.S., 2017. Accounting for profit: How crime activity can

cost you your business. Global Journal of Business Disciplines, 1(2), pp.21-30.

Chen, H., Hua, S. and Sun, X.C., 2018. CEO Age and the Persistence of Internal

Control Deficiencies. Journal of Accounting & Finance (2158-3625), 18(7).

Dagiliene, L. and Šutiene, K., 2019. Corporate sustainability accounting information

systems: a contingency-based approach. Sustainability Accounting, Management

and Policy Journal.

Farkas, M.J. and Hirsch, R.M., 2015. The effect of frequency and automation of

internal control testing on external auditor reliance on the internal audit

function. Journal of Information Systems, 30(1), pp.21-40.

Granlund, M. and Teittinen, H., 2017. Accounting Information Systems and decision-

making. In The Routledge Companion to Accounting Information Systems (pp. 81-

93). Routledge.

Lawrence, A., Minutti-Meza, M. and Vyas, D., 2017. Is operational control risk

informative of financial reporting deficiencies?. Auditing: A Journal of Practice &

Theory, 37(1), pp.139-165.

Machado, M.J. and Gomes, J., 2018. Accounting and the ERP Systems: A Case

Study. International Journal of Knowledge-Based Organizations (IJKBO), 8(2),

pp.32-41.

Mohapatra, P., El-Mahdy, D.F. and Xu, L., 2015. Auditing and internal controls for

offshored accounting processes: a research agenda. International Journal of

Accounting & Information Management, 23(4), pp.310-326.

O’Grady, W., Morlidge, S. and Rouse, P., 2016. Evaluating the completeness and

effectiveness of management control systems with cybernetic tools. Management

Accounting Research, 33, pp.1-15.

Otley, D., 2016. The contingency theory of management accounting and control:

1980–2014. Management accounting research, 31, pp.45-62.

Richardson, A.J., 2017. The relationship between management and financial

accounting as professions and technologies of practice. In The Role of the

Management Accountant (pp. 246-261). Routledge.

Reference list:

Albring, S.M., Elder, R.J. and Xu, X., 2018. Unexpected fees and the prediction of

material weaknesses in internal control over financial reporting. Journal of

Accounting, Auditing & Finance, 33(4), pp.485-505.

Aubert, B. and Bernard, J.G., 2017. Outsourcing of accounting information systems.

In The Routledge Companion to Accounting Information Systems (pp. 120-132).

Routledge.

Berthelot, S. and Morrill, J., 2016. Management Control Systems and the Presence

of a Full-Time Accountant: An Empirical Study of Small-and Medium-Sized

Enterprises (SMEs). In Advances in Management Accounting (pp. 207-242).

Emerald Group Publishing Limited.

Bressler, L.A. and Bressler, M.S., 2017. Accounting for profit: How crime activity can

cost you your business. Global Journal of Business Disciplines, 1(2), pp.21-30.

Chen, H., Hua, S. and Sun, X.C., 2018. CEO Age and the Persistence of Internal

Control Deficiencies. Journal of Accounting & Finance (2158-3625), 18(7).

Dagiliene, L. and Šutiene, K., 2019. Corporate sustainability accounting information

systems: a contingency-based approach. Sustainability Accounting, Management

and Policy Journal.

Farkas, M.J. and Hirsch, R.M., 2015. The effect of frequency and automation of

internal control testing on external auditor reliance on the internal audit

function. Journal of Information Systems, 30(1), pp.21-40.

Granlund, M. and Teittinen, H., 2017. Accounting Information Systems and decision-

making. In The Routledge Companion to Accounting Information Systems (pp. 81-

93). Routledge.

Lawrence, A., Minutti-Meza, M. and Vyas, D., 2017. Is operational control risk

informative of financial reporting deficiencies?. Auditing: A Journal of Practice &

Theory, 37(1), pp.139-165.

Machado, M.J. and Gomes, J., 2018. Accounting and the ERP Systems: A Case

Study. International Journal of Knowledge-Based Organizations (IJKBO), 8(2),

pp.32-41.

Mohapatra, P., El-Mahdy, D.F. and Xu, L., 2015. Auditing and internal controls for

offshored accounting processes: a research agenda. International Journal of

Accounting & Information Management, 23(4), pp.310-326.

O’Grady, W., Morlidge, S. and Rouse, P., 2016. Evaluating the completeness and

effectiveness of management control systems with cybernetic tools. Management

Accounting Research, 33, pp.1-15.

Otley, D., 2016. The contingency theory of management accounting and control:

1980–2014. Management accounting research, 31, pp.45-62.

Richardson, A.J., 2017. The relationship between management and financial

accounting as professions and technologies of practice. In The Role of the

Management Accountant (pp. 246-261). Routledge.

CASE STUDY- ADAM & CO

Shen, J. and Han, L., 2019. Design process optimization and profit calculation

module development simulation analysis of financial accounting information system

based on particle swarm optimization (PSO). Information Systems and e-Business

Management, pp.1-14.

Stafievskaya, M.V., Nikolayeva, L.V., Kreneva, S.G., Shakirova, R.K., Semenova,

O.A., Larionova, T.P. and Filyushin, N.V., 2015. Accounting risks in the subjects of

business systems. Review of European studies, 7(8), p.127.

Susanto, A., 2018. The influence of business process and risk management on the

quality of accounting information system. Journal of Theoretical & Applied

Information Technology, 96(9).

Wilford, A.L., 2016. Internal control reporting and accounting standards: A cross-

country comparison. Journal of Accounting and Public Policy, 35(3), pp.276-302.

Shen, J. and Han, L., 2019. Design process optimization and profit calculation

module development simulation analysis of financial accounting information system

based on particle swarm optimization (PSO). Information Systems and e-Business

Management, pp.1-14.

Stafievskaya, M.V., Nikolayeva, L.V., Kreneva, S.G., Shakirova, R.K., Semenova,

O.A., Larionova, T.P. and Filyushin, N.V., 2015. Accounting risks in the subjects of

business systems. Review of European studies, 7(8), p.127.

Susanto, A., 2018. The influence of business process and risk management on the

quality of accounting information system. Journal of Theoretical & Applied

Information Technology, 96(9).

Wilford, A.L., 2016. Internal control reporting and accounting standards: A cross-

country comparison. Journal of Accounting and Public Policy, 35(3), pp.276-302.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.