Holmes Institute HA2042: Case Study Analysis of Adam & Co's AIS

VerifiedAdded on 2022/10/31

|12

|3075

|211

Case Study

AI Summary

This case study analyzes the accounting information system of Adam & Co, focusing on its centralized system across multiple terminals. The report details the company's expenditure cycle, including purchases from manufacturers in China, Vietnam, and Thailand. It examines the system flowcharts and descriptions of the purchases, cash disbursements, and payroll systems. The analysis covers internal controls and associated risks within these systems, providing an evaluation for the Managing Director. The case study emphasizes the importance of documentation, support, and training in implementing and maintaining an effective accounting information system. It also highlights the objectives of the system, such as protecting the firm from risks and meeting statutory requirements. The study uses flowcharts to illustrate the processes within each system, including inventory checks, order placements, cheque preparation, and payroll processing. The analysis concludes with an overview of internal controls and associated risks, with the goal of improving efficiency and minimizing errors. The case study adheres to the guidelines provided by Holmes Institute for the HA2042 Accounting Information Systems unit.

Running head: CASE STUDY- ADAM & CO

Case Study – Adam & Co

Name of the Student:

Name of the University:

Author Note

Case Study – Adam & Co

Name of the Student:

Name of the University:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CASE STUDY – ADAM & CO

Executive Summary

The business analyst of Adam & Co has prepared the report to analyze the

performance of the company. The characteristics and objectives of the system have

been highlighted. The system flowchart of purchasing system, cash disbursement

system and payroll system has been described.

Executive Summary

The business analyst of Adam & Co has prepared the report to analyze the

performance of the company. The characteristics and objectives of the system have

been highlighted. The system flowchart of purchasing system, cash disbursement

system and payroll system has been described.

2CASE STUDY – ADAM & CO

Table of Contents

Introduction...................................................................................................................3

System flowchart and description of purchases system..............................................5

System flowchart and description of cash disbursements system...............................6

System flowchart and description of payroll system....................................................7

Internal control and associated risk..............................................................................9

Conclusion....................................................................................................................9

Reference list..............................................................................................................10

Table of Contents

Introduction...................................................................................................................3

System flowchart and description of purchases system..............................................5

System flowchart and description of cash disbursements system...............................6

System flowchart and description of payroll system....................................................7

Internal control and associated risk..............................................................................9

Conclusion....................................................................................................................9

Reference list..............................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CASE STUDY – ADAM & CO

Introduction

Accounting Information System is a mechanism of collection, storage and

processing of accounting and financial data which are used for the purpose of

decision making by the makers of decision. It is a method based on computer for

tracking its accounting activities in relation to the resources of information

technology. The financial reports prepared are used by the internal management as

well as by external interested parties like investors, tax authorities and creditors

(Ceran, Gungor and Konya 2016). It is designed in a manner that supports all the

accounting activities and functions relating to financial reporting and accounting,

managerial accounting and tax and auditing. The commonly used modules of

accounting systems are financial reporting and auditing by most companies. One

such company is Adam & Co that follows a centralized accounting system for its

network of terminals across different locations. As its business analyst the

performance of the company has been analysed (Collier 2015). The company has its

source of inventories from China, Vietnam and Thailand manufacturers. The

expenditure cycle procedures has been described. The management of the

purchases system by the purchasing system has been elaborated. The cash

disbursement system is managed by the clerk and updates are made in the books.

The process of pay roll system followed by the company is explained. The evaluation

of the process, risk and internal control of its expenditure cycle for the Managing

Director has been prepared.

The implementation of the system have certain steps that are required to be

fulfilled. Several firms have started adopting effective cost accounting information

system based on cloud (Galliers and Leidner 2014). Most firms used to hire external

consultants from the software consultants or publishers who would have a good

understanding of the business. They help in the work by selecting and implementing

the desired configuration by incorporating all the parts into its consideration.

Synthesis of systems design

An analysis is conducted based on which there is creation of new systems.

The surrounding systems play an important role in it. The data that needs to be

fetched into the system and the process of handling it is described ( Gullberg 2016).

The information that needs to be fetched out of the system and the way it is to be

modified is illustrated. The input and output data should be determined for the

processing by the system. The selection of the program has to be appropriately

handled to conduct its process. The mechanism is structured with sample master

records and control files. It is designed in a manner which facilitates internal control

and provides the management with relevant information for decision making. The

characteristics of the system are meaningful, useful, relevant, current and reliable

(Guragai et al. 2015). For achieving it, the system is built in a manner where the

transactions are recorded on their occurrence and immediately made available for

the management.

Documentation

The documentation is prepared while it is designed. It is inclusive of

documents by the vendor and detailed instructions for the users that helps them to

handle every process which is organization specific. Most procedures and

documentation are online and they are helpful upon receiving instructions from the

Introduction

Accounting Information System is a mechanism of collection, storage and

processing of accounting and financial data which are used for the purpose of

decision making by the makers of decision. It is a method based on computer for

tracking its accounting activities in relation to the resources of information

technology. The financial reports prepared are used by the internal management as

well as by external interested parties like investors, tax authorities and creditors

(Ceran, Gungor and Konya 2016). It is designed in a manner that supports all the

accounting activities and functions relating to financial reporting and accounting,

managerial accounting and tax and auditing. The commonly used modules of

accounting systems are financial reporting and auditing by most companies. One

such company is Adam & Co that follows a centralized accounting system for its

network of terminals across different locations. As its business analyst the

performance of the company has been analysed (Collier 2015). The company has its

source of inventories from China, Vietnam and Thailand manufacturers. The

expenditure cycle procedures has been described. The management of the

purchases system by the purchasing system has been elaborated. The cash

disbursement system is managed by the clerk and updates are made in the books.

The process of pay roll system followed by the company is explained. The evaluation

of the process, risk and internal control of its expenditure cycle for the Managing

Director has been prepared.

The implementation of the system have certain steps that are required to be

fulfilled. Several firms have started adopting effective cost accounting information

system based on cloud (Galliers and Leidner 2014). Most firms used to hire external

consultants from the software consultants or publishers who would have a good

understanding of the business. They help in the work by selecting and implementing

the desired configuration by incorporating all the parts into its consideration.

Synthesis of systems design

An analysis is conducted based on which there is creation of new systems.

The surrounding systems play an important role in it. The data that needs to be

fetched into the system and the process of handling it is described ( Gullberg 2016).

The information that needs to be fetched out of the system and the way it is to be

modified is illustrated. The input and output data should be determined for the

processing by the system. The selection of the program has to be appropriately

handled to conduct its process. The mechanism is structured with sample master

records and control files. It is designed in a manner which facilitates internal control

and provides the management with relevant information for decision making. The

characteristics of the system are meaningful, useful, relevant, current and reliable

(Guragai et al. 2015). For achieving it, the system is built in a manner where the

transactions are recorded on their occurrence and immediately made available for

the management.

Documentation

The documentation is prepared while it is designed. It is inclusive of

documents by the vendor and detailed instructions for the users that helps them to

handle every process which is organization specific. Most procedures and

documentation are online and they are helpful upon receiving instructions from the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CASE STUDY – ADAM & CO

vendor of software (Krahel and Vasarhelyi 2014). Procedures and documentation

are the afterthought while the insurance tool and policy are used during the process

of training and testing before its launch. The testing of the documentation is done

during the training phase for the launch of system without any queries by its users.

Support

The managers and end users have continuous availability of support all the

time. The system upgrades adhere to a similar kind of process and all its users are

apprised of its changes, upgraded in a manner that is efficient. Certain firms limit the

money and time they spend on its design, training, analysis and documentation

(Medina-Quintero, Mora and Abrego 2015). They further move directly into the

selection of software and implementation. In case of receiving a detailed analysis

with the use of sufficient time on its analysis, implementation and support.

Tools

Accounting information system is assisted with available online resources for

its strategic planning. Financial forms and information systems help in concluding the

particular needs of every organization along with responsibilities being assigned to

the principles that have been involved (Yigitbasioglu 2016).

Training

The users are trained with the procedures before the launch. A trainer has

been appointed who assists the users about the handling of procedures. The

procedures have to be updated during the process of training as the users keep

describing their specific circumstances (Nan and Wen 2014). The design is also

modified by incorporating the additional information. The procedure is performed with

the trainer as well as the documentation.

Characteristics-

It satisfies the needs of information for both its internal as well as external

users of information. The internal users include the managers at different

levels for the purpose of control and planning. The standard definitions of

accounting terms are followed to assure consistency in the information

recorded. The external users include vendors, stock exchanges, customers,

investors and many more.

The mechanism deals with financial transactions that can be shown having

monetary value.

It is a well-structured and simple system involving procedures and principles

for accounting its data. The objective is to protect the interests of vendors,

customers, general public and investors.

The data for the mechanism is obtained from internal sources. Therefore, the

databases are integrated, controlled and well-defined.

It makes use of historical data and includes future data as forecasts and

budgets.

Objectives-

Protecting the firm from the potential risks that could arise in future from

improper use of accounting data

vendor of software (Krahel and Vasarhelyi 2014). Procedures and documentation

are the afterthought while the insurance tool and policy are used during the process

of training and testing before its launch. The testing of the documentation is done

during the training phase for the launch of system without any queries by its users.

Support

The managers and end users have continuous availability of support all the

time. The system upgrades adhere to a similar kind of process and all its users are

apprised of its changes, upgraded in a manner that is efficient. Certain firms limit the

money and time they spend on its design, training, analysis and documentation

(Medina-Quintero, Mora and Abrego 2015). They further move directly into the

selection of software and implementation. In case of receiving a detailed analysis

with the use of sufficient time on its analysis, implementation and support.

Tools

Accounting information system is assisted with available online resources for

its strategic planning. Financial forms and information systems help in concluding the

particular needs of every organization along with responsibilities being assigned to

the principles that have been involved (Yigitbasioglu 2016).

Training

The users are trained with the procedures before the launch. A trainer has

been appointed who assists the users about the handling of procedures. The

procedures have to be updated during the process of training as the users keep

describing their specific circumstances (Nan and Wen 2014). The design is also

modified by incorporating the additional information. The procedure is performed with

the trainer as well as the documentation.

Characteristics-

It satisfies the needs of information for both its internal as well as external

users of information. The internal users include the managers at different

levels for the purpose of control and planning. The standard definitions of

accounting terms are followed to assure consistency in the information

recorded. The external users include vendors, stock exchanges, customers,

investors and many more.

The mechanism deals with financial transactions that can be shown having

monetary value.

It is a well-structured and simple system involving procedures and principles

for accounting its data. The objective is to protect the interests of vendors,

customers, general public and investors.

The data for the mechanism is obtained from internal sources. Therefore, the

databases are integrated, controlled and well-defined.

It makes use of historical data and includes future data as forecasts and

budgets.

Objectives-

Protecting the firm from the potential risks that could arise in future from

improper use of accounting data

5CASE STUDY – ADAM & CO

Meeting the statutory requirements of the organization

Providing reliable information on accounting to its various users

System flowchart and description of purchases system

Purchases system is a mechanism for the process of purchasing products

upon identification of low levels. It involves purchasing upon requisition and through

purchase order using product payment and receipt. The key components of these

systems are the inventory management in which they review the existing stock and

helps the company in determining the further purchases to be done. It also helps to

ascertain the quantity and time frame of purchasing it. The blue prints are created by

the clerk and forwarded to the respective departments (Nurhayati and Mulyani 2015).

The receipt of goods are verified with the digital purchase order along with the

packing slip by the receiving clerk. The blue prints are prepared manually on the

reports received (Prasad and Green 2015). The goods are shelved and the ledgers

are updated using the computer terminal. After receiving the invoice, the receiving

report is pulled from its temporary file and the documents are reconciled. The

ledgers, accounts are updated digitally by the clerk. The relevant documents are

forwarded to the department of cash disbursement.

Meeting the statutory requirements of the organization

Providing reliable information on accounting to its various users

System flowchart and description of purchases system

Purchases system is a mechanism for the process of purchasing products

upon identification of low levels. It involves purchasing upon requisition and through

purchase order using product payment and receipt. The key components of these

systems are the inventory management in which they review the existing stock and

helps the company in determining the further purchases to be done. It also helps to

ascertain the quantity and time frame of purchasing it. The blue prints are created by

the clerk and forwarded to the respective departments (Nurhayati and Mulyani 2015).

The receipt of goods are verified with the digital purchase order along with the

packing slip by the receiving clerk. The blue prints are prepared manually on the

reports received (Prasad and Green 2015). The goods are shelved and the ledgers

are updated using the computer terminal. After receiving the invoice, the receiving

report is pulled from its temporary file and the documents are reconciled. The

ledgers, accounts are updated digitally by the clerk. The relevant documents are

forwarded to the department of cash disbursement.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CASE STUDY – ADAM & CO

Inventory check

Placing of order

upon detecting low

levels of quantity

Printing of hard

copies and

recording in the

purchase order file

Receiving and

inspection of

goods by the clerk

Reconciliation of

documents

Receipt of documents

by cash disbursement

department

System flowchart and description of cash disbursements system

It is a mechanism of cash outflow for payments done in return for the goods

provided. It is also a disbursement of cash on refund made to customers that has

been recorded as a decrease in sales. The cash disbursement clerk does the filing of

documents after receiving the documents from the department of accounts payable.

(Silviu-Virgil 2014). The cheque is prepared by the clerk for the department of

accounts payable and forwarded to the treasurer for signing. The cheque is mailed to

the vendor (Usenko et al. 2018). The updates in the cheque register, subsidiary

ledgers and accounts payable are made by the clerk from the computer terminal.

The function of cash disbursement is effective when it includes proper

documentation and is recorded in the financial records of the company (Syaifullah

2014).

Inventory check

Placing of order

upon detecting low

levels of quantity

Printing of hard

copies and

recording in the

purchase order file

Receiving and

inspection of

goods by the clerk

Reconciliation of

documents

Receipt of documents

by cash disbursement

department

System flowchart and description of cash disbursements system

It is a mechanism of cash outflow for payments done in return for the goods

provided. It is also a disbursement of cash on refund made to customers that has

been recorded as a decrease in sales. The cash disbursement clerk does the filing of

documents after receiving the documents from the department of accounts payable.

(Silviu-Virgil 2014). The cheque is prepared by the clerk for the department of

accounts payable and forwarded to the treasurer for signing. The cheque is mailed to

the vendor (Usenko et al. 2018). The updates in the cheque register, subsidiary

ledgers and accounts payable are made by the clerk from the computer terminal.

The function of cash disbursement is effective when it includes proper

documentation and is recorded in the financial records of the company (Syaifullah

2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CASE STUDY – ADAM & CO

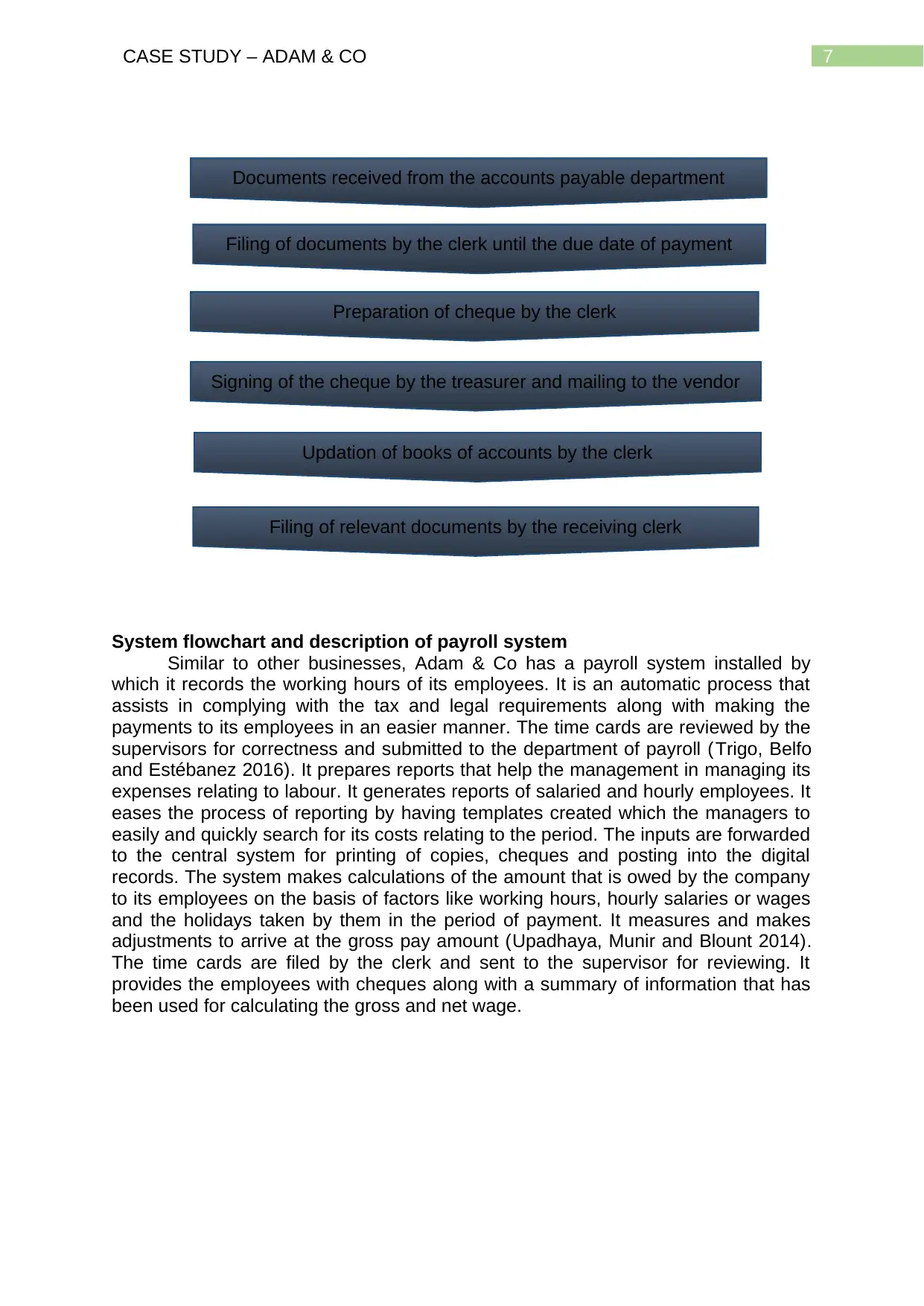

Documents received from the accounts payable department

Signing of the cheque by the treasurer and mailing to the vendor

Preparation of cheque by the clerk

Filing of relevant documents by the receiving clerk

Updation of books of accounts by the clerk

Filing of documents by the clerk until the due date of payment

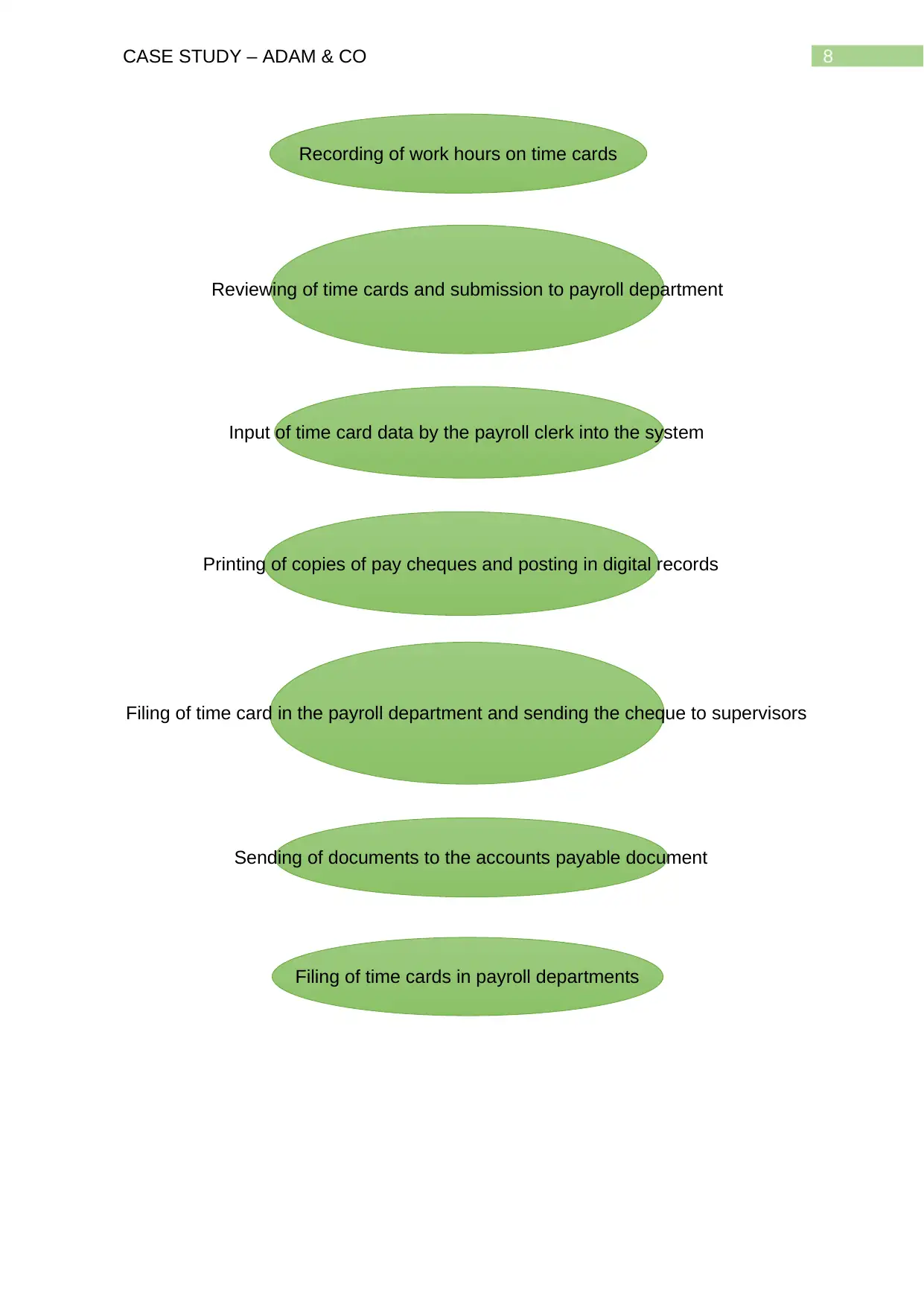

System flowchart and description of payroll system

Similar to other businesses, Adam & Co has a payroll system installed by

which it records the working hours of its employees. It is an automatic process that

assists in complying with the tax and legal requirements along with making the

payments to its employees in an easier manner. The time cards are reviewed by the

supervisors for correctness and submitted to the department of payroll (Trigo, Belfo

and Estébanez 2016). It prepares reports that help the management in managing its

expenses relating to labour. It generates reports of salaried and hourly employees. It

eases the process of reporting by having templates created which the managers to

easily and quickly search for its costs relating to the period. The inputs are forwarded

to the central system for printing of copies, cheques and posting into the digital

records. The system makes calculations of the amount that is owed by the company

to its employees on the basis of factors like working hours, hourly salaries or wages

and the holidays taken by them in the period of payment. It measures and makes

adjustments to arrive at the gross pay amount (Upadhaya, Munir and Blount 2014).

The time cards are filed by the clerk and sent to the supervisor for reviewing. It

provides the employees with cheques along with a summary of information that has

been used for calculating the gross and net wage.

Documents received from the accounts payable department

Signing of the cheque by the treasurer and mailing to the vendor

Preparation of cheque by the clerk

Filing of relevant documents by the receiving clerk

Updation of books of accounts by the clerk

Filing of documents by the clerk until the due date of payment

System flowchart and description of payroll system

Similar to other businesses, Adam & Co has a payroll system installed by

which it records the working hours of its employees. It is an automatic process that

assists in complying with the tax and legal requirements along with making the

payments to its employees in an easier manner. The time cards are reviewed by the

supervisors for correctness and submitted to the department of payroll (Trigo, Belfo

and Estébanez 2016). It prepares reports that help the management in managing its

expenses relating to labour. It generates reports of salaried and hourly employees. It

eases the process of reporting by having templates created which the managers to

easily and quickly search for its costs relating to the period. The inputs are forwarded

to the central system for printing of copies, cheques and posting into the digital

records. The system makes calculations of the amount that is owed by the company

to its employees on the basis of factors like working hours, hourly salaries or wages

and the holidays taken by them in the period of payment. It measures and makes

adjustments to arrive at the gross pay amount (Upadhaya, Munir and Blount 2014).

The time cards are filed by the clerk and sent to the supervisor for reviewing. It

provides the employees with cheques along with a summary of information that has

been used for calculating the gross and net wage.

8CASE STUDY – ADAM & CO

Recording of work hours on time cards

Printing of copies of pay cheques and posting in digital records

Input of time card data by the payroll clerk into the system

Reviewing of time cards and submission to payroll department

Filing of time cards in payroll departments

Sending of documents to the accounts payable document

Filing of time card in the payroll department and sending the cheque to supervisors

Recording of work hours on time cards

Printing of copies of pay cheques and posting in digital records

Input of time card data by the payroll clerk into the system

Reviewing of time cards and submission to payroll department

Filing of time cards in payroll departments

Sending of documents to the accounts payable document

Filing of time card in the payroll department and sending the cheque to supervisors

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CASE STUDY – ADAM & CO

Internal control and associated risk

The cash disbursement system helps the company to reduce its supply cost,

administrative cost and increase its efficiency. Therefore, decrease human error as

well as minimize the shortages. The purchases system helps to simplify the tracking

of orders and make the process of managing the purchase budgets easier by quick

preparation of expenditure reports. It helps the company in controlling the cash

outflows. It also ensures the necessary purchases that are to be done at affordable

prices. The outputs constitute the amount of inputs that are required for the process

of production. Disbursement of cash is generally detected in the accounts payable

system. However, it has also been found to be disbursed by use of petty cash and

payroll systems. A system of disbursement is required by all firms for efficient and

secure handling of cash payments. Cash payments are processed through the

accounts payable of a company. The internal control plays an important role in this

process and helps to ensure legitimate cash payment transactions. The function of

accounts payable has the responsibility of approving the payments of vendors and

transactions of creditors only if the supporting documents exist. As the transactions

are recorded upon having supporting paperwork the chances of invalid transactions

get reduced. Generally firms incorporate the system software for the payroll process.

It processes information and calculates the amount to be paid. It also helps in

checking facts like vacation balances, headcounts and earnings of employees.

Conclusion

The report helps to conclude the analysis that has been done by the business

analyst of Adam & Co. The accounting information system has been described with

its main functions been highlighted. The synthesis of system design, support,

documentation, tools along with training are its main components that help to make

the mechanism successful in an organization. The system of purchase system has

been described and the process by which it helps to determine the inventory

management for the firm. The disbursement system of cash also been discussed.

The payroll system adopted by the firm has been explained. The reports generated

by the payroll system helps the management in taking appropriate decisions.

Internal control and associated risk

The cash disbursement system helps the company to reduce its supply cost,

administrative cost and increase its efficiency. Therefore, decrease human error as

well as minimize the shortages. The purchases system helps to simplify the tracking

of orders and make the process of managing the purchase budgets easier by quick

preparation of expenditure reports. It helps the company in controlling the cash

outflows. It also ensures the necessary purchases that are to be done at affordable

prices. The outputs constitute the amount of inputs that are required for the process

of production. Disbursement of cash is generally detected in the accounts payable

system. However, it has also been found to be disbursed by use of petty cash and

payroll systems. A system of disbursement is required by all firms for efficient and

secure handling of cash payments. Cash payments are processed through the

accounts payable of a company. The internal control plays an important role in this

process and helps to ensure legitimate cash payment transactions. The function of

accounts payable has the responsibility of approving the payments of vendors and

transactions of creditors only if the supporting documents exist. As the transactions

are recorded upon having supporting paperwork the chances of invalid transactions

get reduced. Generally firms incorporate the system software for the payroll process.

It processes information and calculates the amount to be paid. It also helps in

checking facts like vacation balances, headcounts and earnings of employees.

Conclusion

The report helps to conclude the analysis that has been done by the business

analyst of Adam & Co. The accounting information system has been described with

its main functions been highlighted. The synthesis of system design, support,

documentation, tools along with training are its main components that help to make

the mechanism successful in an organization. The system of purchase system has

been described and the process by which it helps to determine the inventory

management for the firm. The disbursement system of cash also been discussed.

The payroll system adopted by the firm has been explained. The reports generated

by the payroll system helps the management in taking appropriate decisions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CASE STUDY – ADAM & CO

Reference list

Ceran, M.B., Gungor, S. and Konya, S., 2016. The role of accounting information

systems in preventing the financial crises experienced in businesses. Economics,

Management, and Financial Markets, 11(1), pp.294-303.

Collier, P.M., 2015. Accounting for managers: Interpreting accounting information for

decision making. John Wiley & Sons.

Galliers, R.D. and Leidner, D.E., 2014. Strategic information management:

challenges and strategies in managing information systems. Routledge.

Gullberg, C., 2016. What makes accounting information timely?. Qualitative

Research in Accounting & Management, 13(2), pp.189-215.

Guragai, B., Hunt, N.C., Neri, M.P. and Taylor, E.Z., 2015. Accounting information

systems and ethics research: Review, synthesis, and the future. Journal of

Information Systems, 31(2), pp.65-81.

Krahel, J.P. and Vasarhelyi, M.A., 2014. AIS as a facilitator of accounting change:

Technology, practice, and education. Journal of Information Systems, 28(2), pp.1-15.

Medina-Quintero, J.M., Mora, A. and Abrego, D., 2015. Enterprise technology in

support for accounting information systems. An innovation and productivity

approach. JISTEM-Journal of Information Systems and Technology

Management, 12(1), pp.26-44.

Nan, L. and Wen, X., 2014. Financing and investment efficiency, information quality,

and accounting biases. Management Science, 60(9), pp.2308-2323.

Nurhayati, N. and Mulyani, S., 2015. User participation on system development, user

competence and top management commitment and their effect on the success of the

implementation of accounting information systems. European Journal of Business

and Innovation Research, 3(2), pp.22-35.

Prasad, A. and Green, P., 2015. Organizational competencies and dynamic

accounting information system capability: impact on AIS processes and firm

performance. Journal of Information Systems, 29(3), pp.123-149.

Silviu-Virgil, C., 2014. The importance of the accounting information for the

decisional process. THE ANNALS OF THE UNIVERSITY OF ORADEA, p.591.

Syaifullah, M., 2014. Influence Organizational Commitment On The Quality Of

Accounting Information System. International Journal of Scientific & Technology

Research, 3(9), pp.299-305.

Trigo, A., Belfo, F. and Estébanez, R.P., 2016. Accounting Information Systems:

evolving towards a business process oriented accounting. Procedia Computer

Science, 100, pp.987-994.

Upadhaya, B., Munir, R. and Blount, Y., 2014. Association between performance

measurement systems and organisational effectiveness. International Journal of

Operations & Production Management, 34(7), pp.853-875.

Reference list

Ceran, M.B., Gungor, S. and Konya, S., 2016. The role of accounting information

systems in preventing the financial crises experienced in businesses. Economics,

Management, and Financial Markets, 11(1), pp.294-303.

Collier, P.M., 2015. Accounting for managers: Interpreting accounting information for

decision making. John Wiley & Sons.

Galliers, R.D. and Leidner, D.E., 2014. Strategic information management:

challenges and strategies in managing information systems. Routledge.

Gullberg, C., 2016. What makes accounting information timely?. Qualitative

Research in Accounting & Management, 13(2), pp.189-215.

Guragai, B., Hunt, N.C., Neri, M.P. and Taylor, E.Z., 2015. Accounting information

systems and ethics research: Review, synthesis, and the future. Journal of

Information Systems, 31(2), pp.65-81.

Krahel, J.P. and Vasarhelyi, M.A., 2014. AIS as a facilitator of accounting change:

Technology, practice, and education. Journal of Information Systems, 28(2), pp.1-15.

Medina-Quintero, J.M., Mora, A. and Abrego, D., 2015. Enterprise technology in

support for accounting information systems. An innovation and productivity

approach. JISTEM-Journal of Information Systems and Technology

Management, 12(1), pp.26-44.

Nan, L. and Wen, X., 2014. Financing and investment efficiency, information quality,

and accounting biases. Management Science, 60(9), pp.2308-2323.

Nurhayati, N. and Mulyani, S., 2015. User participation on system development, user

competence and top management commitment and their effect on the success of the

implementation of accounting information systems. European Journal of Business

and Innovation Research, 3(2), pp.22-35.

Prasad, A. and Green, P., 2015. Organizational competencies and dynamic

accounting information system capability: impact on AIS processes and firm

performance. Journal of Information Systems, 29(3), pp.123-149.

Silviu-Virgil, C., 2014. The importance of the accounting information for the

decisional process. THE ANNALS OF THE UNIVERSITY OF ORADEA, p.591.

Syaifullah, M., 2014. Influence Organizational Commitment On The Quality Of

Accounting Information System. International Journal of Scientific & Technology

Research, 3(9), pp.299-305.

Trigo, A., Belfo, F. and Estébanez, R.P., 2016. Accounting Information Systems:

evolving towards a business process oriented accounting. Procedia Computer

Science, 100, pp.987-994.

Upadhaya, B., Munir, R. and Blount, Y., 2014. Association between performance

measurement systems and organisational effectiveness. International Journal of

Operations & Production Management, 34(7), pp.853-875.

11CASE STUDY – ADAM & CO

Usenko, L.N., Bogataya, I.N., Bukhov, N.V., Kuvaldina, T.B. and Pavlyuk, A.V.,

2018. Formation of an integrated accounting and analytical management system for

value analysis purposes. European Research Studies, 21, p.63.

Yigitbasioglu, O., 2016. Firms’ information system characteristics and management

accounting adaptability. International Journal of Accounting and Information

Management, 24(1), pp.20-37.

Usenko, L.N., Bogataya, I.N., Bukhov, N.V., Kuvaldina, T.B. and Pavlyuk, A.V.,

2018. Formation of an integrated accounting and analytical management system for

value analysis purposes. European Research Studies, 21, p.63.

Yigitbasioglu, O., 2016. Firms’ information system characteristics and management

accounting adaptability. International Journal of Accounting and Information

Management, 24(1), pp.20-37.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.