Holmes Institute HA2042: Case Study of Adam & Co. Accounting Systems

VerifiedAdded on 2022/09/18

|13

|2979

|31

Case Study

AI Summary

This case study analyzes the accounting information systems of Adam & Co., a Perth-based wholesaler, focusing on its purchases, cash disbursements, and payroll systems. The analysis begins with system flowcharts illustrating the processes within each system. The report identifies weaknesses in the purchases system, such as the involvement of multiple clerks and potential risks related to supplier fraud, delivery issues, and inventory management. The cash disbursements system is evaluated for internal control weaknesses, including lack of proper oversight, potential for fictitious payments, and inefficiencies in matching documents. The payroll system is also examined for internal control weaknesses. The study concludes with recommendations for improving these systems, addressing the identified risks, and enhancing overall efficiency and control within Adam & Co.'s accounting operations. The assignment highlights the need for stronger internal controls, improved authorization procedures, and more streamlined processes to mitigate risks and ensure accurate financial reporting. The case study is based on the assignment brief for HA2042 Accounting Information Systems, submitted to Holmes Institute.

Running head: CASE STUDY – ADAM & CO.

Case Study – Adam & Co.

Name of the Student

Name of the University

Author Note

Case Study – Adam & Co.

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CASE STUDY – ADAM & CO.

Executive Summary

This report contains an analysis of the Purchases System, Cash Disbursements System and the

Payroll System that the organisation Adam & Co. has in place. This analysis is initially done

through a diagrammatic representation of all the systems in the form of flowcharts. The

flowcharts also enable a smoother analysis of the processes being undertaken by the company.

Various sources of literature are then referred to get an idea about the ideal systems that every

company should have in place. The analysis has identified the problems associated with each of

the systems. The risks that occur due to these problems are also mentioned in detail. This report

ends with a conclusion which contains the final meaning of all the analysis conducted on Adam

& Co. Some recommendations are also made to improve the processes undertaken by the

company.

Executive Summary

This report contains an analysis of the Purchases System, Cash Disbursements System and the

Payroll System that the organisation Adam & Co. has in place. This analysis is initially done

through a diagrammatic representation of all the systems in the form of flowcharts. The

flowcharts also enable a smoother analysis of the processes being undertaken by the company.

Various sources of literature are then referred to get an idea about the ideal systems that every

company should have in place. The analysis has identified the problems associated with each of

the systems. The risks that occur due to these problems are also mentioned in detail. This report

ends with a conclusion which contains the final meaning of all the analysis conducted on Adam

& Co. Some recommendations are also made to improve the processes undertaken by the

company.

2CASE STUDY – ADAM & CO.

Table of Contents

Introduction..................................................................................................................................3

System flowchart of payroll system.............................................................................................6

Description of weaknesses and risks of the purchases system.....................................................7

Description of internal control weakness in the Cash Disbursements System............................8

Description of internal control weakness in the Payroll System.................................................9

Conclusion.................................................................................................................................10

References..................................................................................................................................12

Table of Contents

Introduction..................................................................................................................................3

System flowchart of payroll system.............................................................................................6

Description of weaknesses and risks of the purchases system.....................................................7

Description of internal control weakness in the Cash Disbursements System............................8

Description of internal control weakness in the Payroll System.................................................9

Conclusion.................................................................................................................................10

References..................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CASE STUDY – ADAM & CO.

Introduction

Adam & Co. is a Perth based wholesaler of industrial supplies. It imports its inventories

from manufacturers in China, Thailand and Vietnam. It also has a centralised accounting system

which consist of different terminals. The company mainly consists of three accounting systems

called the Purchases system, Payroll system and Cash distributions system. All the systems are

maintained in a systematic manner in accordance with the necessities of the organisation.

Although the system is considered to be robust and satisfying the needs of the organisation, there

may still be a few weaknesses that might be existing within these systems. A visual

representation of the process flows is undertaken for the convenience. An analysis of the existing

systems is done to identify the potential weaknesses that exist within the system and to identify

the measures to rectify them.

Introduction

Adam & Co. is a Perth based wholesaler of industrial supplies. It imports its inventories

from manufacturers in China, Thailand and Vietnam. It also has a centralised accounting system

which consist of different terminals. The company mainly consists of three accounting systems

called the Purchases system, Payroll system and Cash distributions system. All the systems are

maintained in a systematic manner in accordance with the necessities of the organisation.

Although the system is considered to be robust and satisfying the needs of the organisation, there

may still be a few weaknesses that might be existing within these systems. A visual

representation of the process flows is undertaken for the convenience. An analysis of the existing

systems is done to identify the potential weaknesses that exist within the system and to identify

the measures to rectify them.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CASE STUDY – ADAM & CO.

System flowchart of purchases system

Yes

No

Select a vendor and prepare

a purchase order. Print two

hard copies of the order and

send one to vendor

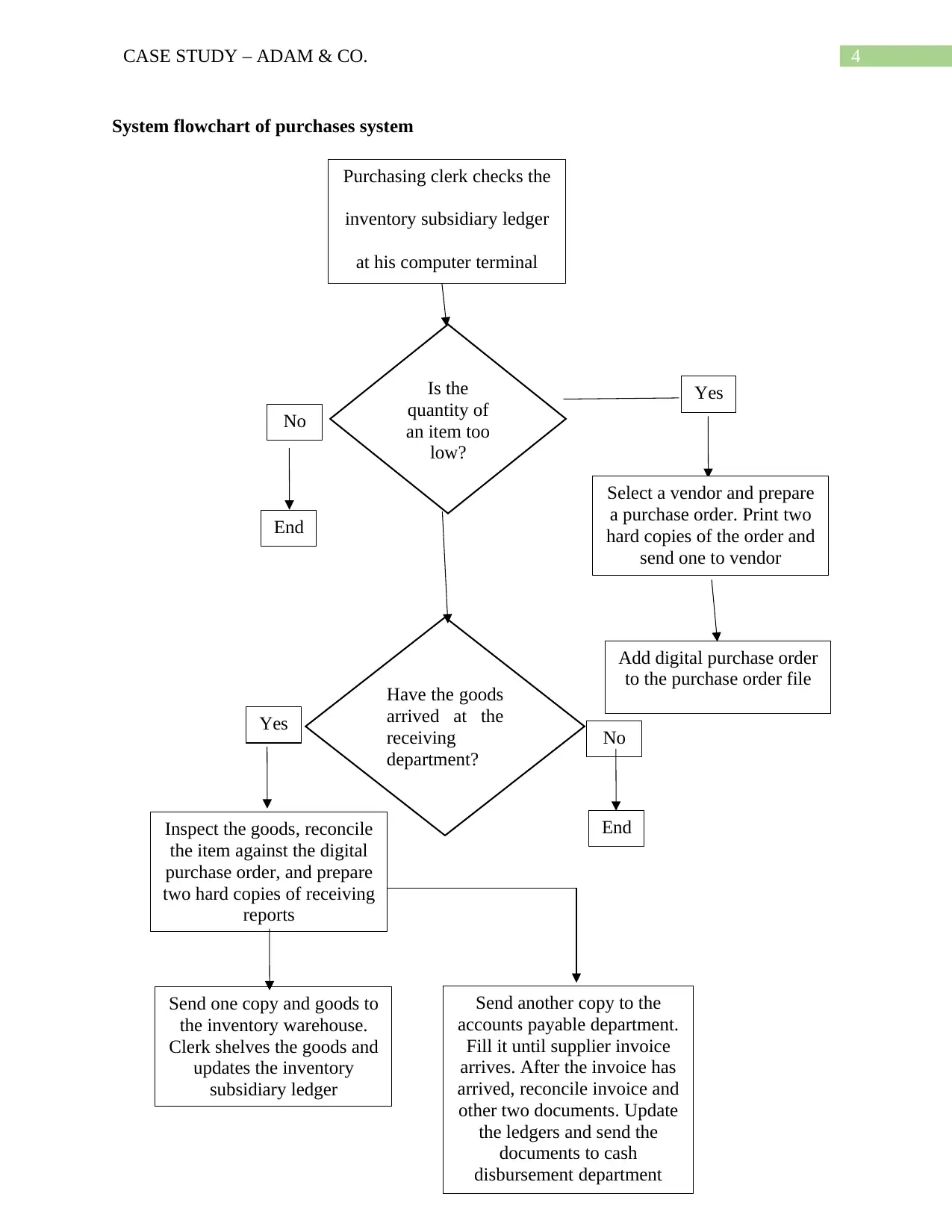

Purchasing clerk checks the

inventory subsidiary ledger

at his computer terminal

Is the

quantity of

an item too

low?

Add digital purchase order

to the purchase order file

End

Have the goods

arrived at the

receiving

department?

Yes

Inspect the goods, reconcile

the item against the digital

purchase order, and prepare

two hard copies of receiving

reports

Send one copy and goods to

the inventory warehouse.

Clerk shelves the goods and

updates the inventory

subsidiary ledger

Send another copy to the

accounts payable department.

Fill it until supplier invoice

arrives. After the invoice has

arrived, reconcile invoice and

other two documents. Update

the ledgers and send the

documents to cash

disbursement department

No

End

System flowchart of purchases system

Yes

No

Select a vendor and prepare

a purchase order. Print two

hard copies of the order and

send one to vendor

Purchasing clerk checks the

inventory subsidiary ledger

at his computer terminal

Is the

quantity of

an item too

low?

Add digital purchase order

to the purchase order file

End

Have the goods

arrived at the

receiving

department?

Yes

Inspect the goods, reconcile

the item against the digital

purchase order, and prepare

two hard copies of receiving

reports

Send one copy and goods to

the inventory warehouse.

Clerk shelves the goods and

updates the inventory

subsidiary ledger

Send another copy to the

accounts payable department.

Fill it until supplier invoice

arrives. After the invoice has

arrived, reconcile invoice and

other two documents. Update

the ledgers and send the

documents to cash

disbursement department

No

End

5CASE STUDY – ADAM & CO.

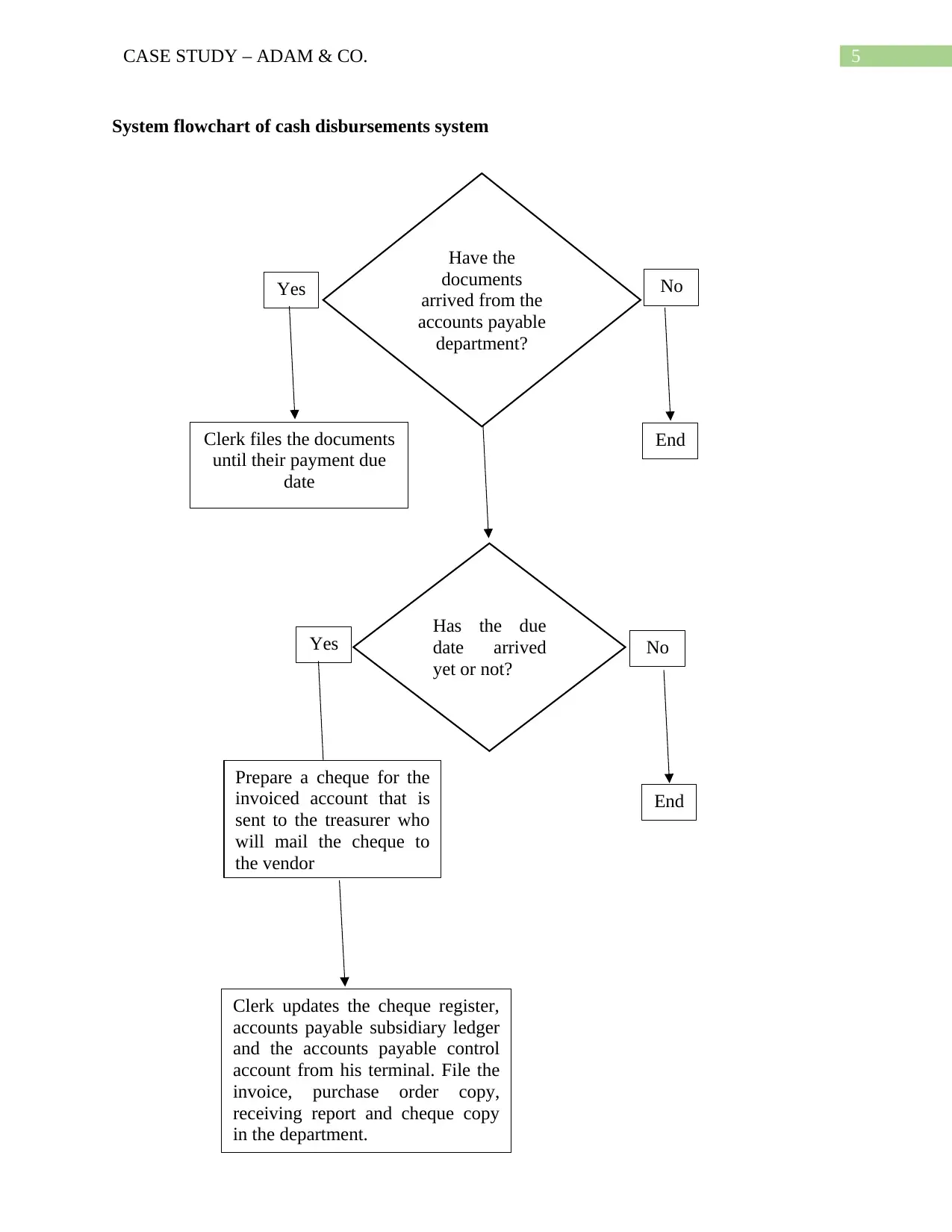

System flowchart of cash disbursements system

Have the

documents

arrived from the

accounts payable

department?

Yes No

Clerk files the documents

until their payment due

date

End

Has the due

date arrived

yet or not?

Yes No

Prepare a cheque for the

invoiced account that is

sent to the treasurer who

will mail the cheque to

the vendor

End

Clerk updates the cheque register,

accounts payable subsidiary ledger

and the accounts payable control

account from his terminal. File the

invoice, purchase order copy,

receiving report and cheque copy

in the department.

System flowchart of cash disbursements system

Have the

documents

arrived from the

accounts payable

department?

Yes No

Clerk files the documents

until their payment due

date

End

Has the due

date arrived

yet or not?

Yes No

Prepare a cheque for the

invoiced account that is

sent to the treasurer who

will mail the cheque to

the vendor

End

Clerk updates the cheque register,

accounts payable subsidiary ledger

and the accounts payable control

account from his terminal. File the

invoice, purchase order copy,

receiving report and cheque copy

in the department.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CASE STUDY – ADAM & CO.

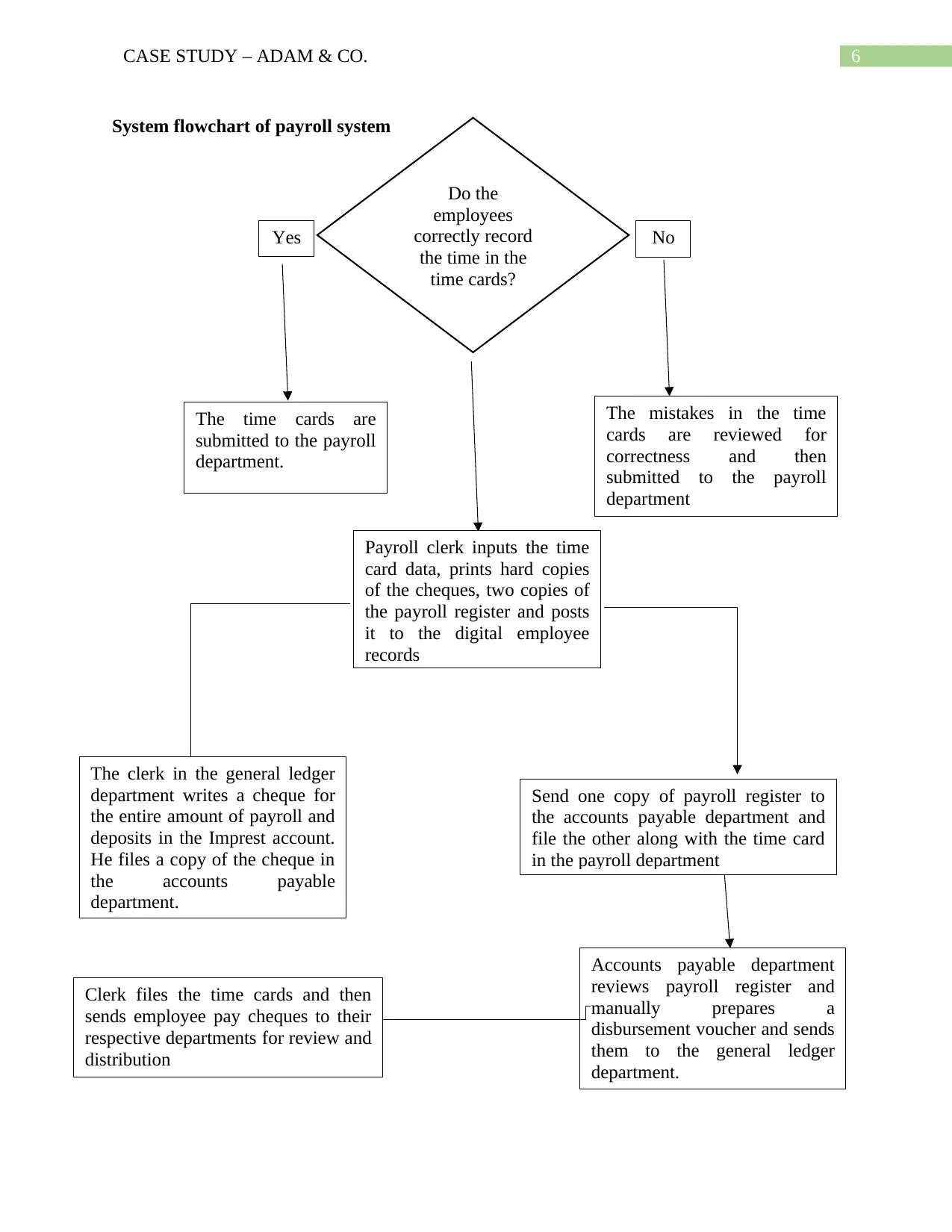

System flowchart of payroll system

The mistakes in the time

cards are reviewed for

correctness and then

submitted to the payroll

department

The time cards are

submitted to the payroll

department.

Do the

employees

correctly record

the time in the

time cards?

Yes No

Payroll clerk inputs the time

card data, prints hard copies

of the cheques, two copies of

the payroll register and posts

it to the digital employee

records

Clerk files the time cards and then

sends employee pay cheques to their

respective departments for review and

distribution

Send one copy of payroll register to

the accounts payable department and

file the other along with the time card

in the payroll department

Accounts payable department

reviews payroll register and

manually prepares a

disbursement voucher and sends

them to the general ledger

department.

The clerk in the general ledger

department writes a cheque for

the entire amount of payroll and

deposits in the Imprest account.

He files a copy of the cheque in

the accounts payable

department.

System flowchart of payroll system

The mistakes in the time

cards are reviewed for

correctness and then

submitted to the payroll

department

The time cards are

submitted to the payroll

department.

Do the

employees

correctly record

the time in the

time cards?

Yes No

Payroll clerk inputs the time

card data, prints hard copies

of the cheques, two copies of

the payroll register and posts

it to the digital employee

records

Clerk files the time cards and then

sends employee pay cheques to their

respective departments for review and

distribution

Send one copy of payroll register to

the accounts payable department and

file the other along with the time card

in the payroll department

Accounts payable department

reviews payroll register and

manually prepares a

disbursement voucher and sends

them to the general ledger

department.

The clerk in the general ledger

department writes a cheque for

the entire amount of payroll and

deposits in the Imprest account.

He files a copy of the cheque in

the accounts payable

department.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CASE STUDY – ADAM & CO.

Description of weaknesses and risks of the purchases system

In case of the purchases system, the main weakness is the presence of too many people

who are responsible for its maintenance. The functions of ordering the goods whose stock levels

are too low and the clerk responsible for inspecting the goods and receiving them. The received

goods are sent to another clerk who is responsible for maintaining the goods received by the

company at a particular point of time. One of the goods received report is then sent to the

accounts payable department. The clerk in this department is responsible for filing it until the

arrival of the supplier’s invoice. After receiving the invoice, this clerk then pulls up another

temporary file and reconciles the three documents that were received by him. While the process

followed by the system ensures that the stock taking and record keeping are done in an efficient

manner, it is too costly for a number of reasons. The main risks associated with a purchase

system are the frauds by suppliers, delivery risks in transporting from a different country, fraud

that can be committed by the suppliers or the employees and problems related to the quality of

the products (Sandberg and Mena 2015). These risks also highlight the inefficiencies in the

current system. While the clerks maintain the records and quantity of the product required

efficiently, they fail to inspect the quality of the product at the time of the delivery itself. In case

of delivery of bad quality products, it will cause a delay in the reorder or return of the bad quality

products. Another inefficiency is having a terminal that is responsible for ordering the quantity

of goods. This could be done away with as the department responsible for receiving the goods

can also perform the function of placing the order of a particular item. Another risk is associated

with the estimates made by the clerks about the quantity of goods required at once. Too much of

a conservative estimate by the clerk results in the overstocking of goods and increases the

Description of weaknesses and risks of the purchases system

In case of the purchases system, the main weakness is the presence of too many people

who are responsible for its maintenance. The functions of ordering the goods whose stock levels

are too low and the clerk responsible for inspecting the goods and receiving them. The received

goods are sent to another clerk who is responsible for maintaining the goods received by the

company at a particular point of time. One of the goods received report is then sent to the

accounts payable department. The clerk in this department is responsible for filing it until the

arrival of the supplier’s invoice. After receiving the invoice, this clerk then pulls up another

temporary file and reconciles the three documents that were received by him. While the process

followed by the system ensures that the stock taking and record keeping are done in an efficient

manner, it is too costly for a number of reasons. The main risks associated with a purchase

system are the frauds by suppliers, delivery risks in transporting from a different country, fraud

that can be committed by the suppliers or the employees and problems related to the quality of

the products (Sandberg and Mena 2015). These risks also highlight the inefficiencies in the

current system. While the clerks maintain the records and quantity of the product required

efficiently, they fail to inspect the quality of the product at the time of the delivery itself. In case

of delivery of bad quality products, it will cause a delay in the reorder or return of the bad quality

products. Another inefficiency is having a terminal that is responsible for ordering the quantity

of goods. This could be done away with as the department responsible for receiving the goods

can also perform the function of placing the order of a particular item. Another risk is associated

with the estimates made by the clerks about the quantity of goods required at once. Too much of

a conservative estimate by the clerk results in the overstocking of goods and increases the

8CASE STUDY – ADAM & CO.

carrying costs associated with the goods. Another risk associated with the department is the

allocation of the budget (Dai and Gao 2014). The risks associated with this department are

similar to the risks associated with placing an order. Improper allocation of the budget results in

making the business operations unprofitable. The final problem associated with the purchases

system is related to the authorisation procedures. While individual clerks oversee their respective

functions, there is no authority that oversees the efficiency with which they function and results

in identifying any misdoings more difficult than in the normal course.

Description of internal control weakness in the Cash Disbursements System

As in the case of Purchases System, there is no proper authority that is overseeing the

operations of the Cash disbursements system. While it is true that the cash disbursements system

should be overseen only by the accounts payable department, there is always a risk due to the

nature of the people operating in the accounts payable department. Another problem is the

involvement of the receiving clerk in the process implemented by the organisation (Attom 2013).

All cheques related to a particular order should always be maintained by the accounts payable

department. Having too many copies of the same cheque results in the creation of fictitious

payments and omission of payments by one of the clerks. Matching various documents like

invoice, purchase order copy, receiving report and cheque copy of a single transaction becomes a

tedious process to undertake. There is also an absence of an authority that is responsible for

managing the restricted funds. Although this type of authority is common in non-profit

organisations, funds which are set aside for a specific purpose like procurement of goods or

payment to creditors could be utilised in the wrong manner in the current system (Herrera and

Ibeas 2015). The other problem associated with the current system is the number of signing

authorities that the company has in place. While it is always advisable that the number of signing

carrying costs associated with the goods. Another risk associated with the department is the

allocation of the budget (Dai and Gao 2014). The risks associated with this department are

similar to the risks associated with placing an order. Improper allocation of the budget results in

making the business operations unprofitable. The final problem associated with the purchases

system is related to the authorisation procedures. While individual clerks oversee their respective

functions, there is no authority that oversees the efficiency with which they function and results

in identifying any misdoings more difficult than in the normal course.

Description of internal control weakness in the Cash Disbursements System

As in the case of Purchases System, there is no proper authority that is overseeing the

operations of the Cash disbursements system. While it is true that the cash disbursements system

should be overseen only by the accounts payable department, there is always a risk due to the

nature of the people operating in the accounts payable department. Another problem is the

involvement of the receiving clerk in the process implemented by the organisation (Attom 2013).

All cheques related to a particular order should always be maintained by the accounts payable

department. Having too many copies of the same cheque results in the creation of fictitious

payments and omission of payments by one of the clerks. Matching various documents like

invoice, purchase order copy, receiving report and cheque copy of a single transaction becomes a

tedious process to undertake. There is also an absence of an authority that is responsible for

managing the restricted funds. Although this type of authority is common in non-profit

organisations, funds which are set aside for a specific purpose like procurement of goods or

payment to creditors could be utilised in the wrong manner in the current system (Herrera and

Ibeas 2015). The other problem associated with the current system is the number of signing

authorities that the company has in place. While it is always advisable that the number of signing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CASE STUDY – ADAM & CO.

authorities should be kept to a minimum, it is better to have another signing authority. This is

due to the risk that occurs with the processing of urgent payments in case of the absence of a

signing authority. There is also no mention of the company maintaining pre-numbered cheques.

This will cause confusion in the maintenance and identification of pre-existing records. There is

also no pre-written notice that prohibits the signing of cheques in advance. This is another way

of manipulating the records where multiple cheques can be issued to manipulate the records but

they are related to a single transaction. The mail system that is implemented by the company also

needs to be efficient to ensure that the cheques that are being mailed by the accounts payable

department reach the vendor correctly. There is also no segregation of a cheque that is being

mailed on the basis of amount. Cheques containing large amounts and petty cash cheques are

different from each other and hence should be treated separately. This will lead to the creation of

a more clear system that maintains records in an appropriate manner.

Description of internal control weakness in the Payroll System

In the given scenario, the main inefficiency that exists in the payroll system of Adam &

Co. is the time card system (Oloyede, Adedoyin and Adewole 2013). There are a large number

of these time cards and maintaining them properly is an extremely difficult task. One of the main

problems that exist in a payroll system are the improper claims made on the basis of improper

bills (Sullivan 2014). An unethical understanding between the supervisors and employees of the

payroll department will likely result in overpayment of wages. The lack of supervision also

increases the chances of the occurrence of this risk. The payroll patterns that are being followed

by the company are quite complicated in nature and any form of ignorance by anyone involved

in the system will lead to major frauds or errors in the payroll system of the company. Involving

the accounts payable department in the payroll department increases the pressure on them as they

authorities should be kept to a minimum, it is better to have another signing authority. This is

due to the risk that occurs with the processing of urgent payments in case of the absence of a

signing authority. There is also no mention of the company maintaining pre-numbered cheques.

This will cause confusion in the maintenance and identification of pre-existing records. There is

also no pre-written notice that prohibits the signing of cheques in advance. This is another way

of manipulating the records where multiple cheques can be issued to manipulate the records but

they are related to a single transaction. The mail system that is implemented by the company also

needs to be efficient to ensure that the cheques that are being mailed by the accounts payable

department reach the vendor correctly. There is also no segregation of a cheque that is being

mailed on the basis of amount. Cheques containing large amounts and petty cash cheques are

different from each other and hence should be treated separately. This will lead to the creation of

a more clear system that maintains records in an appropriate manner.

Description of internal control weakness in the Payroll System

In the given scenario, the main inefficiency that exists in the payroll system of Adam &

Co. is the time card system (Oloyede, Adedoyin and Adewole 2013). There are a large number

of these time cards and maintaining them properly is an extremely difficult task. One of the main

problems that exist in a payroll system are the improper claims made on the basis of improper

bills (Sullivan 2014). An unethical understanding between the supervisors and employees of the

payroll department will likely result in overpayment of wages. The lack of supervision also

increases the chances of the occurrence of this risk. The payroll patterns that are being followed

by the company are quite complicated in nature and any form of ignorance by anyone involved

in the system will lead to major frauds or errors in the payroll system of the company. Involving

the accounts payable department in the payroll department increases the pressure on them as they

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CASE STUDY – ADAM & CO.

also have to undertake the responsibilities of the cash disbursements department and purchases

system (Thite and Sandhu 2014). There is no proper authority for the cheques written by the

clerk for the entire payroll system. As the amounts that would be written by him tend me of large

scale, there should be a proper authority that is responsible for processing and authorising the

cheques written by the clerk. Having one person responsible for the entire payroll increases the

risk of theft, embezzlement, falsification of documents and manipulations for personal gains.

Clerical errors like setting up the wrong tax rate, mismanaging documents related to the salaries

and missing deadlines is also a risk that is faced by the current payroll system. This also leads to

the risk of paying huge penalties to the regulatory authorities for mismanagement and

falsification of funds. Wrong processing of the documents results in the miscalculation of the

salaries of the people in the payroll and causes losses or unnecessary disruptions in the

organisation. Although this may not always occur due to the intentional misdeed of the person in

charge, the consequences occurring due to the misdeed cannot be avoided altogether. The tasks

undertaken by the general ledger clerk are also complicated in nature and require them to deal

with a huge number of documents at once.

Conclusion

From the above analysis, it can be suggested that the systems that the organisation has in

place are intended to make sure that all the processes within the organisation are carried out

smoothly. However, there are a huge amount of risks that the entity is facing due to the

responsibilities being placed on a selected group of persons. There are a number of risks that are

being faced by Adam & Co. due to the lack of a proper internal control system. Some of them

include the falsification and manipulation of documents, embezzlement of records, wrong claims

made by employees and ignoring the patterns being followed in the company as a whole. The

also have to undertake the responsibilities of the cash disbursements department and purchases

system (Thite and Sandhu 2014). There is no proper authority for the cheques written by the

clerk for the entire payroll system. As the amounts that would be written by him tend me of large

scale, there should be a proper authority that is responsible for processing and authorising the

cheques written by the clerk. Having one person responsible for the entire payroll increases the

risk of theft, embezzlement, falsification of documents and manipulations for personal gains.

Clerical errors like setting up the wrong tax rate, mismanaging documents related to the salaries

and missing deadlines is also a risk that is faced by the current payroll system. This also leads to

the risk of paying huge penalties to the regulatory authorities for mismanagement and

falsification of funds. Wrong processing of the documents results in the miscalculation of the

salaries of the people in the payroll and causes losses or unnecessary disruptions in the

organisation. Although this may not always occur due to the intentional misdeed of the person in

charge, the consequences occurring due to the misdeed cannot be avoided altogether. The tasks

undertaken by the general ledger clerk are also complicated in nature and require them to deal

with a huge number of documents at once.

Conclusion

From the above analysis, it can be suggested that the systems that the organisation has in

place are intended to make sure that all the processes within the organisation are carried out

smoothly. However, there are a huge amount of risks that the entity is facing due to the

responsibilities being placed on a selected group of persons. There are a number of risks that are

being faced by Adam & Co. due to the lack of a proper internal control system. Some of them

include the falsification and manipulation of documents, embezzlement of records, wrong claims

made by employees and ignoring the patterns being followed in the company as a whole. The

11CASE STUDY – ADAM & CO.

company needs to employ more people in the organisation, especially in the supervision of tasks.

While this may not immediately reduce all the risks, it reduces the burden on the employees and

ensures a more efficient performance by the company.

company needs to employ more people in the organisation, especially in the supervision of tasks.

While this may not immediately reduce all the risks, it reduces the burden on the employees and

ensures a more efficient performance by the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.