HA2042: Case Study Analysis of Adam & Co Accounting Systems

VerifiedAdded on 2022/11/01

|11

|3026

|419

Case Study

AI Summary

This case study analyzes the accounting information systems of Adam & Co, a wholesaler of industrial supplies. It examines the system flowcharts for the purchase, cash disbursement, and payroll systems, identifying weaknesses in internal controls. The report highlights risks associated with these weaknesses, such as the lack of segregation of duties, potential delays in inventory management, and vulnerabilities in payroll processing. The study emphasizes the need for improved procedures, including the use of automated systems, dual approvals, and regular internal audits, to mitigate these risks and enhance the efficiency and accuracy of the accounting processes. The case study also underlines the importance of secure data storage and the implementation of robust internal controls to safeguard sensitive financial information. The analysis covers the advantages of interdepartmental interfacing, the need for a system that can handle emergencies and the importance of ensuring that only valid creditors are paid on time.

Running head: CASE STUDY – ADAM & CO

Case Study – Adam & Co

Name of the Student:

Name of the University:

Author Note

Case Study – Adam & Co

Name of the Student:

Name of the University:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CASE STUDY – ADAM & CO

Executive Summary

The report has been prepared by the business analyst of Adam & Co for the analysis

and decision making. The system flowchart of purchase, cash disbursement and

payroll has been described. The internal control weaknesses have been detected by

him. The associated risks with the relevant fault have been highlighted.

Executive Summary

The report has been prepared by the business analyst of Adam & Co for the analysis

and decision making. The system flowchart of purchase, cash disbursement and

payroll has been described. The internal control weaknesses have been detected by

him. The associated risks with the relevant fault have been highlighted.

2CASE STUDY – ADAM & CO

Table of Contents

Introduction...................................................................................................................3

System flowchart of purchases system........................................................................4

System flowchart of cash disbursements system........................................................5

System flowchart of payroll system..............................................................................7

Conclusion....................................................................................................................8

Reference list................................................................................................................9

Table of Contents

Introduction...................................................................................................................3

System flowchart of purchases system........................................................................4

System flowchart of cash disbursements system........................................................5

System flowchart of payroll system..............................................................................7

Conclusion....................................................................................................................8

Reference list................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CASE STUDY – ADAM & CO

Introduction

Adam & Co is a wholesaler of industrial supplies based in Perth. The sources

for its inventories are from manufacturers in Thailand, Vietnam and China. The

company has adopted a centralized accounting system having networked terminals

at various locations. An accounting information system is a mechanism which

generates financial statements by incorporating the bookkeeping process. It stores

and manages the data which are useful to its users for reporting the relevant

information to its owners and shareholders. Accounting Information System makes

use of high quality, rapid and current information regarding the internal conditions to

formulate their strategic decisions (Collier 2015). This system is built in a manner by

which the data to be displayed can be customized as per the required information

relating to the business. The users of the data are creditors, tax authorities and

investors. It is a method used to track the accounting activities concerning the

resources of information technology (Patel 2015). It combines the traditional

practices of accounting like Generally Accepted Accounting Principles with new

supplies of information technology.

The system includes several elements in its accounting cycle. The contents of an

information system vary from industry to another. However, the essential items of

expenses, employee information, tax information, customer information and revenue

are included in most systems (Prasad and Green 2015). Individual data

specifications include purchase requisitions, check registers, payroll, financial

statement information, invoices, inventory, trial balance, ledger and reports relating

to sales order and analysis. It has the structure of a database for storing data. It is

programmed and designed in a manner which permits the data and table

manipulation. It facilitates input of data and editing of previously entered data

(Laudon and Laudon 2016). These are highly secured platforms having measures

taken for prevention against hackers, viruses and other sources that have been

attempted to collect information. As cybersecurity has increasingly been given

importance, the companies have started storing their data using this electronic

method.

The financial statements that are prepared by bookkeeping of accounts are used by

the users for the purpose of decision making. It involves the preparation of income

statement, balance sheet and statement of cash flows (Jing 2015). It has the

features of cost benefits, compatibility and flexibility. It follows four types of

principles-

Output of data – The system stores the data and supports with relevant data at the

time of decision making. The output devices used by the system are projectors,

printers and other similar devices which help to provide with an outcome.

Processing device – The processing device takes the input which has been received

by the input device and processes it to provide results. It handles the data in a digital

format which is a language of the computer itself (Taiwo 2016). It transforms large

portions of data into user friendly reports within minutes of time.

Source documents – These documents are essential parts of the accounting

information system as they contain the data of the organization. Invoices, sales

orders and other relevant documents relating to the business are prepared by the

accounting information system.

Introduction

Adam & Co is a wholesaler of industrial supplies based in Perth. The sources

for its inventories are from manufacturers in Thailand, Vietnam and China. The

company has adopted a centralized accounting system having networked terminals

at various locations. An accounting information system is a mechanism which

generates financial statements by incorporating the bookkeeping process. It stores

and manages the data which are useful to its users for reporting the relevant

information to its owners and shareholders. Accounting Information System makes

use of high quality, rapid and current information regarding the internal conditions to

formulate their strategic decisions (Collier 2015). This system is built in a manner by

which the data to be displayed can be customized as per the required information

relating to the business. The users of the data are creditors, tax authorities and

investors. It is a method used to track the accounting activities concerning the

resources of information technology (Patel 2015). It combines the traditional

practices of accounting like Generally Accepted Accounting Principles with new

supplies of information technology.

The system includes several elements in its accounting cycle. The contents of an

information system vary from industry to another. However, the essential items of

expenses, employee information, tax information, customer information and revenue

are included in most systems (Prasad and Green 2015). Individual data

specifications include purchase requisitions, check registers, payroll, financial

statement information, invoices, inventory, trial balance, ledger and reports relating

to sales order and analysis. It has the structure of a database for storing data. It is

programmed and designed in a manner which permits the data and table

manipulation. It facilitates input of data and editing of previously entered data

(Laudon and Laudon 2016). These are highly secured platforms having measures

taken for prevention against hackers, viruses and other sources that have been

attempted to collect information. As cybersecurity has increasingly been given

importance, the companies have started storing their data using this electronic

method.

The financial statements that are prepared by bookkeeping of accounts are used by

the users for the purpose of decision making. It involves the preparation of income

statement, balance sheet and statement of cash flows (Jing 2015). It has the

features of cost benefits, compatibility and flexibility. It follows four types of

principles-

Output of data – The system stores the data and supports with relevant data at the

time of decision making. The output devices used by the system are projectors,

printers and other similar devices which help to provide with an outcome.

Processing device – The processing device takes the input which has been received

by the input device and processes it to provide results. It handles the data in a digital

format which is a language of the computer itself (Taiwo 2016). It transforms large

portions of data into user friendly reports within minutes of time.

Source documents – These documents are essential parts of the accounting

information system as they contain the data of the organization. Invoices, sales

orders and other relevant documents relating to the business are prepared by the

accounting information system.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CASE STUDY – ADAM & CO

Collection of data – The input device collects all the data that has been sent by the

accountant. It has the capability to store bulk data within it. The system processes

the data and saves it in the digital format, which it can read and process to provide

outcome (Galliers and Leidner 2014). This information is used for carrying out the

decision making processes.

Advantages of the system

Interdepartmental interfacing – The system tries to interface across various

departments at the same time. The sales department has the authority to

upload the budget of sales. The team of inventory management makes use of

the information for conducting the purchase materials and counts of inventory.

On purchasing the stock, there is a notification from the system for the

department of accounts payable of the new invoice (Mancini 2016). The

mechanism can even transfer information of a new order for the customer

service, shipping and manufacturing department are notified of the sale.

Internal controls – Procedures and policies are put forward to the system for

making sure that sensitive vendor, business and customer information are

maintained internal to the company (Pan and Seow 2016). The login

requirements, authorizations, segregation of duties, approvals of physical

access and access approvals used by the users are restricted, which help

them perform the function of the business.

System flowchart of purchases system

The responsibility is allocated to the purchasing clerk who looks after the

inventories every morning by using the computer terminals. He places an order

request with the vendor upon detecting the low quantity of any item. The

management should appoint two clerks for this task as one clerk can be absent and

the inventory for that particular shall not get checked (Ponisciakova, Gogolova and

Ivankova 2015). A situation of emergency may arise in which the demands for the

goods rose which could not have been predicted by him on the previous day.

Therefore, there will be a delay and hindrance of work as the inventory levels will not

be sufficient to meet the demands of its consumers. The receiving reports prepared

by the clerk can be done, which will make the process faster and easier for preparing

reports instead of preparing it manually. All the recording of the transactions should

be conducted technically using the computers as the company has a centralized

accounting system (Upadhaya, Munir and Blount 2014). A change done by an

employee from one department will automatically get updated in the operations of

the other departments wherever required. There will be no requirement of making

the adjustments manually by the employee of each department. The mechanism

helps to manage the costs and order quantities for effective and efficient utilization of

resources. It helps to reduce the additional costs by using computer systems. The

budget calculation is done and purchase requisition is prepared. The quotation is

obtained and invoices are reviewed upon receipt. The payments are recorded in the

cashbook.

Collection of data – The input device collects all the data that has been sent by the

accountant. It has the capability to store bulk data within it. The system processes

the data and saves it in the digital format, which it can read and process to provide

outcome (Galliers and Leidner 2014). This information is used for carrying out the

decision making processes.

Advantages of the system

Interdepartmental interfacing – The system tries to interface across various

departments at the same time. The sales department has the authority to

upload the budget of sales. The team of inventory management makes use of

the information for conducting the purchase materials and counts of inventory.

On purchasing the stock, there is a notification from the system for the

department of accounts payable of the new invoice (Mancini 2016). The

mechanism can even transfer information of a new order for the customer

service, shipping and manufacturing department are notified of the sale.

Internal controls – Procedures and policies are put forward to the system for

making sure that sensitive vendor, business and customer information are

maintained internal to the company (Pan and Seow 2016). The login

requirements, authorizations, segregation of duties, approvals of physical

access and access approvals used by the users are restricted, which help

them perform the function of the business.

System flowchart of purchases system

The responsibility is allocated to the purchasing clerk who looks after the

inventories every morning by using the computer terminals. He places an order

request with the vendor upon detecting the low quantity of any item. The

management should appoint two clerks for this task as one clerk can be absent and

the inventory for that particular shall not get checked (Ponisciakova, Gogolova and

Ivankova 2015). A situation of emergency may arise in which the demands for the

goods rose which could not have been predicted by him on the previous day.

Therefore, there will be a delay and hindrance of work as the inventory levels will not

be sufficient to meet the demands of its consumers. The receiving reports prepared

by the clerk can be done, which will make the process faster and easier for preparing

reports instead of preparing it manually. All the recording of the transactions should

be conducted technically using the computers as the company has a centralized

accounting system (Upadhaya, Munir and Blount 2014). A change done by an

employee from one department will automatically get updated in the operations of

the other departments wherever required. There will be no requirement of making

the adjustments manually by the employee of each department. The mechanism

helps to manage the costs and order quantities for effective and efficient utilization of

resources. It helps to reduce the additional costs by using computer systems. The

budget calculation is done and purchase requisition is prepared. The quotation is

obtained and invoices are reviewed upon receipt. The payments are recorded in the

cashbook.

5CASE STUDY – ADAM & CO

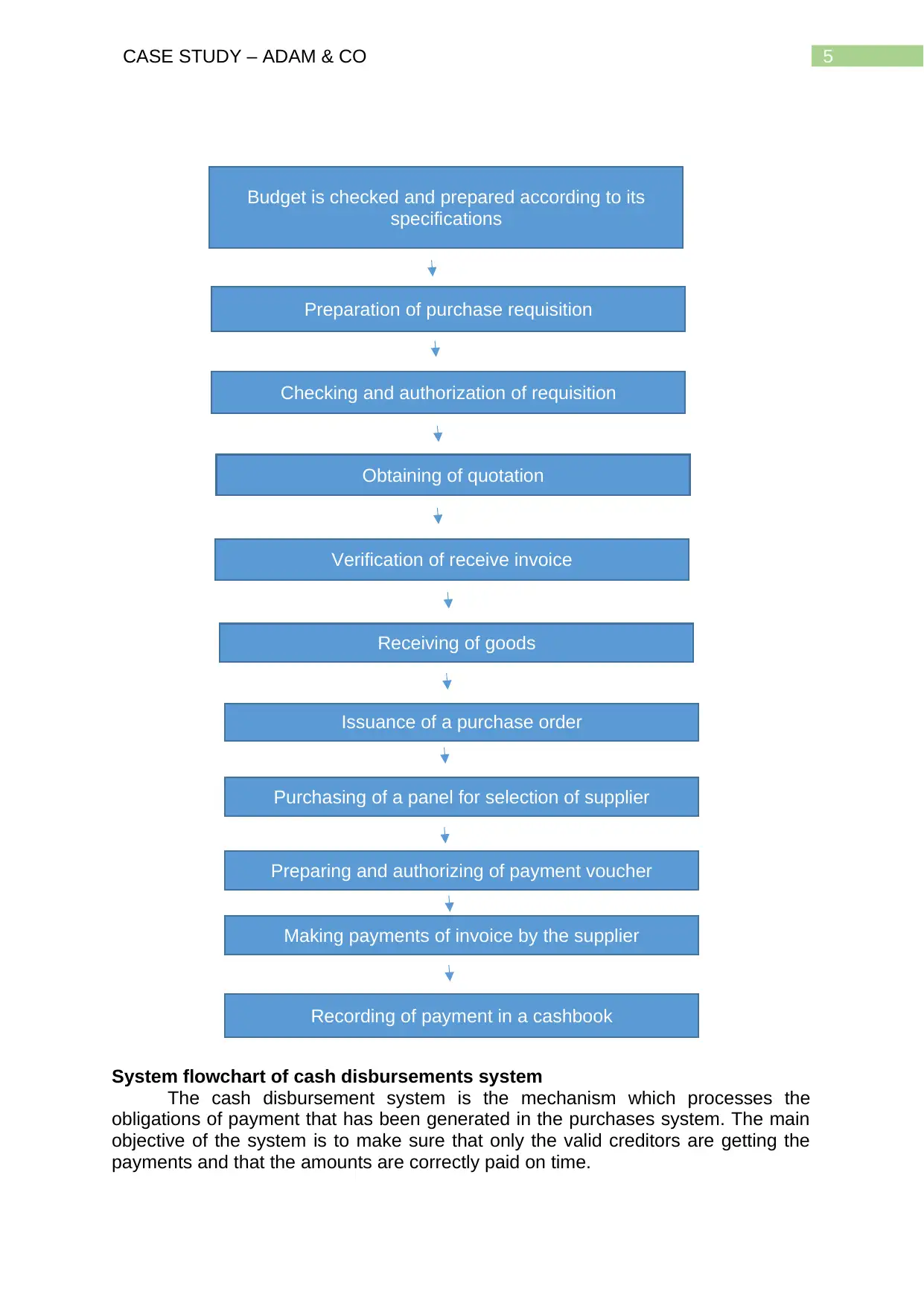

System flowchart of cash disbursements system

The cash disbursement system is the mechanism which processes the

obligations of payment that has been generated in the purchases system. The main

objective of the system is to make sure that only the valid creditors are getting the

payments and that the amounts are correctly paid on time.

Budget is checked and prepared according to its

specifications

Preparation of purchase requisition

Checking and authorization of requisition

Obtaining of quotation

Verification of receive invoice

Receiving of goods

Issuance of a purchase order

Purchasing of a panel for selection of supplier

Preparing and authorizing of payment voucher

Making payments of invoice by the supplier

Recording of payment in a cashbook

System flowchart of cash disbursements system

The cash disbursement system is the mechanism which processes the

obligations of payment that has been generated in the purchases system. The main

objective of the system is to make sure that only the valid creditors are getting the

payments and that the amounts are correctly paid on time.

Budget is checked and prepared according to its

specifications

Preparation of purchase requisition

Checking and authorization of requisition

Obtaining of quotation

Verification of receive invoice

Receiving of goods

Issuance of a purchase order

Purchasing of a panel for selection of supplier

Preparing and authorizing of payment voucher

Making payments of invoice by the supplier

Recording of payment in a cashbook

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CASE STUDY – ADAM & CO

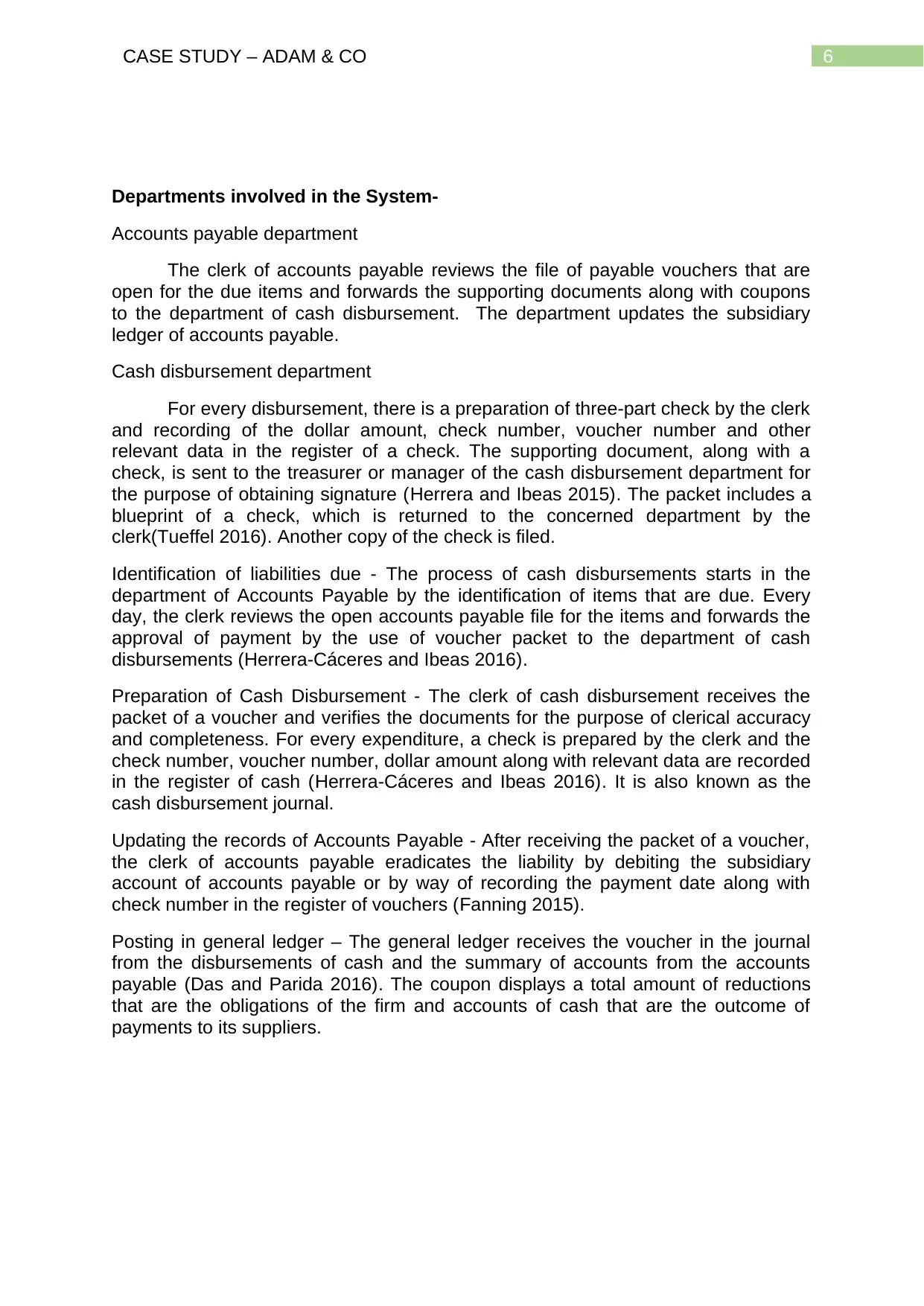

Departments involved in the System-

Accounts payable department

The clerk of accounts payable reviews the file of payable vouchers that are

open for the due items and forwards the supporting documents along with coupons

to the department of cash disbursement. The department updates the subsidiary

ledger of accounts payable.

Cash disbursement department

For every disbursement, there is a preparation of three-part check by the clerk

and recording of the dollar amount, check number, voucher number and other

relevant data in the register of a check. The supporting document, along with a

check, is sent to the treasurer or manager of the cash disbursement department for

the purpose of obtaining signature (Herrera and Ibeas 2015). The packet includes a

blueprint of a check, which is returned to the concerned department by the

clerk(Tueffel 2016). Another copy of the check is filed.

Identification of liabilities due - The process of cash disbursements starts in the

department of Accounts Payable by the identification of items that are due. Every

day, the clerk reviews the open accounts payable file for the items and forwards the

approval of payment by the use of voucher packet to the department of cash

disbursements (Herrera-Cáceres and Ibeas 2016).

Preparation of Cash Disbursement - The clerk of cash disbursement receives the

packet of a voucher and verifies the documents for the purpose of clerical accuracy

and completeness. For every expenditure, a check is prepared by the clerk and the

check number, voucher number, dollar amount along with relevant data are recorded

in the register of cash (Herrera-Cáceres and Ibeas 2016). It is also known as the

cash disbursement journal.

Updating the records of Accounts Payable - After receiving the packet of a voucher,

the clerk of accounts payable eradicates the liability by debiting the subsidiary

account of accounts payable or by way of recording the payment date along with

check number in the register of vouchers (Fanning 2015).

Posting in general ledger – The general ledger receives the voucher in the journal

from the disbursements of cash and the summary of accounts from the accounts

payable (Das and Parida 2016). The coupon displays a total amount of reductions

that are the obligations of the firm and accounts of cash that are the outcome of

payments to its suppliers.

Departments involved in the System-

Accounts payable department

The clerk of accounts payable reviews the file of payable vouchers that are

open for the due items and forwards the supporting documents along with coupons

to the department of cash disbursement. The department updates the subsidiary

ledger of accounts payable.

Cash disbursement department

For every disbursement, there is a preparation of three-part check by the clerk

and recording of the dollar amount, check number, voucher number and other

relevant data in the register of a check. The supporting document, along with a

check, is sent to the treasurer or manager of the cash disbursement department for

the purpose of obtaining signature (Herrera and Ibeas 2015). The packet includes a

blueprint of a check, which is returned to the concerned department by the

clerk(Tueffel 2016). Another copy of the check is filed.

Identification of liabilities due - The process of cash disbursements starts in the

department of Accounts Payable by the identification of items that are due. Every

day, the clerk reviews the open accounts payable file for the items and forwards the

approval of payment by the use of voucher packet to the department of cash

disbursements (Herrera-Cáceres and Ibeas 2016).

Preparation of Cash Disbursement - The clerk of cash disbursement receives the

packet of a voucher and verifies the documents for the purpose of clerical accuracy

and completeness. For every expenditure, a check is prepared by the clerk and the

check number, voucher number, dollar amount along with relevant data are recorded

in the register of cash (Herrera-Cáceres and Ibeas 2016). It is also known as the

cash disbursement journal.

Updating the records of Accounts Payable - After receiving the packet of a voucher,

the clerk of accounts payable eradicates the liability by debiting the subsidiary

account of accounts payable or by way of recording the payment date along with

check number in the register of vouchers (Fanning 2015).

Posting in general ledger – The general ledger receives the voucher in the journal

from the disbursements of cash and the summary of accounts from the accounts

payable (Das and Parida 2016). The coupon displays a total amount of reductions

that are the obligations of the firm and accounts of cash that are the outcome of

payments to its suppliers.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CASE STUDY – ADAM & CO

System flowchart of payroll system

The automated mechanism of payroll system makes the reporting handling of

the payroll functions automatic and smooth without any manual labour involved. It

helps to prepare reports for the purpose of documentation and auditing (Mahajan,

Shukla and Soni 2015). As the company does manual recording, these benefits

could not be enjoyed by them and became their weakness. The electronic method

prevents false and dummy transactions being reported. It automatically helps to

calculate the paid time offs and other employee benefits which the employees are

entitled on the basis of their worked hours. It is vulnerable to be accessible by

dishonest employees. The employees should be allocated unique codes for their

recognition which will help to make the process of reporting smoother and prevent

chaos (Bajdor and Grabara 2014). A clear reporting procedure should be laid out by

the human resource manager. A signature should be made mandatory for the

changes in the employee’s payroll processing (Donelson, Ege and McInnis 2016).

The responsibility of data inputs should be distributed into two departments where

the work by one department gets scrutinized by the other upon carrying out its

process of recording the data. Another weakness detected is printing the copies of

the payroll details and issuing the checks without the accuracies being reviewed.

The accounting department must train one of its employee for conducting the internal

payroll audit at a regular and timely basis. It will prevent the error and manipulation

of data.

System flowchart of payroll system

The automated mechanism of payroll system makes the reporting handling of

the payroll functions automatic and smooth without any manual labour involved. It

helps to prepare reports for the purpose of documentation and auditing (Mahajan,

Shukla and Soni 2015). As the company does manual recording, these benefits

could not be enjoyed by them and became their weakness. The electronic method

prevents false and dummy transactions being reported. It automatically helps to

calculate the paid time offs and other employee benefits which the employees are

entitled on the basis of their worked hours. It is vulnerable to be accessible by

dishonest employees. The employees should be allocated unique codes for their

recognition which will help to make the process of reporting smoother and prevent

chaos (Bajdor and Grabara 2014). A clear reporting procedure should be laid out by

the human resource manager. A signature should be made mandatory for the

changes in the employee’s payroll processing (Donelson, Ege and McInnis 2016).

The responsibility of data inputs should be distributed into two departments where

the work by one department gets scrutinized by the other upon carrying out its

process of recording the data. Another weakness detected is printing the copies of

the payroll details and issuing the checks without the accuracies being reviewed.

The accounting department must train one of its employee for conducting the internal

payroll audit at a regular and timely basis. It will prevent the error and manipulation

of data.

8CASE STUDY – ADAM & CO

Conclusion

As a business analyst of Adam & Co, the report has been prepared for highlighting

the system of a flowchart of purchases system, cash disbursement system and

payroll system. The weakness of internal control in every system, along with its risk

association, has been identified. The preparations of books of accounts and reports

get more accessible and more straightforward by the use of an accounting

information system by a business. The centralized system helps in quick

modifications being done without making manual changes in every system. A proper

reporting system should be followed by the company to overcome its weaknesses

and improve its internal control system. The principles followed by an accounting

information system have been described. The inventory levels are managed by the

purchasing clerk and required orders are placed with the respective vendors. The

cash disbursement transactions should have to be verified and checked before the

checks are issued to its employees. There may be certain false transactions and

diversion of funds from the business. The payroll system keeps track of its

employees and their working hours. The centralized accounting system makes the

process of decision making easier by preparing appropriate and relevant reports.

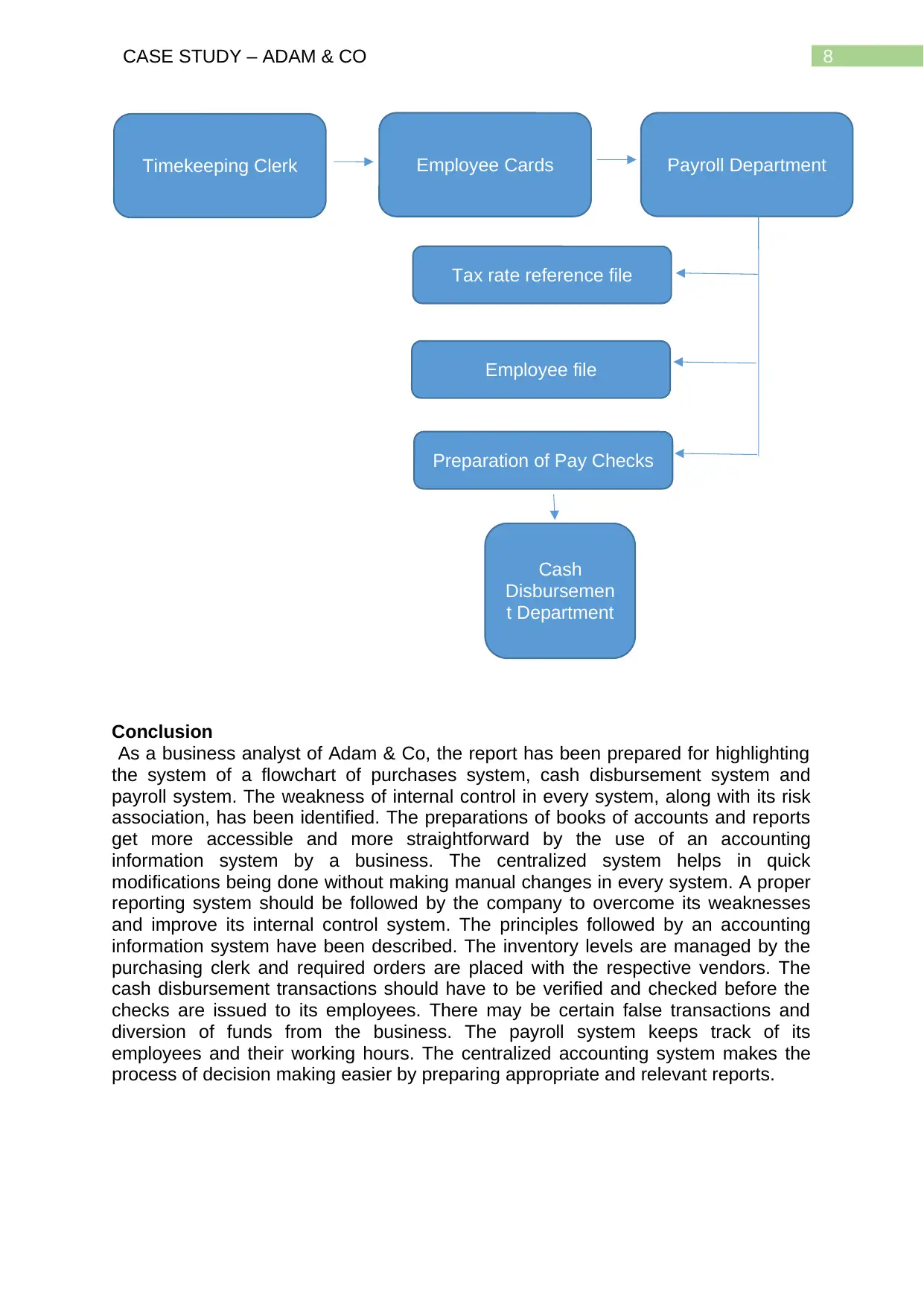

Timekeeping Clerk Employee Cards Payroll Department

Tax rate reference file

Employee file

Preparation of Pay Checks

Cash

Disbursemen

t Department

Conclusion

As a business analyst of Adam & Co, the report has been prepared for highlighting

the system of a flowchart of purchases system, cash disbursement system and

payroll system. The weakness of internal control in every system, along with its risk

association, has been identified. The preparations of books of accounts and reports

get more accessible and more straightforward by the use of an accounting

information system by a business. The centralized system helps in quick

modifications being done without making manual changes in every system. A proper

reporting system should be followed by the company to overcome its weaknesses

and improve its internal control system. The principles followed by an accounting

information system have been described. The inventory levels are managed by the

purchasing clerk and required orders are placed with the respective vendors. The

cash disbursement transactions should have to be verified and checked before the

checks are issued to its employees. There may be certain false transactions and

diversion of funds from the business. The payroll system keeps track of its

employees and their working hours. The centralized accounting system makes the

process of decision making easier by preparing appropriate and relevant reports.

Timekeeping Clerk Employee Cards Payroll Department

Tax rate reference file

Employee file

Preparation of Pay Checks

Cash

Disbursemen

t Department

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CASE STUDY – ADAM & CO

Reference list

Bajdor, P. and Grabara, I., 2014. The Role of Information System Flows in Fulfilling

Customers' Individual Orders. Journal of Studies in Social Sciences, 7(2).

Collier, P.M., 2015. Accounting for managers: Interpreting accounting information for

decision making. John Wiley & Sons.

Das, C.P. and Parida, M., 2016. A Study on Cash Management and Determinants of

Cash Holding. Splint International Journal of Professionals, 3(3), p.102.

Donelson, D.C., Ege, M.S. and McInnis, J.M., 2016. Internal control weaknesses and

financial reporting fraud. Auditing: A Journal of Practice & Theory, 36(3), pp.45-69.

Fanning, K., 2015. Benefits of Using a Single‐Account Cash Management

Structure. Journal of Corporate Accounting & Finance, 27(1), pp.35-39.

Galliers, R.D. and Leidner, D.E., 2014. Strategic information management:

challenges and strategies in managing information systems. Routledge.

Herrera, C.A. and Ibeas, A., 2015, June. A simulation model for a Cash

Concentration and Disbursements System. In 2015 23rd Mediterranean Conference

on Control and Automation (MED) (pp. 895-902). IEEE.

Herrera-Cáceres, C.A. and Ibeas, A., 2016, June. Model predictive control for a

revenue account of a cash concentration and disbursements system. In 2016 24th

Mediterranean Conference on Control and Automation (MED)(pp. 118-124). IEEE.

Herrera-Cáceres, C.A. and Ibeas, A., 2016. Model predictive control of cash balance

in a cash concentration and disbursements system. Journal of the Franklin

Institute, 353(18), pp.4885-4923.

Jing, H., 2015. The study on the impact of data storage from accounting information

processing procedure. International Journal of Database Theory and

Application, 8(3), pp.323-332.

Laudon, K.C. and Laudon, J.P., 2016. Management information system. Pearson

Education India.

Mahajan, K., Shukla, S. and Soni, N., 2015. A Review of Computerized Payroll

System. University of Lingaya, Department of Computer Science.

Mancini, D., 2016. Accounting information systems in an open society. Emerging

Trends and Issues. Management Control.

Pan, G. and Seow, P.S., 2016. Preparing accounting graduates for digital revolution:

A critical review of information technology competencies and skills

development. Journal of Education for business, 91(3), pp.166-175.

Patel, F., 2015. Effects of accounting information system on organizational

profitability. International Journal of Research and Analytical Reviews, 2(1), pp.168-

174.

Reference list

Bajdor, P. and Grabara, I., 2014. The Role of Information System Flows in Fulfilling

Customers' Individual Orders. Journal of Studies in Social Sciences, 7(2).

Collier, P.M., 2015. Accounting for managers: Interpreting accounting information for

decision making. John Wiley & Sons.

Das, C.P. and Parida, M., 2016. A Study on Cash Management and Determinants of

Cash Holding. Splint International Journal of Professionals, 3(3), p.102.

Donelson, D.C., Ege, M.S. and McInnis, J.M., 2016. Internal control weaknesses and

financial reporting fraud. Auditing: A Journal of Practice & Theory, 36(3), pp.45-69.

Fanning, K., 2015. Benefits of Using a Single‐Account Cash Management

Structure. Journal of Corporate Accounting & Finance, 27(1), pp.35-39.

Galliers, R.D. and Leidner, D.E., 2014. Strategic information management:

challenges and strategies in managing information systems. Routledge.

Herrera, C.A. and Ibeas, A., 2015, June. A simulation model for a Cash

Concentration and Disbursements System. In 2015 23rd Mediterranean Conference

on Control and Automation (MED) (pp. 895-902). IEEE.

Herrera-Cáceres, C.A. and Ibeas, A., 2016, June. Model predictive control for a

revenue account of a cash concentration and disbursements system. In 2016 24th

Mediterranean Conference on Control and Automation (MED)(pp. 118-124). IEEE.

Herrera-Cáceres, C.A. and Ibeas, A., 2016. Model predictive control of cash balance

in a cash concentration and disbursements system. Journal of the Franklin

Institute, 353(18), pp.4885-4923.

Jing, H., 2015. The study on the impact of data storage from accounting information

processing procedure. International Journal of Database Theory and

Application, 8(3), pp.323-332.

Laudon, K.C. and Laudon, J.P., 2016. Management information system. Pearson

Education India.

Mahajan, K., Shukla, S. and Soni, N., 2015. A Review of Computerized Payroll

System. University of Lingaya, Department of Computer Science.

Mancini, D., 2016. Accounting information systems in an open society. Emerging

Trends and Issues. Management Control.

Pan, G. and Seow, P.S., 2016. Preparing accounting graduates for digital revolution:

A critical review of information technology competencies and skills

development. Journal of Education for business, 91(3), pp.166-175.

Patel, F., 2015. Effects of accounting information system on organizational

profitability. International Journal of Research and Analytical Reviews, 2(1), pp.168-

174.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CASE STUDY – ADAM & CO

Ponisciakova, O., Gogolova, M. and Ivankova, K., 2015. The use of accounting

information system for the management of business costs. Procedia Economics and

Finance, 26, pp.418-422.

Prasad, A. and Green, P., 2015. Organizational competencies and dynamic

accounting information system capability: impact on AIS processes and firm

performance. Journal of Information Systems, 29(3), pp.123-149.

Taiwo, J.N., 2016. EFFECT OF ICT ON ACCOUNTING INFORMATION SYSTEM

AND ORGANIZATIONAL PERFORMANCE: THE APPLICATION OF

INFORMATION AND COMMUNICATION TECHNOLOGY ON ACCOUNTING

INFORMATION SYSTEM. European Journal of Business and Social Sciences, 5(2),

pp.1-15.

Tueffel, H., 2016. Boost the bottom line with accounts payable best

practices. Journal of accountancy, 222(5), p.50.

Upadhaya, B., Munir, R. and Blount, Y., 2014. Association between performance

measurement systems and organizational effectiveness. International Journal of

Operations & Production Management, 34(7), pp.853-875.

Ponisciakova, O., Gogolova, M. and Ivankova, K., 2015. The use of accounting

information system for the management of business costs. Procedia Economics and

Finance, 26, pp.418-422.

Prasad, A. and Green, P., 2015. Organizational competencies and dynamic

accounting information system capability: impact on AIS processes and firm

performance. Journal of Information Systems, 29(3), pp.123-149.

Taiwo, J.N., 2016. EFFECT OF ICT ON ACCOUNTING INFORMATION SYSTEM

AND ORGANIZATIONAL PERFORMANCE: THE APPLICATION OF

INFORMATION AND COMMUNICATION TECHNOLOGY ON ACCOUNTING

INFORMATION SYSTEM. European Journal of Business and Social Sciences, 5(2),

pp.1-15.

Tueffel, H., 2016. Boost the bottom line with accounts payable best

practices. Journal of accountancy, 222(5), p.50.

Upadhaya, B., Munir, R. and Blount, Y., 2014. Association between performance

measurement systems and organizational effectiveness. International Journal of

Operations & Production Management, 34(7), pp.853-875.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.