Holmes Institute HA2042: Case Study Analysis of Adam & Co's Systems

VerifiedAdded on 2022/12/27

|14

|2935

|77

Case Study

AI Summary

This case study analyzes the accounting information systems of Adam & Co, focusing on its expenditure cycle. The analysis includes system flowcharts for the purchase, cash disbursement, and payroll systems. The report identifies internal control weaknesses within each system, such as manual processes, lack of verification, and segregation of duties issues. Associated risks, including potential fraud and errors, are also discussed. The purchase system's weaknesses include manual receiving reports and filing delays. The cash disbursement system lacks proper verification of documents and cheques. The payroll system suffers from a lack of segregation of duties and manual voucher preparation. The case study highlights the importance of robust internal controls to mitigate these risks and ensure the accuracy and integrity of financial information.

Running head: CASE STUDY- ADAM & CO

Case study- Adam & Co

Name of the Student

Name of the University

Author Note

Case study- Adam & Co

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CASE STUDY- ADAM & CO

Executive summary:

The paper is prepared to analyze the given case study by addressing the facts identified. In

this paper, risks, process and internal control system of the expenditure cycle of Adam and

Co has been evaluated. The expenditure cycle proceeds in three main systems of the

organization that is purchase system, cash disbursement system and payroll system. Analysis

of such system is done by preparing of flow chart depicting the flow of activities in respective

systems. In the later part of the paper, the weakness in the internal control of each of the

systems described has been demonstrated along with the risks faced by the organization in the

presence of such shortcomings.

Executive summary:

The paper is prepared to analyze the given case study by addressing the facts identified. In

this paper, risks, process and internal control system of the expenditure cycle of Adam and

Co has been evaluated. The expenditure cycle proceeds in three main systems of the

organization that is purchase system, cash disbursement system and payroll system. Analysis

of such system is done by preparing of flow chart depicting the flow of activities in respective

systems. In the later part of the paper, the weakness in the internal control of each of the

systems described has been demonstrated along with the risks faced by the organization in the

presence of such shortcomings.

CASE STUDY- ADAM & CO

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................2

System flow chart of purchase system:......................................................................................2

System flow chart of cash disbursement system:.......................................................................2

System flow chart of payroll system:.........................................................................................2

Identifying the internal control weakness in the system and its associated risks:.....................2

Conclusion:................................................................................................................................2

Reference list:.............................................................................................................................3

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................2

System flow chart of purchase system:......................................................................................2

System flow chart of cash disbursement system:.......................................................................2

System flow chart of payroll system:.........................................................................................2

Identifying the internal control weakness in the system and its associated risks:.....................2

Conclusion:................................................................................................................................2

Reference list:.............................................................................................................................3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CASE STUDY- ADAM & CO

Introduction:

The report is prepared to evaluate the risks, process and internal control of the

expenditure cycle of the company named Adam & Co illustrated in the case study. Evaluation

of the risks and internal control system of the expenditure cycle is done by analyzing the facts

presented in the case study. Discussion includes evaluating the purchase system, cash

disbursement system and the payroll system of Adam & Co and the analysis of all such

systems are done by drawing a system flow chart. Such system flowchart helps in the

identification of different elements in the process and understanding the interrelationships

between several steps of the system (Libby 2017). Later part of the report demonstrates the

description of the weakness of the internal control system and the risks associated with each

system.

Discussion:

System flow chart of purchase system:

Depletion of inventories is done by the firm by transferring raw materials in the

production process and the finished goods are sold to the customers. The process of purchase

by the purchasing clerk of Adam & Co is initiated when the inventory is dropped to a

predetermined level. The procedures of determining the inventory varies from one firm to

another firm and for each of the items of inventory, clerk purchase separate purchase order

recognition. The procedures of purchase involves identifying the needs of inventory, placing

the order, receiving the order and recognition of liability in the form of account payable.

Inventory is monitored and controlled by the clerk and after then inventory has fallen to a

predetermined reorder level, then a digital purchase order is prepared by clerk by selecting

valid vendor file (Appelbaum et al. 2017). When preparing digital purchase order, two hard

Introduction:

The report is prepared to evaluate the risks, process and internal control of the

expenditure cycle of the company named Adam & Co illustrated in the case study. Evaluation

of the risks and internal control system of the expenditure cycle is done by analyzing the facts

presented in the case study. Discussion includes evaluating the purchase system, cash

disbursement system and the payroll system of Adam & Co and the analysis of all such

systems are done by drawing a system flow chart. Such system flowchart helps in the

identification of different elements in the process and understanding the interrelationships

between several steps of the system (Libby 2017). Later part of the report demonstrates the

description of the weakness of the internal control system and the risks associated with each

system.

Discussion:

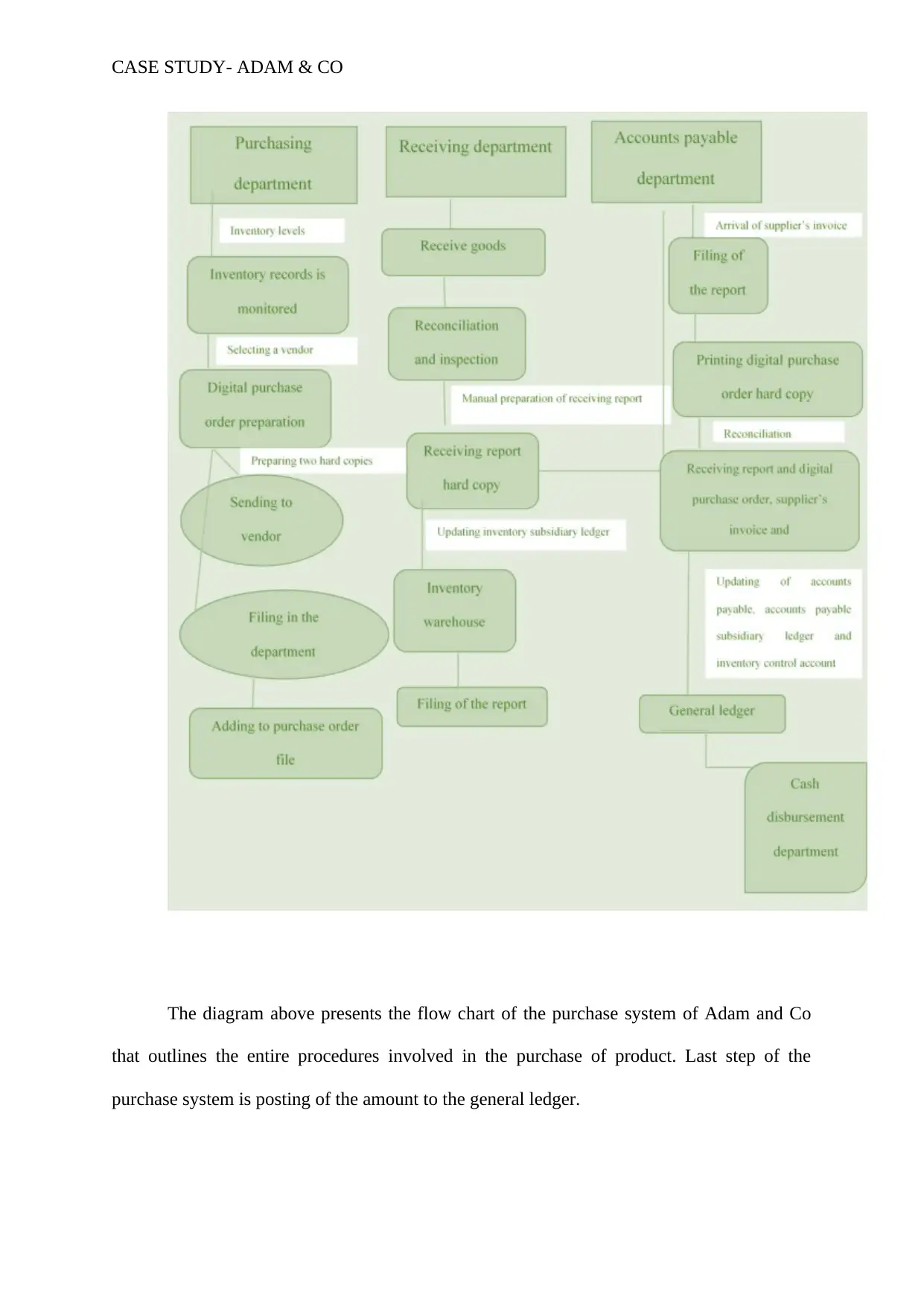

System flow chart of purchase system:

Depletion of inventories is done by the firm by transferring raw materials in the

production process and the finished goods are sold to the customers. The process of purchase

by the purchasing clerk of Adam & Co is initiated when the inventory is dropped to a

predetermined level. The procedures of determining the inventory varies from one firm to

another firm and for each of the items of inventory, clerk purchase separate purchase order

recognition. The procedures of purchase involves identifying the needs of inventory, placing

the order, receiving the order and recognition of liability in the form of account payable.

Inventory is monitored and controlled by the clerk and after then inventory has fallen to a

predetermined reorder level, then a digital purchase order is prepared by clerk by selecting

valid vendor file (Appelbaum et al. 2017). When preparing digital purchase order, two hard

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CASE STUDY- ADAM & CO

copies is prepared by clerk, of which one copy is sent to purchasing department and other

copy is send to the vendor. After this, purchase recognition is send to the purchasing

department. Purchase order is prepared for the valid vendor that has been identified. A

separate purchase recognition is prepared for each inventory and for a given vendor, there can

be multiple purchase recognition and such purchase recognized is combined to form a single

purchase order. After placing the purchase order, goods are received by the receiving

department and the goods received reconciled by the receiving clerk against the packing slip

and purchase order. Two copies of receiving reports are prepared by the clerk and one copy is

send to the inventory warehouse and other is send to the accounts payable department. The

accounts payable clerk reconcile three documents after receiving the invoice. Three accounts

are updated by the clerk that is the account payable clerk, digital accounts payable subsidiary

ledger and inventory control account in the form of general ledger. After these three

documents are prepared, receiving report, invoice and purchase order is send by the clerk to

the cash disbursement department. A journal voucher is received by the general ledger

function from the accounts payable department and account summary is generated from

inventory control (Quinn and Strauss 2017). The posting of approved journal voucher to the

file of journal voucher and the purchase phase of expenditure cycle is completed with this

step.

copies is prepared by clerk, of which one copy is sent to purchasing department and other

copy is send to the vendor. After this, purchase recognition is send to the purchasing

department. Purchase order is prepared for the valid vendor that has been identified. A

separate purchase recognition is prepared for each inventory and for a given vendor, there can

be multiple purchase recognition and such purchase recognized is combined to form a single

purchase order. After placing the purchase order, goods are received by the receiving

department and the goods received reconciled by the receiving clerk against the packing slip

and purchase order. Two copies of receiving reports are prepared by the clerk and one copy is

send to the inventory warehouse and other is send to the accounts payable department. The

accounts payable clerk reconcile three documents after receiving the invoice. Three accounts

are updated by the clerk that is the account payable clerk, digital accounts payable subsidiary

ledger and inventory control account in the form of general ledger. After these three

documents are prepared, receiving report, invoice and purchase order is send by the clerk to

the cash disbursement department. A journal voucher is received by the general ledger

function from the accounts payable department and account summary is generated from

inventory control (Quinn and Strauss 2017). The posting of approved journal voucher to the

file of journal voucher and the purchase phase of expenditure cycle is completed with this

step.

CASE STUDY- ADAM & CO

The diagram above presents the flow chart of the purchase system of Adam and Co

that outlines the entire procedures involved in the purchase of product. Last step of the

purchase system is posting of the amount to the general ledger.

The diagram above presents the flow chart of the purchase system of Adam and Co

that outlines the entire procedures involved in the purchase of product. Last step of the

purchase system is posting of the amount to the general ledger.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CASE STUDY- ADAM & CO

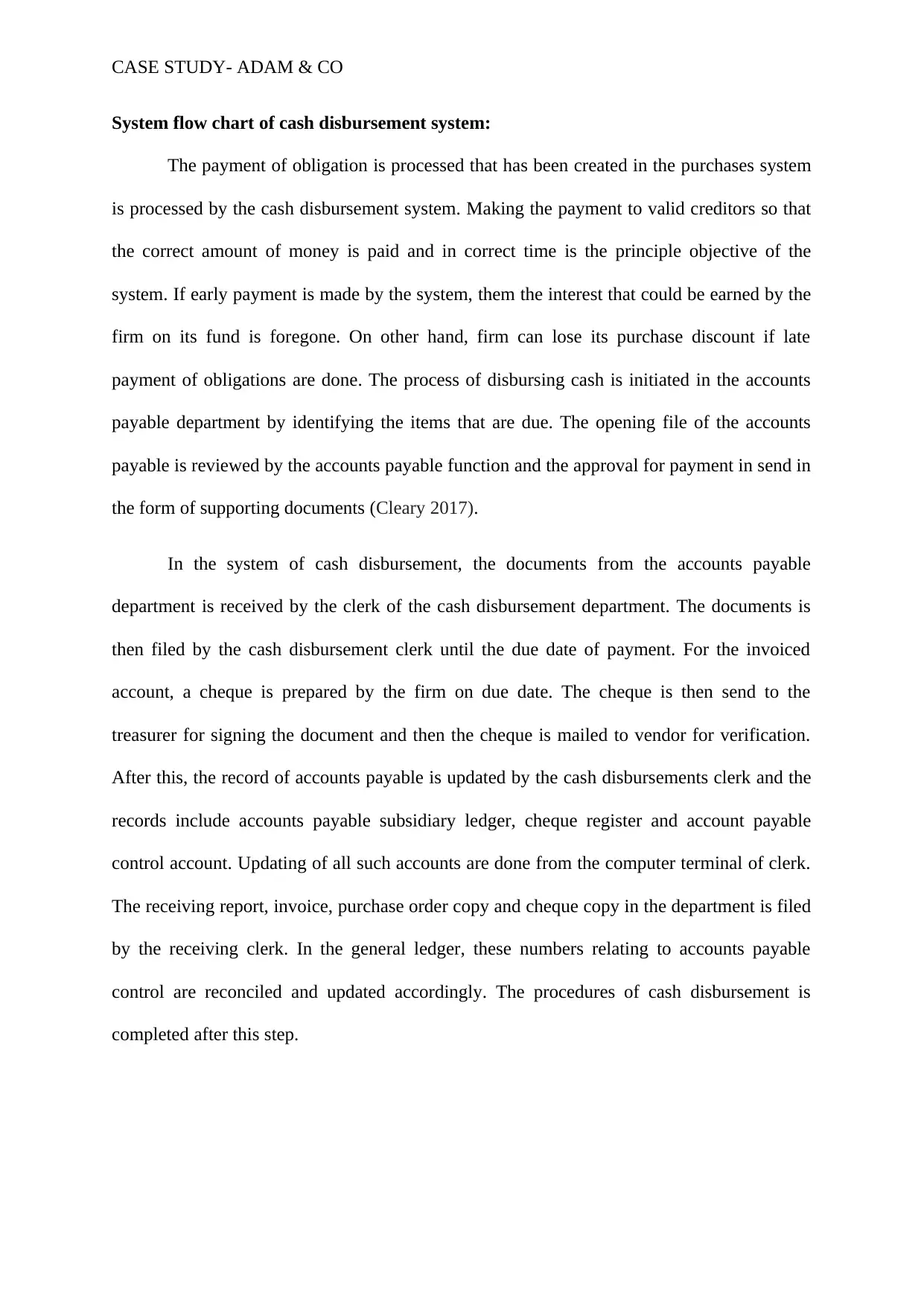

System flow chart of cash disbursement system:

The payment of obligation is processed that has been created in the purchases system

is processed by the cash disbursement system. Making the payment to valid creditors so that

the correct amount of money is paid and in correct time is the principle objective of the

system. If early payment is made by the system, them the interest that could be earned by the

firm on its fund is foregone. On other hand, firm can lose its purchase discount if late

payment of obligations are done. The process of disbursing cash is initiated in the accounts

payable department by identifying the items that are due. The opening file of the accounts

payable is reviewed by the accounts payable function and the approval for payment in send in

the form of supporting documents (Cleary 2017).

In the system of cash disbursement, the documents from the accounts payable

department is received by the clerk of the cash disbursement department. The documents is

then filed by the cash disbursement clerk until the due date of payment. For the invoiced

account, a cheque is prepared by the firm on due date. The cheque is then send to the

treasurer for signing the document and then the cheque is mailed to vendor for verification.

After this, the record of accounts payable is updated by the cash disbursements clerk and the

records include accounts payable subsidiary ledger, cheque register and account payable

control account. Updating of all such accounts are done from the computer terminal of clerk.

The receiving report, invoice, purchase order copy and cheque copy in the department is filed

by the receiving clerk. In the general ledger, these numbers relating to accounts payable

control are reconciled and updated accordingly. The procedures of cash disbursement is

completed after this step.

System flow chart of cash disbursement system:

The payment of obligation is processed that has been created in the purchases system

is processed by the cash disbursement system. Making the payment to valid creditors so that

the correct amount of money is paid and in correct time is the principle objective of the

system. If early payment is made by the system, them the interest that could be earned by the

firm on its fund is foregone. On other hand, firm can lose its purchase discount if late

payment of obligations are done. The process of disbursing cash is initiated in the accounts

payable department by identifying the items that are due. The opening file of the accounts

payable is reviewed by the accounts payable function and the approval for payment in send in

the form of supporting documents (Cleary 2017).

In the system of cash disbursement, the documents from the accounts payable

department is received by the clerk of the cash disbursement department. The documents is

then filed by the cash disbursement clerk until the due date of payment. For the invoiced

account, a cheque is prepared by the firm on due date. The cheque is then send to the

treasurer for signing the document and then the cheque is mailed to vendor for verification.

After this, the record of accounts payable is updated by the cash disbursements clerk and the

records include accounts payable subsidiary ledger, cheque register and account payable

control account. Updating of all such accounts are done from the computer terminal of clerk.

The receiving report, invoice, purchase order copy and cheque copy in the department is filed

by the receiving clerk. In the general ledger, these numbers relating to accounts payable

control are reconciled and updated accordingly. The procedures of cash disbursement is

completed after this step.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Filing of the documents

Cash disbursement clerk

Preparing a cheque

Invoiced account

Treasurer

Vendor

Sign

Updating payable control

account, cheque register,

subsidiary ledger

Filing the documents

Mail

Receiving

clerk

CASE STUDY- ADAM & CO

The above figure presents the flow of procedures of making payment to the suppliers

after the goods are received by issuing purchase requisition. The receiving department

receives the document from accounts payable department and then a cheque is prepared for

the invoice account. Approved journal voucher is then posted to general ledger along with

sending a copy of cheque to the clerk of cash disbursement.

Cash disbursement clerk

Preparing a cheque

Invoiced account

Treasurer

Vendor

Sign

Updating payable control

account, cheque register,

subsidiary ledger

Filing the documents

Receiving

clerk

CASE STUDY- ADAM & CO

The above figure presents the flow of procedures of making payment to the suppliers

after the goods are received by issuing purchase requisition. The receiving department

receives the document from accounts payable department and then a cheque is prepared for

the invoice account. Approved journal voucher is then posted to general ledger along with

sending a copy of cheque to the clerk of cash disbursement.

CASE STUDY- ADAM & CO

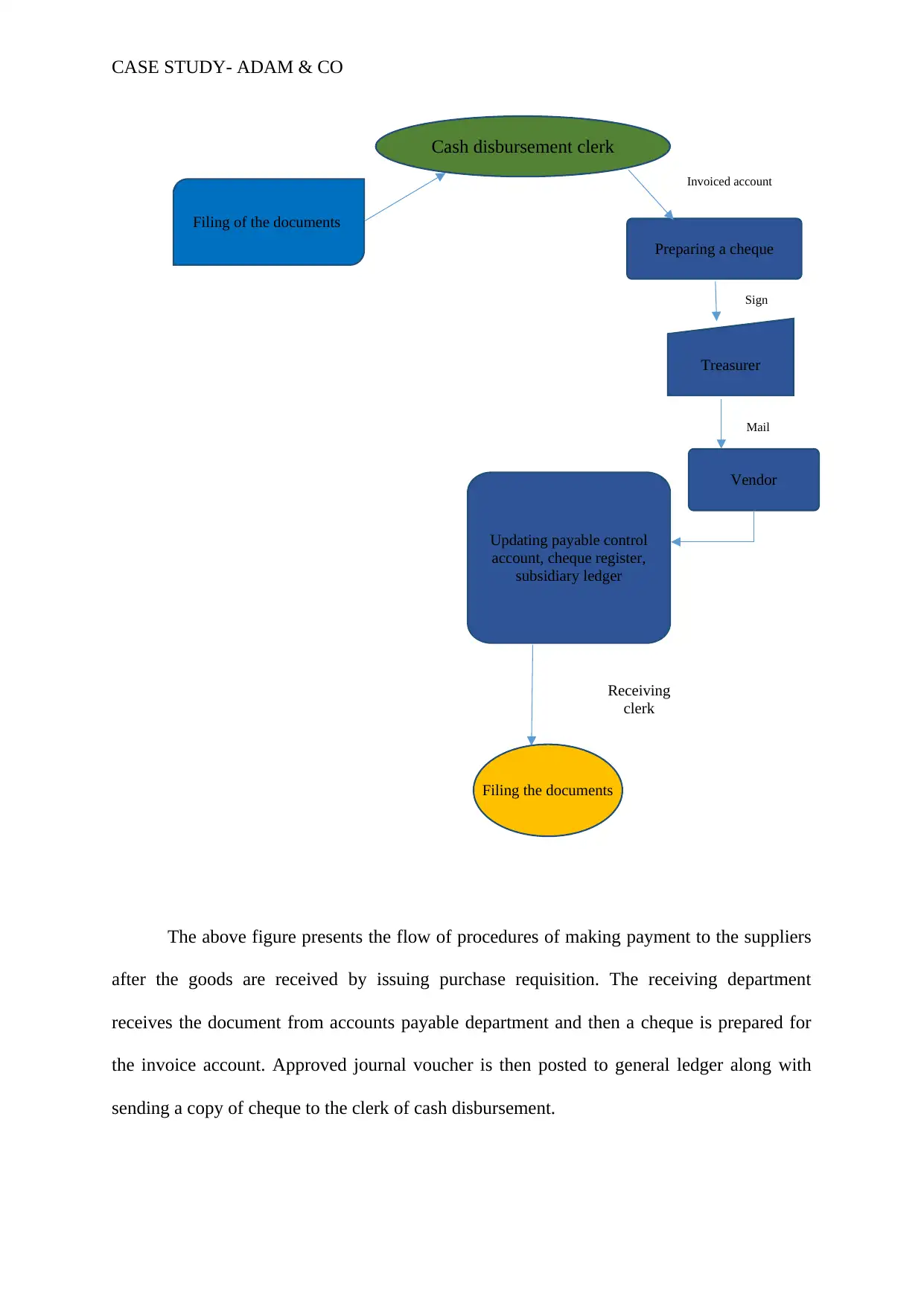

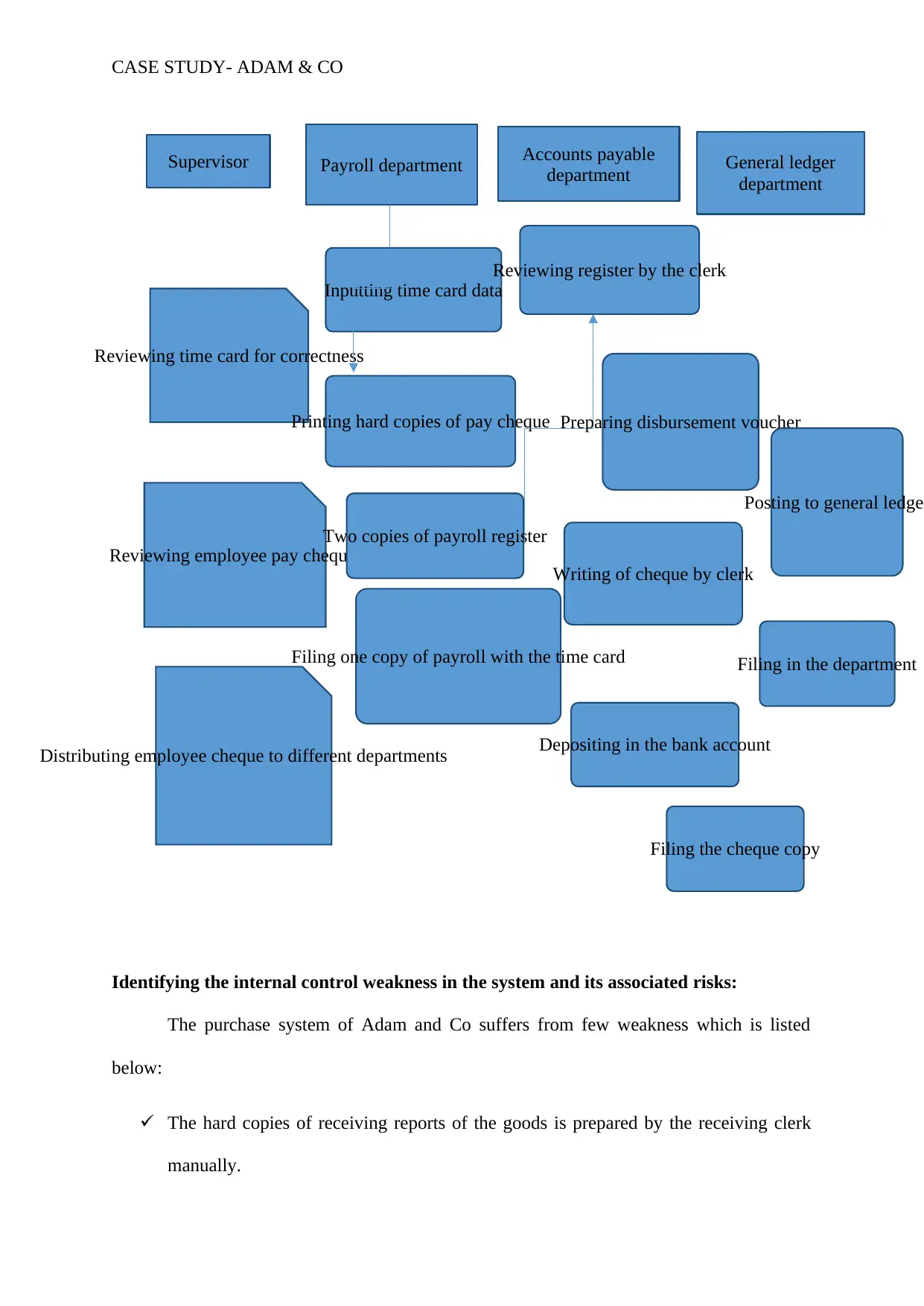

System flow chart of payroll system:

The payroll system of Adam and Co works on a card system as the total hours worked

is recorded on cards. The time card is reviewed for correctness s by the supervisors and at the

end of each week, supervisors are responsible for submitting the card to the payroll

department. The central payroll system has a computer terminal connected to it and the

computer is located in the unit of data processing. In addition to this, the data on the time card

is inputted by the payroll clerk. The hard copies of the pay cheque is printed by the clerk of

processing department and in addition to printing of hard copies of cheque, clerk is also

responsible for printing two copies of payroll register and thereafter positing to digital

employee records is done. The time card is filed in the payroll department by the payroll

clerk and several supervisors review the employee pay cheque when it is send by payroll

clerk. The employee pay cheque is then distributed to the employees of respective

departments. One copy of payroll register is send by the payroll clerk to accounts payable

department and other copy is send to the payroll department. The payroll register is reviewed

by the accounts payable clerk and he is also responsible for preparing the disbursement

voucher. Accounts payable clerk is also responsible for writing the cheque for the entire

payroll and depositing in the account of the bank along with filing the cheque copy in the

accounts department (Chalmers et al. 2019). General ledger department receives the payroll

register and the voucher. After this is done, another duty of accounts payable clerk is to post

the general ledger, voucher filing and payroll register to the department.

System flow chart of payroll system:

The payroll system of Adam and Co works on a card system as the total hours worked

is recorded on cards. The time card is reviewed for correctness s by the supervisors and at the

end of each week, supervisors are responsible for submitting the card to the payroll

department. The central payroll system has a computer terminal connected to it and the

computer is located in the unit of data processing. In addition to this, the data on the time card

is inputted by the payroll clerk. The hard copies of the pay cheque is printed by the clerk of

processing department and in addition to printing of hard copies of cheque, clerk is also

responsible for printing two copies of payroll register and thereafter positing to digital

employee records is done. The time card is filed in the payroll department by the payroll

clerk and several supervisors review the employee pay cheque when it is send by payroll

clerk. The employee pay cheque is then distributed to the employees of respective

departments. One copy of payroll register is send by the payroll clerk to accounts payable

department and other copy is send to the payroll department. The payroll register is reviewed

by the accounts payable clerk and he is also responsible for preparing the disbursement

voucher. Accounts payable clerk is also responsible for writing the cheque for the entire

payroll and depositing in the account of the bank along with filing the cheque copy in the

accounts department (Chalmers et al. 2019). General ledger department receives the payroll

register and the voucher. After this is done, another duty of accounts payable clerk is to post

the general ledger, voucher filing and payroll register to the department.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Supervisor Payroll department Accounts payable

department General ledger

department

Reviewing time card for correctness

Reviewing employee pay cheque

Distributing employee cheque to different departments

Inputting time card data

Printing hard copies of pay cheque

Two copies of payroll register

Filing one copy of payroll with the time card

Reviewing register by the clerk

Preparing disbursement voucher

Writing of cheque by clerk

Depositing in the bank account

Filing the cheque copy

Posting to general ledge

Filing in the department

CASE STUDY- ADAM & CO

Identifying the internal control weakness in the system and its associated risks:

The purchase system of Adam and Co suffers from few weakness which is listed

below:

The hard copies of receiving reports of the goods is prepared by the receiving clerk

manually.

department General ledger

department

Reviewing time card for correctness

Reviewing employee pay cheque

Distributing employee cheque to different departments

Inputting time card data

Printing hard copies of pay cheque

Two copies of payroll register

Filing one copy of payroll with the time card

Reviewing register by the clerk

Preparing disbursement voucher

Writing of cheque by clerk

Depositing in the bank account

Filing the cheque copy

Posting to general ledge

Filing in the department

CASE STUDY- ADAM & CO

Identifying the internal control weakness in the system and its associated risks:

The purchase system of Adam and Co suffers from few weakness which is listed

below:

The hard copies of receiving reports of the goods is prepared by the receiving clerk

manually.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CASE STUDY- ADAM & CO

The accounts payable clerk files the receiving report until the time when the invoice

of supplier arrives. Therefore, filing of the copy of receiving report seems to be time

consuming.

From the above two points identified, it can be inferred that the company has poor

record keeping for the intakes, request and needs of the goods. It is observed that the

appropriateness of the transaction is not questioned by the subordinate staffs. In addition to

this, the manual preparation of hard copy of receiving report by the receiving clerk would

increase the probability of occurrence of the fraud as the total quantities of goods received

might not be entered manually (Asatiani et al. 2019). This also increase the chance of manual

error and thereby weakens the internal control of the purchase system.

The internal control of cash disbursement system of Adam and Co has been evaluated

in terms of its effectiveness and it has been ascertained that:

The system of cash disbursement suffers from few shortcomings as there is no

adequate verification of the documents received.

Moreover, the cheque prepared by the clerk are not verified by the treasurer before

signing and mailing it to the vendor (Mahama et al. 2016).

This increases the probability of the occurrence of fraud as the figures on the cheque

might be misappropriate. There should be a centralized computer system so that any errors or

fraud activities can be traced automatically and leaving no room for conducting the fraud

(Frazer 2016).

The payroll system of Adam and Co also suffers from few weakness that are listed below:

It can be seen that the disbursement voucher is manually prepared by the account

payable clerk. In addition to this, the process of data which includes inputting of the

time card data, printing hard copies of the payroll register and cheque and posting to

The accounts payable clerk files the receiving report until the time when the invoice

of supplier arrives. Therefore, filing of the copy of receiving report seems to be time

consuming.

From the above two points identified, it can be inferred that the company has poor

record keeping for the intakes, request and needs of the goods. It is observed that the

appropriateness of the transaction is not questioned by the subordinate staffs. In addition to

this, the manual preparation of hard copy of receiving report by the receiving clerk would

increase the probability of occurrence of the fraud as the total quantities of goods received

might not be entered manually (Asatiani et al. 2019). This also increase the chance of manual

error and thereby weakens the internal control of the purchase system.

The internal control of cash disbursement system of Adam and Co has been evaluated

in terms of its effectiveness and it has been ascertained that:

The system of cash disbursement suffers from few shortcomings as there is no

adequate verification of the documents received.

Moreover, the cheque prepared by the clerk are not verified by the treasurer before

signing and mailing it to the vendor (Mahama et al. 2016).

This increases the probability of the occurrence of fraud as the figures on the cheque

might be misappropriate. There should be a centralized computer system so that any errors or

fraud activities can be traced automatically and leaving no room for conducting the fraud

(Frazer 2016).

The payroll system of Adam and Co also suffers from few weakness that are listed below:

It can be seen that the disbursement voucher is manually prepared by the account

payable clerk. In addition to this, the process of data which includes inputting of the

time card data, printing hard copies of the payroll register and cheque and posting to

CASE STUDY- ADAM & CO

the record are all done by account payable clerk. Therefore, there is a lack of

segregation of duties in the payroll department.

There is manual preparation of disbursement voucher that might increase the chances

of occurrence of error and cause others to indulge in conducting some fraudulent

activities (Huerta and Jensen 2017).

The payroll system of the company is suffering from monitoring issue as there is lack

of monitoring of the transactions and preparation of documents. Hence, the reliability and

accuracy of the accounting records become doubtful. In addition to this, the procedure of

documentation is not well established and this might increase the occurrence of errors and

missing of relevant files for verifying the records of transaction (Guragai et al. 2015).

Conclusion:

The report prepared above analyzed the risks and the process of the internal control

system of expenditure cycle of Adam and Co. In this regard, the three departments that is

purchase system, cash disbursement system and payroll system has been evaluated for its

effectiveness. It has been ascertained from the analysis of the different systems of the

company that the internal control suffers from few weakness that might cause the chance of

increasing the fraud activities and commitment of errors by the staff members. One of the

significant weaknesses that has been observed in the purchase and payroll system of the

company is that the staffs are manually engaged in the preparation of reports and voucher.

Such manual recording of the facts comes with the increased chances of human errors and

thereby making the data less reliable and inaccurate. Furthermore, there is absence of the

adequate verification of the documents and accounting record and this increase the risk of

indulging in the fraud activities.

the record are all done by account payable clerk. Therefore, there is a lack of

segregation of duties in the payroll department.

There is manual preparation of disbursement voucher that might increase the chances

of occurrence of error and cause others to indulge in conducting some fraudulent

activities (Huerta and Jensen 2017).

The payroll system of the company is suffering from monitoring issue as there is lack

of monitoring of the transactions and preparation of documents. Hence, the reliability and

accuracy of the accounting records become doubtful. In addition to this, the procedure of

documentation is not well established and this might increase the occurrence of errors and

missing of relevant files for verifying the records of transaction (Guragai et al. 2015).

Conclusion:

The report prepared above analyzed the risks and the process of the internal control

system of expenditure cycle of Adam and Co. In this regard, the three departments that is

purchase system, cash disbursement system and payroll system has been evaluated for its

effectiveness. It has been ascertained from the analysis of the different systems of the

company that the internal control suffers from few weakness that might cause the chance of

increasing the fraud activities and commitment of errors by the staff members. One of the

significant weaknesses that has been observed in the purchase and payroll system of the

company is that the staffs are manually engaged in the preparation of reports and voucher.

Such manual recording of the facts comes with the increased chances of human errors and

thereby making the data less reliable and inaccurate. Furthermore, there is absence of the

adequate verification of the documents and accounting record and this increase the risk of

indulging in the fraud activities.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.