HA2042 Case Study: Adam & Co - Expenditure System Analysis Report

VerifiedAdded on 2022/11/03

|12

|2543

|222

Case Study

AI Summary

This case study examines the expenditure cycle of Adam & Co, a Perth-based wholesaler, focusing on its purchase, cash disbursement, and payroll systems. The analysis identifies significant internal control weaknesses within these systems, including a lack of purchase approval authority, inadequate vendor surveillance, and insufficient segregation of duties. The report highlights potential risks such as financial losses, fraud, and reputational damage. The study emphasizes the need for regular audits to mitigate these risks and improve the company's financial accountability. The weaknesses in the cash disbursement system include lack of document verification and cheque review, and the payroll system is subject to risks from manual timecard systems and lack of payroll preview. The study concludes that addressing these weaknesses is crucial for the financial health and integrity of Adam & Co.

HA2042

Case Study – Adam & Co

Student name

Student Id

Case Study – Adam & Co

Student name

Student Id

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

TABLE OF CONTENTS

TOPIC PAGE NUMBER

Executive summary 2

Introduction 2-3

System flowchart of purchases system 2

Internal control weaknesses in the Purchase

system

4-5

System flowchart of cash disbursement system 6

Internal control weaknesses in the cash

disbursement system

7

System flowchart of payroll system 8

Internal control weaknesses in the payroll

system

9

Conclusion 10

References 11

TABLE OF CONTENTS

TOPIC PAGE NUMBER

Executive summary 2

Introduction 2-3

System flowchart of purchases system 2

Internal control weaknesses in the Purchase

system

4-5

System flowchart of cash disbursement system 6

Internal control weaknesses in the cash

disbursement system

7

System flowchart of payroll system 8

Internal control weaknesses in the payroll

system

9

Conclusion 10

References 11

2

EXECUTIVE SUMMARY

A Perth-based wholesaler of industrial supplies, Adam & Co, outsources its inventories from the

manufacturers in countries such as China, Thailand and Vietnam. Being a business Analyst, I

have been given the task of analyzing the expenditure cycle of the company. The company’s

expenses are operated using a centralized accounting system software with the networking

terminals at different locations. Purchasing clerk, receivable clerk and accounts payable clerk are

included in the purchase system of the company for deliberately keeping an eye on the overall

process, that is, from checking the inventory to updating accounts and ledgers, preparing

company reports and sending it to cash disbursement department where the clerk would be held

responsible for keeping checks and updating systems. The whole payroll process in accounts

payable department and the payroll department are operated under the surveillance of the clerks.

A close observance of the weaknesses in the internal control of the expenditure systems

determines the risks associated, which generally includes financial losses, debt accumulation,

reputation loss etc. which are normally incidental to a business.

INTRODUCTION

The expenditure at Adam & Co, is carried along using a centralized accounting system with

networking terminal software at different locations. There are specific systems installed with

respect to purchase, cash disbursement and payroll functions which are followed as per the

company policies and regulations. On keeping a close track of the processes, it is observed that

all the three exhibited expenditure processes primarily including internal control weaknesses

needs to be removed by conducting regular and random audits.

The report starts with a review of the literature stating the important internal control techniques

and benefits of conducting audits. This report also lays down to identify the internal control

weaknesses in each of the three expenditure systems and the risk associated with those

weaknesses.

Zhang, Zhou and Zhou (2007) defined internal control as “a process, effected by an

entity's board of directors, management and other personnel, designed to provide

reasonable assurance regarding the achievement of objectives”.

2 | Page

EXECUTIVE SUMMARY

A Perth-based wholesaler of industrial supplies, Adam & Co, outsources its inventories from the

manufacturers in countries such as China, Thailand and Vietnam. Being a business Analyst, I

have been given the task of analyzing the expenditure cycle of the company. The company’s

expenses are operated using a centralized accounting system software with the networking

terminals at different locations. Purchasing clerk, receivable clerk and accounts payable clerk are

included in the purchase system of the company for deliberately keeping an eye on the overall

process, that is, from checking the inventory to updating accounts and ledgers, preparing

company reports and sending it to cash disbursement department where the clerk would be held

responsible for keeping checks and updating systems. The whole payroll process in accounts

payable department and the payroll department are operated under the surveillance of the clerks.

A close observance of the weaknesses in the internal control of the expenditure systems

determines the risks associated, which generally includes financial losses, debt accumulation,

reputation loss etc. which are normally incidental to a business.

INTRODUCTION

The expenditure at Adam & Co, is carried along using a centralized accounting system with

networking terminal software at different locations. There are specific systems installed with

respect to purchase, cash disbursement and payroll functions which are followed as per the

company policies and regulations. On keeping a close track of the processes, it is observed that

all the three exhibited expenditure processes primarily including internal control weaknesses

needs to be removed by conducting regular and random audits.

The report starts with a review of the literature stating the important internal control techniques

and benefits of conducting audits. This report also lays down to identify the internal control

weaknesses in each of the three expenditure systems and the risk associated with those

weaknesses.

Zhang, Zhou and Zhou (2007) defined internal control as “a process, effected by an

entity's board of directors, management and other personnel, designed to provide

reasonable assurance regarding the achievement of objectives”.

2 | Page

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

The large private companies in Australia, are forced to conduct the audits (Carey, Simnett and

Tanewski, 2000) On the contrary, the research has shown that carrying out the voluntary audits

is beneficial to the organisation.

In the assurance of the corporate accountability, auditing forepays primarily giving the accurate

financial report (Carcello and Neal, 2000) and an important governance mechanism (Zhang et

al., 2007).

Blackwell et al. (2008) had laid in their study that 37% of the private firms independantly

audited in the US. Lower interest rates are paid by these firms significantly on rotating the bank

loans than the unaudited firms. Minnis (2011) reported that auditing lowers down the

asymmetry in information by improving the ability of the expected net income for future cash

flows, thereby reducing the firm’s cost of debt with audited financial statements in opposition to

the unaudited financial statements.

At last, the audits of the private company are economically fruitful by giving the lower interest

rates on debt, thereby increasing the credit ratings and always trying to have better access to

credit (Lennox and Pittman, 2011).

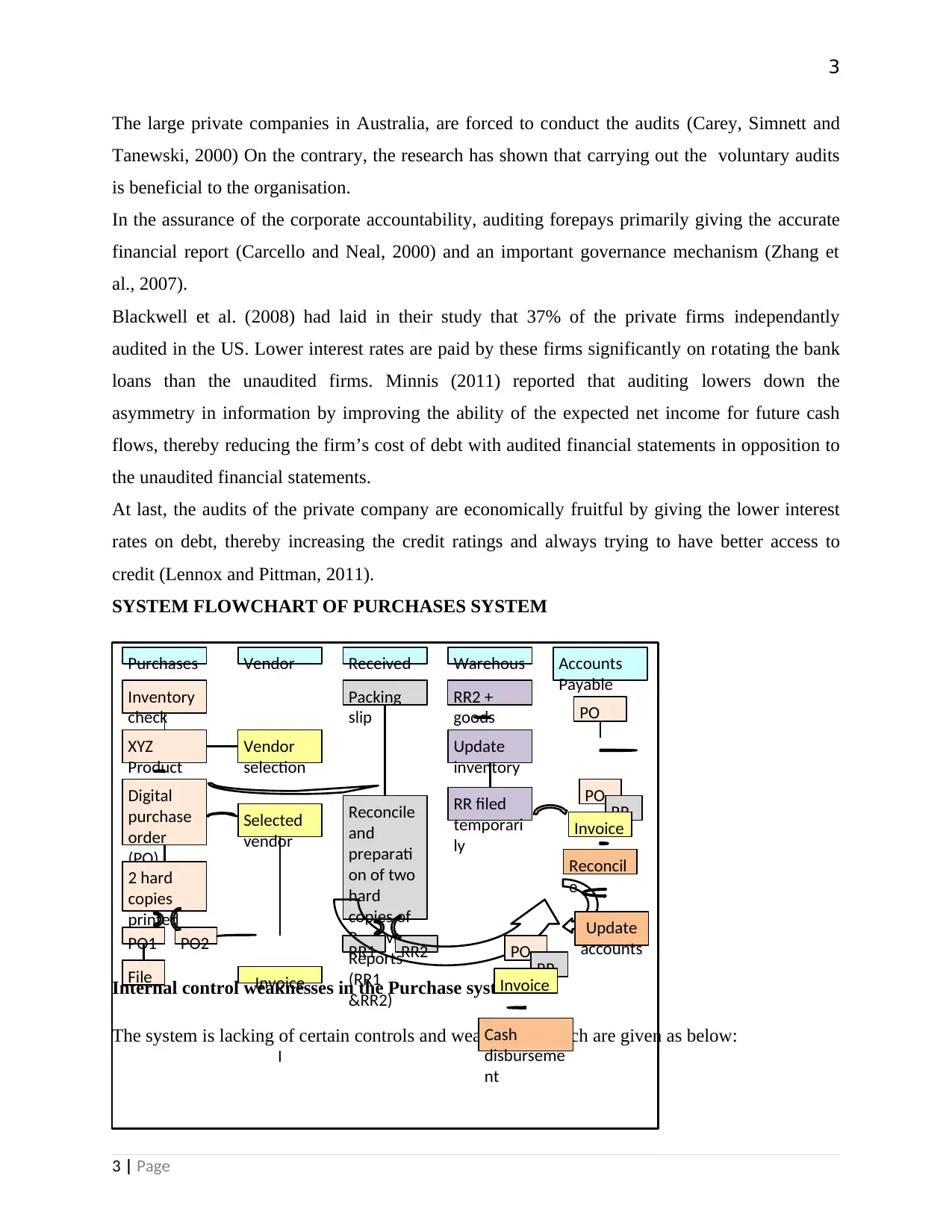

SYSTEM FLOWCHART OF PURCHASES SYSTEM

Internal control weaknesses in the Purchase system

The system is lacking of certain controls and weaknesses which are given as below:

3 | Page

Purchases

Inventory

check

XYZ

Product

required

Vendor Received Warehous

e

Accounts

Payable

Vendor

selection

Digital

purchase

order

(PO)

created2 hard

copies

printed

PO1 PO2

Selected

vendor

File Invoice

I

Packing

slip

Reconcile

and

preparati

on of two

hard

copies of

Receiving

Reports

(RR1

&RR2)

RR1 RR2

RR2 +

goods

Update

inventory

RR filed

temporari

ly

PO

Reconcil

e

PO RR

Invoice

Cash

disburseme

nt

Update

accounts

PO RR

Invoice

The large private companies in Australia, are forced to conduct the audits (Carey, Simnett and

Tanewski, 2000) On the contrary, the research has shown that carrying out the voluntary audits

is beneficial to the organisation.

In the assurance of the corporate accountability, auditing forepays primarily giving the accurate

financial report (Carcello and Neal, 2000) and an important governance mechanism (Zhang et

al., 2007).

Blackwell et al. (2008) had laid in their study that 37% of the private firms independantly

audited in the US. Lower interest rates are paid by these firms significantly on rotating the bank

loans than the unaudited firms. Minnis (2011) reported that auditing lowers down the

asymmetry in information by improving the ability of the expected net income for future cash

flows, thereby reducing the firm’s cost of debt with audited financial statements in opposition to

the unaudited financial statements.

At last, the audits of the private company are economically fruitful by giving the lower interest

rates on debt, thereby increasing the credit ratings and always trying to have better access to

credit (Lennox and Pittman, 2011).

SYSTEM FLOWCHART OF PURCHASES SYSTEM

Internal control weaknesses in the Purchase system

The system is lacking of certain controls and weaknesses which are given as below:

3 | Page

Purchases

Inventory

check

XYZ

Product

required

Vendor Received Warehous

e

Accounts

Payable

Vendor

selection

Digital

purchase

order

(PO)

created2 hard

copies

printed

PO1 PO2

Selected

vendor

File Invoice

I

Packing

slip

Reconcile

and

preparati

on of two

hard

copies of

Receiving

Reports

(RR1

&RR2)

RR1 RR2

RR2 +

goods

Update

inventory

RR filed

temporari

ly

PO

Reconcil

e

PO RR

Invoice

Cash

disburseme

nt

Update

accounts

PO RR

Invoice

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

● That there is evident scarcity of the purchase approving authority, which might result in

the expenditure to follow on the unwanted purchase materials, maybe even for the clerk’s

personal usage. There can be theft in the company, both financially and inventorily, due

to this lack of the improper and avoidable expenditures Clearly evident from the

instances of the case study, there is no proper authorized check on the purchases in the

company, which when associated combined with a complete lack of approving authority,

is considered to be an authentic taboo providing a lot more power to the accounts

receivable clerk who can misuse it to order products for personal use or carry out theft in

the name of product purchasing.

● There is no surveillance on the vendors providing competitive prices, better quality

and/or shorter delivery time in the market to compare from the ones associated with the

company. The company might be following the partial laws in which the clerk receives

favors, gifts and/or kickbacks from the supplier for continuous orders. Lot of activities

are maintained under the supervision of many clerks who are illegally taking out the

office goods for use. Various accounts payable clerks controls the selection of vendors,

placement of orders, updating the bills’ file, updating accounts payable subsidiary ledger,

the accounts payable control account and the inventory control account in the general

ledger and many more such services. There is a policy for the receiving clerks to inspect

the goods, match the items against the information in the digital purchase order and the

packing slip, prepares receiving reports, and updates the inventory subsidiary ledger. One

copy of receiving report is received by the accounts payable clerk who filed the report in

the department. All these duties assigned to the accounts payable clerk allows lot of

fraudulent practices to take place each time. For example, receiving and approving the

poor quality products or maybe accepting the products falling short than the numbers

ordered, from the vendors wherein the deal is settled for certain favours or gifts from the

vendors which is kept hidden from the company. This is the reason why duties should be

segregated and reviewed by some other trustworthy person.

An unsupervised purchase system cost heavily to J.M. Smucker Company when one of their

employees. Mark R. Kershey was the chief airplane mechanic in the company who had

submitted false invoices in the name of a fictitious entity called Aircraft Parts Services, Co. to

4 | Page

● That there is evident scarcity of the purchase approving authority, which might result in

the expenditure to follow on the unwanted purchase materials, maybe even for the clerk’s

personal usage. There can be theft in the company, both financially and inventorily, due

to this lack of the improper and avoidable expenditures Clearly evident from the

instances of the case study, there is no proper authorized check on the purchases in the

company, which when associated combined with a complete lack of approving authority,

is considered to be an authentic taboo providing a lot more power to the accounts

receivable clerk who can misuse it to order products for personal use or carry out theft in

the name of product purchasing.

● There is no surveillance on the vendors providing competitive prices, better quality

and/or shorter delivery time in the market to compare from the ones associated with the

company. The company might be following the partial laws in which the clerk receives

favors, gifts and/or kickbacks from the supplier for continuous orders. Lot of activities

are maintained under the supervision of many clerks who are illegally taking out the

office goods for use. Various accounts payable clerks controls the selection of vendors,

placement of orders, updating the bills’ file, updating accounts payable subsidiary ledger,

the accounts payable control account and the inventory control account in the general

ledger and many more such services. There is a policy for the receiving clerks to inspect

the goods, match the items against the information in the digital purchase order and the

packing slip, prepares receiving reports, and updates the inventory subsidiary ledger. One

copy of receiving report is received by the accounts payable clerk who filed the report in

the department. All these duties assigned to the accounts payable clerk allows lot of

fraudulent practices to take place each time. For example, receiving and approving the

poor quality products or maybe accepting the products falling short than the numbers

ordered, from the vendors wherein the deal is settled for certain favours or gifts from the

vendors which is kept hidden from the company. This is the reason why duties should be

segregated and reviewed by some other trustworthy person.

An unsupervised purchase system cost heavily to J.M. Smucker Company when one of their

employees. Mark R. Kershey was the chief airplane mechanic in the company who had

submitted false invoices in the name of a fictitious entity called Aircraft Parts Services, Co. to

4 | Page

5

Smucker from a period of October 1997 to January 2013. His fraudulent activities cost the

company upwards of $4.1 million (Lumenlearning, 2014).

5 | Page

Smucker from a period of October 1997 to January 2013. His fraudulent activities cost the

company upwards of $4.1 million (Lumenlearning, 2014).

5 | Page

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

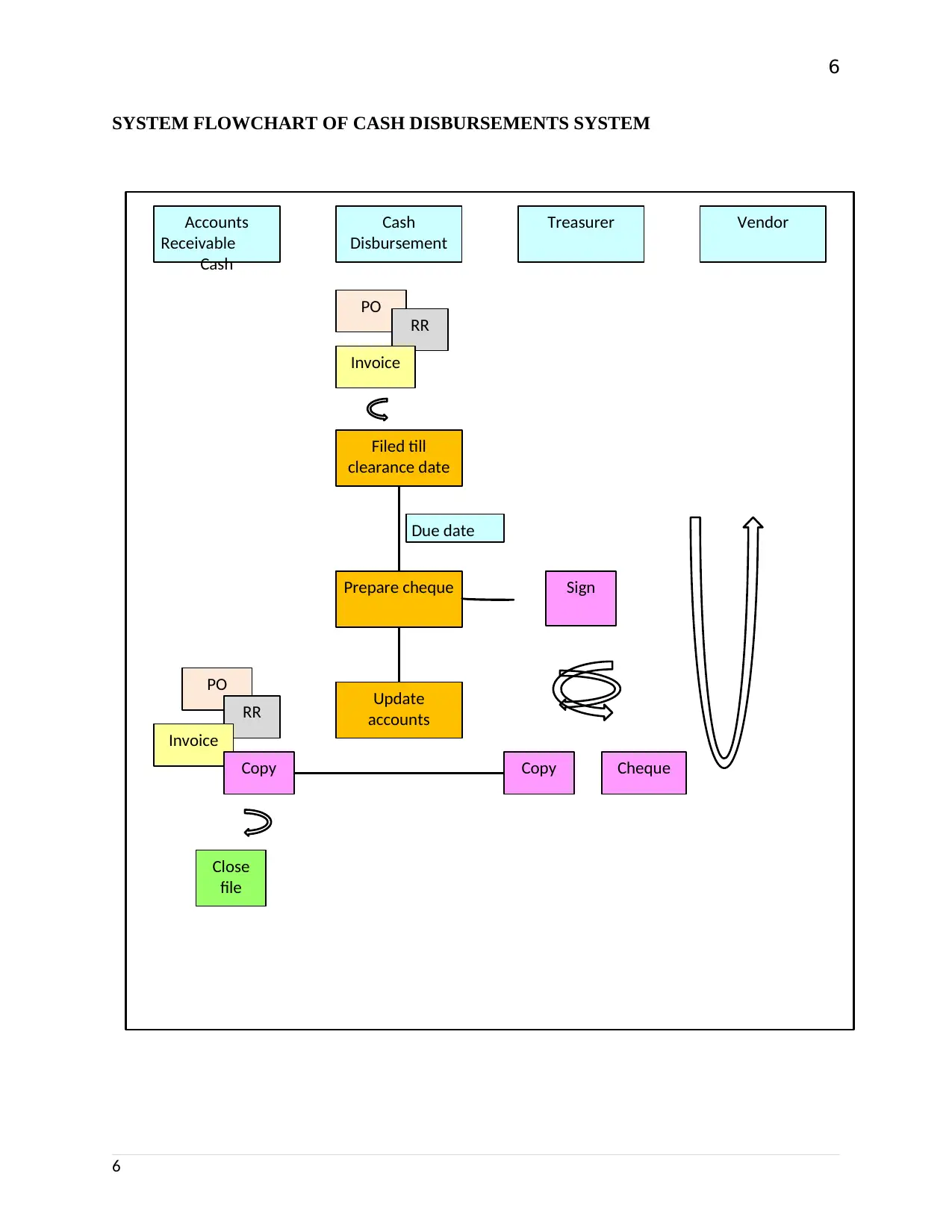

SYSTEM FLOWCHART OF CASH DISBURSEMENTS SYSTEM

6

Accounts

Receivable

Cash

PO

Cash

Disbursement

Treasurer Vendor

RR

Invoice

Filed till

clearance date

Due date

Prepare cheque Sign

Copy Cheque

Update

accounts

PO

RR

Invoice

Copy

Close

file

SYSTEM FLOWCHART OF CASH DISBURSEMENTS SYSTEM

6

Accounts

Receivable

Cash

PO

Cash

Disbursement

Treasurer Vendor

RR

Invoice

Filed till

clearance date

Due date

Prepare cheque Sign

Copy Cheque

Update

accounts

PO

RR

Invoice

Copy

Close

file

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Internal control weaknesses in the cash disbursement system

The difficulties arising out in the cash disbursement system are as detailed below:

● That the documents received from the accounts payable department are not properly

signed and double checked because of which there is generally no accountability of the

actions relating to the cash disbursement. This non-accountability causes serious issues

for the company in the near future since there is no track record found when the

documents are audited at any later date.

● The another problem which creates a nuisance later is that the cheques, prepared by the

cask clerks are not reviewed twice in order to make sure if its correct. In addition, the

treasurer of the company is also receives the cheque duly prepared by the cash clerk

without its supporting documents for keeping track of the transaction when reviewed at

any later date. This ignorance creates chances for forgery or misleading transactions in

the company as there is a wide scope of the clerks, filling in the incorrect information in

the cheque, which could be either intentional or a mistake. Suppose, if the clerk has

erroneously filled in the amount which is less than the actual payable amount, then there

are high chances of deteriorating the vendor-company relationships, and if vice-versa is

done, that is higher is amount is written, then the company would be at a financial loss

only.

The cash disbursement clerk is assigned with a wide range of tasks starting from preparing the

cheque, updating the books of the cheque paid or received register, accounts payable subsidiary

ledger, and the accounts payable control account along with filing invoice, purchase order copy,

receiving report, and cheque copy in the department. This huge responsibilities on signle

employee are always associated with high probability of errors like, he /she may forget to update

the accounts, or may update them incorrectly maybe intentionally or unintentionally, which can

make the financial records appear wrong, confusing and incorrect. Also, there is no review of the

activities of the cash disbursement clerk giving him/her an opportunity to carry out fraudulent

activities.

7

Internal control weaknesses in the cash disbursement system

The difficulties arising out in the cash disbursement system are as detailed below:

● That the documents received from the accounts payable department are not properly

signed and double checked because of which there is generally no accountability of the

actions relating to the cash disbursement. This non-accountability causes serious issues

for the company in the near future since there is no track record found when the

documents are audited at any later date.

● The another problem which creates a nuisance later is that the cheques, prepared by the

cask clerks are not reviewed twice in order to make sure if its correct. In addition, the

treasurer of the company is also receives the cheque duly prepared by the cash clerk

without its supporting documents for keeping track of the transaction when reviewed at

any later date. This ignorance creates chances for forgery or misleading transactions in

the company as there is a wide scope of the clerks, filling in the incorrect information in

the cheque, which could be either intentional or a mistake. Suppose, if the clerk has

erroneously filled in the amount which is less than the actual payable amount, then there

are high chances of deteriorating the vendor-company relationships, and if vice-versa is

done, that is higher is amount is written, then the company would be at a financial loss

only.

The cash disbursement clerk is assigned with a wide range of tasks starting from preparing the

cheque, updating the books of the cheque paid or received register, accounts payable subsidiary

ledger, and the accounts payable control account along with filing invoice, purchase order copy,

receiving report, and cheque copy in the department. This huge responsibilities on signle

employee are always associated with high probability of errors like, he /she may forget to update

the accounts, or may update them incorrectly maybe intentionally or unintentionally, which can

make the financial records appear wrong, confusing and incorrect. Also, there is no review of the

activities of the cash disbursement clerk giving him/her an opportunity to carry out fraudulent

activities.

7

8

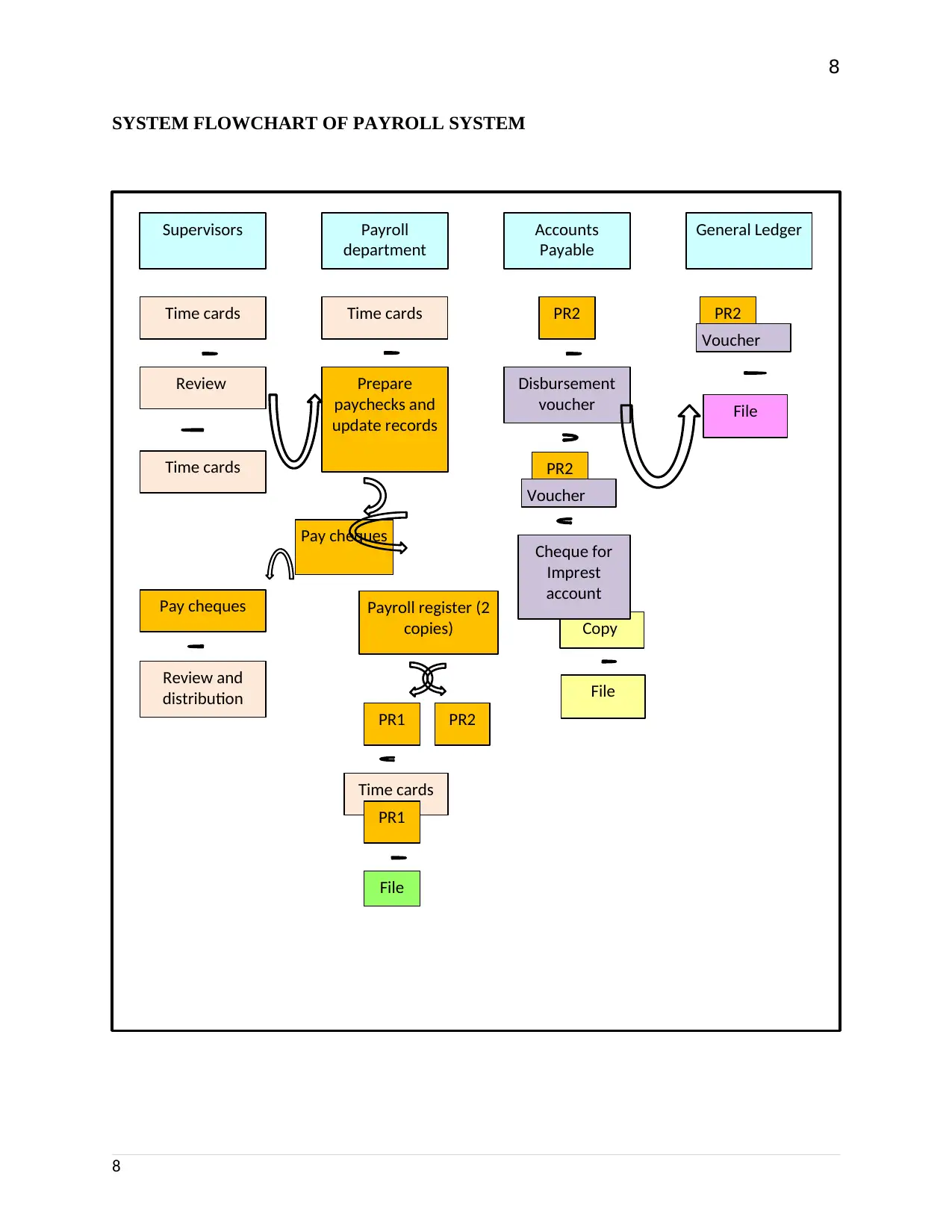

SYSTEM FLOWCHART OF PAYROLL SYSTEM

8

Copy

Supervisors

PR2

Payroll

department

Accounts

Payable

General Ledger

Disbursement

voucher

PR2

Prepare

paychecks and

update records

Voucher

Pay cheques Cheque for

Imprest

account

PR1 PR2

Payroll register (2

copies)

Time cards

Review

Pay cheques

Review and

distribution

File

Time cards

Time cards PR2

Voucher

File

Time cards

PR1

File

SYSTEM FLOWCHART OF PAYROLL SYSTEM

8

Copy

Supervisors

PR2

Payroll

department

Accounts

Payable

General Ledger

Disbursement

voucher

PR2

Prepare

paychecks and

update records

Voucher

Pay cheques Cheque for

Imprest

account

PR1 PR2

Payroll register (2

copies)

Time cards

Review

Pay cheques

Review and

distribution

File

Time cards

Time cards PR2

Voucher

File

Time cards

PR1

File

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

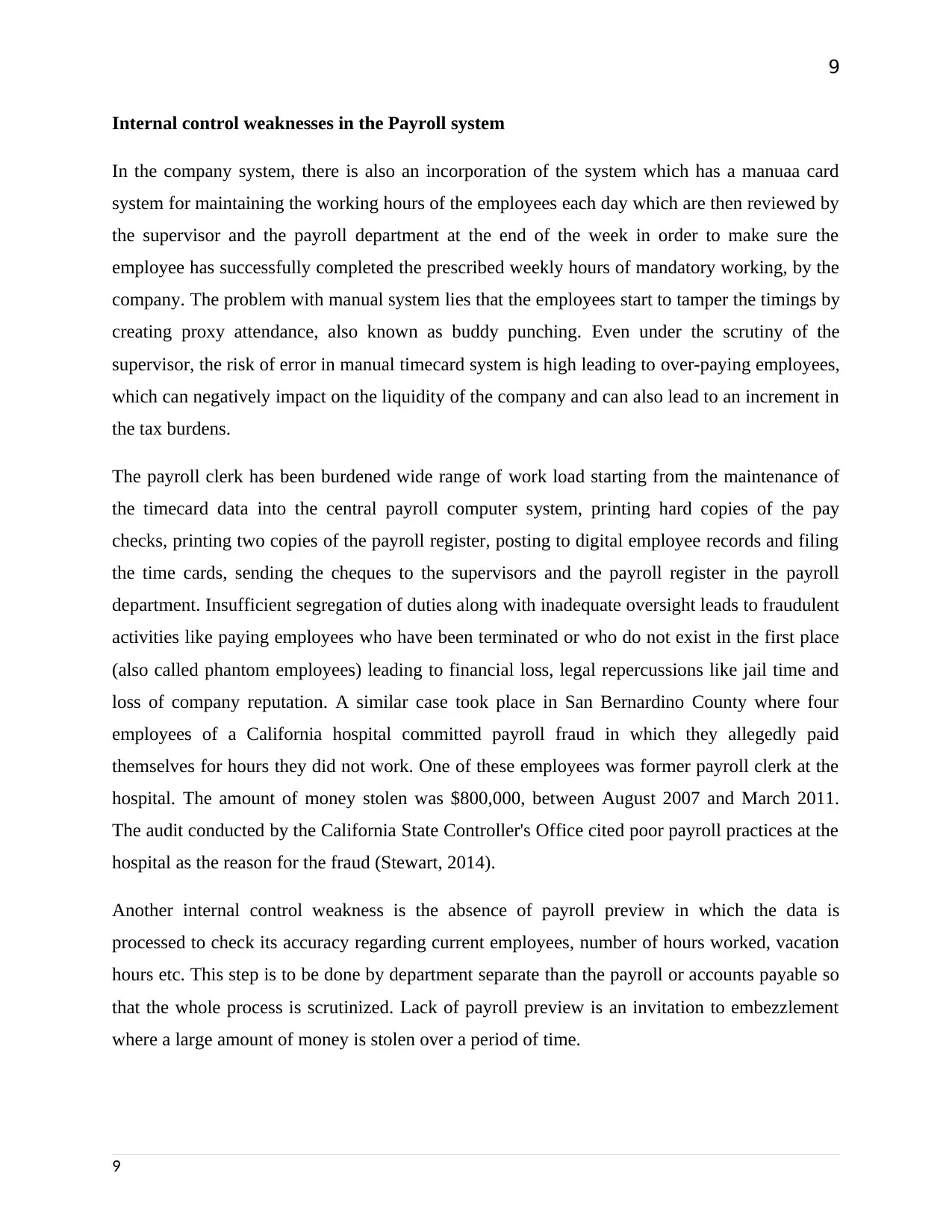

Internal control weaknesses in the Payroll system

In the company system, there is also an incorporation of the system which has a manuaa card

system for maintaining the working hours of the employees each day which are then reviewed by

the supervisor and the payroll department at the end of the week in order to make sure the

employee has successfully completed the prescribed weekly hours of mandatory working, by the

company. The problem with manual system lies that the employees start to tamper the timings by

creating proxy attendance, also known as buddy punching. Even under the scrutiny of the

supervisor, the risk of error in manual timecard system is high leading to over-paying employees,

which can negatively impact on the liquidity of the company and can also lead to an increment in

the tax burdens.

The payroll clerk has been burdened wide range of work load starting from the maintenance of

the timecard data into the central payroll computer system, printing hard copies of the pay

checks, printing two copies of the payroll register, posting to digital employee records and filing

the time cards, sending the cheques to the supervisors and the payroll register in the payroll

department. Insufficient segregation of duties along with inadequate oversight leads to fraudulent

activities like paying employees who have been terminated or who do not exist in the first place

(also called phantom employees) leading to financial loss, legal repercussions like jail time and

loss of company reputation. A similar case took place in San Bernardino County where four

employees of a California hospital committed payroll fraud in which they allegedly paid

themselves for hours they did not work. One of these employees was former payroll clerk at the

hospital. The amount of money stolen was $800,000, between August 2007 and March 2011.

The audit conducted by the California State Controller's Office cited poor payroll practices at the

hospital as the reason for the fraud (Stewart, 2014).

Another internal control weakness is the absence of payroll preview in which the data is

processed to check its accuracy regarding current employees, number of hours worked, vacation

hours etc. This step is to be done by department separate than the payroll or accounts payable so

that the whole process is scrutinized. Lack of payroll preview is an invitation to embezzlement

where a large amount of money is stolen over a period of time.

9

Internal control weaknesses in the Payroll system

In the company system, there is also an incorporation of the system which has a manuaa card

system for maintaining the working hours of the employees each day which are then reviewed by

the supervisor and the payroll department at the end of the week in order to make sure the

employee has successfully completed the prescribed weekly hours of mandatory working, by the

company. The problem with manual system lies that the employees start to tamper the timings by

creating proxy attendance, also known as buddy punching. Even under the scrutiny of the

supervisor, the risk of error in manual timecard system is high leading to over-paying employees,

which can negatively impact on the liquidity of the company and can also lead to an increment in

the tax burdens.

The payroll clerk has been burdened wide range of work load starting from the maintenance of

the timecard data into the central payroll computer system, printing hard copies of the pay

checks, printing two copies of the payroll register, posting to digital employee records and filing

the time cards, sending the cheques to the supervisors and the payroll register in the payroll

department. Insufficient segregation of duties along with inadequate oversight leads to fraudulent

activities like paying employees who have been terminated or who do not exist in the first place

(also called phantom employees) leading to financial loss, legal repercussions like jail time and

loss of company reputation. A similar case took place in San Bernardino County where four

employees of a California hospital committed payroll fraud in which they allegedly paid

themselves for hours they did not work. One of these employees was former payroll clerk at the

hospital. The amount of money stolen was $800,000, between August 2007 and March 2011.

The audit conducted by the California State Controller's Office cited poor payroll practices at the

hospital as the reason for the fraud (Stewart, 2014).

Another internal control weakness is the absence of payroll preview in which the data is

processed to check its accuracy regarding current employees, number of hours worked, vacation

hours etc. This step is to be done by department separate than the payroll or accounts payable so

that the whole process is scrutinized. Lack of payroll preview is an invitation to embezzlement

where a large amount of money is stolen over a period of time.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CONCLUSION

A concrete view of the expenses and the entire expenditure system of the company, can lead to

the recognition of a number of internal control weaknesses which if not considered then and

there might cause serious financial and reputational and goodwill losses to the company.

Auditing in the company is immediately required for balancing the internal weaknesses and also

identifying the total losses suffered which may have been incurred due to the fraudulent practices

being carried out in the company.

10

CONCLUSION

A concrete view of the expenses and the entire expenditure system of the company, can lead to

the recognition of a number of internal control weaknesses which if not considered then and

there might cause serious financial and reputational and goodwill losses to the company.

Auditing in the company is immediately required for balancing the internal weaknesses and also

identifying the total losses suffered which may have been incurred due to the fraudulent practices

being carried out in the company.

10

11

References

1. Blackwell, D.W., Noland, T.R., and Winters, D.B., 2008. The value of auditor assurance:

evidence from loan pricing. Journal of Accounting Research, 36 (1), 57–70.

2. Carey, P., Simnett, R. and Tanewski, G., 2000. Voluntary demand for internal and

external auditing by family businesses. Auditing: a journal of practice & theory, 19(s-1),

pp.37-51.

3. Carcello, J.V. and Neal, T.L., 2000. Audit committee composition and auditor reporting.

The Accounting Review, 75(4), pp.453-467.

4. Lennox, C.S. and Pittman, J.A., 2011. Voluntary audits versus mandatory audits.

Accounting Review, 86 (5), 1655–1678.

5. Lumenlearning (2014). Internal Control Issues and Procedures for Inventory | Financial

Accounting. Available at:

https://courses.lumenlearning.com/suny-finaccounting/chapter/internal-control-issues-

and-procedures-for-inventory/ [Accessed 30 August 2019]

6. Minnis, M. 2011. The value of financial statement verification in debt financing:

evidence from private U.S. firms. Journal of Accounting Research, 49 (2), 457–506.

7. Stewart, A. (2014). Unhealthy Payroll Practices. Internalauditor. Available at:

https://iaonline.theiia.org/unhealthy-payroll-practices [Accessed 29 August 2019]

8. Ucsd.edu. (2017). Internal Controls. Available at:

https://blink.ucsd.edu/finance/accountability/controls/index.html [Accessed 29 August

2019].

9. Zhang, Y., Zhou, J. and Zhou, N., 2007. Audit committee quality, auditor independence,

and internal control weaknesses. Journal of accounting and public policy, 26(3), pp.300-

327.

11

References

1. Blackwell, D.W., Noland, T.R., and Winters, D.B., 2008. The value of auditor assurance:

evidence from loan pricing. Journal of Accounting Research, 36 (1), 57–70.

2. Carey, P., Simnett, R. and Tanewski, G., 2000. Voluntary demand for internal and

external auditing by family businesses. Auditing: a journal of practice & theory, 19(s-1),

pp.37-51.

3. Carcello, J.V. and Neal, T.L., 2000. Audit committee composition and auditor reporting.

The Accounting Review, 75(4), pp.453-467.

4. Lennox, C.S. and Pittman, J.A., 2011. Voluntary audits versus mandatory audits.

Accounting Review, 86 (5), 1655–1678.

5. Lumenlearning (2014). Internal Control Issues and Procedures for Inventory | Financial

Accounting. Available at:

https://courses.lumenlearning.com/suny-finaccounting/chapter/internal-control-issues-

and-procedures-for-inventory/ [Accessed 30 August 2019]

6. Minnis, M. 2011. The value of financial statement verification in debt financing:

evidence from private U.S. firms. Journal of Accounting Research, 49 (2), 457–506.

7. Stewart, A. (2014). Unhealthy Payroll Practices. Internalauditor. Available at:

https://iaonline.theiia.org/unhealthy-payroll-practices [Accessed 29 August 2019]

8. Ucsd.edu. (2017). Internal Controls. Available at:

https://blink.ucsd.edu/finance/accountability/controls/index.html [Accessed 29 August

2019].

9. Zhang, Y., Zhou, J. and Zhou, N., 2007. Audit committee quality, auditor independence,

and internal control weaknesses. Journal of accounting and public policy, 26(3), pp.300-

327.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.