Adam & Co Case Study: Expenditure Cycle, Internal Controls, and Risks

VerifiedAdded on 2022/11/17

|21

|2917

|378

Case Study

AI Summary

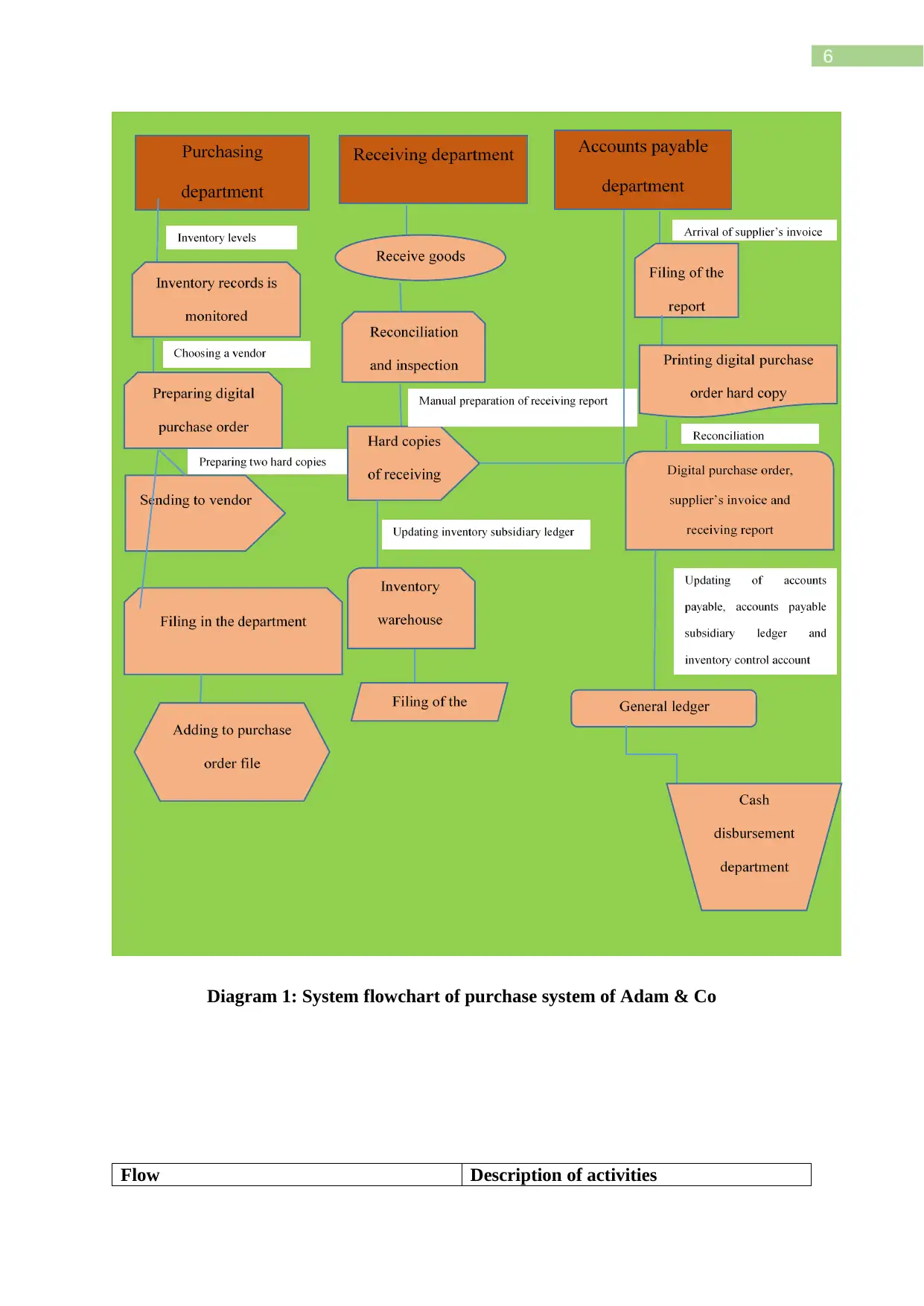

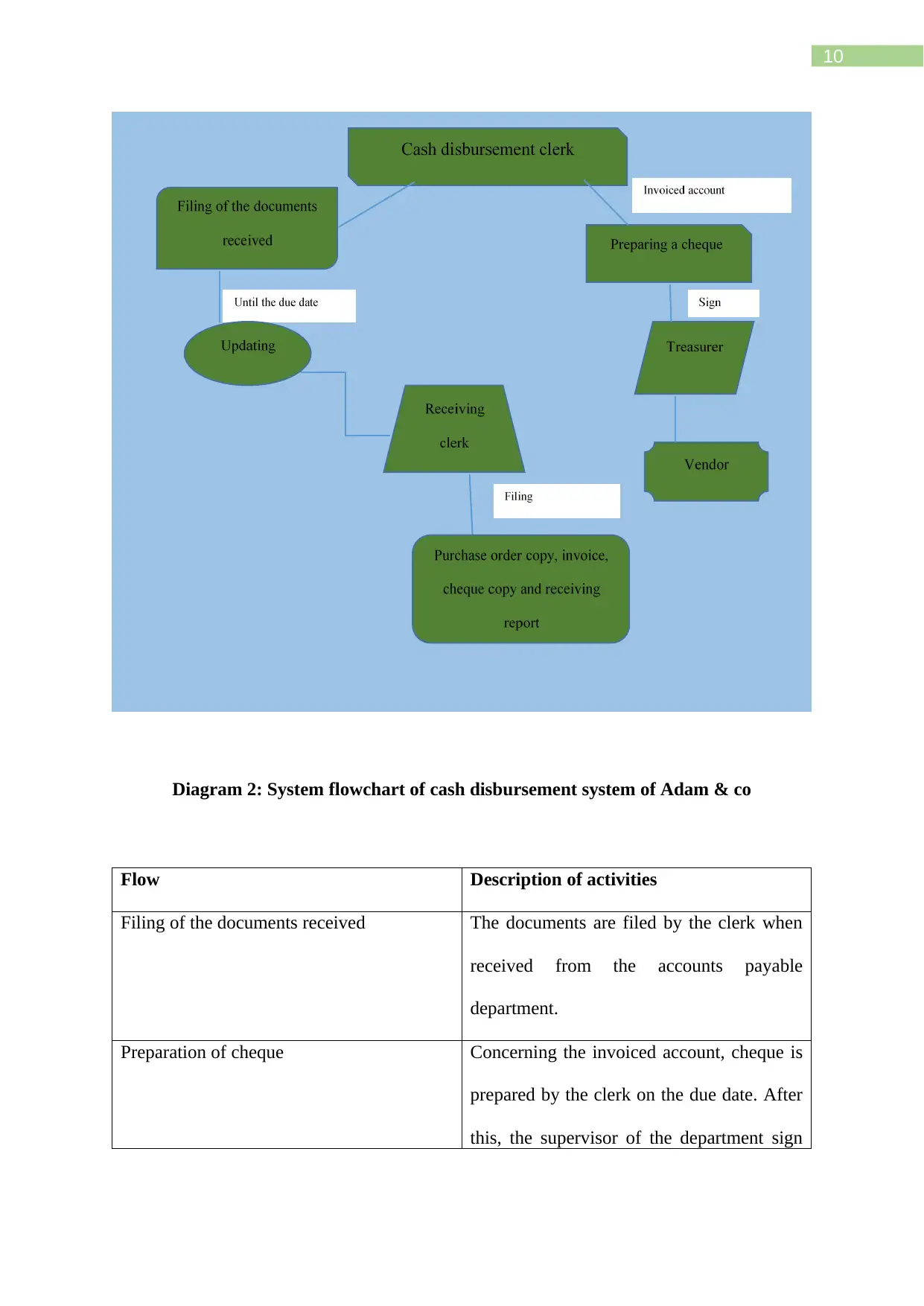

This case study examines Adam & Co, a wholesaler of industrial supplies, and analyzes its expenditure cycle, focusing on purchase, cash disbursement, and payroll systems. The analysis involves creating system flowcharts to illustrate the processes within each system. The purchase system involves steps from need recognition to closing the order, including vendor selection, purchase order preparation, receipt, and reconciliation. The cash disbursement system covers filing documents, cheque preparation, updating documents, and filing. The payroll system encompasses time card information, verification, data input, cheque distribution, voucher preparation, cheque depositing, and general ledger preparation. The study identifies weaknesses in internal controls within each system, such as manual processes, lack of verification, and inadequate segregation of duties, and discusses the associated risks of fraud, errors, and operational inefficiencies.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.