Management Accounting: Systems & Financial Adaptation - HNC

VerifiedAdded on 2023/01/12

|15

|2916

|81

Report

AI Summary

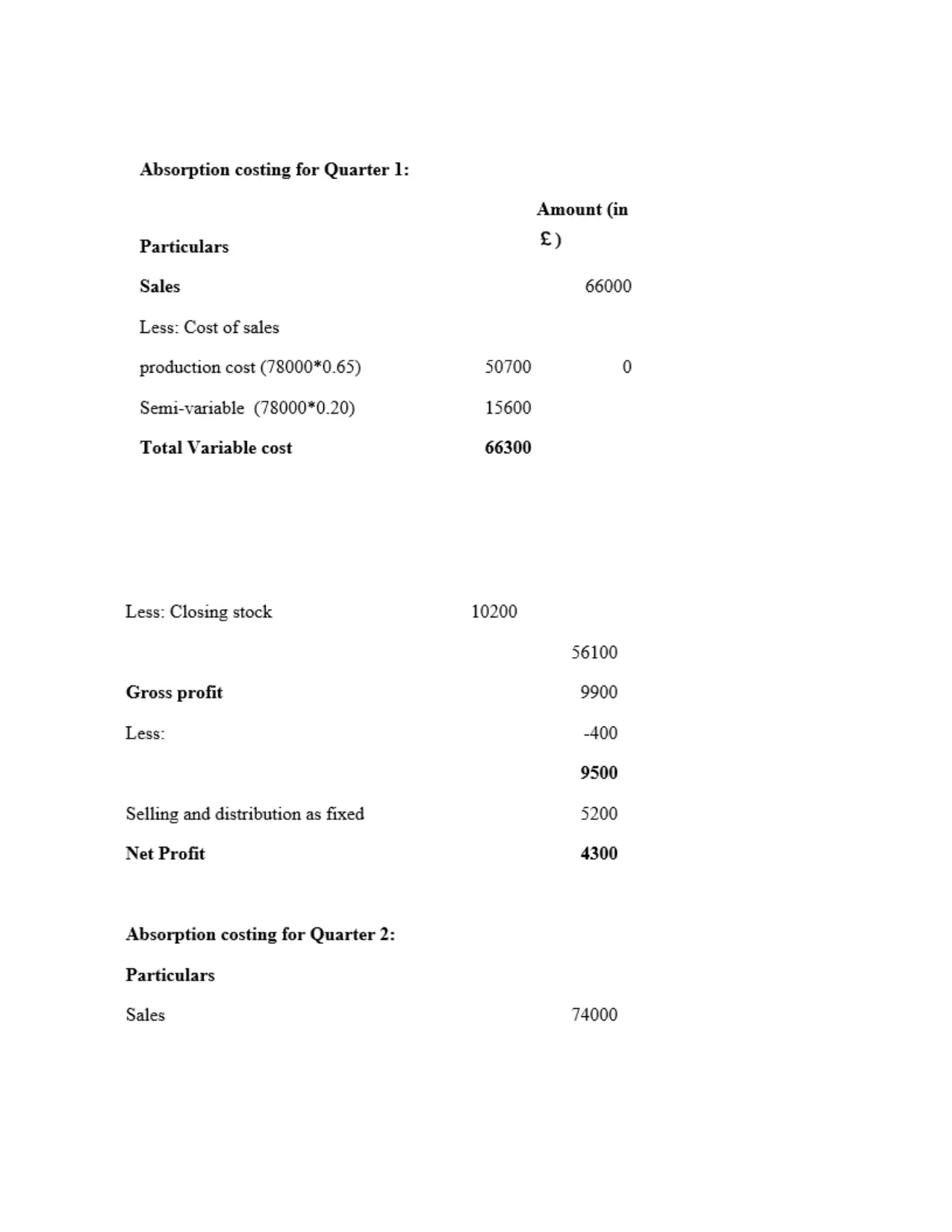

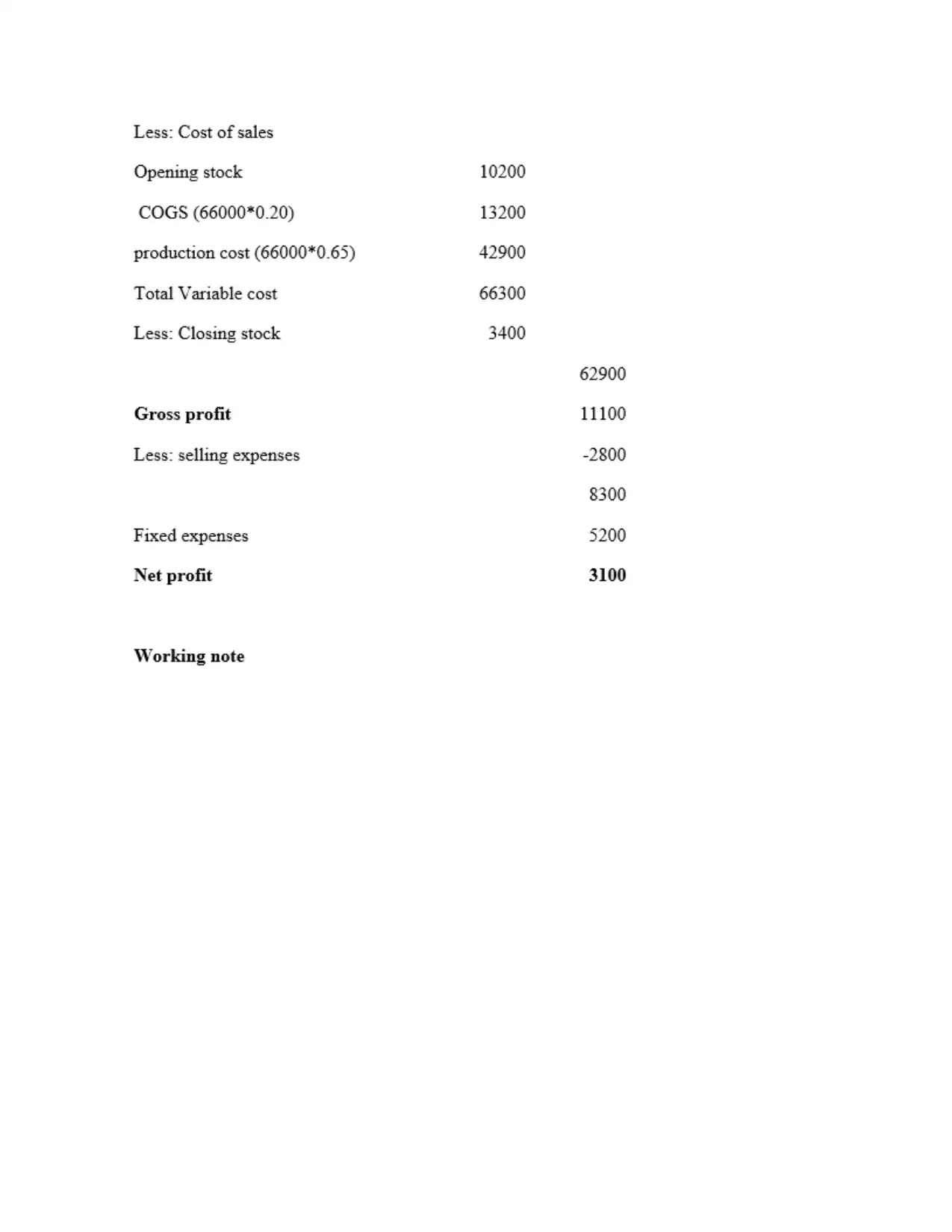

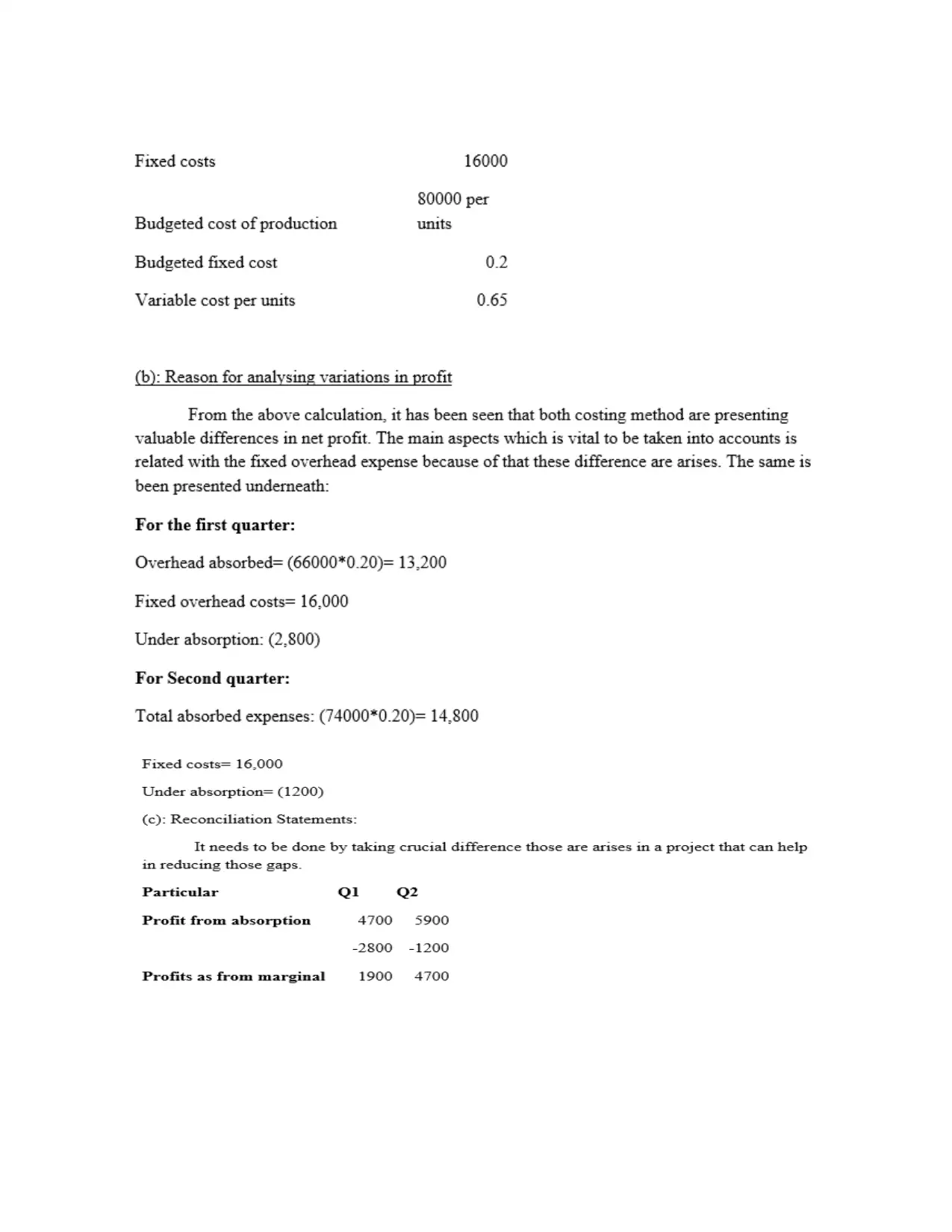

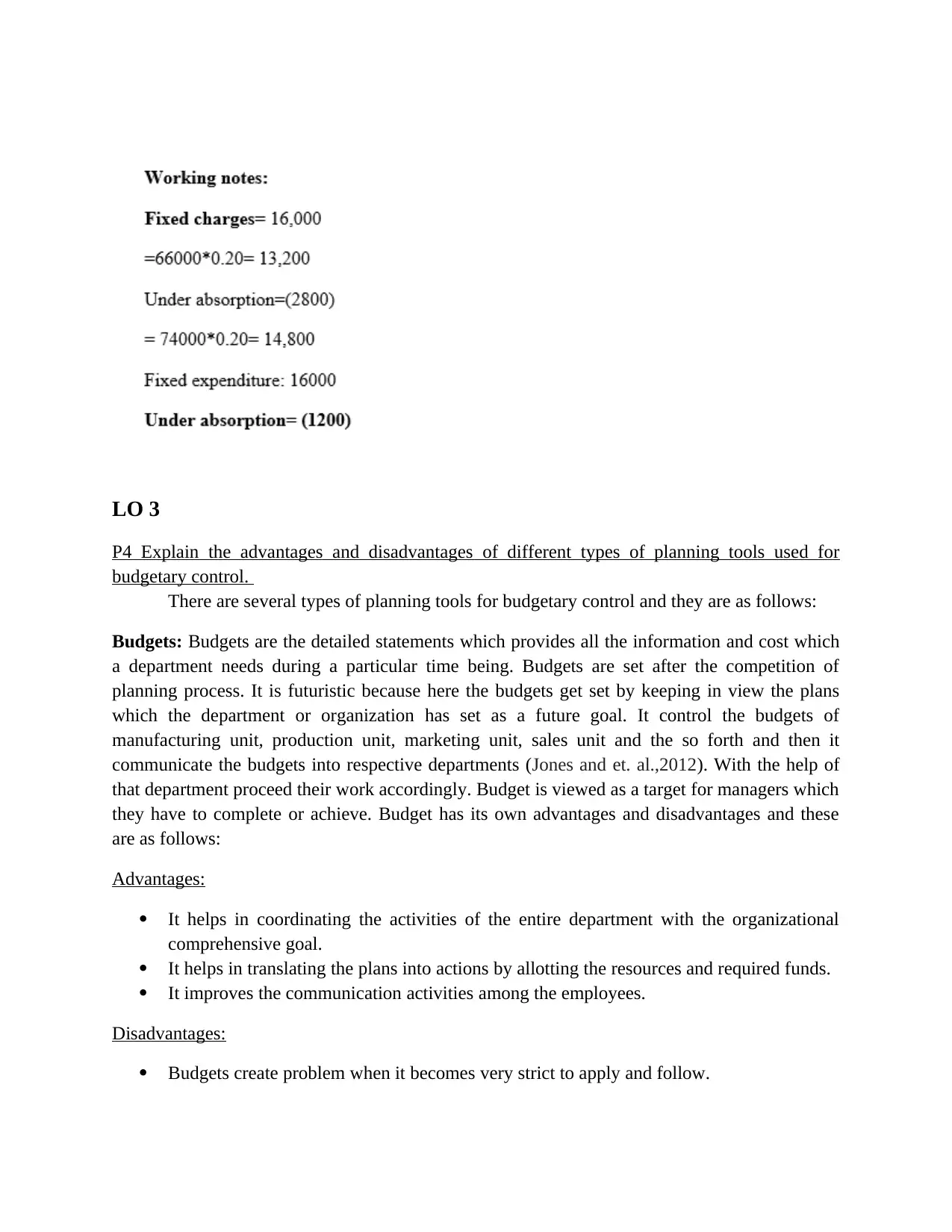

This report provides a comprehensive overview of management accounting, focusing on its essential requirements, reporting methods, and application in addressing financial problems. It begins by explaining management accounting and its role in decision-making and planning, highlighting the importance of management style and organizational structure. The report then details various management accounting reporting methods, including cost reports, budget reports, performance reports, and variance analysis. It also explores planning tools for budgetary control, such as budgets and cost-volume-profit analysis, outlining their advantages and disadvantages. Finally, the report compares how organizations adapt their management accounting systems to respond to financial problems, emphasizing the importance of identifying financial issues, financial governance, and managerial accounting skill sets. The report uses Marriot as an example to illustrate these concepts.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.