Finance Case Study: Hedging Strategies for Receivables and Payables

VerifiedAdded on 2022/09/26

|4

|924

|18

Case Study

AI Summary

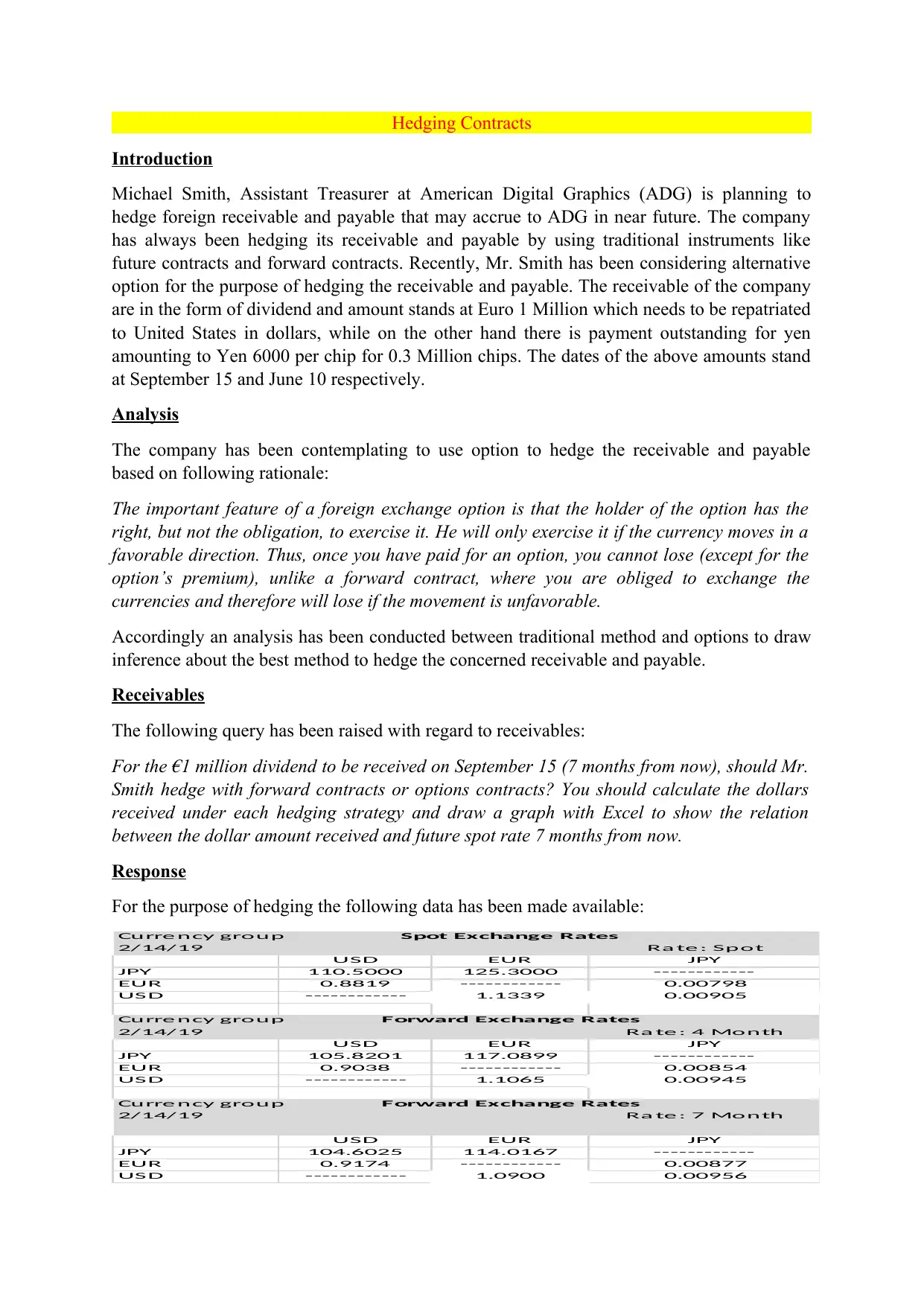

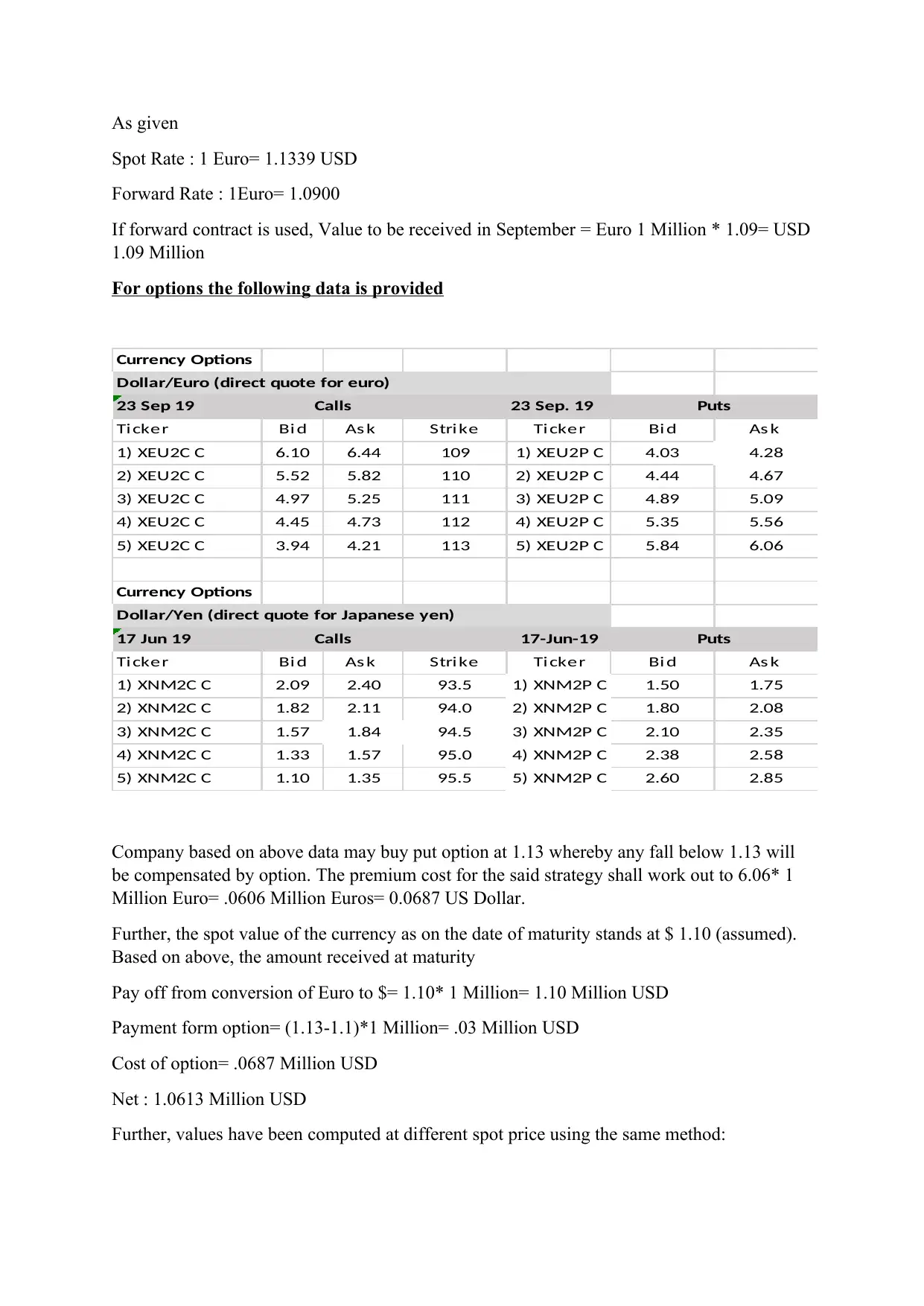

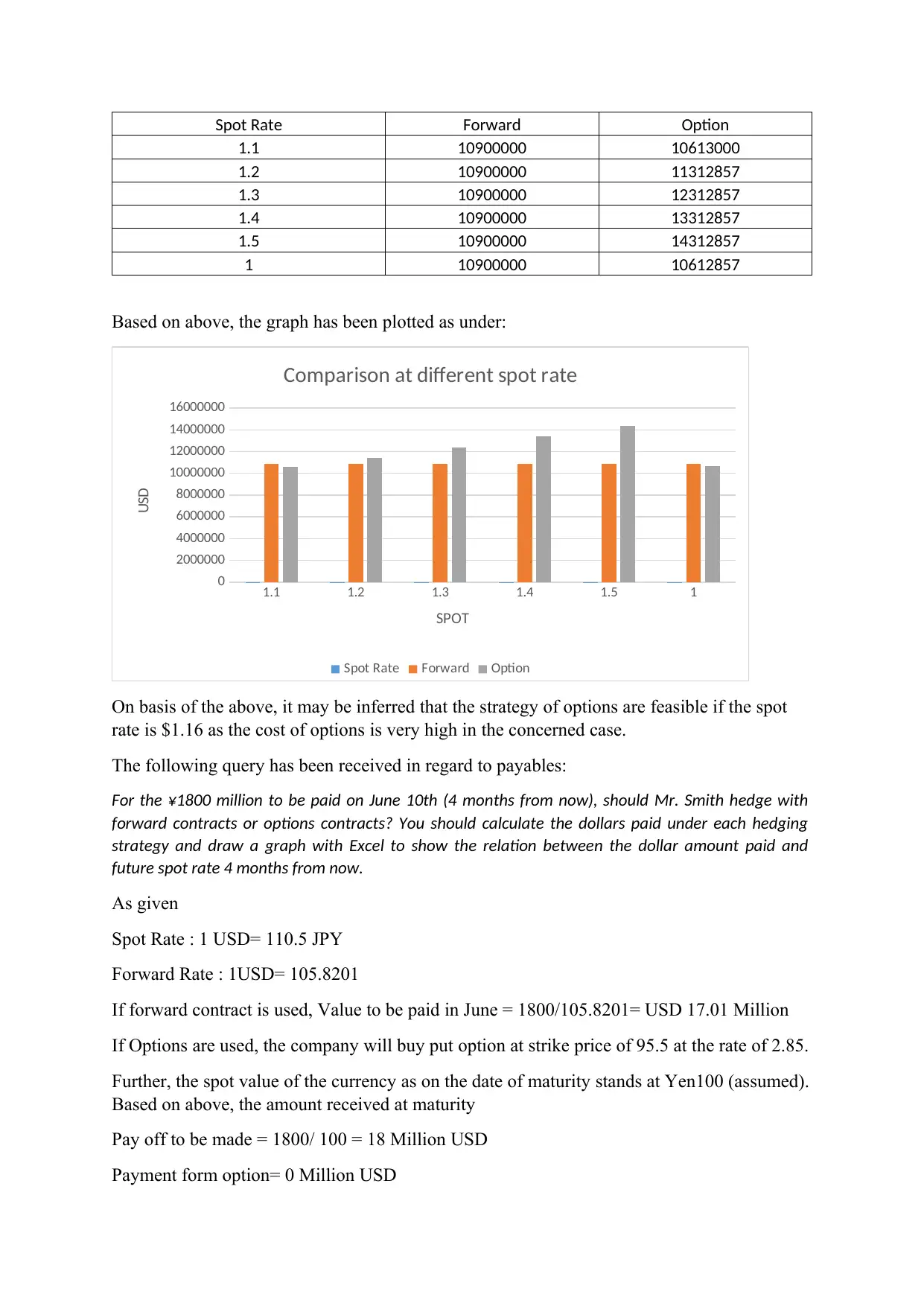

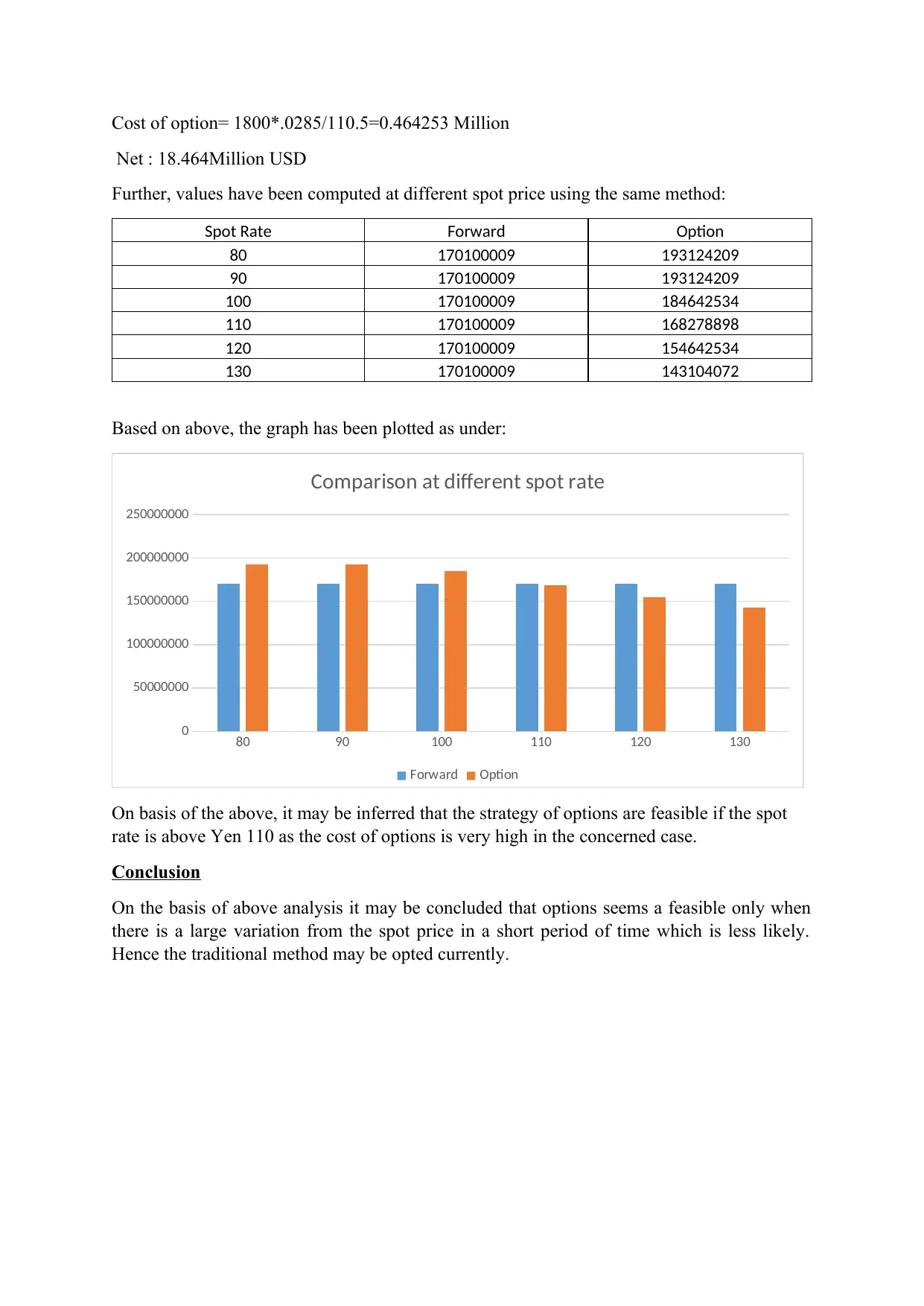

This case study analyzes hedging strategies for American Digital Graphics (ADG), focusing on managing foreign exchange risk associated with a Euro-denominated receivable and a Yen-denominated payable. The analysis compares the effectiveness of forward contracts and options contracts in hedging these exposures. For the receivable, the study calculates the dollar amounts received under both strategies and uses a graph to illustrate the relationship between the dollar amount received and future spot rates. Similarly, for the payable, the analysis determines the dollar amounts paid under each hedging method and creates a corresponding graph. The conclusion suggests that options are only feasible when there is a large variation from the spot price in a short period of time, and therefore the traditional method may be opted currently.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.