Strategic Cost Management Techniques: Adidas Case Study Analysis

VerifiedAdded on 2019/09/18

|15

|3068

|630

Report

AI Summary

This report delves into the realm of strategic cost management, providing a comprehensive overview of its principles and techniques. It explores two primary methods: activity-based cost allocation (ABC) and benchmarking. The report elucidates the benefits of ABC, such as identifying waste and improving processes, while also acknowledging its limitations, including high implementation costs. The application of ABC within Adidas is examined, highlighting the company's transition from a traditional accounting system to an ABC system, the challenges faced, and the eventual improvements in cost accuracy and operational efficiency. Furthermore, the report discusses benchmarking as a strategic tool for evaluating organizational processes against industry leaders. It outlines the pros and cons of benchmarking, emphasizing performance improvement and the identification of new paradigms. The report concludes with a case study on Adidas and its implementation of benchmarking. Overall, the report provides a detailed analysis of strategic cost management, offering valuable insights into cost optimization strategies and their practical application within a real-world business context.

Strategic Cost Management

Name

Subject

Submitted to

Date

Name

Subject

Submitted to

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................4

Activity based cost allocation system..........................................................................................4

Advantage of ABC..................................................................................................................5

Disadvantages of Activity Based Costing...............................................................................6

Adidas and Activity based cost allocation system...................................................................6

Benchmarking..............................................................................................................................8

Pros of Benchmarking.............................................................................................................9

Cons of Benchmarking..........................................................................................................10

Adidas and Benchmarking.....................................................................................................10

Conclusion and Recommendations................................................................................................12

References......................................................................................................................................14

Introduction......................................................................................................................................3

Discussion........................................................................................................................................4

Activity based cost allocation system..........................................................................................4

Advantage of ABC..................................................................................................................5

Disadvantages of Activity Based Costing...............................................................................6

Adidas and Activity based cost allocation system...................................................................6

Benchmarking..............................................................................................................................8

Pros of Benchmarking.............................................................................................................9

Cons of Benchmarking..........................................................................................................10

Adidas and Benchmarking.....................................................................................................10

Conclusion and Recommendations................................................................................................12

References......................................................................................................................................14

Introduction

In the competitive marketplace, all of the spending being done by the firms and organizations are

seen as investments. The organizations are making efficient decisions on their spending on the

basis of their internal and external capabilities and their strategic vision for delivering the value

from the investment being made. Traditionally, it was seen that the firms were under intense

pressure of cutting the costs without analyzing the integration and sustainable growth of the

business strategy.

There is a need for the development of multifaceted cost competence due to increased regulation,

increased global competition, changing demographics, etc. It was seen that the tactical solutions

used traditionally had failed to deliver the cost reductions and did not produce effective results

despite considerable consumptions of the resources. Various cases saw a substantial damage to

the image, corporate structure, culture and morale of the company. Therefore, it is imperative of

the organization to understand Cost as a strategic issue and should strive to optimize their

spending in the context of the business model. Further, a balance must be maintained between

the cost and the revenue growth of the company. There is a need to scrutinize the organizational

processes so as to knock down all the departmental barriers and to understand the business of the

suppliers in order to improve the process. Further, the cost management techniques have to be

applied for improving the strategic position of the firm and further to reduce the cost. (Cooper,

R., and Slagmulder, R., 1998).

This paper will discuss the various characteristics of the strategic cost management and the

techniques of activity-based cost allocation system and benchmark relating it to Adidas and its

functioning on the organization.

In the competitive marketplace, all of the spending being done by the firms and organizations are

seen as investments. The organizations are making efficient decisions on their spending on the

basis of their internal and external capabilities and their strategic vision for delivering the value

from the investment being made. Traditionally, it was seen that the firms were under intense

pressure of cutting the costs without analyzing the integration and sustainable growth of the

business strategy.

There is a need for the development of multifaceted cost competence due to increased regulation,

increased global competition, changing demographics, etc. It was seen that the tactical solutions

used traditionally had failed to deliver the cost reductions and did not produce effective results

despite considerable consumptions of the resources. Various cases saw a substantial damage to

the image, corporate structure, culture and morale of the company. Therefore, it is imperative of

the organization to understand Cost as a strategic issue and should strive to optimize their

spending in the context of the business model. Further, a balance must be maintained between

the cost and the revenue growth of the company. There is a need to scrutinize the organizational

processes so as to knock down all the departmental barriers and to understand the business of the

suppliers in order to improve the process. Further, the cost management techniques have to be

applied for improving the strategic position of the firm and further to reduce the cost. (Cooper,

R., and Slagmulder, R., 1998).

This paper will discuss the various characteristics of the strategic cost management and the

techniques of activity-based cost allocation system and benchmark relating it to Adidas and its

functioning on the organization.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Discussion

Strategic cost management is beneficial in developing a framework for the organization which

will review the strategic allocation of all the resources across all the operational functions of the

nosiness on the basis of their core business activities and processes. It is also beneficial in

improving the business and its understanding of all the cost drivers so as to maintain an

improved articulation of the strategic plans regarding the cost (Shank, J., and Govindarajan, V.,

2004). The following section discusses the two primary techniques of strategic cost management

along with discussing the usage of these techniques in Adidas.

Activity based cost allocation system

ABC can be considered as a natural outgrowth of the competitive and complex marketplace

present today. It helps in providing an approximation of the product cost rather than providing by

the traditional volume based costing method. This technique of strategic cost management

follows the principles that the activities lead to costs, and in order to control the costs, all the

activities must be controlled. In this technique of strategic cost management, all the activities are

first identified and then expense associated with each activity is clubbed together for getting a

detailed activity-based expense. Then a cost driver is selected for each activity, and product cost

is worked out in the end. Whereas the traditional cost accounting used to measure the cost related

to the task but ABC also was taken into account the cost of not doing the task. The system then

monitors every activity closely by relating the activities to their costs and bringing upon the

effectiveness of the cost. ABC helps in recognizing the activities relating to special engineering,

machine setups, special testing and others which cause costs to the company by consuming the

resources (Kaplan, R.S., and Atkinson, A.A., 2015). It is recognized as one of the most important

techniques in the recent decades due to

Strategic cost management is beneficial in developing a framework for the organization which

will review the strategic allocation of all the resources across all the operational functions of the

nosiness on the basis of their core business activities and processes. It is also beneficial in

improving the business and its understanding of all the cost drivers so as to maintain an

improved articulation of the strategic plans regarding the cost (Shank, J., and Govindarajan, V.,

2004). The following section discusses the two primary techniques of strategic cost management

along with discussing the usage of these techniques in Adidas.

Activity based cost allocation system

ABC can be considered as a natural outgrowth of the competitive and complex marketplace

present today. It helps in providing an approximation of the product cost rather than providing by

the traditional volume based costing method. This technique of strategic cost management

follows the principles that the activities lead to costs, and in order to control the costs, all the

activities must be controlled. In this technique of strategic cost management, all the activities are

first identified and then expense associated with each activity is clubbed together for getting a

detailed activity-based expense. Then a cost driver is selected for each activity, and product cost

is worked out in the end. Whereas the traditional cost accounting used to measure the cost related

to the task but ABC also was taken into account the cost of not doing the task. The system then

monitors every activity closely by relating the activities to their costs and bringing upon the

effectiveness of the cost. ABC helps in recognizing the activities relating to special engineering,

machine setups, special testing and others which cause costs to the company by consuming the

resources (Kaplan, R.S., and Atkinson, A.A., 2015). It is recognized as one of the most important

techniques in the recent decades due to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. Increment in the manufacturing overhead costs;

2. No relation to the manufacturing overhead costs with the direct labor hours or the

productive machine hours;

3. Production of some products in large and small batches respectively and

4. The diversity of the demands of the customers and the products.

Advantage of ABC

1. Identification of waste

Usually, the overhead costs are seen to include few wasteful products, and these can

easily be identified with the help of ABC method of cost allocation. These wastes can be

removed from the business to manage effectively.

2. Improvement of overall Processes

With the help of ABC system, the activity based costing method can scrutinize all the

processes and look into the depth. This way all the processes can be seen in the bigger

picture, and all the processes can be improved.

3. Pricing is organized

With the help of ABC, the cost associated with each and every activity can be identified,

and various pricing strategies can be developed and marketed. This helps in organizing

the spending in an efficient manner.

4. Can Be Applied To The Entire Business

It can be seen to be an effective method for production costs along with reducing the

overhead costs by using this method. Therefore, the system of allocating cost can be

applied to entire organization so as to get desired results (DRURY, C.M., 2013).

2. No relation to the manufacturing overhead costs with the direct labor hours or the

productive machine hours;

3. Production of some products in large and small batches respectively and

4. The diversity of the demands of the customers and the products.

Advantage of ABC

1. Identification of waste

Usually, the overhead costs are seen to include few wasteful products, and these can

easily be identified with the help of ABC method of cost allocation. These wastes can be

removed from the business to manage effectively.

2. Improvement of overall Processes

With the help of ABC system, the activity based costing method can scrutinize all the

processes and look into the depth. This way all the processes can be seen in the bigger

picture, and all the processes can be improved.

3. Pricing is organized

With the help of ABC, the cost associated with each and every activity can be identified,

and various pricing strategies can be developed and marketed. This helps in organizing

the spending in an efficient manner.

4. Can Be Applied To The Entire Business

It can be seen to be an effective method for production costs along with reducing the

overhead costs by using this method. Therefore, the system of allocating cost can be

applied to entire organization so as to get desired results (DRURY, C.M., 2013).

Disadvantages of Activity Based Costing

1. High Implementation Costs

Activity based costing is not the best method to be implemented in case the overhead

waste is low in the organization due to high cost of the implementation of the activity

based costing. Along with its implementation, other factors have to be brought in the

system for this system to be highly effective.

2. Reduction Is Not Always Possible

In case the overhead costs are extremely high due to volume issues, it is unlikely to have

any benefit to the organization. Furthermore, it is not seen to be efficient if the system is

representing the small portion of the costs.

3. Time Involved

The period involved in this system is extremely long, and it takes the time to examine all

the employee actions, production processes and other aspects of business for gaining a

larger view on the business issues.

4. Data Flaws

For successful implementation of ABC, all the departments and individuals must collect

and then input the data. In the case of smallest flaw, the information can be damaged

throughout the process and lead to tainting of the outcome. This can be seen as the

biggest risks while implementation of the system (DRURY, C.M., 2013).

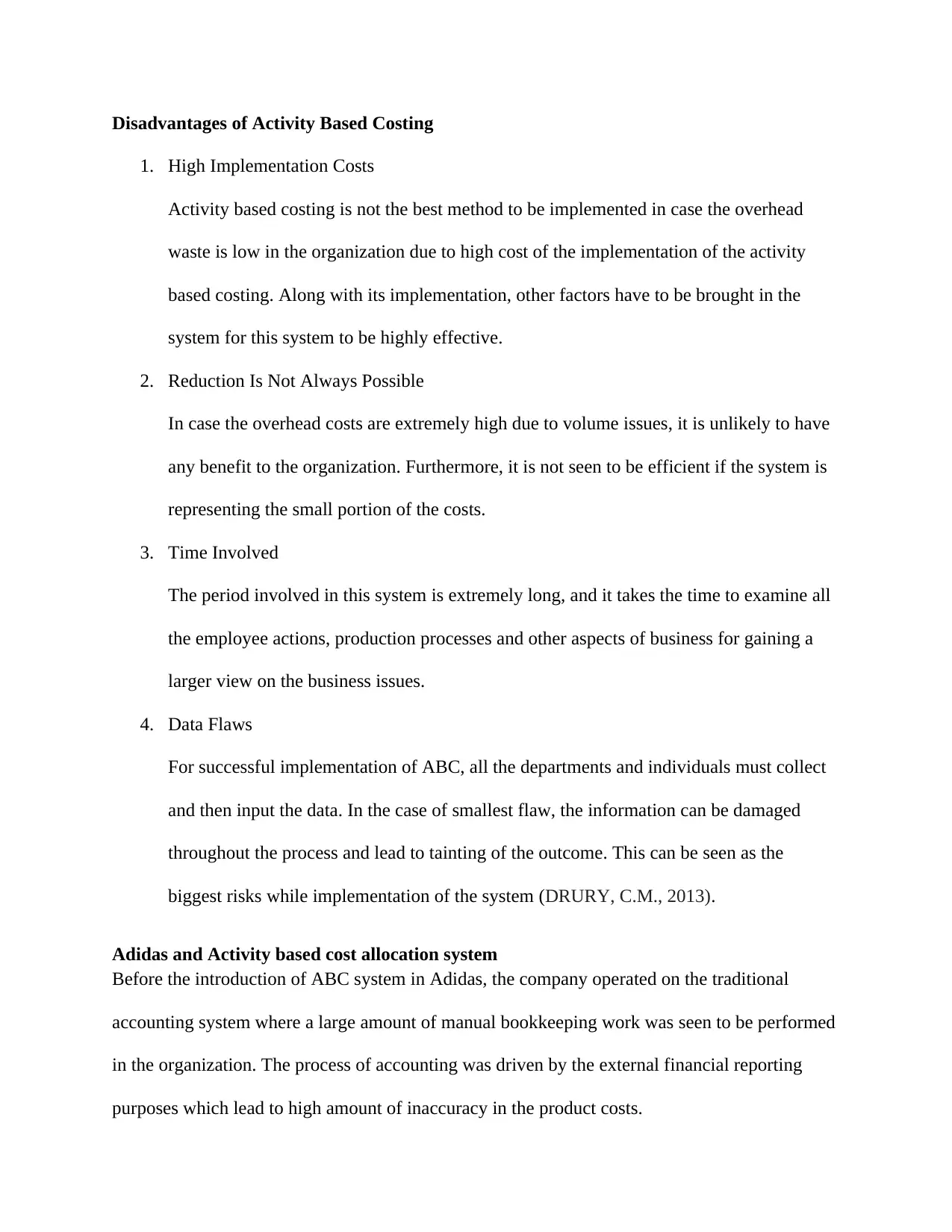

Adidas and Activity based cost allocation system

Before the introduction of ABC system in Adidas, the company operated on the traditional

accounting system where a large amount of manual bookkeeping work was seen to be performed

in the organization. The process of accounting was driven by the external financial reporting

purposes which lead to high amount of inaccuracy in the product costs.

1. High Implementation Costs

Activity based costing is not the best method to be implemented in case the overhead

waste is low in the organization due to high cost of the implementation of the activity

based costing. Along with its implementation, other factors have to be brought in the

system for this system to be highly effective.

2. Reduction Is Not Always Possible

In case the overhead costs are extremely high due to volume issues, it is unlikely to have

any benefit to the organization. Furthermore, it is not seen to be efficient if the system is

representing the small portion of the costs.

3. Time Involved

The period involved in this system is extremely long, and it takes the time to examine all

the employee actions, production processes and other aspects of business for gaining a

larger view on the business issues.

4. Data Flaws

For successful implementation of ABC, all the departments and individuals must collect

and then input the data. In the case of smallest flaw, the information can be damaged

throughout the process and lead to tainting of the outcome. This can be seen as the

biggest risks while implementation of the system (DRURY, C.M., 2013).

Adidas and Activity based cost allocation system

Before the introduction of ABC system in Adidas, the company operated on the traditional

accounting system where a large amount of manual bookkeeping work was seen to be performed

in the organization. The process of accounting was driven by the external financial reporting

purposes which lead to high amount of inaccuracy in the product costs.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Figure 1: Adidas' traditional accounting system

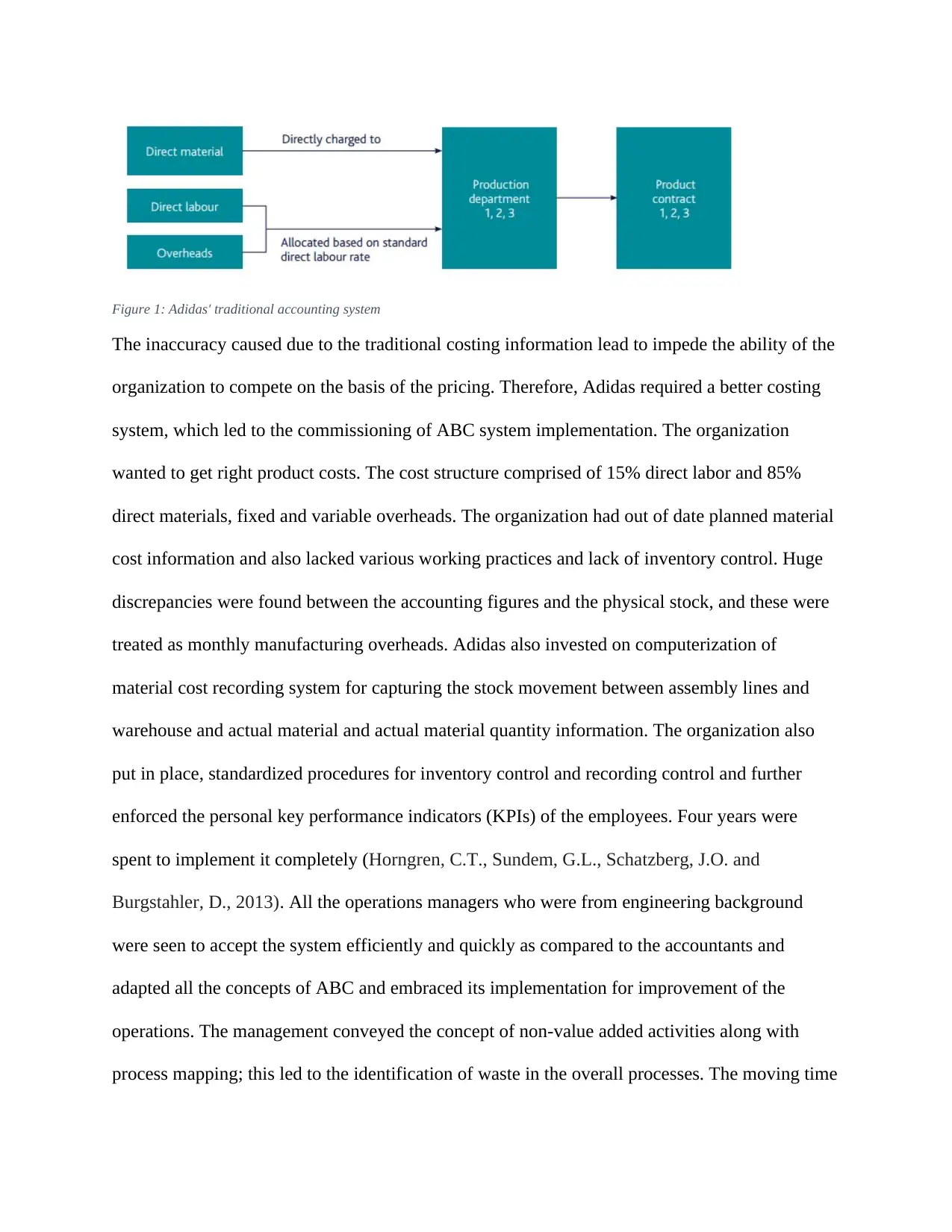

The inaccuracy caused due to the traditional costing information lead to impede the ability of the

organization to compete on the basis of the pricing. Therefore, Adidas required a better costing

system, which led to the commissioning of ABC system implementation. The organization

wanted to get right product costs. The cost structure comprised of 15% direct labor and 85%

direct materials, fixed and variable overheads. The organization had out of date planned material

cost information and also lacked various working practices and lack of inventory control. Huge

discrepancies were found between the accounting figures and the physical stock, and these were

treated as monthly manufacturing overheads. Adidas also invested on computerization of

material cost recording system for capturing the stock movement between assembly lines and

warehouse and actual material and actual material quantity information. The organization also

put in place, standardized procedures for inventory control and recording control and further

enforced the personal key performance indicators (KPIs) of the employees. Four years were

spent to implement it completely (Horngren, C.T., Sundem, G.L., Schatzberg, J.O. and

Burgstahler, D., 2013). All the operations managers who were from engineering background

were seen to accept the system efficiently and quickly as compared to the accountants and

adapted all the concepts of ABC and embraced its implementation for improvement of the

operations. The management conveyed the concept of non-value added activities along with

process mapping; this led to the identification of waste in the overall processes. The moving time

The inaccuracy caused due to the traditional costing information lead to impede the ability of the

organization to compete on the basis of the pricing. Therefore, Adidas required a better costing

system, which led to the commissioning of ABC system implementation. The organization

wanted to get right product costs. The cost structure comprised of 15% direct labor and 85%

direct materials, fixed and variable overheads. The organization had out of date planned material

cost information and also lacked various working practices and lack of inventory control. Huge

discrepancies were found between the accounting figures and the physical stock, and these were

treated as monthly manufacturing overheads. Adidas also invested on computerization of

material cost recording system for capturing the stock movement between assembly lines and

warehouse and actual material and actual material quantity information. The organization also

put in place, standardized procedures for inventory control and recording control and further

enforced the personal key performance indicators (KPIs) of the employees. Four years were

spent to implement it completely (Horngren, C.T., Sundem, G.L., Schatzberg, J.O. and

Burgstahler, D., 2013). All the operations managers who were from engineering background

were seen to accept the system efficiently and quickly as compared to the accountants and

adapted all the concepts of ABC and embraced its implementation for improvement of the

operations. The management conveyed the concept of non-value added activities along with

process mapping; this led to the identification of waste in the overall processes. The moving time

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

was reduced due to the reorganization of the assembly line layout, and the top management was

seen to become highly confident of the accuracy of their calculations and direct costs.

Figure 2: ABC System

Benchmarking

Benchmarking is considered as a process of evaluating services, products, and processes of an

organization against the functions of another organization known to be leaders in one or more

aspects of different business operations. It is an efficient tool for strategic cost management

which help an organization in measuring the overall operational proficiency of an organization. It

gives a significant understanding about how an organization compares itself with the similar

function organization, even if they are in a different field or have different customers. In addition

to it, benchmarking help an organization in recognizing systems, areas, and processes which

seen to become highly confident of the accuracy of their calculations and direct costs.

Figure 2: ABC System

Benchmarking

Benchmarking is considered as a process of evaluating services, products, and processes of an

organization against the functions of another organization known to be leaders in one or more

aspects of different business operations. It is an efficient tool for strategic cost management

which help an organization in measuring the overall operational proficiency of an organization. It

gives a significant understanding about how an organization compares itself with the similar

function organization, even if they are in a different field or have different customers. In addition

to it, benchmarking help an organization in recognizing systems, areas, and processes which

require necessary improvements either dramatic or incremental improvements (Camp, R.C.,

2013). Benchmarking can be of two types:

Technical Benchmarking

It is the benchmarking which is performed with the help of design staff to evaluate the

capabilities of products and services, especially in comparison to products and services of the

nearest competitors. If an organization is not able to gain hard data, the design efforts prove

inadequate, and products and services may become a failure in comparison to the leading

competitor.

Competitive Benchmarking

It is utilized by various organizations to analyze their existing position in the marketplace.

Competitive benchmarking mainly compares the ability of an organization with respect to the

growing competitive organization, especially with respect to more important operations, values

or attributes related to the products and services of an organization. If the organization is not able

to obtain the hard data, all marketing efforts prove misdirected and design efforts misguided.

Pros of Benchmarking

Performance Improvement: The main benefit of benchmarking is that it develops the base

of performance improvement aimed at increasing competitiveness. By displaying how to

improve competitors, benchmarking ensures the long-term survival of an organization.

With the help of benchmarking the management of an organization able to identify the

best practices of different business processes and determines what factors improve the

existing performance.

2013). Benchmarking can be of two types:

Technical Benchmarking

It is the benchmarking which is performed with the help of design staff to evaluate the

capabilities of products and services, especially in comparison to products and services of the

nearest competitors. If an organization is not able to gain hard data, the design efforts prove

inadequate, and products and services may become a failure in comparison to the leading

competitor.

Competitive Benchmarking

It is utilized by various organizations to analyze their existing position in the marketplace.

Competitive benchmarking mainly compares the ability of an organization with respect to the

growing competitive organization, especially with respect to more important operations, values

or attributes related to the products and services of an organization. If the organization is not able

to obtain the hard data, all marketing efforts prove misdirected and design efforts misguided.

Pros of Benchmarking

Performance Improvement: The main benefit of benchmarking is that it develops the base

of performance improvement aimed at increasing competitiveness. By displaying how to

improve competitors, benchmarking ensures the long-term survival of an organization.

With the help of benchmarking the management of an organization able to identify the

best practices of different business processes and determines what factors improve the

existing performance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

New Paradigms: A regular benchmarking program of an organization brings organization

out of their comfort zones and offer various measurable and specific short-term

improvement plans with which the organizations can significantly improve their

performance. Most of the time organizations establish their objectives on the basis of

established internal patterns and past trends. With the help of benchmarking, the

organizations able to remove their paradigm blindness and can establish a fresh approach

towards a settlement of goal. (Davies, J., ONS, D.E., Aston, J. and Sayal, H., 2015)

Change: Benchmarking helps the organizations to focus more on creating change and

also provide significant directions towards different change processes.

Cons of Benchmarking

The key cons of benchmarking are that it helps the organization in evaluating the efficiency of

their operational metrics, but it is not able to properly measure the overall effectiveness of such

metrics. Due to which it provide the wrong outcomes about their operational performance.

Benchmarking represents the principles and standards utilize by different competitors but does

not consider the circumstances under which the competitors able to obtain such standards. If the

objectives and goals of the competitors were flawed or prohibited due to any available factor, an

organization by benchmarking able to runs the risk of trying to ape such standards. The most

important cons of benchmarking are the danger of arrogance and complacency. This will reduce

the overall performance of an organization (Camp, R. C., 1995).

Adidas and Benchmarking

The strong market position of Adidas in London, United Kingdom led the company to achieve

great heights and the organization grew immensely and acquired various companies and a

majority stake. It also diversified itself in terms of technology by acquiring various information

technology techniques in the organization. Later on, the organization became increasingly

out of their comfort zones and offer various measurable and specific short-term

improvement plans with which the organizations can significantly improve their

performance. Most of the time organizations establish their objectives on the basis of

established internal patterns and past trends. With the help of benchmarking, the

organizations able to remove their paradigm blindness and can establish a fresh approach

towards a settlement of goal. (Davies, J., ONS, D.E., Aston, J. and Sayal, H., 2015)

Change: Benchmarking helps the organizations to focus more on creating change and

also provide significant directions towards different change processes.

Cons of Benchmarking

The key cons of benchmarking are that it helps the organization in evaluating the efficiency of

their operational metrics, but it is not able to properly measure the overall effectiveness of such

metrics. Due to which it provide the wrong outcomes about their operational performance.

Benchmarking represents the principles and standards utilize by different competitors but does

not consider the circumstances under which the competitors able to obtain such standards. If the

objectives and goals of the competitors were flawed or prohibited due to any available factor, an

organization by benchmarking able to runs the risk of trying to ape such standards. The most

important cons of benchmarking are the danger of arrogance and complacency. This will reduce

the overall performance of an organization (Camp, R. C., 1995).

Adidas and Benchmarking

The strong market position of Adidas in London, United Kingdom led the company to achieve

great heights and the organization grew immensely and acquired various companies and a

majority stake. It also diversified itself in terms of technology by acquiring various information

technology techniques in the organization. Later on, the organization became increasingly

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

vulnerable when it started facing intense competition from other strong brands like Nike. As per

the analyst, the organization failed to provide a strategic direction to the company. The operating

cost of the company was seen to be high and its products were seen to be of inferior quality when

compared with Nike products. Further, it was seen to suffer from the centralized decision-

making process which resulted in fall of assets, and the market share was also seen to come

down sharply. The top management started emphasizing on reduction in the manufacturing costs

giving a new thrust for improvement in the quality control (Hinton, M., Francis, G., Holloway,

J., 2000). The organization now implemented a new program wherein the benchmarking

program was incorporated in the company. This led to playing a major role in the company, and

the implementation of the program led to reap various benefits in the company.

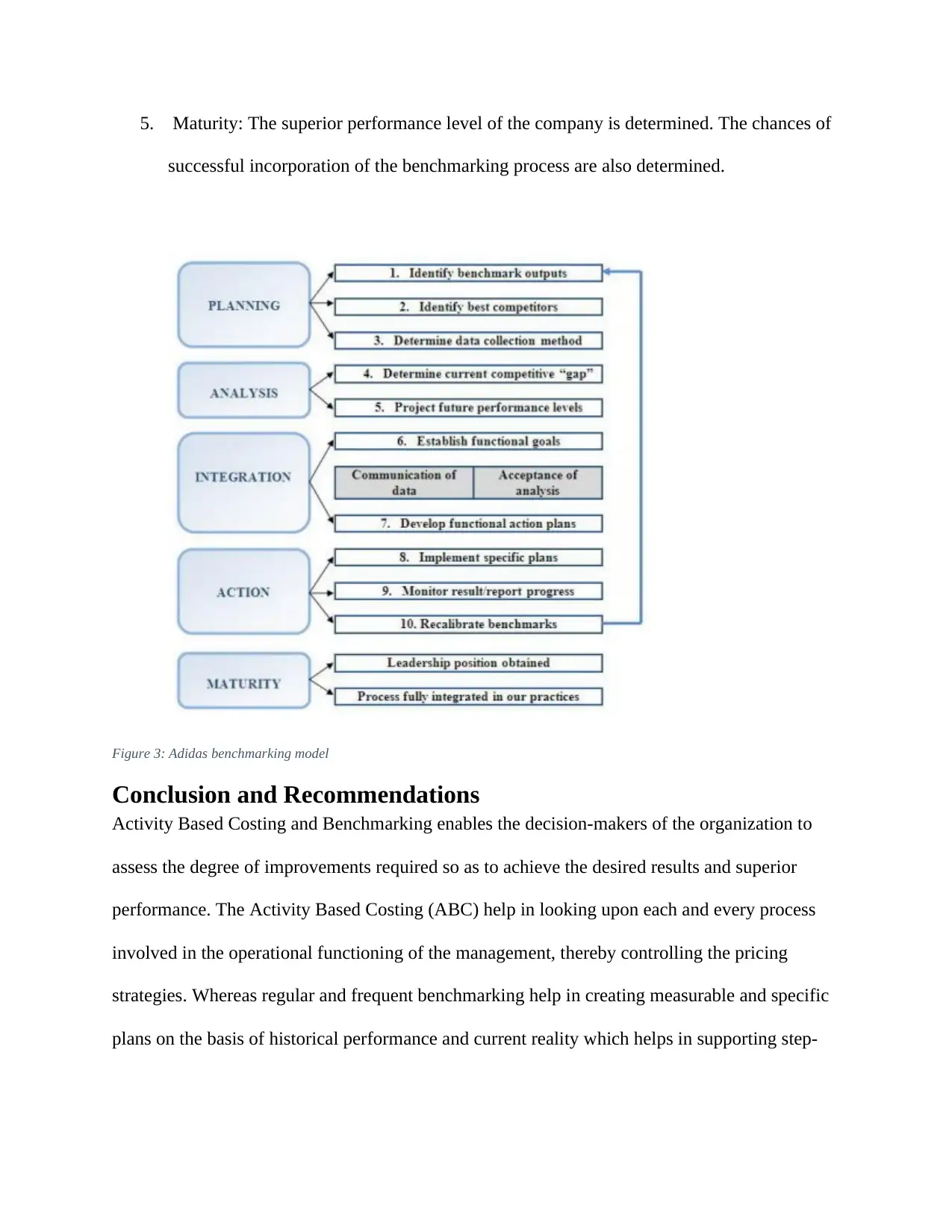

The company introduced a five-stage process which involved the following activities:

1. Planning: the subject to be benchmarked it determined and the most suitable data

collection technique is selected.

2. Analysis: The strengths of all the competitors are assessed, and the performance of

Adidas is compared with its competitors like Nike for determining the competitive gap

and to gain the projected competitive gap.

3. Integration: The necessary goals are established based on the data collected for attaining

best performance wherein all the objectives and goals of the company are integrated.

New goals and objectives of the company are determined which are communicated across

the whole organization.

4. Action: The action plans are established and then assesses periodically for determining

the achievement of the company’s objectives. Any type of deviations from the selected

plan are scrutinized.

the analyst, the organization failed to provide a strategic direction to the company. The operating

cost of the company was seen to be high and its products were seen to be of inferior quality when

compared with Nike products. Further, it was seen to suffer from the centralized decision-

making process which resulted in fall of assets, and the market share was also seen to come

down sharply. The top management started emphasizing on reduction in the manufacturing costs

giving a new thrust for improvement in the quality control (Hinton, M., Francis, G., Holloway,

J., 2000). The organization now implemented a new program wherein the benchmarking

program was incorporated in the company. This led to playing a major role in the company, and

the implementation of the program led to reap various benefits in the company.

The company introduced a five-stage process which involved the following activities:

1. Planning: the subject to be benchmarked it determined and the most suitable data

collection technique is selected.

2. Analysis: The strengths of all the competitors are assessed, and the performance of

Adidas is compared with its competitors like Nike for determining the competitive gap

and to gain the projected competitive gap.

3. Integration: The necessary goals are established based on the data collected for attaining

best performance wherein all the objectives and goals of the company are integrated.

New goals and objectives of the company are determined which are communicated across

the whole organization.

4. Action: The action plans are established and then assesses periodically for determining

the achievement of the company’s objectives. Any type of deviations from the selected

plan are scrutinized.

5. Maturity: The superior performance level of the company is determined. The chances of

successful incorporation of the benchmarking process are also determined.

Figure 3: Adidas benchmarking model

Conclusion and Recommendations

Activity Based Costing and Benchmarking enables the decision-makers of the organization to

assess the degree of improvements required so as to achieve the desired results and superior

performance. The Activity Based Costing (ABC) help in looking upon each and every process

involved in the operational functioning of the management, thereby controlling the pricing

strategies. Whereas regular and frequent benchmarking help in creating measurable and specific

plans on the basis of historical performance and current reality which helps in supporting step-

successful incorporation of the benchmarking process are also determined.

Figure 3: Adidas benchmarking model

Conclusion and Recommendations

Activity Based Costing and Benchmarking enables the decision-makers of the organization to

assess the degree of improvements required so as to achieve the desired results and superior

performance. The Activity Based Costing (ABC) help in looking upon each and every process

involved in the operational functioning of the management, thereby controlling the pricing

strategies. Whereas regular and frequent benchmarking help in creating measurable and specific

plans on the basis of historical performance and current reality which helps in supporting step-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.