Advance Accounting Principles Report: AASB 2 and iSignthis Limited

VerifiedAdded on 2020/05/28

|8

|1934

|69

Report

AI Summary

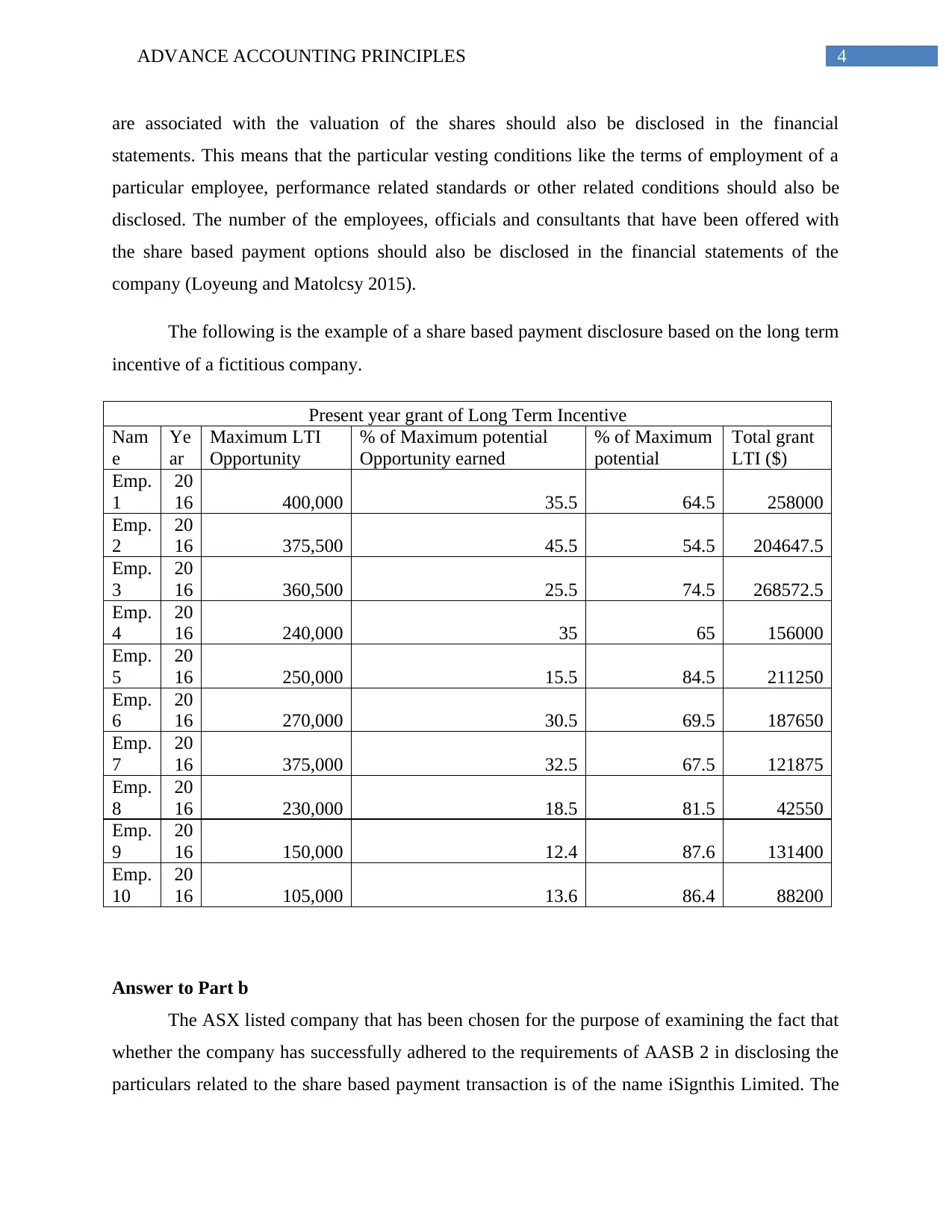

This report delves into the intricacies of AASB 2, focusing on share-based payment disclosure requirements. It begins with a business memorandum outlining the necessary disclosures for Alpha Ltd's share option plan, detailing equity-settled transactions, vesting conditions, and the importance of fair value measurement. The report then examines the annual report of iSignthis Limited, an ASX-listed company, to assess its compliance with AASB 2. The analysis reveals that iSignthis Limited's disclosures are insufficient, lacking critical information regarding share valuation techniques, vesting conditions, and the nature of the share-based payment transactions. The report highlights the importance of comprehensive disclosures to ensure transparency and adherence to accounting standards, providing a comprehensive overview of the accounting treatment of share-based payments and their impact on financial reporting.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.