Advance Financial Accounting: Rio Tinto Annual Report Analysis

VerifiedAdded on 2022/11/13

|11

|3474

|189

Report

AI Summary

This report provides an executive summary and detailed analysis of advanced financial accounting principles, focusing on the annual report of Rio Tinto Limited, an ASX-listed entity. It examines key accounting concepts like the going concern, business entity, and accounting period and cost concepts. The report delves into the measurement issues within the conceptual framework, particularly the trade-off between historical cost and fair value in asset and liability valuation. It evaluates the importance of relevance and representational faithfulness in financial reporting, supported by examples from Rio Tinto's financial statements, including asset measurement and revenue recognition. The report also discusses the implications of different measurement approaches and their impact on the comparability of financial information, especially concerning intangible assets, leases, and financial instruments. Finally, the report also explains how the company has adopted various measurement approaches as per the nature of assets and liabilities, causing the issue of inconsistency in the financial reporting of the company.

Advance Financial Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The main objective of the report is to present an examination of the contemporary issue

in accounting by analyzing the annual report of a selected ASX listed entity. The report in this

context has presented an evaluation of the annual report of Rio Tinto Limited to determine the

accounting method used by it for financial reporting. Also, it has examined the need of achieving

a trade-off between relevancy and faithful presentation of financial information to meet the

qualitative criteria of these two fundamental features of conceptual accounting framework. This

is essential because the presence of both the characteristic is essential in the financial reports and

as such the accounting of assets and liabilities should be done in a manner so that both the stated

criteria’s are able to be met by the business entities.

2

The main objective of the report is to present an examination of the contemporary issue

in accounting by analyzing the annual report of a selected ASX listed entity. The report in this

context has presented an evaluation of the annual report of Rio Tinto Limited to determine the

accounting method used by it for financial reporting. Also, it has examined the need of achieving

a trade-off between relevancy and faithful presentation of financial information to meet the

qualitative criteria of these two fundamental features of conceptual accounting framework. This

is essential because the presence of both the characteristic is essential in the financial reports and

as such the accounting of assets and liabilities should be done in a manner so that both the stated

criteria’s are able to be met by the business entities.

2

Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

1: Description of accountings concepts and their application through providing examples of real

life company namely Rio Tinto.......................................................................................................4

Going Concern Accounting Concept...........................................................................................4

Business entity concept................................................................................................................5

Accounting period and cost concept............................................................................................5

2: Analysis of Issue of Measurement in the Conceptual Framework and Example from Selected

Company..........................................................................................................................................6

3: Evaluation of Relevance and Representational Faithfulness and their Importance in

Accounting for Assets and Liabilities..............................................................................................7

Conclusion.......................................................................................................................................9

References......................................................................................................................................10

3

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

1: Description of accountings concepts and their application through providing examples of real

life company namely Rio Tinto.......................................................................................................4

Going Concern Accounting Concept...........................................................................................4

Business entity concept................................................................................................................5

Accounting period and cost concept............................................................................................5

2: Analysis of Issue of Measurement in the Conceptual Framework and Example from Selected

Company..........................................................................................................................................6

3: Evaluation of Relevance and Representational Faithfulness and their Importance in

Accounting for Assets and Liabilities..............................................................................................7

Conclusion.......................................................................................................................................9

References......................................................................................................................................10

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The conceptual accounting framework is being developed and provided by the IASB to

direct and support the business entities cross the world in selection of appropriate accounting

concepts and approach for reporting of financial information. The ASX listed entities comply

with the IASB standard and therefore also integrate the use of qualitative principles for the

development of financial reports. As such, this report presents an evaluation of the accounting

concepts and policies implemented by an ASX listed entity, that is Rio Tinto Limited, a mining

company of Australia at the time of developing its financial statements. Also, it presents a

discussion regarding the measurement issue in accounting by stating examples from the selected

ASX listed entity. The importance of relevance and faithful representation as two major criteria

of financial reporting has been evaluated in the report by the use of selected ASX listed entity.

1: Description of accountings concepts and their application through providing examples of

real life company namely Rio Tinto

Below are some major accounting concepts that have been mandatory to apply by all

entities in world:

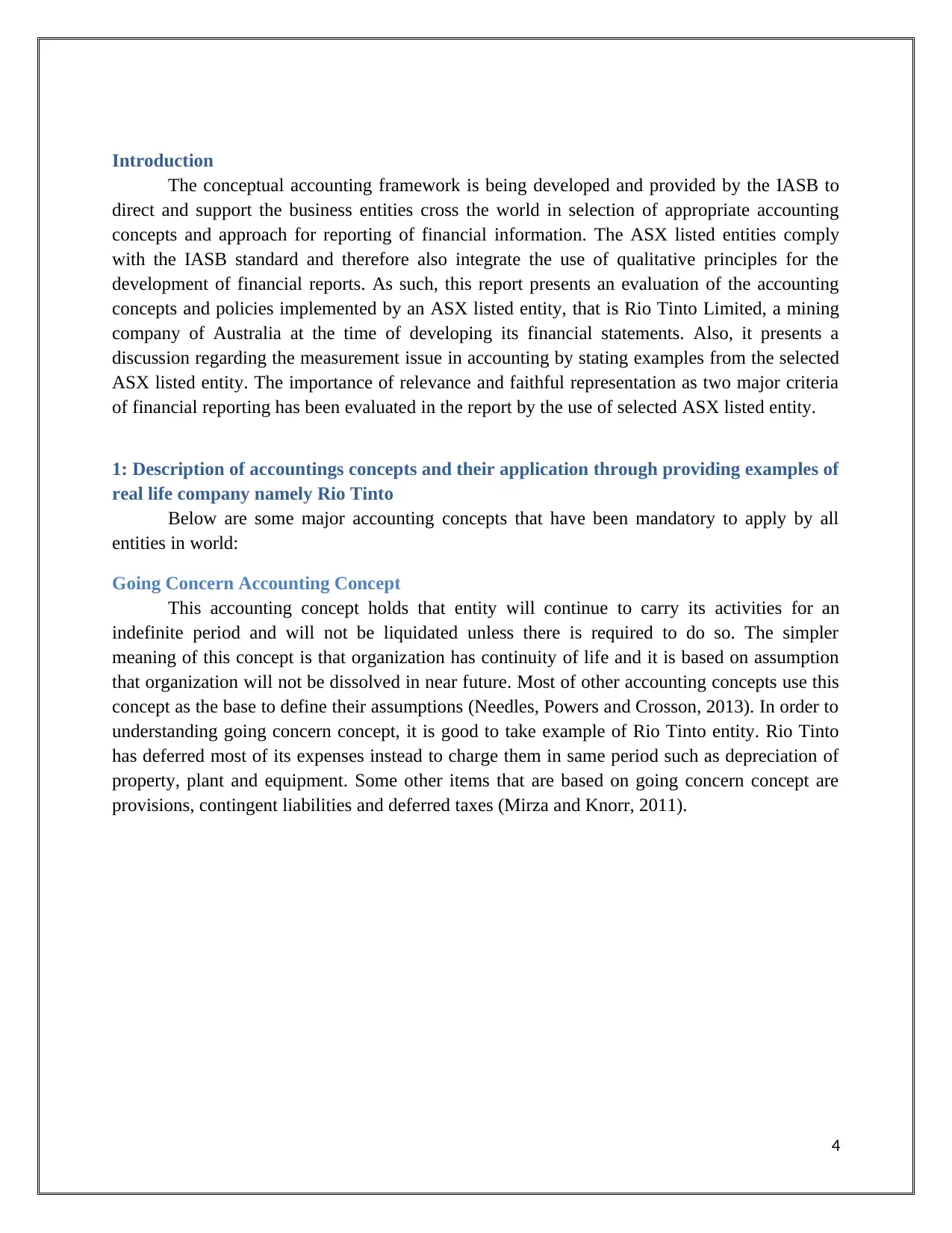

Going Concern Accounting Concept

This accounting concept holds that entity will continue to carry its activities for an

indefinite period and will not be liquidated unless there is required to do so. The simpler

meaning of this concept is that organization has continuity of life and it is based on assumption

that organization will not be dissolved in near future. Most of other accounting concepts use this

concept as the base to define their assumptions (Needles, Powers and Crosson, 2013). In order to

understanding going concern concept, it is good to take example of Rio Tinto entity. Rio Tinto

has deferred most of its expenses instead to charge them in same period such as depreciation of

property, plant and equipment. Some other items that are based on going concern concept are

provisions, contingent liabilities and deferred taxes (Mirza and Knorr, 2011).

4

The conceptual accounting framework is being developed and provided by the IASB to

direct and support the business entities cross the world in selection of appropriate accounting

concepts and approach for reporting of financial information. The ASX listed entities comply

with the IASB standard and therefore also integrate the use of qualitative principles for the

development of financial reports. As such, this report presents an evaluation of the accounting

concepts and policies implemented by an ASX listed entity, that is Rio Tinto Limited, a mining

company of Australia at the time of developing its financial statements. Also, it presents a

discussion regarding the measurement issue in accounting by stating examples from the selected

ASX listed entity. The importance of relevance and faithful representation as two major criteria

of financial reporting has been evaluated in the report by the use of selected ASX listed entity.

1: Description of accountings concepts and their application through providing examples of

real life company namely Rio Tinto

Below are some major accounting concepts that have been mandatory to apply by all

entities in world:

Going Concern Accounting Concept

This accounting concept holds that entity will continue to carry its activities for an

indefinite period and will not be liquidated unless there is required to do so. The simpler

meaning of this concept is that organization has continuity of life and it is based on assumption

that organization will not be dissolved in near future. Most of other accounting concepts use this

concept as the base to define their assumptions (Needles, Powers and Crosson, 2013). In order to

understanding going concern concept, it is good to take example of Rio Tinto entity. Rio Tinto

has deferred most of its expenses instead to charge them in same period such as depreciation of

property, plant and equipment. Some other items that are based on going concern concept are

provisions, contingent liabilities and deferred taxes (Mirza and Knorr, 2011).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Annual report, 2018)

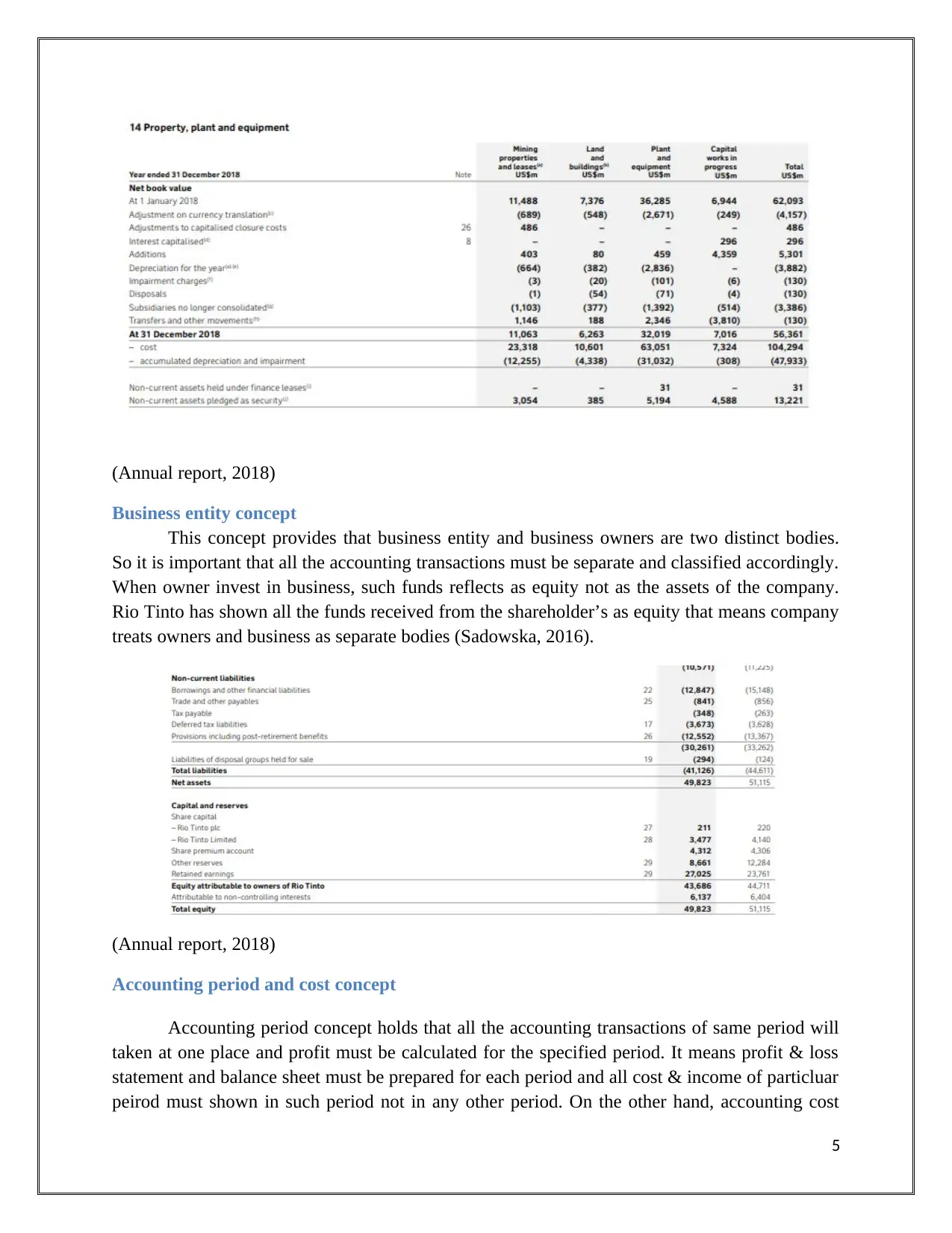

Business entity concept

This concept provides that business entity and business owners are two distinct bodies.

So it is important that all the accounting transactions must be separate and classified accordingly.

When owner invest in business, such funds reflects as equity not as the assets of the company.

Rio Tinto has shown all the funds received from the shareholder’s as equity that means company

treats owners and business as separate bodies (Sadowska, 2016).

(Annual report, 2018)

Accounting period and cost concept

Accounting period concept holds that all the accounting transactions of same period will

taken at one place and profit must be calculated for the specified period. It means profit & loss

statement and balance sheet must be prepared for each period and all cost & income of particluar

peirod must shown in such period not in any other period. On the other hand, accounting cost

5

Business entity concept

This concept provides that business entity and business owners are two distinct bodies.

So it is important that all the accounting transactions must be separate and classified accordingly.

When owner invest in business, such funds reflects as equity not as the assets of the company.

Rio Tinto has shown all the funds received from the shareholder’s as equity that means company

treats owners and business as separate bodies (Sadowska, 2016).

(Annual report, 2018)

Accounting period and cost concept

Accounting period concept holds that all the accounting transactions of same period will

taken at one place and profit must be calculated for the specified period. It means profit & loss

statement and balance sheet must be prepared for each period and all cost & income of particluar

peirod must shown in such period not in any other period. On the other hand, accounting cost

5

concept provides entity must reflect all their assets at cost basis unless specific standard states to

value the asset on fair value (Wahlen, Baginski and Bradshaw, 2017).

2: Analysis of Issue of Measurement in the Conceptual Framework and Example from

Selected Company

The conceptual framework of accounting has been developed to provide guidance to the

preparers regarding the special accounting methods and policies to be used for development of

financial reports. The accounting framework has been developed by the IASB and therefore need

to be adopted by all the business entities across the world complying with the IASB standards.

The accounting framework has stated that the objective of providing financial reports to the

general users is to help them in economic decision-making ( Filipova, 2016). The framework has

also provided a standard framework to be used by businesses for identification, recognition and

measurement of its subsequent financial items. The conceptual framework is recognized as the

first framework in accounting that has helped in clarifying the concepts regarding measurement

approaches to be used in financial reporting. The framework has generally regarded historical

cost and fair value as the two main measurement concepts that are to be used by businesses for

the purpose of financial reporting (International Accounting Standards Board, 2016).

However, the issue of measurement that is present within the conceptual framework is

regarding the selection of an appropriate measurement approach for accounting of financial

items. The issue that exists in this context is whether the financial items such as assets or

liabilities should be identified and measured on cost basis or value basis as stated by the

framework. This is because cost measurement approach will tend to provide more reliable

information to the users while might not be largely effective in depicting relevant financial

information as it is past oriented (IFRS, 2017). However, the use of valuation method will

provide current value of a financial item on the basis of its active market but will not be reliable

in absence of present of an active market. Therefore, there is a conflict present between the uses

of two approaches for measurement in the process of financial reporting. The failure of the

framework top predict an accurate way for measuring the value of financial items is the main

issue that is present in the system of financial reporting (Gassen and Schwedler, 2010).

The financial analysts and investors are regarded to be fair value measurement approach

as more consistent with the objective of financial reporting in comparison to the historical cost

basis. This is because it reflects an accurate value of financial assets on the basis of its current

market conditions and thus helpful in providing trustworthy and relevant information to the

investors (Wolk, Dodd and Rozycki, 2016). The debate over measurement in accounting is

related to the shift of traditional basis of measurement, that is, historical cots, towards the use of

fair value. This is on the basis of changes in the nature of financial reporting due to development

of new ways of carrying business operations (ICAEW, 2016). The major challenge that is present

before the accounts in this regard is to develop an adequate method of measuring the value of

leasing, financial instruments, share-based payments as they do not have a historical cost.

6

value the asset on fair value (Wahlen, Baginski and Bradshaw, 2017).

2: Analysis of Issue of Measurement in the Conceptual Framework and Example from

Selected Company

The conceptual framework of accounting has been developed to provide guidance to the

preparers regarding the special accounting methods and policies to be used for development of

financial reports. The accounting framework has been developed by the IASB and therefore need

to be adopted by all the business entities across the world complying with the IASB standards.

The accounting framework has stated that the objective of providing financial reports to the

general users is to help them in economic decision-making ( Filipova, 2016). The framework has

also provided a standard framework to be used by businesses for identification, recognition and

measurement of its subsequent financial items. The conceptual framework is recognized as the

first framework in accounting that has helped in clarifying the concepts regarding measurement

approaches to be used in financial reporting. The framework has generally regarded historical

cost and fair value as the two main measurement concepts that are to be used by businesses for

the purpose of financial reporting (International Accounting Standards Board, 2016).

However, the issue of measurement that is present within the conceptual framework is

regarding the selection of an appropriate measurement approach for accounting of financial

items. The issue that exists in this context is whether the financial items such as assets or

liabilities should be identified and measured on cost basis or value basis as stated by the

framework. This is because cost measurement approach will tend to provide more reliable

information to the users while might not be largely effective in depicting relevant financial

information as it is past oriented (IFRS, 2017). However, the use of valuation method will

provide current value of a financial item on the basis of its active market but will not be reliable

in absence of present of an active market. Therefore, there is a conflict present between the uses

of two approaches for measurement in the process of financial reporting. The failure of the

framework top predict an accurate way for measuring the value of financial items is the main

issue that is present in the system of financial reporting (Gassen and Schwedler, 2010).

The financial analysts and investors are regarded to be fair value measurement approach

as more consistent with the objective of financial reporting in comparison to the historical cost

basis. This is because it reflects an accurate value of financial assets on the basis of its current

market conditions and thus helpful in providing trustworthy and relevant information to the

investors (Wolk, Dodd and Rozycki, 2016). The debate over measurement in accounting is

related to the shift of traditional basis of measurement, that is, historical cots, towards the use of

fair value. This is on the basis of changes in the nature of financial reporting due to development

of new ways of carrying business operations (ICAEW, 2016). The major challenge that is present

before the accounts in this regard is to develop an adequate method of measuring the value of

leasing, financial instruments, share-based payments as they do not have a historical cost.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Therefore, more emphasis is placed on using fair value method of accounting as an adequate

approach to measure the value of complex financial accounting items. However, the question

that is associated with the use of fair value is regarding the anticipation of uncertainty in the

future outcomes to provide a fair picture of the current performance of an asset till measurement

date. As such, the IFRS has provided that prepares can adopt the use of different measurement

concepts for recognition of the value of the key financial items of an entity. The use of different

method of measurement makes financial information less comparable due to inconsistency in the

financial results over the period of time. The issue in measurement can also be elaborated by

providing examples from the financial report of the selected company of Rio Tinto Limited for

the year 2018 (Hopwood, 2013).

The fixed assets such as property, plant and equipment are measured at cost less

deprecation by considering the expected useful life. The recoverable mount of asset of less that

the depreciated historical cost them the assets are required to be written down at the recoverable

amount which is higher of its net fair value and value in use as per IAS 16. The inventories are

recognized at lower of historical cost and net realizable value. The company has also categorized

its financial assets into two categories, those that are measured at fair value or those held at

amortized cost(Annual report : Rio Tinto Limited, 2018). The measurement approach is selected

on the basis of the contractual terms of the cash flows. The financial liabilities are recognized at

fair value and are measured subsequently with the use of amortized cost. The share plans are also

recognized at fair value which is then stated as expense over the expected financial period

(Grüber, 2014).

Sales revenue is recognized on the basis of carrying value that is likely to be received

after the transfer of goods and services to the customers. The intangible assets are recorded

initially at costs and they are amortized over their useful economic lives. The accounting for

lessees is done as pre the IAS 17 standard that measures the lease liability at present value of

future cash flow obligations for meeting the retail payments. As the standard, a lessee needs to

identify all the use of assets and liabilities in a lease. The right of use of an asset depicts the lease

liability. There is also a need to recognize deprecation of the right of using assets and interest to

be paid on lease liabilities within the income statements. The total amount of cash paid and the

interest incurred for taking a lease should be stated in the cash flow statements. Therefore, it can

be said that Rio Tinto ahs adopted the use of various measurement approaches as per the nature

of assets and liabilities and this has resulted in causing the issue of inconsistency in the financial

reporting of the company(Annual report : Rio Tinto Limited, 2018).

3: Evaluation of Relevance and Representational Faithfulness and their Importance in

Accounting for Assets and Liabilities

The conceptual accounting framework has presented two major qualitative principles that

need to be present within the financial reports for increasing their usefulness in economic

decision-making of investors. The relevancy as stated by the conceptual accounting framework

7

approach to measure the value of complex financial accounting items. However, the question

that is associated with the use of fair value is regarding the anticipation of uncertainty in the

future outcomes to provide a fair picture of the current performance of an asset till measurement

date. As such, the IFRS has provided that prepares can adopt the use of different measurement

concepts for recognition of the value of the key financial items of an entity. The use of different

method of measurement makes financial information less comparable due to inconsistency in the

financial results over the period of time. The issue in measurement can also be elaborated by

providing examples from the financial report of the selected company of Rio Tinto Limited for

the year 2018 (Hopwood, 2013).

The fixed assets such as property, plant and equipment are measured at cost less

deprecation by considering the expected useful life. The recoverable mount of asset of less that

the depreciated historical cost them the assets are required to be written down at the recoverable

amount which is higher of its net fair value and value in use as per IAS 16. The inventories are

recognized at lower of historical cost and net realizable value. The company has also categorized

its financial assets into two categories, those that are measured at fair value or those held at

amortized cost(Annual report : Rio Tinto Limited, 2018). The measurement approach is selected

on the basis of the contractual terms of the cash flows. The financial liabilities are recognized at

fair value and are measured subsequently with the use of amortized cost. The share plans are also

recognized at fair value which is then stated as expense over the expected financial period

(Grüber, 2014).

Sales revenue is recognized on the basis of carrying value that is likely to be received

after the transfer of goods and services to the customers. The intangible assets are recorded

initially at costs and they are amortized over their useful economic lives. The accounting for

lessees is done as pre the IAS 17 standard that measures the lease liability at present value of

future cash flow obligations for meeting the retail payments. As the standard, a lessee needs to

identify all the use of assets and liabilities in a lease. The right of use of an asset depicts the lease

liability. There is also a need to recognize deprecation of the right of using assets and interest to

be paid on lease liabilities within the income statements. The total amount of cash paid and the

interest incurred for taking a lease should be stated in the cash flow statements. Therefore, it can

be said that Rio Tinto ahs adopted the use of various measurement approaches as per the nature

of assets and liabilities and this has resulted in causing the issue of inconsistency in the financial

reporting of the company(Annual report : Rio Tinto Limited, 2018).

3: Evaluation of Relevance and Representational Faithfulness and their Importance in

Accounting for Assets and Liabilities

The conceptual accounting framework has presented two major qualitative principles that

need to be present within the financial reports for increasing their usefulness in economic

decision-making of investors. The relevancy as stated by the conceptual accounting framework

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

depicts that the financial information should be capable to support the decision-making of the

end users. The financial information should provide feedback and predictive value to the end-

users of an entity. The predictive value denotes that an entity must disclose the financial

information that is able to provide an estimate of its future cash flows. For example, the financial

information regarding the financial figures of sales and revenue that is disclosed within the

income statement of a company represents the predictive value. Also, the confirmatory value

denotes providing information that is able to confirm the past evaluations of a company. The

financial information by having predictive and confirmatory value must be able to make a

difference in the decision-making of the users.

On the other hand, faithful representation of information denotes that it should be

complete, free from any type of error and should be materially correct. The complete aspect of

the financial information signifies that a reader must be able to gain a clear picture of the

financial position of an entity (Bellandi, 2017). The error-free characteristic of the financial

information denotes that it should not have any error and depicts a fair view of an entity. The

relevance and faithful representation of financial information can be regarded as the two major

qualitative principles that need to be used by preparers during the time of developing and

presenting the financial information. It has been stated by the conceptual accounting framework

that an entity need to ensure that both the fundamental qualities must be present within the

financial reports and the selection of an accounting alternative must be based on the criteria of

meeting the reliability and relevancy of financial reporting (Ashford, 2011).

However, the major problem that exists in this regard for developers of financial report is

to meet both the qualitative criteria’s adequately. This is because making the financial

information too reliable can negatively impact its relevancy and vice-versa. For example,

accounting of assets and liabilities using the cost basis might result in making the financial

information more reliable but can have a negative impact on its relevancy. This is because

historical cost method of accounting can provide information on the basis of past evaluations and

therefore is not very useful for the investors to determine the future financial performance of an

entity. On the other hand, the use of fair valuation method can result in making information more

relevant for the investors to aid economic decision-making but make it less reliable for auditors

as it is based on future predictions and might not represent actual value of assets and liabilities in

the condition of presence of market volatility (Dye and Sridhar, 2010).

Therefore, the business entities are adopting the use of mixed model of accounting and as

such account certain assets and liabilities at historical cost while some are measured at fair value

of accounting. This helps them to achieve a tradeoff between both qualitative characteristics of

accounting for meeting the interest of its various stakeholders. The financial analysts and

investors regards relevancy to be most important criteria for accounting of assets and liabilities

whereas auditors regard representation of information in an effective manner as an important

criteria for accounting of financial items (Albrecht, Stice and Stice, 2010). The implications of

both these qualitative characteristics in developing high quality financial reports can be depicted

8

end users. The financial information should provide feedback and predictive value to the end-

users of an entity. The predictive value denotes that an entity must disclose the financial

information that is able to provide an estimate of its future cash flows. For example, the financial

information regarding the financial figures of sales and revenue that is disclosed within the

income statement of a company represents the predictive value. Also, the confirmatory value

denotes providing information that is able to confirm the past evaluations of a company. The

financial information by having predictive and confirmatory value must be able to make a

difference in the decision-making of the users.

On the other hand, faithful representation of information denotes that it should be

complete, free from any type of error and should be materially correct. The complete aspect of

the financial information signifies that a reader must be able to gain a clear picture of the

financial position of an entity (Bellandi, 2017). The error-free characteristic of the financial

information denotes that it should not have any error and depicts a fair view of an entity. The

relevance and faithful representation of financial information can be regarded as the two major

qualitative principles that need to be used by preparers during the time of developing and

presenting the financial information. It has been stated by the conceptual accounting framework

that an entity need to ensure that both the fundamental qualities must be present within the

financial reports and the selection of an accounting alternative must be based on the criteria of

meeting the reliability and relevancy of financial reporting (Ashford, 2011).

However, the major problem that exists in this regard for developers of financial report is

to meet both the qualitative criteria’s adequately. This is because making the financial

information too reliable can negatively impact its relevancy and vice-versa. For example,

accounting of assets and liabilities using the cost basis might result in making the financial

information more reliable but can have a negative impact on its relevancy. This is because

historical cost method of accounting can provide information on the basis of past evaluations and

therefore is not very useful for the investors to determine the future financial performance of an

entity. On the other hand, the use of fair valuation method can result in making information more

relevant for the investors to aid economic decision-making but make it less reliable for auditors

as it is based on future predictions and might not represent actual value of assets and liabilities in

the condition of presence of market volatility (Dye and Sridhar, 2010).

Therefore, the business entities are adopting the use of mixed model of accounting and as

such account certain assets and liabilities at historical cost while some are measured at fair value

of accounting. This helps them to achieve a tradeoff between both qualitative characteristics of

accounting for meeting the interest of its various stakeholders. The financial analysts and

investors regards relevancy to be most important criteria for accounting of assets and liabilities

whereas auditors regard representation of information in an effective manner as an important

criteria for accounting of financial items (Albrecht, Stice and Stice, 2010). The implications of

both these qualitative characteristics in developing high quality financial reports can be depicted

8

by analyzing the annual report of the selected company. Rio Tinto has also emphasized on

achieving a tradeoff between the two qualitative principles of conceptual framework by placing

emphasis on relevance in accounting of certain assets while on faithful presentation in

accounting of other assets. The company has presented the financial instruments, financial assets

and liabilities at fair value. This is because the use of fair valuation method can help in accurate

identification and recognition of these assets and liabilities due to presence of their active

market. On the other hand, the non-current assets and liabilities are measured at historical cost

due to absence of their active markets. Thus, it has adopted the use of mixed model of

accounting for measuring the value of assets and liabilities to ensure that the investors are able to

predict the future financial performance and auditors are able to assess the materially correctness

of the financial information (Annual report : Rio Tinto Limited, 2018). The fair valuation

approach can help in providing an estimate of the future cash flows associated with an asset

while historical method can help in confirming the present value of an asset on the basis of past

evaluation (Burlaud, 2013).

Conclusion

The report has inferred that business entities such as those listed on ASX that are

preparing their financial reports as per the IASB standards need to comply with qualitative

principle of conceptual framework. It has been examined on the basis of financial report of Rio

Tinto Limited, an ASX listed entity, that it has adopted qualitative features of accounting

framework for developing high quality financial reports. However, it has integrated the use of

mixed model of accounting for reporting of value of its assets and liabilities to achieve

congruence between the two above mentioned criteria of financial reporting.

9

achieving a tradeoff between the two qualitative principles of conceptual framework by placing

emphasis on relevance in accounting of certain assets while on faithful presentation in

accounting of other assets. The company has presented the financial instruments, financial assets

and liabilities at fair value. This is because the use of fair valuation method can help in accurate

identification and recognition of these assets and liabilities due to presence of their active

market. On the other hand, the non-current assets and liabilities are measured at historical cost

due to absence of their active markets. Thus, it has adopted the use of mixed model of

accounting for measuring the value of assets and liabilities to ensure that the investors are able to

predict the future financial performance and auditors are able to assess the materially correctness

of the financial information (Annual report : Rio Tinto Limited, 2018). The fair valuation

approach can help in providing an estimate of the future cash flows associated with an asset

while historical method can help in confirming the present value of an asset on the basis of past

evaluation (Burlaud, 2013).

Conclusion

The report has inferred that business entities such as those listed on ASX that are

preparing their financial reports as per the IASB standards need to comply with qualitative

principle of conceptual framework. It has been examined on the basis of financial report of Rio

Tinto Limited, an ASX listed entity, that it has adopted qualitative features of accounting

framework for developing high quality financial reports. However, it has integrated the use of

mixed model of accounting for reporting of value of its assets and liabilities to achieve

congruence between the two above mentioned criteria of financial reporting.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Albrecht, W., Stice, E. and Stice, J. 2010. Financial Accounting. UK: Cengage Learning.

Annual report. 2018. Rio Tinto Limited. [Online]. Available at:

http://www.riotinto.com/documents/RT_2018_annual_report.pdf [Accessed on: 23 May, 2019].

Ashford, C. 2011. Fair Value Accounting: It’s Impact on Financial Reporting and how it can be

enhanced to Provide More Clarity and Reliability of Information for Users of Financial

Statements. International Journal of Business and Social Science 2 (20), pp.12-19.

Bellandi, F. 2017. Materiality in Financial Reporting: An Integrative Perspective. UK: Emerald

Group Publishing.

Burlaud, A. 2013. Should Financial Statements Represent Fairly or be Relevant? [Online].

Available at: https://halshs.archives-ouvertes.fr/halshs-00873959/document [Accessed on: 26

May 2019].

Conceptual framework — Measurements and elements of financial statements. 2013. [Online].

Available at: https://www.iasplus.com/en/meeting-notes/iasb/2013/march/cf [Accessed on: 26

May 2018].

Conceptual Framework for Financial Reporting 2018. 2018. [Online]. Available at:

https://www.iasplus.com/en/standards/other/framework[Accessed on: 26 May 2019].

Dye, R. A., and Sridhar, S. S. 2010. Reliability-relevance trade-offs and the efficiency of

aggregation. Journal of Accounting Research, 42(1), 51-88.

Filipova, F. 2016. The Problem of Measurement in the Revised Conceptual Framework of IFRS.

International Conference on Application of Information and Communication Technology, pp. 2-

14.

Gassen, J and Schwedler, K. 2010. The Decision Usefulness of Financial Accounting

Measurement Concepts: Evidence from an Online Survey of Professional Investors and their

Advisors. European Accounting Review, 9(3),495-509.

10

Albrecht, W., Stice, E. and Stice, J. 2010. Financial Accounting. UK: Cengage Learning.

Annual report. 2018. Rio Tinto Limited. [Online]. Available at:

http://www.riotinto.com/documents/RT_2018_annual_report.pdf [Accessed on: 23 May, 2019].

Ashford, C. 2011. Fair Value Accounting: It’s Impact on Financial Reporting and how it can be

enhanced to Provide More Clarity and Reliability of Information for Users of Financial

Statements. International Journal of Business and Social Science 2 (20), pp.12-19.

Bellandi, F. 2017. Materiality in Financial Reporting: An Integrative Perspective. UK: Emerald

Group Publishing.

Burlaud, A. 2013. Should Financial Statements Represent Fairly or be Relevant? [Online].

Available at: https://halshs.archives-ouvertes.fr/halshs-00873959/document [Accessed on: 26

May 2019].

Conceptual framework — Measurements and elements of financial statements. 2013. [Online].

Available at: https://www.iasplus.com/en/meeting-notes/iasb/2013/march/cf [Accessed on: 26

May 2018].

Conceptual Framework for Financial Reporting 2018. 2018. [Online]. Available at:

https://www.iasplus.com/en/standards/other/framework[Accessed on: 26 May 2019].

Dye, R. A., and Sridhar, S. S. 2010. Reliability-relevance trade-offs and the efficiency of

aggregation. Journal of Accounting Research, 42(1), 51-88.

Filipova, F. 2016. The Problem of Measurement in the Revised Conceptual Framework of IFRS.

International Conference on Application of Information and Communication Technology, pp. 2-

14.

Gassen, J and Schwedler, K. 2010. The Decision Usefulness of Financial Accounting

Measurement Concepts: Evidence from an Online Survey of Professional Investors and their

Advisors. European Accounting Review, 9(3),495-509.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Grüber, S. 2014. Intangible Values in Financial Accounting and Reporting: An Analysis from the

Perspective of Financial Analysts. Switzerland: Springer.

Hopwood, T. 2013. Accounting From the Outside (RLE Accounting): The Collected Papers of

Anthony G. Hopwood. London: Routledge.

ICAEW. 2016. Measurement in financial reporting. [Online]. Available at:

https://www.icaew.com/-/media/corporate/files/technical/financial-reporting/information-for-

better-markets/ifbm-reports/measurement-in-financial-reporting.ashx [Accessed on: 26 May

2018].

IFRS. 2017. Measurement uncertainty and the fundamental qualitative characteristics of useful

financial information. [Online]. Available at:

https://www.ifrs.org/-/media/feature/meetings/2017/september/iasb/cf/ap10-conceptual-

framework.pdf[Accessed on: 26 May 2019].

International Accounting Standards Board. 2016. Measurement Bases for Financial Accounting.

[Online]. Available at: https://www.efrag.org/Assets/Download?assetUrl=%2Fsites

%2Fwebpublishing%2FProject%20Documents%2F53%2FDP%20Measurement%20on

%20Initial%20Recognition.pdf [Accessed on: 26 May 2018].

Mirza, A. and Knorr, L. 2011. Wiley IFRS: Practical Implementation Guide and Workbook.

USA: John Wiley & Sons.

Needles, B.E., Powers, M. and Crosson, S.V. 2013. Principles of Accounting. UK: Cengage

Learning.

Sadowska, B. 2016. Measuring and valuation in accounting – theoretical basis and contemporary

dilemmas. World Scientific News 56, pp. 247-256.

Wahlen, J., Baginski, S. and Bradshaw, M. 2017. Financial Reporting, Financial Statement

Analysis and Valuation. USA: Cengage Learning.

Wolk, H., Dodd, J.L. and Rozycki, J. 2016. Accounting Theory: Conceptual Issues in a Political

and Economic Environment. USA: SAGE Publications.

11

Perspective of Financial Analysts. Switzerland: Springer.

Hopwood, T. 2013. Accounting From the Outside (RLE Accounting): The Collected Papers of

Anthony G. Hopwood. London: Routledge.

ICAEW. 2016. Measurement in financial reporting. [Online]. Available at:

https://www.icaew.com/-/media/corporate/files/technical/financial-reporting/information-for-

better-markets/ifbm-reports/measurement-in-financial-reporting.ashx [Accessed on: 26 May

2018].

IFRS. 2017. Measurement uncertainty and the fundamental qualitative characteristics of useful

financial information. [Online]. Available at:

https://www.ifrs.org/-/media/feature/meetings/2017/september/iasb/cf/ap10-conceptual-

framework.pdf[Accessed on: 26 May 2019].

International Accounting Standards Board. 2016. Measurement Bases for Financial Accounting.

[Online]. Available at: https://www.efrag.org/Assets/Download?assetUrl=%2Fsites

%2Fwebpublishing%2FProject%20Documents%2F53%2FDP%20Measurement%20on

%20Initial%20Recognition.pdf [Accessed on: 26 May 2018].

Mirza, A. and Knorr, L. 2011. Wiley IFRS: Practical Implementation Guide and Workbook.

USA: John Wiley & Sons.

Needles, B.E., Powers, M. and Crosson, S.V. 2013. Principles of Accounting. UK: Cengage

Learning.

Sadowska, B. 2016. Measuring and valuation in accounting – theoretical basis and contemporary

dilemmas. World Scientific News 56, pp. 247-256.

Wahlen, J., Baginski, S. and Bradshaw, M. 2017. Financial Reporting, Financial Statement

Analysis and Valuation. USA: Cengage Learning.

Wolk, H., Dodd, J.L. and Rozycki, J. 2016. Accounting Theory: Conceptual Issues in a Political

and Economic Environment. USA: SAGE Publications.

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.