Advance Financial Accounting Assignment: AASB 138 and Superannuation

VerifiedAdded on 2020/03/15

|12

|3221

|38

Homework Assignment

AI Summary

This document presents a comprehensive solution to an Advance Financial Accounting assignment. It begins with a discussion on fair value measurement, including valuation techniques for land, and journal entries for property, plant, and equipment. The assignment delves into the accounting treatment of intangible assets, exploring the impact of internally generated assets under AASB 138/IAS 38, the differences between acquired and internally generated intangibles, and the reasons companies may be reluctant to change. Furthermore, the document provides a detailed analysis of a defined benefit superannuation plan, including calculations for surplus/deficit, net asset/liability, net interest, and reconciliation of balances, along with the corresponding journal entries. The solution incorporates references to relevant accounting standards and literature.

Running head: ADVANCE FINANCIAL ACCOUNTING

Advance Financial Accounting

Name of the Student:

Name of the University:

Authors Note:

Advance Financial Accounting

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCE FINANCIAL ACCOUNTING

1

Table of Contents

Question 1: Stating the measures used in identifying fair value................................................2

Question 2:.................................................................................................................................3

1. Peewee Ltd journal entries for the year ended 30 June 2017:................................................3

2. Peewee Ltd journal entries for the year ended 30 June 2018:................................................4

Question 3:.................................................................................................................................6

1. Stating the impact of internally generated intangible assets in AASB 138/IAS 38:..............6

2. Difference between accounting for internally generated intangible assets and acquired

intangible assets in AASB 138/IAS 38:.....................................................................................7

3. Mentioning the reasons behind companies being reluctant to change in AASB 138/IAS 38:

....................................................................................................................................................7

Question 4:.................................................................................................................................8

1. Revealing the surplus or deficit of Wattle Ltd’s defined benefit plan at 31 December 2016:

....................................................................................................................................................8

2. Mentioning the net defined benefit asset or liability at 31 December 2016:.........................9

3. Stating the net interest and the return on plan assets in 31 December 2016:.........................9

4. Providing reconciliation regarding opening balance and closing balance of the net defined

benefit liability:..........................................................................................................................9

5. Drafting journal entry to defined benefit superannuation plan in the books of Wattle Ltd for

the year ended 31 December 2016:..........................................................................................10

Reference and Bibliography:....................................................................................................12

1

Table of Contents

Question 1: Stating the measures used in identifying fair value................................................2

Question 2:.................................................................................................................................3

1. Peewee Ltd journal entries for the year ended 30 June 2017:................................................3

2. Peewee Ltd journal entries for the year ended 30 June 2018:................................................4

Question 3:.................................................................................................................................6

1. Stating the impact of internally generated intangible assets in AASB 138/IAS 38:..............6

2. Difference between accounting for internally generated intangible assets and acquired

intangible assets in AASB 138/IAS 38:.....................................................................................7

3. Mentioning the reasons behind companies being reluctant to change in AASB 138/IAS 38:

....................................................................................................................................................7

Question 4:.................................................................................................................................8

1. Revealing the surplus or deficit of Wattle Ltd’s defined benefit plan at 31 December 2016:

....................................................................................................................................................8

2. Mentioning the net defined benefit asset or liability at 31 December 2016:.........................9

3. Stating the net interest and the return on plan assets in 31 December 2016:.........................9

4. Providing reconciliation regarding opening balance and closing balance of the net defined

benefit liability:..........................................................................................................................9

5. Drafting journal entry to defined benefit superannuation plan in the books of Wattle Ltd for

the year ended 31 December 2016:..........................................................................................10

Reference and Bibliography:....................................................................................................12

ADVANCE FINANCIAL ACCOUNTING

2

Question 1: Stating the measures used in identifying fair value

The highest valuation of the property is considered:

From the evaluation of the case study it could be identified that if the plot is sold for

residential purposes then the overall and will provide $1,000,000 in revenue. However, there

is relevant estimation of cost for demolition it needs to be incurred by the company, which

amounts to $100,000. Therefore, from the evaluation it could be identified that there are

relevant income that could be provided from the plot is $900,000. Furthermore, if the

property can be used for factory purposes or outlet the relevant cost of $780,000 will be

initiated for building a new factory. However, the existing factory will only cost $390,000 for

the firm, which is relatively lower than the residential plot price. Hence, using the plot for

residential purposes will eventually allow the organisation generate higher revenue from

sales. Consequently, the highest valuation is mainly identified as residential valuation

(Ramachandra, 2017).

Mentioning the overall benefit for selling the plot in market value:

From the evaluation it could be identified that using the property for residential

purposes would eventually allow the organisation to improve its current revenue generation

capacity.

Stating whether the asset is subject to measurement:

The evaluation directly indicates that there are two different types of valuation that

could be conducted for identifying the overall value of the asset. The first valuation could be

conducted only on the premises singly, which would help in identifying the actual value of

the asset. The other valuation directly indicates that both the premises and factory will be

valued separately to identify the total value of the asset (Rooney & Dumay, 2016).

Mentioning the adequately valuation techniques:

2

Question 1: Stating the measures used in identifying fair value

The highest valuation of the property is considered:

From the evaluation of the case study it could be identified that if the plot is sold for

residential purposes then the overall and will provide $1,000,000 in revenue. However, there

is relevant estimation of cost for demolition it needs to be incurred by the company, which

amounts to $100,000. Therefore, from the evaluation it could be identified that there are

relevant income that could be provided from the plot is $900,000. Furthermore, if the

property can be used for factory purposes or outlet the relevant cost of $780,000 will be

initiated for building a new factory. However, the existing factory will only cost $390,000 for

the firm, which is relatively lower than the residential plot price. Hence, using the plot for

residential purposes will eventually allow the organisation generate higher revenue from

sales. Consequently, the highest valuation is mainly identified as residential valuation

(Ramachandra, 2017).

Mentioning the overall benefit for selling the plot in market value:

From the evaluation it could be identified that using the property for residential

purposes would eventually allow the organisation to improve its current revenue generation

capacity.

Stating whether the asset is subject to measurement:

The evaluation directly indicates that there are two different types of valuation that

could be conducted for identifying the overall value of the asset. The first valuation could be

conducted only on the premises singly, which would help in identifying the actual value of

the asset. The other valuation directly indicates that both the premises and factory will be

valued separately to identify the total value of the asset (Rooney & Dumay, 2016).

Mentioning the adequately valuation techniques:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCE FINANCIAL ACCOUNTING

3

There are two types of valuation approaches that need to be conducted for deriving

the fair value of the land, which includes residential valuation approach and industrial

valuation property. However the residential valuation approach only includes the plot and

excludes the factory, which is situated on the plot. This relevant valuation only needs to

evaluate the plot on the basis of residential valuation, which is relevantly at $900,000. The

second valuation mainly depicts the industrial valuation approach which directly evaluates a

possibility of factory on the plot. However, the evaluation of the residential plot is relatively

higher against any other valuation, which directly indicates that the company should use the

residential valuation approach for identifying the fair value of the land (Sugiyama & Islam,

2016).

Question 2:

1. Peewee Ltd journal entries for the year ended 30 June 2017:

1st July

2016

Machine A...........................................................Dr

Machine B...........................................................Dr

Cash........................................................Cr

100,000

60,000

160,000

30th June

2017

Depreciation-Machine A................................................Dr

Accumulated Depreciation............................Cr

(1/5 * $100,000 = $20,000)

20,000

20,000

Depreciation-Machine B................................................Dr

Accumulated Depreciation.............................Cr

(1/3 * $60,000 = $20,000)

20,000

20,000

Accumulated Depreciation Machine A..........................Dr 20,000

3

There are two types of valuation approaches that need to be conducted for deriving

the fair value of the land, which includes residential valuation approach and industrial

valuation property. However the residential valuation approach only includes the plot and

excludes the factory, which is situated on the plot. This relevant valuation only needs to

evaluate the plot on the basis of residential valuation, which is relevantly at $900,000. The

second valuation mainly depicts the industrial valuation approach which directly evaluates a

possibility of factory on the plot. However, the evaluation of the residential plot is relatively

higher against any other valuation, which directly indicates that the company should use the

residential valuation approach for identifying the fair value of the land (Sugiyama & Islam,

2016).

Question 2:

1. Peewee Ltd journal entries for the year ended 30 June 2017:

1st July

2016

Machine A...........................................................Dr

Machine B...........................................................Dr

Cash........................................................Cr

100,000

60,000

160,000

30th June

2017

Depreciation-Machine A................................................Dr

Accumulated Depreciation............................Cr

(1/5 * $100,000 = $20,000)

20,000

20,000

Depreciation-Machine B................................................Dr

Accumulated Depreciation.............................Cr

(1/3 * $60,000 = $20,000)

20,000

20,000

Accumulated Depreciation Machine A..........................Dr 20,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCE FINANCIAL ACCOUNTING

4

Machine A...................................................Cr

(being writing down the carrying amount)

20,000

Machine A.................................................................Dr

Gain on revaluation of Machine A (OCI)........Cr

(being revaluation of increment $80,000 to $84,000)

4,000

4,000

Gain on revaluation of Machine A (OCI)........................Dr

Asset revaluation surplus Machine A..............Cr

(being increase in net revaluation gain in equity)

4,000

4,000

Accumulated Depreciation Machine B..........................Dr

Machine B...................................................Cr

(being writing down the carrying amount)

20,000

20,000

Loss on revaluation-Machine B....................................Dr

Machine B...................................................Cr

(being revaluation to fair value at 30-06-17)

2,000

2,000

2. Peewee Ltd journal entries for the year ended 30 June 2018:

1st

January

2018

Machine C..................................................................Dr

Cash...............................................................Cr

(being acquisition of machine C)

80,000

80,000

Depreciation expense-Machine B.................................Dr

Accumulated Depreciation............................Cr

(1/2 * 1/2 * $38,000 = $9,500)

9,500

9,500

Cash..........................................................................Dr

Proceeds from sale of Machine B....................Cr

29,000

29,000

4

Machine A...................................................Cr

(being writing down the carrying amount)

20,000

Machine A.................................................................Dr

Gain on revaluation of Machine A (OCI)........Cr

(being revaluation of increment $80,000 to $84,000)

4,000

4,000

Gain on revaluation of Machine A (OCI)........................Dr

Asset revaluation surplus Machine A..............Cr

(being increase in net revaluation gain in equity)

4,000

4,000

Accumulated Depreciation Machine B..........................Dr

Machine B...................................................Cr

(being writing down the carrying amount)

20,000

20,000

Loss on revaluation-Machine B....................................Dr

Machine B...................................................Cr

(being revaluation to fair value at 30-06-17)

2,000

2,000

2. Peewee Ltd journal entries for the year ended 30 June 2018:

1st

January

2018

Machine C..................................................................Dr

Cash...............................................................Cr

(being acquisition of machine C)

80,000

80,000

Depreciation expense-Machine B.................................Dr

Accumulated Depreciation............................Cr

(1/2 * 1/2 * $38,000 = $9,500)

9,500

9,500

Cash..........................................................................Dr

Proceeds from sale of Machine B....................Cr

29,000

29,000

ADVANCE FINANCIAL ACCOUNTING

5

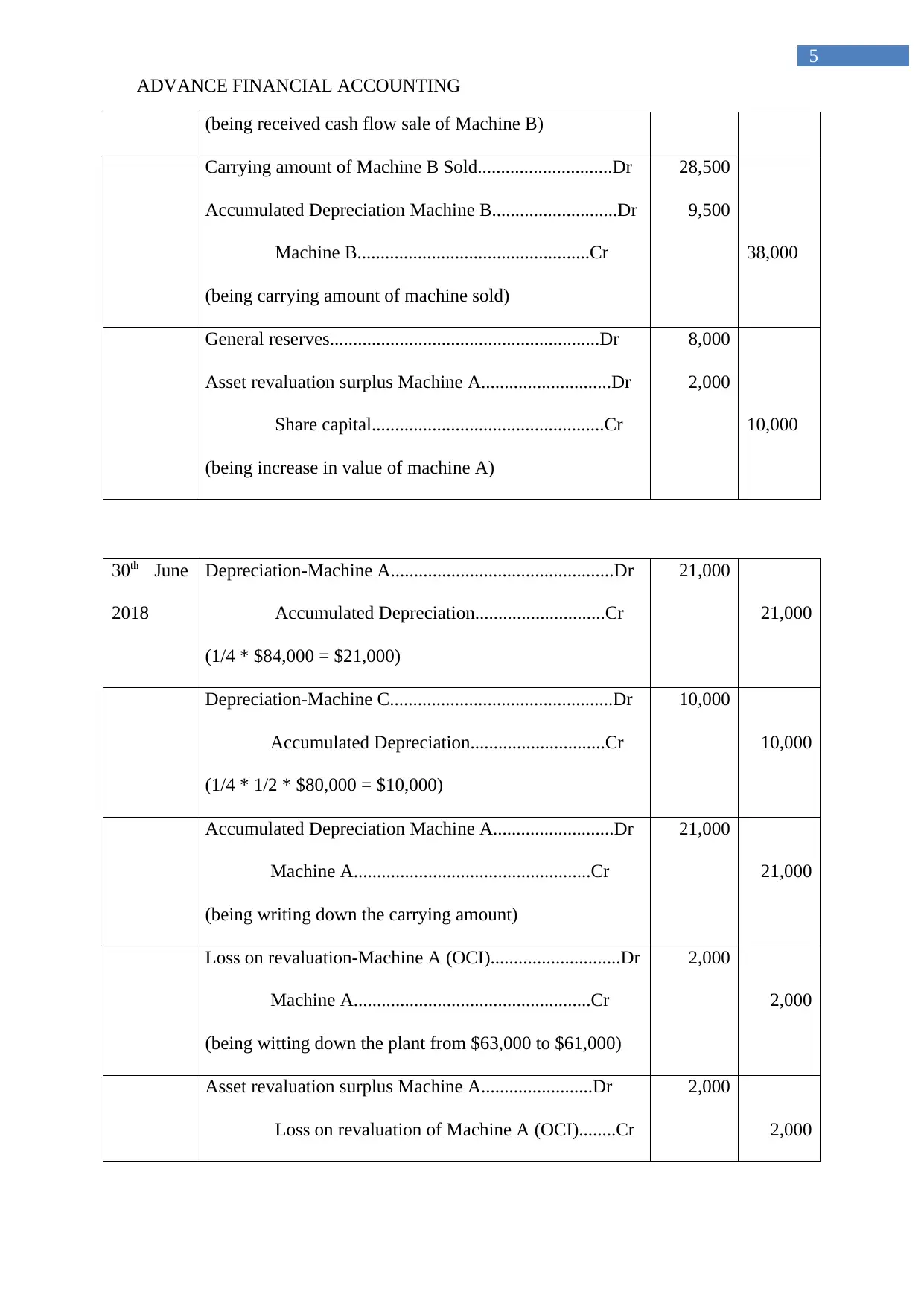

(being received cash flow sale of Machine B)

Carrying amount of Machine B Sold.............................Dr

Accumulated Depreciation Machine B...........................Dr

Machine B..................................................Cr

(being carrying amount of machine sold)

28,500

9,500

38,000

General reserves..........................................................Dr

Asset revaluation surplus Machine A............................Dr

Share capital..................................................Cr

(being increase in value of machine A)

8,000

2,000

10,000

30th June

2018

Depreciation-Machine A................................................Dr

Accumulated Depreciation............................Cr

(1/4 * $84,000 = $21,000)

21,000

21,000

Depreciation-Machine C................................................Dr

Accumulated Depreciation.............................Cr

(1/4 * 1/2 * $80,000 = $10,000)

10,000

10,000

Accumulated Depreciation Machine A..........................Dr

Machine A...................................................Cr

(being writing down the carrying amount)

21,000

21,000

Loss on revaluation-Machine A (OCI)............................Dr

Machine A...................................................Cr

(being witting down the plant from $63,000 to $61,000)

2,000

2,000

Asset revaluation surplus Machine A........................Dr

Loss on revaluation of Machine A (OCI)........Cr

2,000

2,000

5

(being received cash flow sale of Machine B)

Carrying amount of Machine B Sold.............................Dr

Accumulated Depreciation Machine B...........................Dr

Machine B..................................................Cr

(being carrying amount of machine sold)

28,500

9,500

38,000

General reserves..........................................................Dr

Asset revaluation surplus Machine A............................Dr

Share capital..................................................Cr

(being increase in value of machine A)

8,000

2,000

10,000

30th June

2018

Depreciation-Machine A................................................Dr

Accumulated Depreciation............................Cr

(1/4 * $84,000 = $21,000)

21,000

21,000

Depreciation-Machine C................................................Dr

Accumulated Depreciation.............................Cr

(1/4 * 1/2 * $80,000 = $10,000)

10,000

10,000

Accumulated Depreciation Machine A..........................Dr

Machine A...................................................Cr

(being writing down the carrying amount)

21,000

21,000

Loss on revaluation-Machine A (OCI)............................Dr

Machine A...................................................Cr

(being witting down the plant from $63,000 to $61,000)

2,000

2,000

Asset revaluation surplus Machine A........................Dr

Loss on revaluation of Machine A (OCI)........Cr

2,000

2,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCE FINANCIAL ACCOUNTING

6

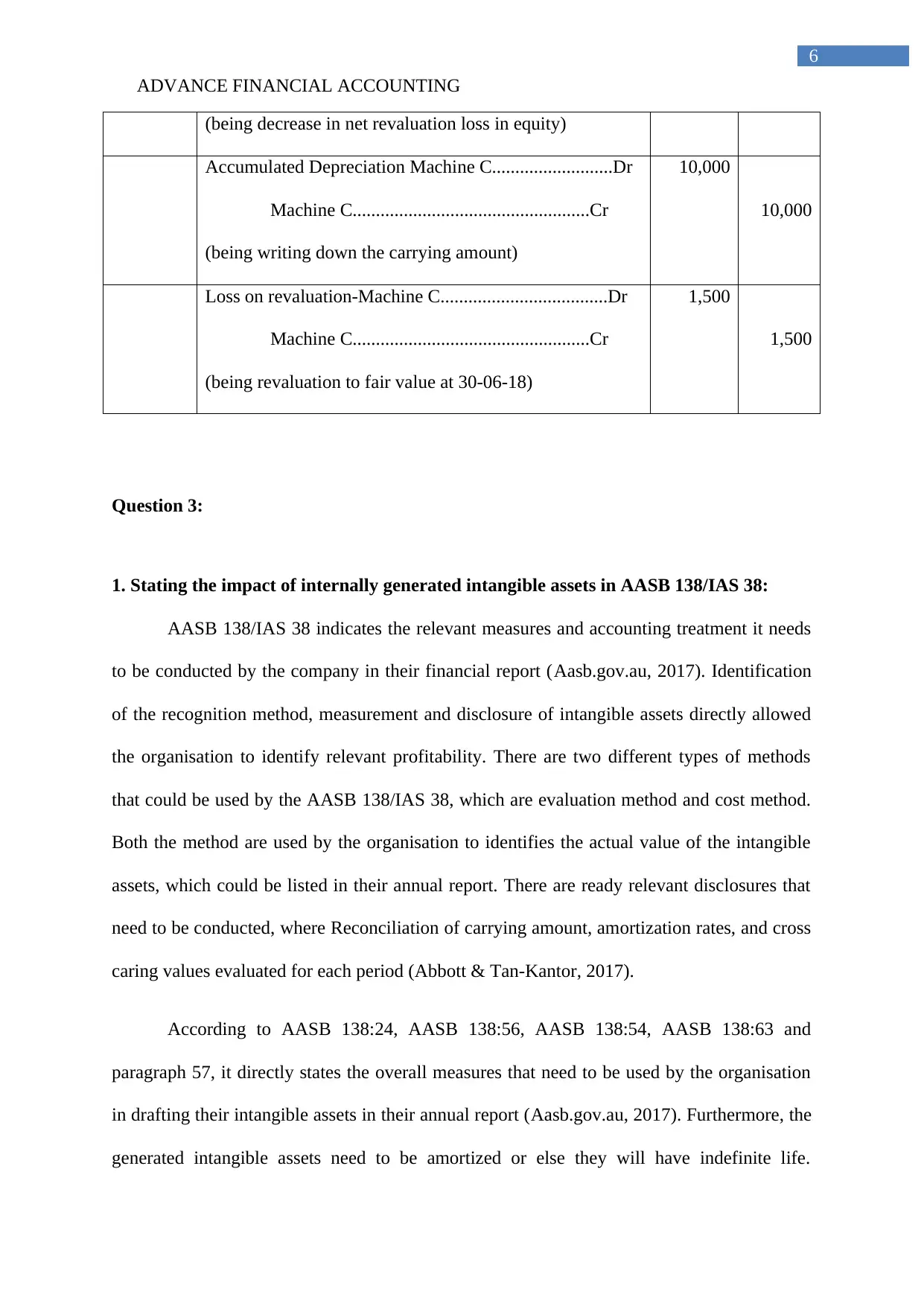

(being decrease in net revaluation loss in equity)

Accumulated Depreciation Machine C..........................Dr

Machine C...................................................Cr

(being writing down the carrying amount)

10,000

10,000

Loss on revaluation-Machine C....................................Dr

Machine C...................................................Cr

(being revaluation to fair value at 30-06-18)

1,500

1,500

Question 3:

1. Stating the impact of internally generated intangible assets in AASB 138/IAS 38:

AASB 138/IAS 38 indicates the relevant measures and accounting treatment it needs

to be conducted by the company in their financial report (Aasb.gov.au, 2017). Identification

of the recognition method, measurement and disclosure of intangible assets directly allowed

the organisation to identify relevant profitability. There are two different types of methods

that could be used by the AASB 138/IAS 38, which are evaluation method and cost method.

Both the method are used by the organisation to identifies the actual value of the intangible

assets, which could be listed in their annual report. There are ready relevant disclosures that

need to be conducted, where Reconciliation of carrying amount, amortization rates, and cross

caring values evaluated for each period (Abbott & Tan‐Kantor, 2017).

According to AASB 138:24, AASB 138:56, AASB 138:54, AASB 138:63 and

paragraph 57, it directly states the overall measures that need to be used by the organisation

in drafting their intangible assets in their annual report (Aasb.gov.au, 2017). Furthermore, the

generated intangible assets need to be amortized or else they will have indefinite life.

6

(being decrease in net revaluation loss in equity)

Accumulated Depreciation Machine C..........................Dr

Machine C...................................................Cr

(being writing down the carrying amount)

10,000

10,000

Loss on revaluation-Machine C....................................Dr

Machine C...................................................Cr

(being revaluation to fair value at 30-06-18)

1,500

1,500

Question 3:

1. Stating the impact of internally generated intangible assets in AASB 138/IAS 38:

AASB 138/IAS 38 indicates the relevant measures and accounting treatment it needs

to be conducted by the company in their financial report (Aasb.gov.au, 2017). Identification

of the recognition method, measurement and disclosure of intangible assets directly allowed

the organisation to identify relevant profitability. There are two different types of methods

that could be used by the AASB 138/IAS 38, which are evaluation method and cost method.

Both the method are used by the organisation to identifies the actual value of the intangible

assets, which could be listed in their annual report. There are ready relevant disclosures that

need to be conducted, where Reconciliation of carrying amount, amortization rates, and cross

caring values evaluated for each period (Abbott & Tan‐Kantor, 2017).

According to AASB 138:24, AASB 138:56, AASB 138:54, AASB 138:63 and

paragraph 57, it directly states the overall measures that need to be used by the organisation

in drafting their intangible assets in their annual report (Aasb.gov.au, 2017). Furthermore, the

generated intangible assets need to be amortized or else they will have indefinite life.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCE FINANCIAL ACCOUNTING

7

Moreover, the intangible assets needs to be evaluated based on cost, which could directly

help in evaluating the actual intangible assets value of an organisation.

2. Difference between accounting for internally generated intangible assets and

acquired intangible assets in AASB 138/IAS 38:

The major difference in generated intangible and acquired intangible assets are mainly

depicted as follows.

Acquired intangible assets can we evaluated under fair value and adequately measured in

annual report of an organisation.

In paragraph 63, relevant measures regarding intangible assets are depicted, which

directly indicates that acquired intangible assets and not considered as internally

generated intangible assets of an organisation (Aasb.gov.au, 2017).

The treatment of the intangible assets after the recognition as internally generated or

acquired is relatively same.

Lastly, with the help of the recognition method internally generated intangible assets can

be valued. Moreover, acquired intangible assets valuation is may be conducted under fair

value method, which is directly depicted in the annual report (Garg, 2017).

3. Mentioning the reasons behind companies being reluctant to change in AASB

138/IAS 38:

There are relevantly reasons where the organisation does not want to impose AASB

138/IAS 38 in their annual report. The reasons are mainly depicted as follows.

Investors many consider number of largest to be adequate and better than the periodic

amortization, where onetime write-off could directly allow the investors to identify the

7

Moreover, the intangible assets needs to be evaluated based on cost, which could directly

help in evaluating the actual intangible assets value of an organisation.

2. Difference between accounting for internally generated intangible assets and

acquired intangible assets in AASB 138/IAS 38:

The major difference in generated intangible and acquired intangible assets are mainly

depicted as follows.

Acquired intangible assets can we evaluated under fair value and adequately measured in

annual report of an organisation.

In paragraph 63, relevant measures regarding intangible assets are depicted, which

directly indicates that acquired intangible assets and not considered as internally

generated intangible assets of an organisation (Aasb.gov.au, 2017).

The treatment of the intangible assets after the recognition as internally generated or

acquired is relatively same.

Lastly, with the help of the recognition method internally generated intangible assets can

be valued. Moreover, acquired intangible assets valuation is may be conducted under fair

value method, which is directly depicted in the annual report (Garg, 2017).

3. Mentioning the reasons behind companies being reluctant to change in AASB

138/IAS 38:

There are relevantly reasons where the organisation does not want to impose AASB

138/IAS 38 in their annual report. The reasons are mainly depicted as follows.

Investors many consider number of largest to be adequate and better than the periodic

amortization, where onetime write-off could directly allow the investors to identify the

ADVANCE FINANCIAL ACCOUNTING

8

profitability of subsequent years. Therefore, the implementation of AASB 138/IAS 38

could directly hinder valuation of the investors (Aasb.gov.au, 2017).

Majority of the Investments Research and Development are written off by the

organisation and their annual report, where adequate valuation could directly be written-

off rather than amortized later.

Moreover, AASB 138/IAS 38 could also reduce the gap between capital costs and

expected future benefits, as valuation of the intangible assets will be conducted

adequately and no knowledge based asset will be measured.

Furthermore, AASB 138/IAS 38 will directly forces the organisation to write-off assets

when denotes failure, which is directly avoided by managers, as relevant questions and

lawsuits will be conducted. Hence, the use of AASB 138/IAS 38 will directly increase

failure of the organisation, which will attract more attention (Kabir & Rahman, 2016).

Question 4:

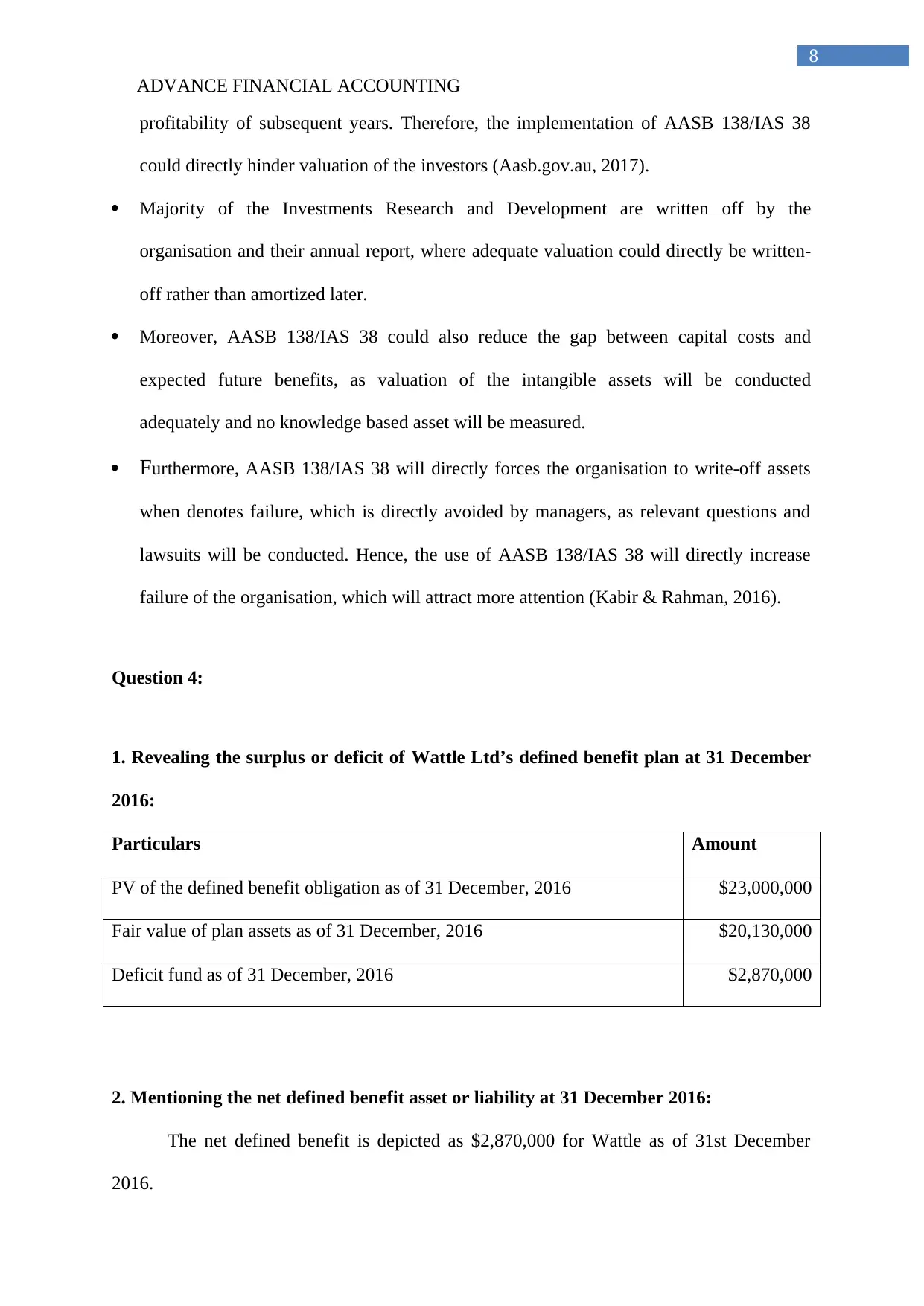

1. Revealing the surplus or deficit of Wattle Ltd’s defined benefit plan at 31 December

2016:

Particulars Amount

PV of the defined benefit obligation as of 31 December, 2016 $23,000,000

Fair value of plan assets as of 31 December, 2016 $20,130,000

Deficit fund as of 31 December, 2016 $2,870,000

2. Mentioning the net defined benefit asset or liability at 31 December 2016:

The net defined benefit is depicted as $2,870,000 for Wattle as of 31st December

2016.

8

profitability of subsequent years. Therefore, the implementation of AASB 138/IAS 38

could directly hinder valuation of the investors (Aasb.gov.au, 2017).

Majority of the Investments Research and Development are written off by the

organisation and their annual report, where adequate valuation could directly be written-

off rather than amortized later.

Moreover, AASB 138/IAS 38 could also reduce the gap between capital costs and

expected future benefits, as valuation of the intangible assets will be conducted

adequately and no knowledge based asset will be measured.

Furthermore, AASB 138/IAS 38 will directly forces the organisation to write-off assets

when denotes failure, which is directly avoided by managers, as relevant questions and

lawsuits will be conducted. Hence, the use of AASB 138/IAS 38 will directly increase

failure of the organisation, which will attract more attention (Kabir & Rahman, 2016).

Question 4:

1. Revealing the surplus or deficit of Wattle Ltd’s defined benefit plan at 31 December

2016:

Particulars Amount

PV of the defined benefit obligation as of 31 December, 2016 $23,000,000

Fair value of plan assets as of 31 December, 2016 $20,130,000

Deficit fund as of 31 December, 2016 $2,870,000

2. Mentioning the net defined benefit asset or liability at 31 December 2016:

The net defined benefit is depicted as $2,870,000 for Wattle as of 31st December

2016.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCE FINANCIAL ACCOUNTING

9

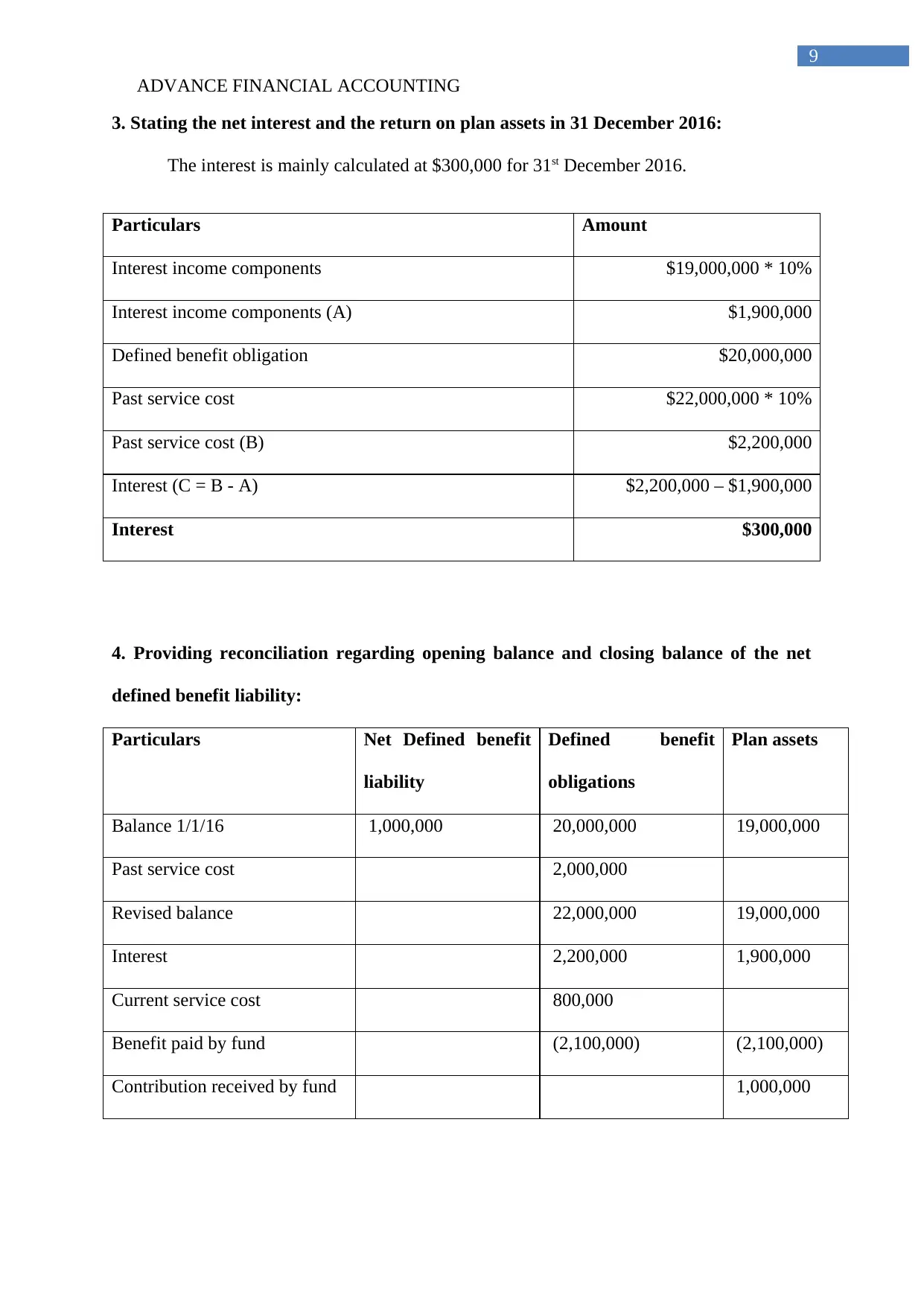

3. Stating the net interest and the return on plan assets in 31 December 2016:

The interest is mainly calculated at $300,000 for 31st December 2016.

Particulars Amount

Interest income components $19,000,000 * 10%

Interest income components (A) $1,900,000

Defined benefit obligation $20,000,000

Past service cost $22,000,000 * 10%

Past service cost (B) $2,200,000

Interest (C = B - A) $2,200,000 – $1,900,000

Interest $300,000

4. Providing reconciliation regarding opening balance and closing balance of the net

defined benefit liability:

Particulars Net Defined benefit

liability

Defined benefit

obligations

Plan assets

Balance 1/1/16 1,000,000 20,000,000 19,000,000

Past service cost 2,000,000

Revised balance 22,000,000 19,000,000

Interest 2,200,000 1,900,000

Current service cost 800,000

Benefit paid by fund (2,100,000) (2,100,000)

Contribution received by fund 1,000,000

9

3. Stating the net interest and the return on plan assets in 31 December 2016:

The interest is mainly calculated at $300,000 for 31st December 2016.

Particulars Amount

Interest income components $19,000,000 * 10%

Interest income components (A) $1,900,000

Defined benefit obligation $20,000,000

Past service cost $22,000,000 * 10%

Past service cost (B) $2,200,000

Interest (C = B - A) $2,200,000 – $1,900,000

Interest $300,000

4. Providing reconciliation regarding opening balance and closing balance of the net

defined benefit liability:

Particulars Net Defined benefit

liability

Defined benefit

obligations

Plan assets

Balance 1/1/16 1,000,000 20,000,000 19,000,000

Past service cost 2,000,000

Revised balance 22,000,000 19,000,000

Interest 2,200,000 1,900,000

Current service cost 800,000

Benefit paid by fund (2,100,000) (2,100,000)

Contribution received by fund 1,000,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCE FINANCIAL ACCOUNTING

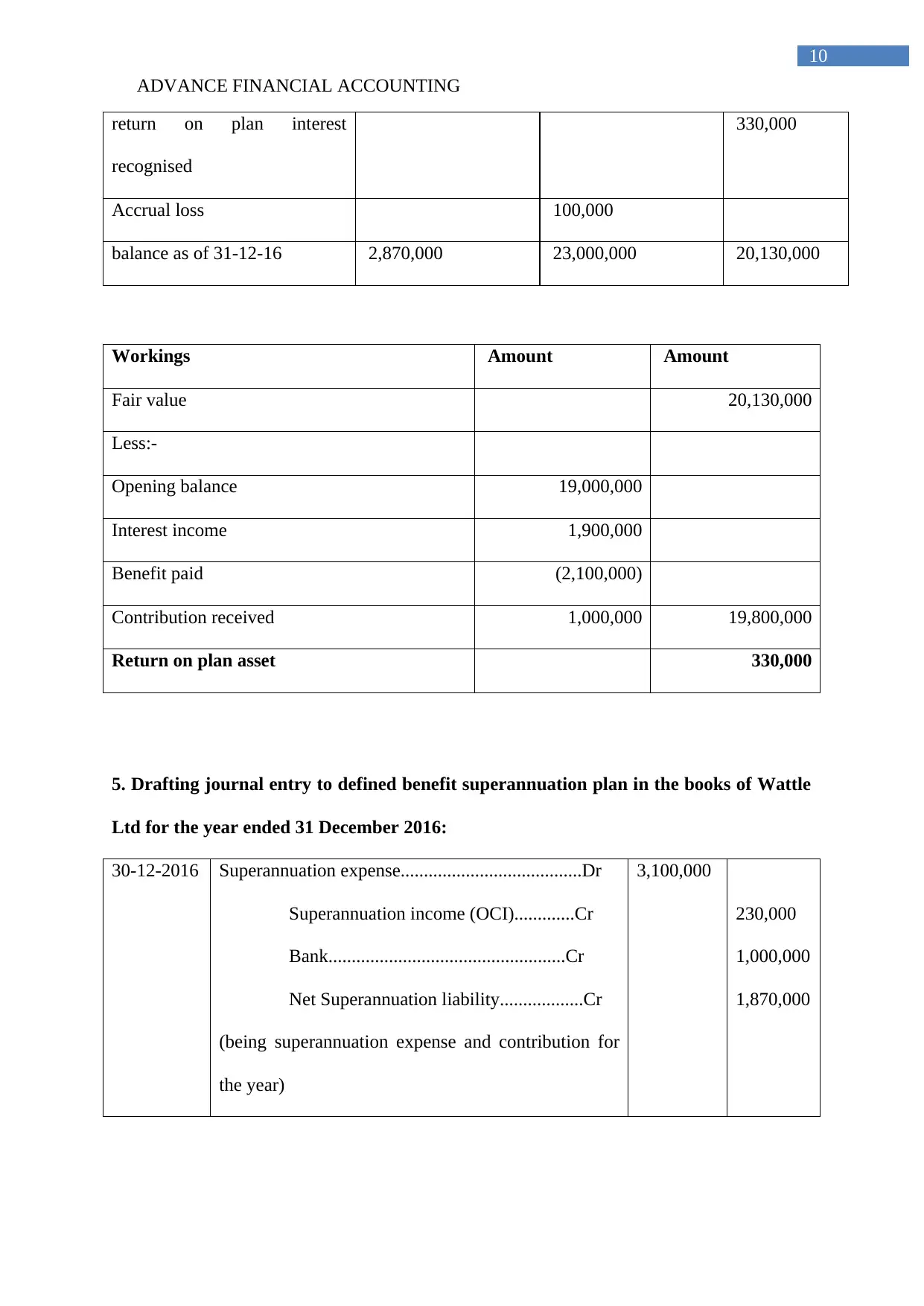

10

return on plan interest

recognised

330,000

Accrual loss 100,000

balance as of 31-12-16 2,870,000 23,000,000 20,130,000

Workings Amount Amount

Fair value 20,130,000

Less:-

Opening balance 19,000,000

Interest income 1,900,000

Benefit paid (2,100,000)

Contribution received 1,000,000 19,800,000

Return on plan asset 330,000

5. Drafting journal entry to defined benefit superannuation plan in the books of Wattle

Ltd for the year ended 31 December 2016:

30-12-2016 Superannuation expense.......................................Dr

Superannuation income (OCI).............Cr

Bank...................................................Cr

Net Superannuation liability..................Cr

(being superannuation expense and contribution for

the year)

3,100,000

230,000

1,000,000

1,870,000

10

return on plan interest

recognised

330,000

Accrual loss 100,000

balance as of 31-12-16 2,870,000 23,000,000 20,130,000

Workings Amount Amount

Fair value 20,130,000

Less:-

Opening balance 19,000,000

Interest income 1,900,000

Benefit paid (2,100,000)

Contribution received 1,000,000 19,800,000

Return on plan asset 330,000

5. Drafting journal entry to defined benefit superannuation plan in the books of Wattle

Ltd for the year ended 31 December 2016:

30-12-2016 Superannuation expense.......................................Dr

Superannuation income (OCI).............Cr

Bank...................................................Cr

Net Superannuation liability..................Cr

(being superannuation expense and contribution for

the year)

3,100,000

230,000

1,000,000

1,870,000

ADVANCE FINANCIAL ACCOUNTING

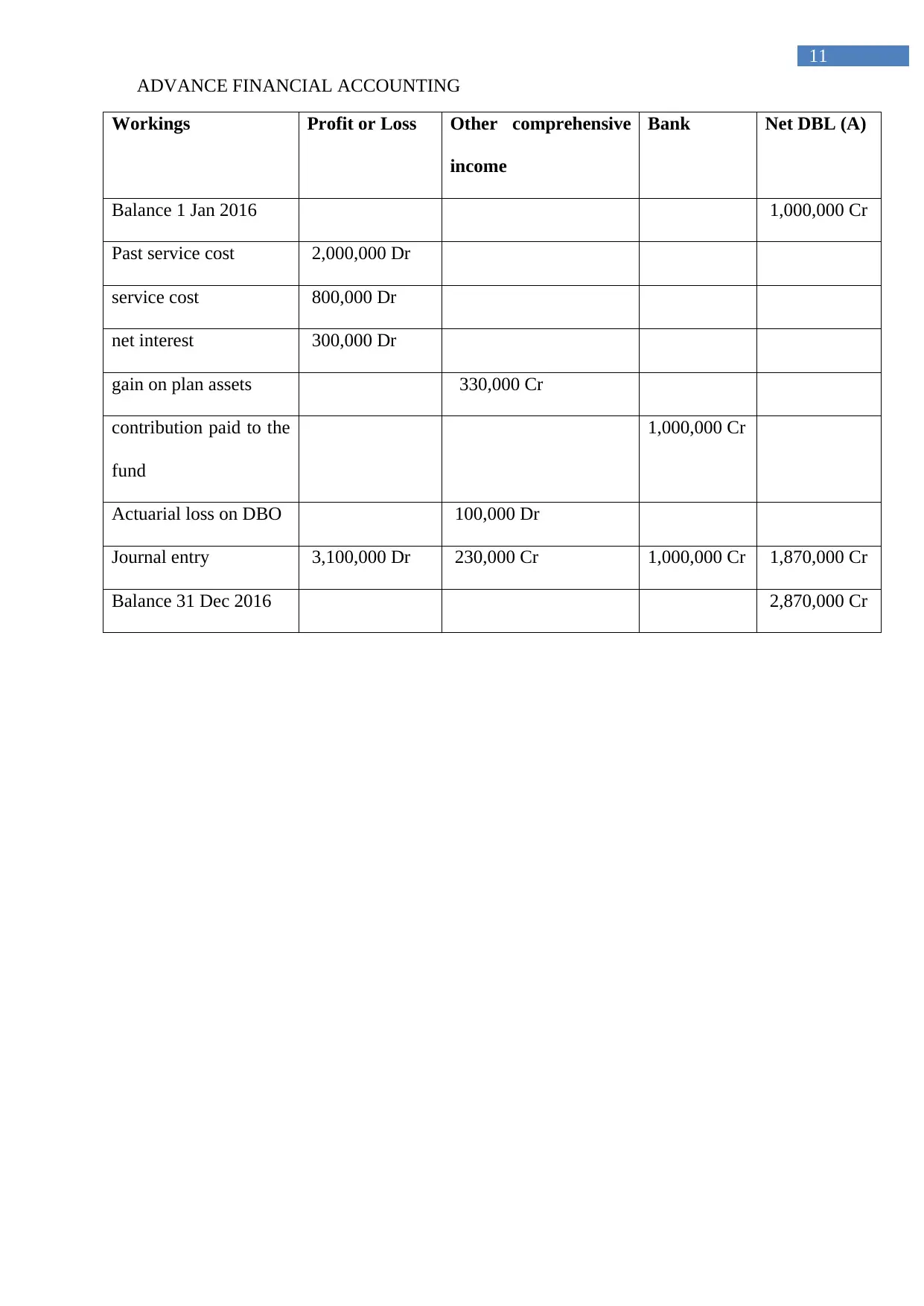

11

Workings Profit or Loss Other comprehensive

income

Bank Net DBL (A)

Balance 1 Jan 2016 1,000,000 Cr

Past service cost 2,000,000 Dr

service cost 800,000 Dr

net interest 300,000 Dr

gain on plan assets 330,000 Cr

contribution paid to the

fund

1,000,000 Cr

Actuarial loss on DBO 100,000 Dr

Journal entry 3,100,000 Dr 230,000 Cr 1,000,000 Cr 1,870,000 Cr

Balance 31 Dec 2016 2,870,000 Cr

11

Workings Profit or Loss Other comprehensive

income

Bank Net DBL (A)

Balance 1 Jan 2016 1,000,000 Cr

Past service cost 2,000,000 Dr

service cost 800,000 Dr

net interest 300,000 Dr

gain on plan assets 330,000 Cr

contribution paid to the

fund

1,000,000 Cr

Actuarial loss on DBO 100,000 Dr

Journal entry 3,100,000 Dr 230,000 Cr 1,000,000 Cr 1,870,000 Cr

Balance 31 Dec 2016 2,870,000 Cr

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.