IIT Advanced Diploma of Accounting: ADACC Chapter 9 Assessment

VerifiedAdded on 2023/01/13

|23

|3447

|34

Homework Assignment

AI Summary

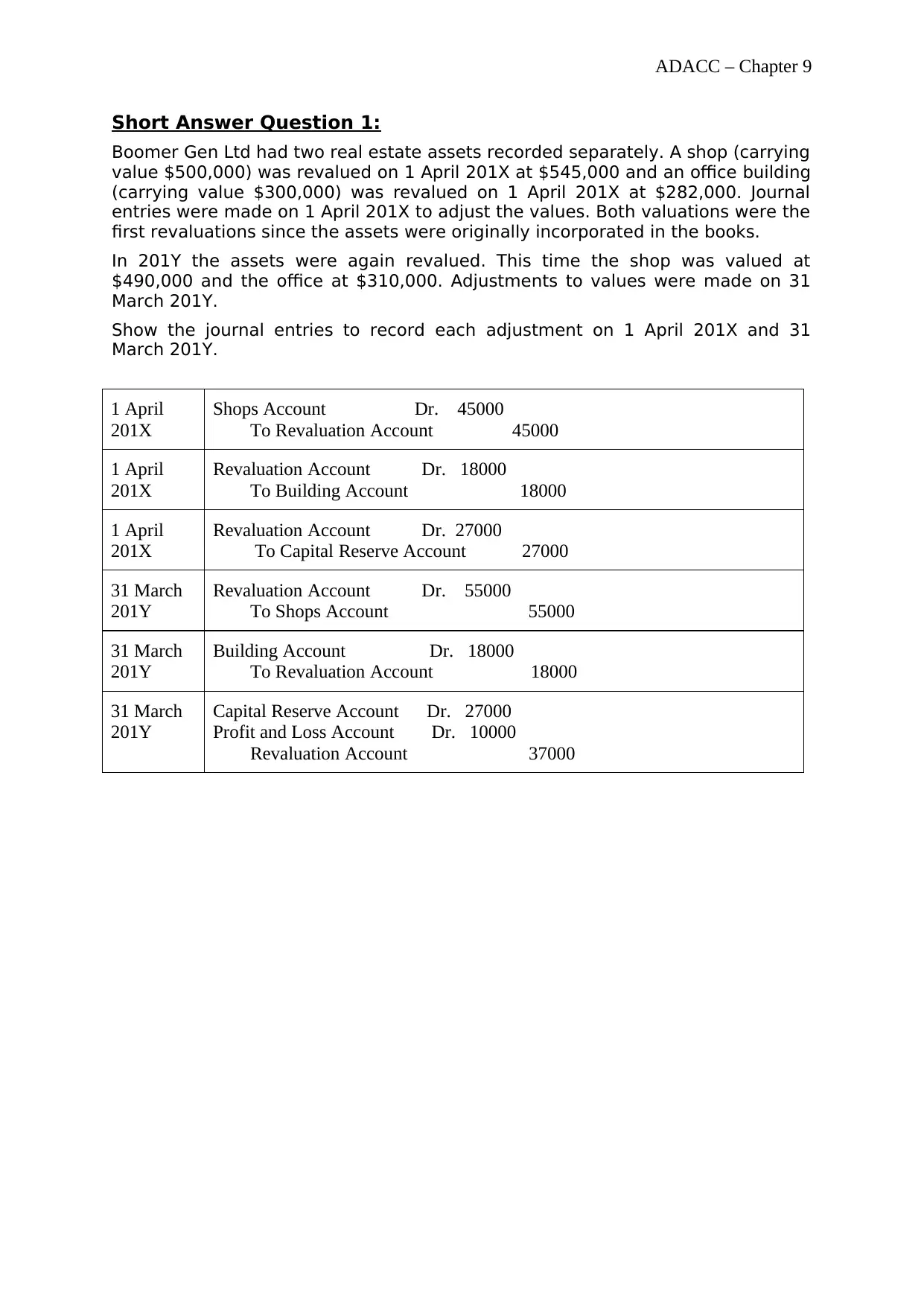

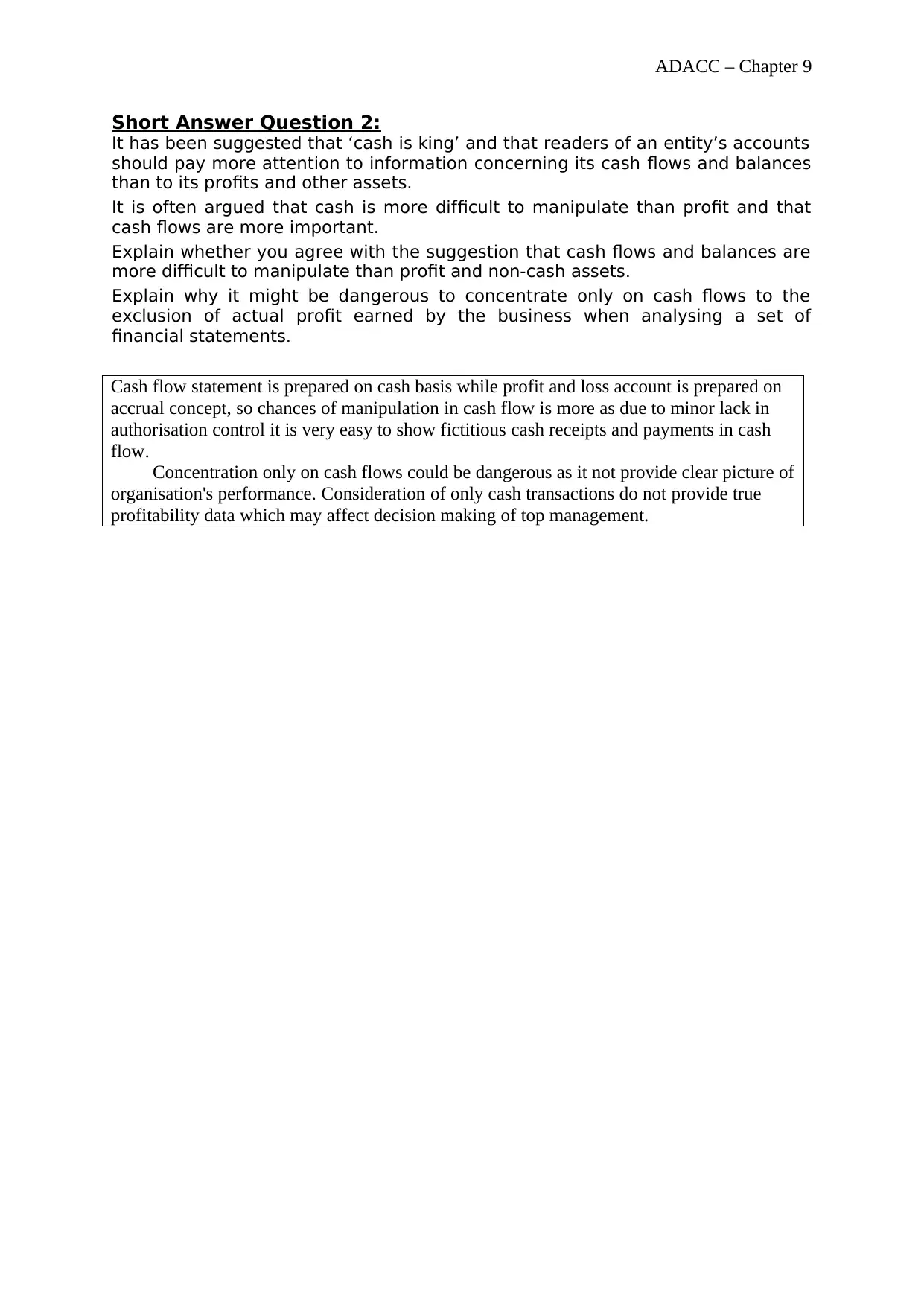

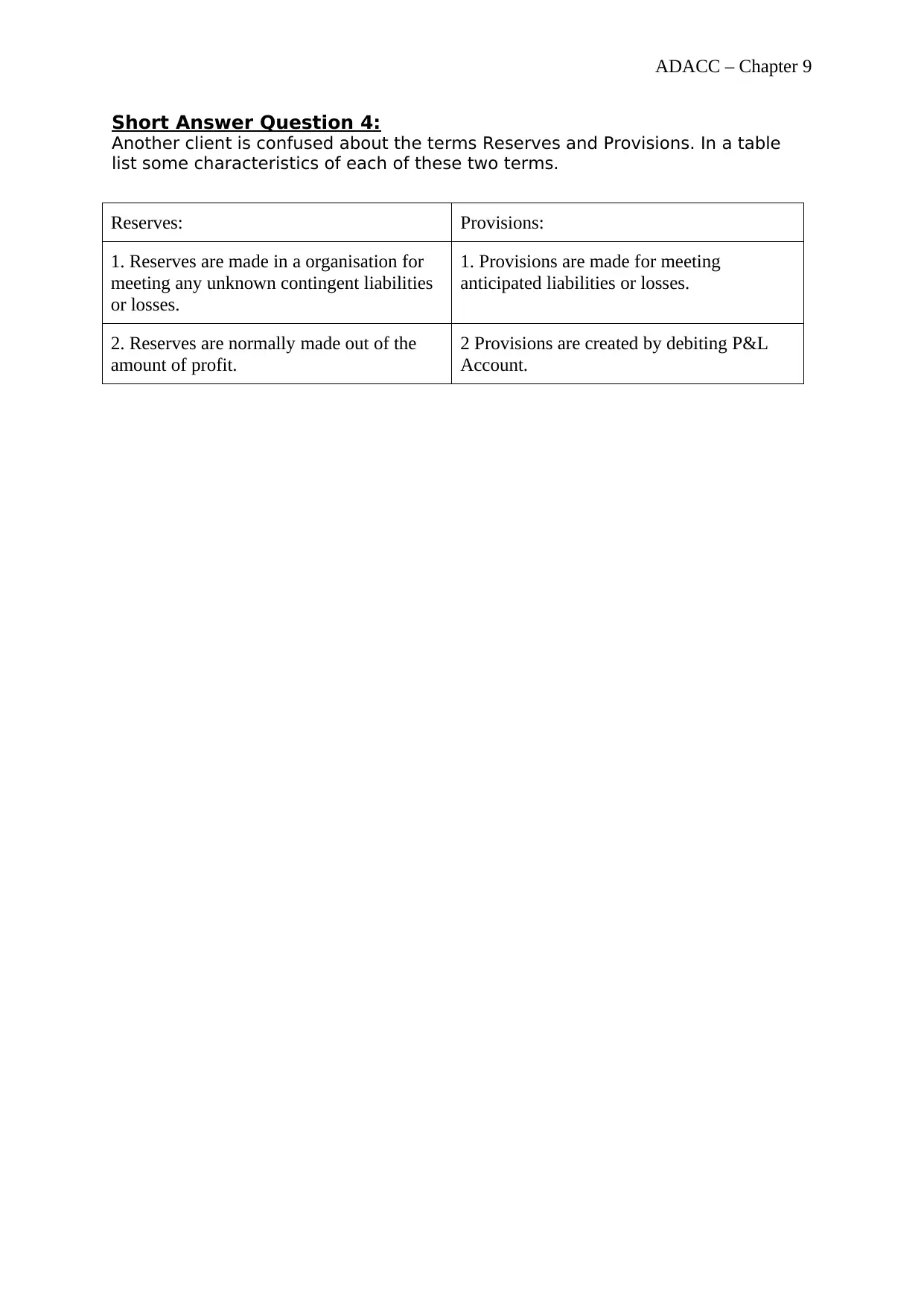

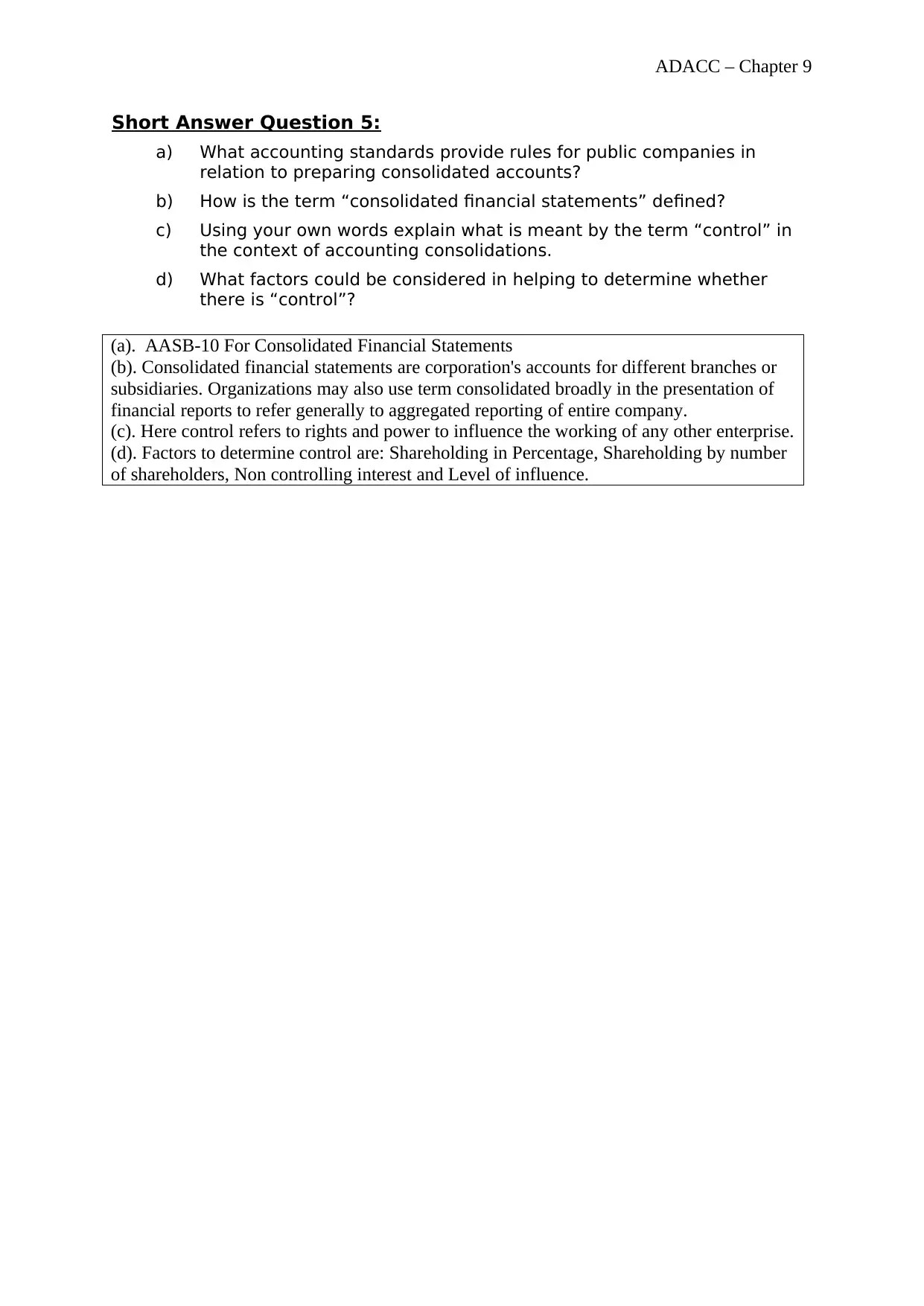

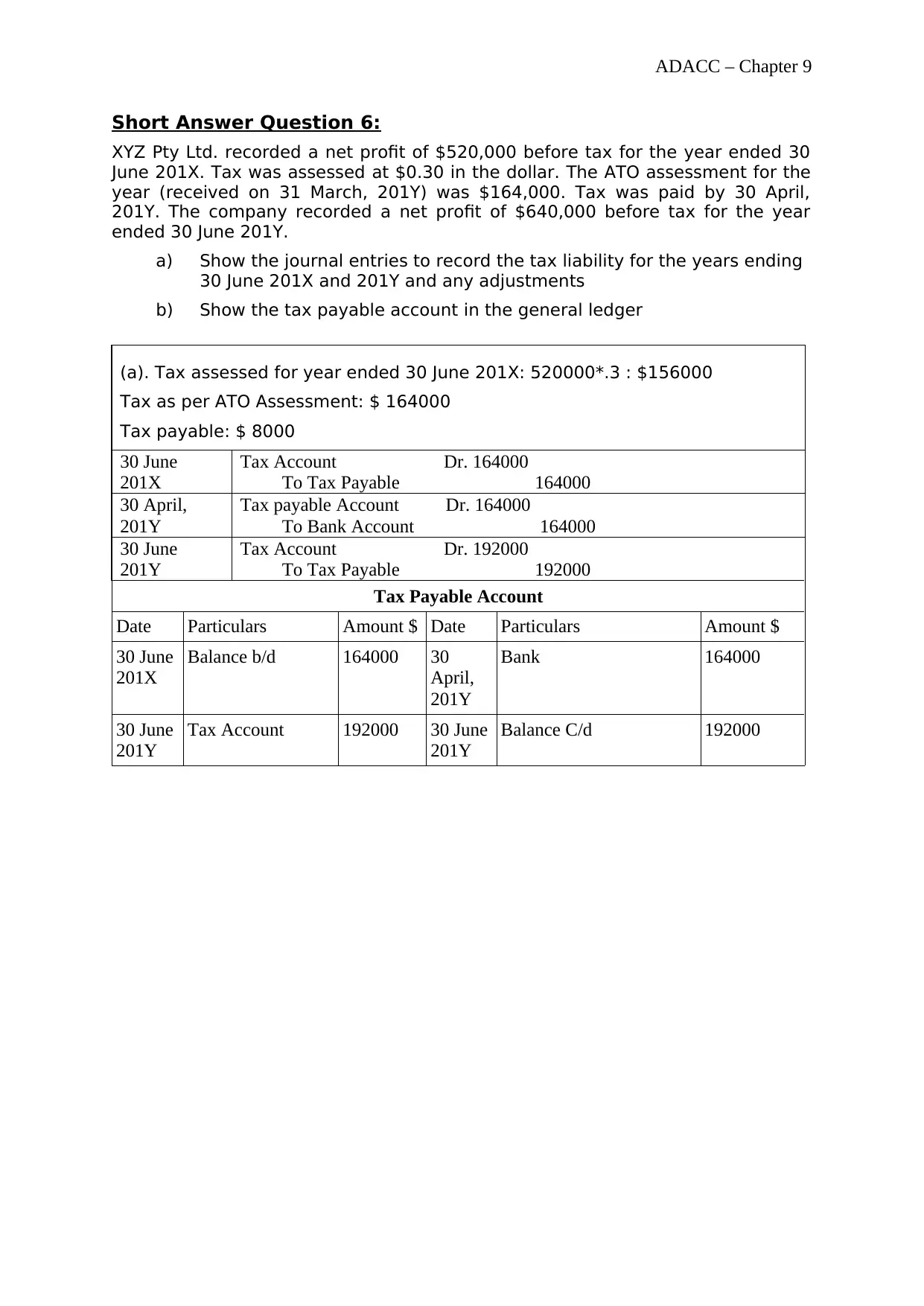

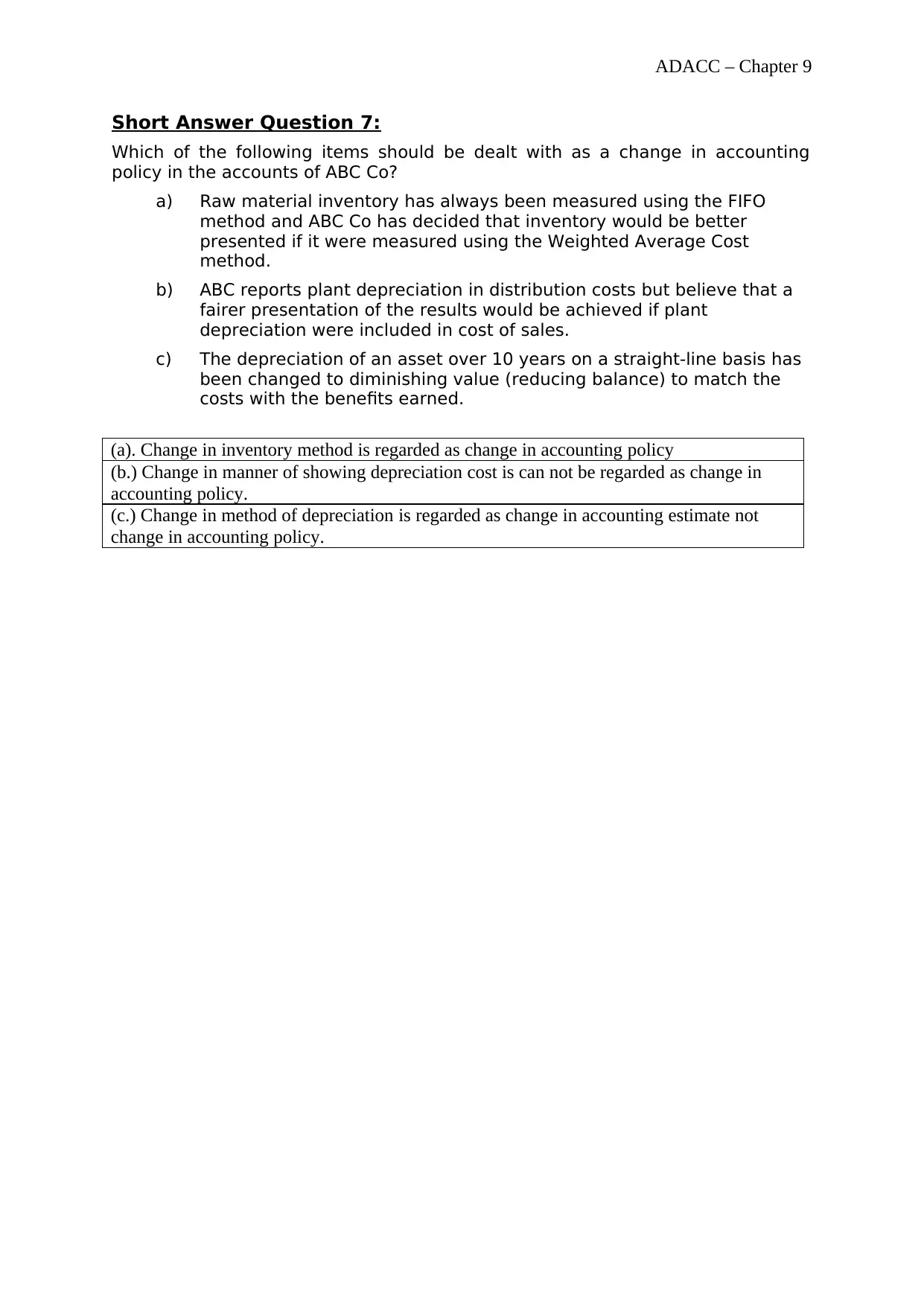

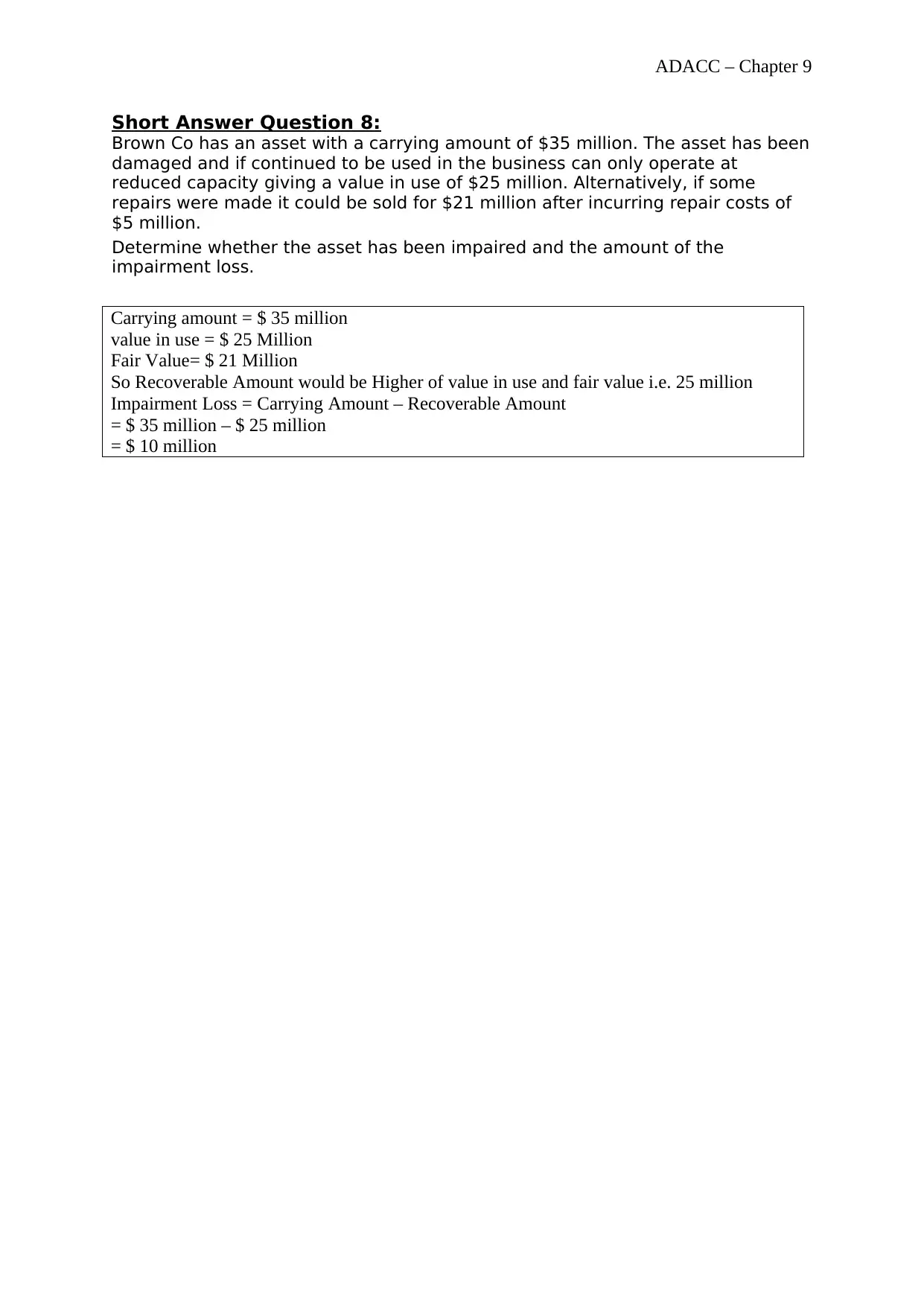

This document presents the solutions to the ADACC Chapter 9 assessment, focusing on financial accounting principles. The assessment covers a range of topics including journal entries for asset revaluations, the manipulation of cash flows versus profit, the role of accounting standards in defining GAAP, the differences between reserves and provisions, the rules for consolidated accounts, journal entries for tax liabilities, changes in accounting policy, impairment losses, and the recognition of investments and financial statement items. The answers demonstrate understanding of accounting concepts, calculations, and the application of relevant accounting standards. The assessment includes short answer questions requiring concise explanations and calculations where necessary. The answers are presented in the format specified by the assessment brief, including proper referencing and adherence to word limits.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.