Advanced Financial Accounting: Analysis of Enron's Reporting Issues

VerifiedAdded on 2023/06/05

|11

|2736

|101

Case Study

AI Summary

This assignment provides a detailed analysis of the Enron scandal through the lens of advanced financial accounting, focusing on the implications of mark-to-market accounting, the use of special purpose entities (SPEs), and the high compensation implemented by Enron's management, evaluated in the context of Agency Theory. It highlights how Enron manipulated its financial reports, inflated its financial position, and hid debt using SPEs, ultimately benefiting its executives at the expense of investors. Additionally, the assignment examines Rio Tinto's financial reporting methodologies, particularly its use of fair value measurement, and assesses the decision-usefulness of this approach for both management and investors. The analysis critically evaluates whether alternative techniques could be more beneficial, concluding that fair value measurement, as implemented under IFRS standards, provides an effective means of assessing asset and liability values. Desklib provides students access to similar solved assignments and past papers.

Running head: ADVANCED FINANCIAL ACCOUNTING

Advanced Financial Accounting

Name of the Student:

Name of the University:

Authors Note:

Advanced Financial Accounting

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED FINANCIAL ACCOUNTING

1

Table of Contents

Assessment Task Part A:............................................................................................................2

a) Indicating the implications of mark-to-market accounting approach with adequate

examples, which has been used by the Enron’s Management in manipulating their overall

annual report:.............................................................................................................................2

b) Identifying the implications of the special purpose entities that have been used by Enron’s

management in formulating the financial report in accordance with their objectives:..............3

c) Arguing about the high compensation, which was implemented by Enron’s management,

while evaluating the decisions in concept of Agency Theory:..................................................5

Assessment Task Part B:............................................................................................................6

a) Detecting the overall measurement methodologies of the company’s annual report:...........6

b) Explaining the measures used by the company for an element, while detecting the

measurement method provided decision-usefulness information and understands the

significance of the decision usefulness for an organisation:......................................................6

c) Portraying a critical analysis of the techniques used by the organisation, while depicting

whether a new technique can be deployed by more useful or practice than another method:...7

References and Bibliography:....................................................................................................9

1

Table of Contents

Assessment Task Part A:............................................................................................................2

a) Indicating the implications of mark-to-market accounting approach with adequate

examples, which has been used by the Enron’s Management in manipulating their overall

annual report:.............................................................................................................................2

b) Identifying the implications of the special purpose entities that have been used by Enron’s

management in formulating the financial report in accordance with their objectives:..............3

c) Arguing about the high compensation, which was implemented by Enron’s management,

while evaluating the decisions in concept of Agency Theory:..................................................5

Assessment Task Part B:............................................................................................................6

a) Detecting the overall measurement methodologies of the company’s annual report:...........6

b) Explaining the measures used by the company for an element, while detecting the

measurement method provided decision-usefulness information and understands the

significance of the decision usefulness for an organisation:......................................................6

c) Portraying a critical analysis of the techniques used by the organisation, while depicting

whether a new technique can be deployed by more useful or practice than another method:...7

References and Bibliography:....................................................................................................9

ADVANCED FINANCIAL ACCOUNTING

2

Assessment Task Part A:

a) Indicating the implications of mark-to-market accounting approach with adequate

examples, which has been used by the Enron’s Management in manipulating their

overall annual report:

After evaluating the overall article conducted by Paul, Healy and Krishna, the overall

manipulation, which was conducted by the management of Enron can be detected. The

company has been using different types manipulative measures for inflating their current

financial position, which has been described in the overall article. In addition, the financial

performance of the organisation has reduced over time, which was supported by the

manipulative measures conducted by the organisations (Healy and Palepu 2003). One of the

major manipulations was mainly conducted with the help of mark-to-market accounting

approach, which allowed the organisation to manipulate the overall income that has been

generated from operations. The mark-to-market accounting approach directly allows the

organisation to understand the present value of the future transaction recorded by the

management. This method directly allows the organisation to forecast its future earnings in

the annual report, which can be used by the investors in detecting the future prospects of the

organisation. The same method was used by the management of Enron in manipulating the

overall annual report and project wrong information in their annual report. Arnold and Kyle

(2017) argued that organisations were able to manipulate the mark-to-market accounting

approach for suiting their personal gains and altering the annual report in accordance with

their requirements.

Therefore, the management of Enron with the help of mark-to-market accounting

approach was able to forecast the energy prices and interest rates, while recognising the

2

Assessment Task Part A:

a) Indicating the implications of mark-to-market accounting approach with adequate

examples, which has been used by the Enron’s Management in manipulating their

overall annual report:

After evaluating the overall article conducted by Paul, Healy and Krishna, the overall

manipulation, which was conducted by the management of Enron can be detected. The

company has been using different types manipulative measures for inflating their current

financial position, which has been described in the overall article. In addition, the financial

performance of the organisation has reduced over time, which was supported by the

manipulative measures conducted by the organisations (Healy and Palepu 2003). One of the

major manipulations was mainly conducted with the help of mark-to-market accounting

approach, which allowed the organisation to manipulate the overall income that has been

generated from operations. The mark-to-market accounting approach directly allows the

organisation to understand the present value of the future transaction recorded by the

management. This method directly allows the organisation to forecast its future earnings in

the annual report, which can be used by the investors in detecting the future prospects of the

organisation. The same method was used by the management of Enron in manipulating the

overall annual report and project wrong information in their annual report. Arnold and Kyle

(2017) argued that organisations were able to manipulate the mark-to-market accounting

approach for suiting their personal gains and altering the annual report in accordance with

their requirements.

Therefore, the management of Enron with the help of mark-to-market accounting

approach was able to forecast the energy prices and interest rates, while recognising the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED FINANCIAL ACCOUNTING

3

income from operations. In addition, the article directly indicated that the management of

Enron manipulated the revenue of $110 million in their annual report, which was to be

generated from the blockbuster deal conducted for 20-year period (Healy and Palepu 2003).

The accumulation of profits from the Blockbuster deal was accumulated by the management,

while the technical capability of the organisation was not certain, which indicated the

problem for the organisation. The second problem stated in the article regarding the mark-to-

market accounting approach is the inclusion of revenue worth half a billion when discounted

the 1.3 billion in income that will be generated from the Indianapolis deal. This increment in

the overall profits was depicted by the organisation in their annual report without the actual

presence of income generated by the organisation during the fiscal year. The increment in the

financial performance was mainly manipulated by the organisation with the help of mark-to-

market accounting approach. Miller and Shawver (2016) mentioned that manipulation

conducted by the management raised concerns regarding the trust issues, which investors

have regarding the operations of the organisation. On the other hand, TAN, Lim and Kuah

(2017) argued that companies using manipulative measure hide their actual performance and

lure more investors into their vicinity.

b) Identifying the implications of the special purpose entities that have been used by

Enron’s management in formulating the financial report in accordance with their

objectives:

One of the major manipulative measures that was being used by the Enron’s

management is the Special Purpose Entities, which can be utilised as an off-balance sheet

financial estimate. The organisation was using the measure exponentially, as it reduces the

implications of debt, which was being used by the organisation in conducting its operations.

Special Purpose Entities was used by the management of Enron for purchasing the overall gas

3

income from operations. In addition, the article directly indicated that the management of

Enron manipulated the revenue of $110 million in their annual report, which was to be

generated from the blockbuster deal conducted for 20-year period (Healy and Palepu 2003).

The accumulation of profits from the Blockbuster deal was accumulated by the management,

while the technical capability of the organisation was not certain, which indicated the

problem for the organisation. The second problem stated in the article regarding the mark-to-

market accounting approach is the inclusion of revenue worth half a billion when discounted

the 1.3 billion in income that will be generated from the Indianapolis deal. This increment in

the overall profits was depicted by the organisation in their annual report without the actual

presence of income generated by the organisation during the fiscal year. The increment in the

financial performance was mainly manipulated by the organisation with the help of mark-to-

market accounting approach. Miller and Shawver (2016) mentioned that manipulation

conducted by the management raised concerns regarding the trust issues, which investors

have regarding the operations of the organisation. On the other hand, TAN, Lim and Kuah

(2017) argued that companies using manipulative measure hide their actual performance and

lure more investors into their vicinity.

b) Identifying the implications of the special purpose entities that have been used by

Enron’s management in formulating the financial report in accordance with their

objectives:

One of the major manipulative measures that was being used by the Enron’s

management is the Special Purpose Entities, which can be utilised as an off-balance sheet

financial estimate. The organisation was using the measure exponentially, as it reduces the

implications of debt, which was being used by the organisation in conducting its operations.

Special Purpose Entities was used by the management of Enron for purchasing the overall gas

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED FINANCIAL ACCOUNTING

4

reserves that was needed to support its operations. In addition, this improvement will directly

have an impact on performance of the organisation, as the investors of the Special Purpose

Entities will be provided with the steady revenue streams from the sale of reserves. The use

of Special Purpose Entities fulfilled certain requirements of the organisations, where the

long-term obligation of the organisation was being supported by the forward contract

purchases for gas reserves. The use of Special Purpose Entities was mainly conducted by the

organisation for supporting purchases of the gas reserves, where during the financial year of

2001 (Healy and Palepu 2003). The management was holding hundreds of the Special

Purpose Entities for supporting its activities and reducing the implication of the activities in

their balance sheet. The manipulative measure was used by management of Enron, as it

directly allowed them to alter the financial report in accordance to their will and projected the

different financial progress of the organisation. In this context, Warren (2017) mentioned that

companies using the special purpose entities were able to hide their current financial

performance and increase the level of risk from investment for the investors.

The Special Purpose Entities was also used for second condition, which was depicted

in the article. This improvement in the current financial performance was mainly conducted

for detecting the accurate financial condition of the company in generating high level of

income from investment. In addition, the management used the Special Purpose Entities for

hiding its overall debt, which was used for acquiring Chewco, Powers, Troubh and Winokur

(Healy and Palepu 2003). This hiding the debt measure mainly allowed the organisation to

improve its financial position and reduce the implication of debt, which might deplete its

financial performance. The organisation directly used the Special Purpose Entities to hide the

debt measure, which was taken by the company to support its operations. The major

accounting failure was mainly depicted from the wrong measure was mainly taken into

consideration by the management, where the downsized risk measure was not used by the

4

reserves that was needed to support its operations. In addition, this improvement will directly

have an impact on performance of the organisation, as the investors of the Special Purpose

Entities will be provided with the steady revenue streams from the sale of reserves. The use

of Special Purpose Entities fulfilled certain requirements of the organisations, where the

long-term obligation of the organisation was being supported by the forward contract

purchases for gas reserves. The use of Special Purpose Entities was mainly conducted by the

organisation for supporting purchases of the gas reserves, where during the financial year of

2001 (Healy and Palepu 2003). The management was holding hundreds of the Special

Purpose Entities for supporting its activities and reducing the implication of the activities in

their balance sheet. The manipulative measure was used by management of Enron, as it

directly allowed them to alter the financial report in accordance to their will and projected the

different financial progress of the organisation. In this context, Warren (2017) mentioned that

companies using the special purpose entities were able to hide their current financial

performance and increase the level of risk from investment for the investors.

The Special Purpose Entities was also used for second condition, which was depicted

in the article. This improvement in the current financial performance was mainly conducted

for detecting the accurate financial condition of the company in generating high level of

income from investment. In addition, the management used the Special Purpose Entities for

hiding its overall debt, which was used for acquiring Chewco, Powers, Troubh and Winokur

(Healy and Palepu 2003). This hiding the debt measure mainly allowed the organisation to

improve its financial position and reduce the implication of debt, which might deplete its

financial performance. The organisation directly used the Special Purpose Entities to hide the

debt measure, which was taken by the company to support its operations. The major

accounting failure was mainly depicted from the wrong measure was mainly taken into

consideration by the management, where the downsized risk measure was not used by the

ADVANCED FINANCIAL ACCOUNTING

5

organisation. The rapid acquisition, which as being conducted by the organisation was not

depicted in the annual report, where the assets were being added, while the debt used for the

acquisition was not disclosed in the annual report. This presented a positive condition of the

organisation in comparing the activities taken by the management. Furthermore, the Special

Purpose Entities also allowed the management and some employee to gain high income,

which directly raised the concern regarding the sensibility of the organisation and its current

financial performance.

c) Arguing about the high compensation, which was implemented by Enron’s

management, while evaluating the decisions in concept of Agency Theory:

The article evaluation also helps in detecting the level of manipulations, which was

conducted by the management in delivering high compensation to their managers. The

management of Enron imposed high level of compensation scheme for the managers, which

was conducted by using the stock options. The organisation had used high end stock options

in compensating its managers, which led to the increment of compensation share to the value

of 96 million that is considered to be 13% of the total outstanding shares of the organisation

(Healy and Palepu 2003). The high compensation that has been provided by the organisation

is to allow the management to make adequate decision for improving the performance of the

share price and in turn generate high capital gain from the commissions.

The decision made the organisation was evaluated in the perspective of the agency

theory, which indicated that the compensation method used was only supporting the share

price for short term period and ignoring the long-term value. This measure used by the

organisation was mainly conducted to hide the current shady operations, which allowed the

managers to benefit handsomely from the endeavour. This rising compensation payment led

to the problematic condition of Enron during the financial year of 2000.

5

organisation. The rapid acquisition, which as being conducted by the organisation was not

depicted in the annual report, where the assets were being added, while the debt used for the

acquisition was not disclosed in the annual report. This presented a positive condition of the

organisation in comparing the activities taken by the management. Furthermore, the Special

Purpose Entities also allowed the management and some employee to gain high income,

which directly raised the concern regarding the sensibility of the organisation and its current

financial performance.

c) Arguing about the high compensation, which was implemented by Enron’s

management, while evaluating the decisions in concept of Agency Theory:

The article evaluation also helps in detecting the level of manipulations, which was

conducted by the management in delivering high compensation to their managers. The

management of Enron imposed high level of compensation scheme for the managers, which

was conducted by using the stock options. The organisation had used high end stock options

in compensating its managers, which led to the increment of compensation share to the value

of 96 million that is considered to be 13% of the total outstanding shares of the organisation

(Healy and Palepu 2003). The high compensation that has been provided by the organisation

is to allow the management to make adequate decision for improving the performance of the

share price and in turn generate high capital gain from the commissions.

The decision made the organisation was evaluated in the perspective of the agency

theory, which indicated that the compensation method used was only supporting the share

price for short term period and ignoring the long-term value. This measure used by the

organisation was mainly conducted to hide the current shady operations, which allowed the

managers to benefit handsomely from the endeavour. This rising compensation payment led

to the problematic condition of Enron during the financial year of 2000.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED FINANCIAL ACCOUNTING

6

Assessment Task Part B:

a) Detecting the overall measurement methodologies of the company’s annual report:

After evaluating the financial report of Rio Tinto the different measurement

methodologies, which has been used by the organisation is adequately identified. In addition,

the evaluation directly indicates the fair value measurement, which is being used by the

organisation in formulating the annual report (Riotinto.com 2018). The organisation has been

using the overall measurement for detecting the overall assets and liabilities. The fair value

measurement directly uses the overall market rates for detecting the actual financial position

of the organisation and detects the level of improvements or demise that has been incurred by

the organisation. The fair value measurement is relevantly considered one of the viable

approaches depicted in IFRS accounting standard from Paragraphs 91-99 of IFRS 13. In this

context, TAN, Lim and Kuah (2017) mentioned that companies using the IFRS 13 are able to

detect the accurate financial condition of their asset, which is essential for maintaining the

standards of IFRS while preparing the annual report. The Rio Tinto organisation has mainly

followed the IFRS system, where IFRS 2 is also used by the organisation for supporting the

fair value measure granted for share based payments. Therefore, Rio Tinto uses the fair value

measure for Asset, liabilities and share based payments.

b) Explaining the measures used by the company for an element, while detecting the

measurement method provided decision-usefulness information and understands the

significance of the decision usefulness for an organisation:

The management of Rio Tinto directly uses fair value measurement for evaluating its

financial performance. The measurement method has allowed the management to understand

its current financial performance, while making adequate decision in improving their current

financial performance. The fair value measurement system allows the organisation to

6

Assessment Task Part B:

a) Detecting the overall measurement methodologies of the company’s annual report:

After evaluating the financial report of Rio Tinto the different measurement

methodologies, which has been used by the organisation is adequately identified. In addition,

the evaluation directly indicates the fair value measurement, which is being used by the

organisation in formulating the annual report (Riotinto.com 2018). The organisation has been

using the overall measurement for detecting the overall assets and liabilities. The fair value

measurement directly uses the overall market rates for detecting the actual financial position

of the organisation and detects the level of improvements or demise that has been incurred by

the organisation. The fair value measurement is relevantly considered one of the viable

approaches depicted in IFRS accounting standard from Paragraphs 91-99 of IFRS 13. In this

context, TAN, Lim and Kuah (2017) mentioned that companies using the IFRS 13 are able to

detect the accurate financial condition of their asset, which is essential for maintaining the

standards of IFRS while preparing the annual report. The Rio Tinto organisation has mainly

followed the IFRS system, where IFRS 2 is also used by the organisation for supporting the

fair value measure granted for share based payments. Therefore, Rio Tinto uses the fair value

measure for Asset, liabilities and share based payments.

b) Explaining the measures used by the company for an element, while detecting the

measurement method provided decision-usefulness information and understands the

significance of the decision usefulness for an organisation:

The management of Rio Tinto directly uses fair value measurement for evaluating its

financial performance. The measurement method has allowed the management to understand

its current financial performance, while making adequate decision in improving their current

financial performance. The fair value measurement system allows the organisation to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED FINANCIAL ACCOUNTING

7

understand its assets and liabilities, which is essential for detecting the actions and decisions

that needs to be taken into consideration by the management. In this context, Barth (2015)

mentioned that with adequate decision management is able to acquire additional profits over

the period and improve their current financial performance. The decision usefulness feature

does not end with the management, as the investors and shareholders of the organisation are

able to understand the current financial position of the organisation. The investors are able to

make adequate decision regarding the investment options, as the fair value helps in detecting

the accurate financial position of the organisation. Therefore, fair value measurement is

considered an adequate method, which allows the management and investors to improve their

current decision usefulness condition.

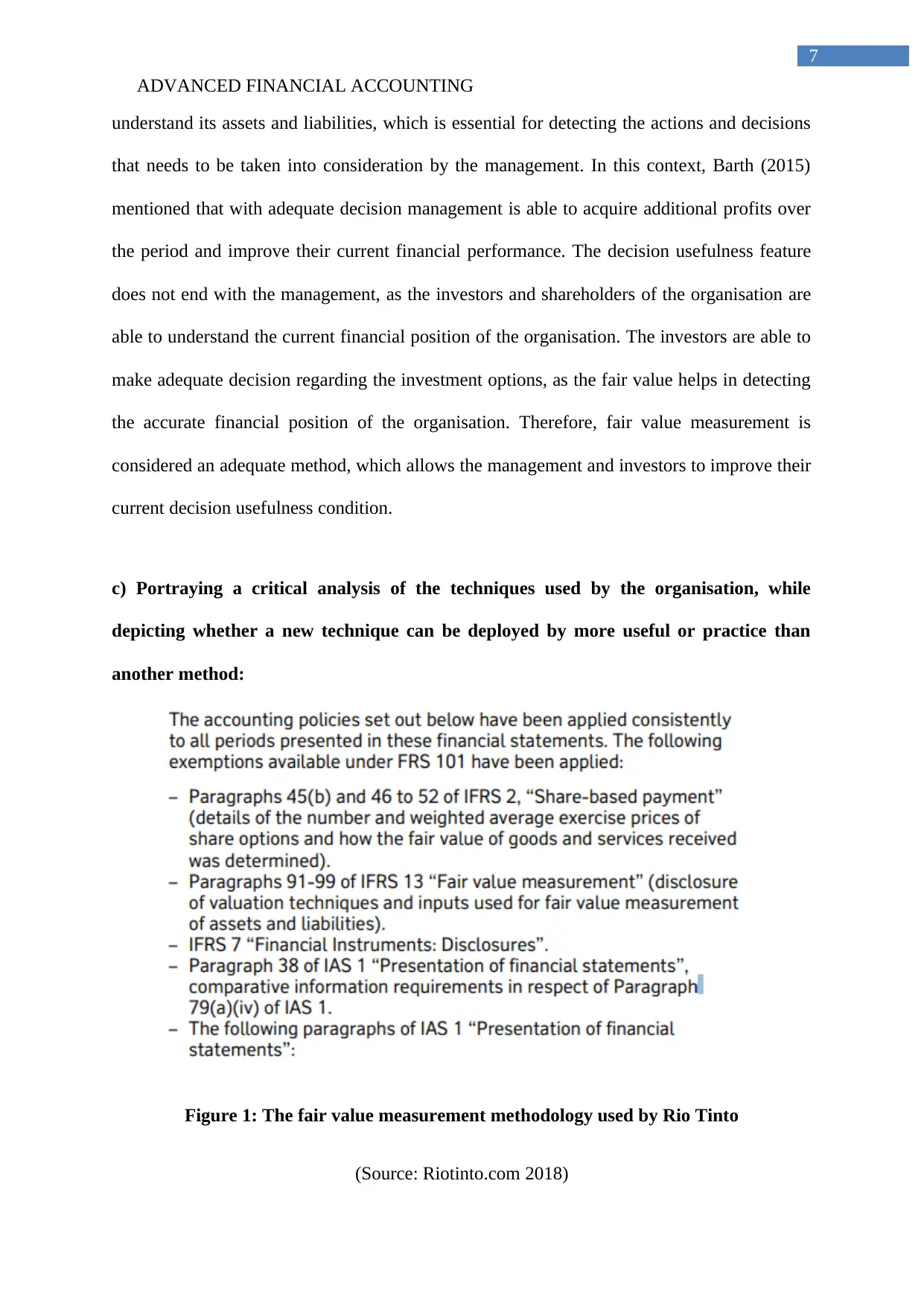

c) Portraying a critical analysis of the techniques used by the organisation, while

depicting whether a new technique can be deployed by more useful or practice than

another method:

Figure 1: The fair value measurement methodology used by Rio Tinto

(Source: Riotinto.com 2018)

7

understand its assets and liabilities, which is essential for detecting the actions and decisions

that needs to be taken into consideration by the management. In this context, Barth (2015)

mentioned that with adequate decision management is able to acquire additional profits over

the period and improve their current financial performance. The decision usefulness feature

does not end with the management, as the investors and shareholders of the organisation are

able to understand the current financial position of the organisation. The investors are able to

make adequate decision regarding the investment options, as the fair value helps in detecting

the accurate financial position of the organisation. Therefore, fair value measurement is

considered an adequate method, which allows the management and investors to improve their

current decision usefulness condition.

c) Portraying a critical analysis of the techniques used by the organisation, while

depicting whether a new technique can be deployed by more useful or practice than

another method:

Figure 1: The fair value measurement methodology used by Rio Tinto

(Source: Riotinto.com 2018)

ADVANCED FINANCIAL ACCOUNTING

8

The above figure directly indicates the level of fair value measurement, which has

been used by Rio Tinto in detecting their current financial performance. The company has

been using the fair value measure, which is considered to be one of the adequate methods that

can be used by companies for detecting their current value of assets and liabilities. Rio Tinto

has been using the fair value measurement in detecting the current condition of their assets

and liabilities (Riotinto.com 2018). The fair value measure is the best method for identifying

the actual position of company assets and liabilities, as depicted in the IFRS accounting

standard. The measurement also helps in detecting the fair value for the share based

payments, which can allow the management to detect the level shares, which could be

delivered, as compensation of the employees and executives.

8

The above figure directly indicates the level of fair value measurement, which has

been used by Rio Tinto in detecting their current financial performance. The company has

been using the fair value measure, which is considered to be one of the adequate methods that

can be used by companies for detecting their current value of assets and liabilities. Rio Tinto

has been using the fair value measurement in detecting the current condition of their assets

and liabilities (Riotinto.com 2018). The fair value measure is the best method for identifying

the actual position of company assets and liabilities, as depicted in the IFRS accounting

standard. The measurement also helps in detecting the fair value for the share based

payments, which can allow the management to detect the level shares, which could be

delivered, as compensation of the employees and executives.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED FINANCIAL ACCOUNTING

9

References and Bibliography:

Abdel-Maksoud, A., Cheffi, W. and Ghoudi, K., 2016. The mediating effect of shop-floor

involvement on relations between advanced management accounting practices and

operational non-financial performance indicators. The British Accounting Review, 48(2),

pp.169-184.

Arnold, G. and Kyle, S., 2017. Intermediate Financial Accounting Volume 2. Lyryx.

Barth, M.E., 2015. Financial accounting research, practice, and financial

accountability. Abacus, 51(4), pp.499-510.

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2-3), pp.339-383.

Healy, P.M. and Palepu, K.G., 2003. The fall of Enron. Journal of economic

perspectives, 17(2), pp.3-26.

Hoskin, R.E., Fizzell, M.R. and Cherry, D.C., 2014. Financial Accounting: a user

perspective. Wiley Global Education.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Jones, J.P., Long, J.H. and Stanley, J.D., 2018. Pane in the Glass: A Review of the

Accounting Cycle.

Laux, C., 2016. The economic consequences of extending the use of fair value accounting in

regulatory capital calculations: A discussion. Journal of Accounting and Economics, 62(2-3),

pp.204-208.

9

References and Bibliography:

Abdel-Maksoud, A., Cheffi, W. and Ghoudi, K., 2016. The mediating effect of shop-floor

involvement on relations between advanced management accounting practices and

operational non-financial performance indicators. The British Accounting Review, 48(2),

pp.169-184.

Arnold, G. and Kyle, S., 2017. Intermediate Financial Accounting Volume 2. Lyryx.

Barth, M.E., 2015. Financial accounting research, practice, and financial

accountability. Abacus, 51(4), pp.499-510.

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2-3), pp.339-383.

Healy, P.M. and Palepu, K.G., 2003. The fall of Enron. Journal of economic

perspectives, 17(2), pp.3-26.

Hoskin, R.E., Fizzell, M.R. and Cherry, D.C., 2014. Financial Accounting: a user

perspective. Wiley Global Education.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Jones, J.P., Long, J.H. and Stanley, J.D., 2018. Pane in the Glass: A Review of the

Accounting Cycle.

Laux, C., 2016. The economic consequences of extending the use of fair value accounting in

regulatory capital calculations: A discussion. Journal of Accounting and Economics, 62(2-3),

pp.204-208.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED FINANCIAL ACCOUNTING

10

Miller, W.F. and Shawver, T.J., 2016. The potential impact of education on whistleblowing

behavior: benefits of an intervention in advanced financial accounting. Journal of Business

Ethics Education, 13, pp.67-90.

Riotinto.com. (2018). [online] Available at:

https://www.riotinto.com/documents/RT_2017_Annual_Report.pdf [Accessed 29 Sep. 2018].

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues,

concepts and practice. Routledge.

TAN, P.H.N., Lim, C.Y. and Kuah, E.W., 2017. Advanced financial accounting: An IFRS

standards approach.

Warren, R.G.J., 2017. Extending the Hegemony of Advanced Financial Capital: The

International Accounting Standards Board and the International Financial Reporting

Standard for Small and Medium-Sized Entities (Doctoral dissertation, Royal Holloway,

University of London).

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial & managerial accounting.

John Wiley & Sons.

Wong, S.T. and Yeung, C.S., 2014. Advanced Financial Accounting. Pearson Education Asia

Limited.

10

Miller, W.F. and Shawver, T.J., 2016. The potential impact of education on whistleblowing

behavior: benefits of an intervention in advanced financial accounting. Journal of Business

Ethics Education, 13, pp.67-90.

Riotinto.com. (2018). [online] Available at:

https://www.riotinto.com/documents/RT_2017_Annual_Report.pdf [Accessed 29 Sep. 2018].

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues,

concepts and practice. Routledge.

TAN, P.H.N., Lim, C.Y. and Kuah, E.W., 2017. Advanced financial accounting: An IFRS

standards approach.

Warren, R.G.J., 2017. Extending the Hegemony of Advanced Financial Capital: The

International Accounting Standards Board and the International Financial Reporting

Standard for Small and Medium-Sized Entities (Doctoral dissertation, Royal Holloway,

University of London).

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial & managerial accounting.

John Wiley & Sons.

Wong, S.T. and Yeung, C.S., 2014. Advanced Financial Accounting. Pearson Education Asia

Limited.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.