Advanced Accounting: Reporting of Financial Instruments (MAA725)

VerifiedAdded on 2022/08/26

|9

|1620

|18

Report

AI Summary

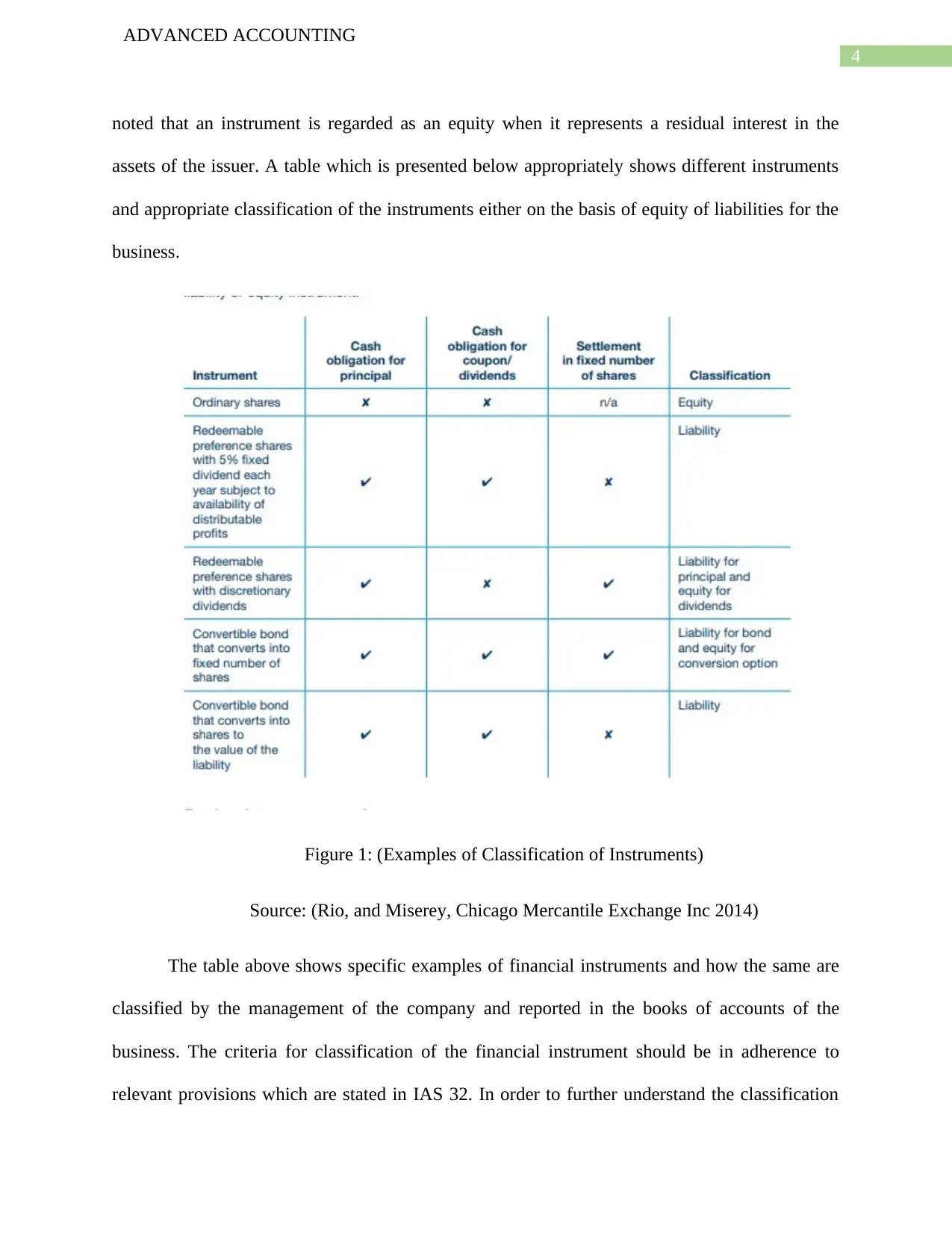

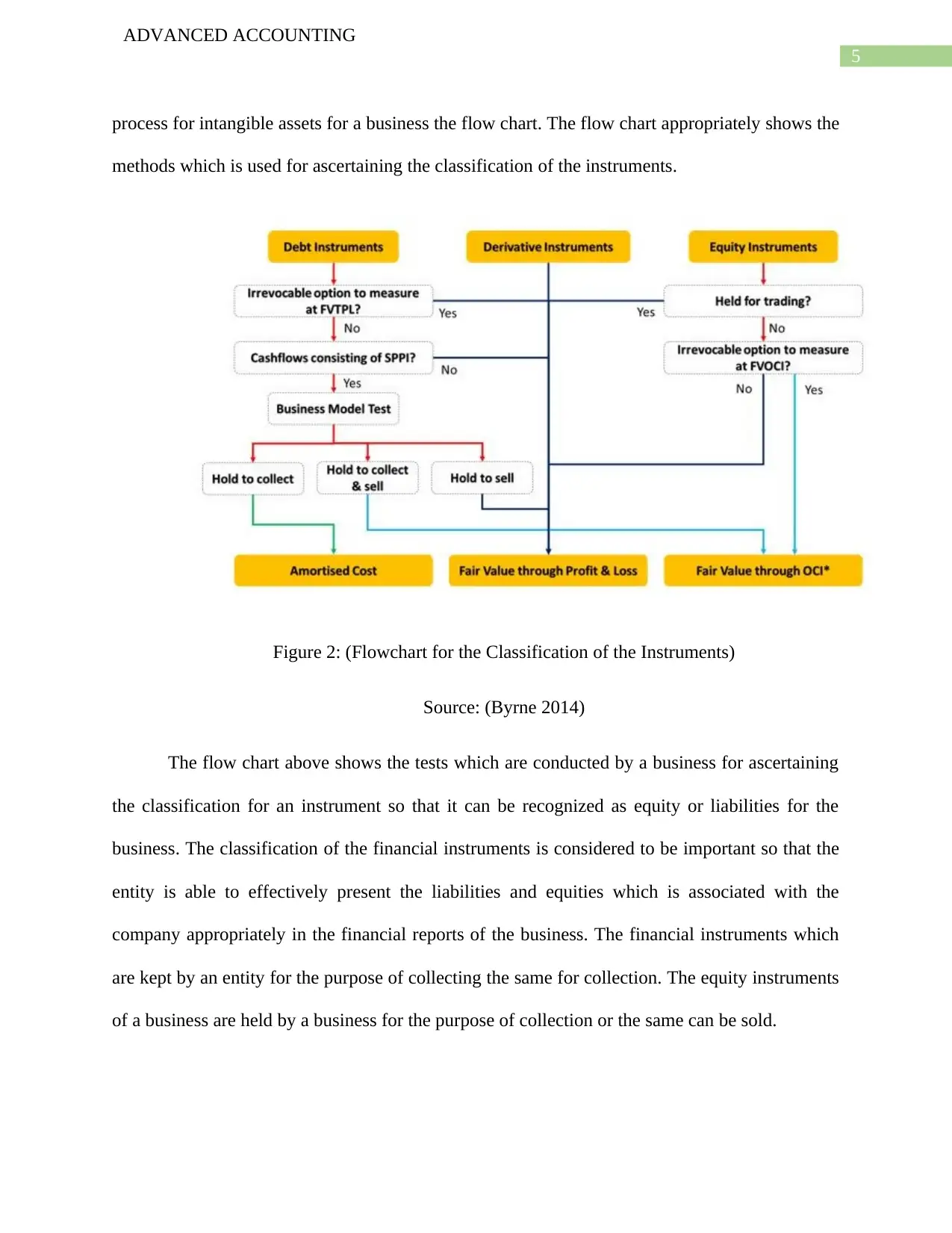

This report provides a comprehensive analysis of financial instruments, focusing on their classification as either equity or liability instruments, and the subsequent reporting requirements. The report delves into the provisions of IAS 32, explaining the criteria for recognizing financial instruments and the reporting processes that follow. It highlights the importance of correctly classifying financial instruments for transparency in financial statements and discusses the differences in classification. The report includes examples of financial instrument classifications, flowcharts illustrating the classification process, and details on the required disclosures as per IFRS 7. Furthermore, the report also covers a practical task involving forward contracts, including calculations and journal entries to illustrate the accounting treatment for such transactions. Overall, the report provides a detailed overview of financial instrument reporting, classification, and the relevant accounting standards.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.