MAA725: Advance Accounting Principles and Practice Assignment

VerifiedAdded on 2022/08/24

|13

|2208

|27

Homework Assignment

AI Summary

This assignment solution addresses the complexities of accounting for financial instruments under IFRS, with specific reference to IAS 32, IFRS 7, and IAS 39. It provides a detailed discussion on the classification of financial instruments as either debt or equity, emphasizing the importance of contractual terms over legal form. The solution explores the definitions and characteristics of financial assets, financial liabilities, and equity instruments, including various categories like common stock and convertible debentures. It highlights the impact of proper classification on key financial metrics such as the gearing ratio and earnings per share (EPS). Furthermore, the assignment includes journal entries for foreign exchange and references relevant accounting standards and literature. The solution also discusses the implications of the new standard AASB 9 for financial reporting, which provides new rules for the impairment of financial assets.

Running head: ADVANCE ACCOUNTING

ADVANCE ACCOUNTING

Name of the Student

Name of the University

Author Note:

ADVANCE ACCOUNTING

Name of the Student

Name of the University

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ADVANCE ACCOUNTING

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................2

Classification as liability or Equity..............................................................................................5

Conclusion.......................................................................................................................................7

Reference.......................................................................................................................................11

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................2

Classification as liability or Equity..............................................................................................5

Conclusion.......................................................................................................................................7

Reference.......................................................................................................................................11

2ADVANCE ACCOUNTING

Introduction

Accounting for financial instruments is complex under IFRS. A broad review has been

provided considering IAS 32, ‘Financial Instrument: Presentation’, IFRS 7, ‘Financial

Instrument Disclosure’, and IAS 39. ‘Financial Instrument: Recognition and Measurement’. The

following chapters have been addressed among which includes classification of debt and equity

and scope of the requirement (Uyar, Kılıç and Gökçen, 2016). Financial Instrument can also be

interpret as any contract which gives an addition in the asset of one entity and a financial liability

or an instrument of equity to the other entity.

Discussion

General Accepted Accounting Principal (GAAP) explains the financial instrument as

money in form of cash or any other evidence of ownership interest in the company or an entity

(Wild, Creighton and Simmonds, 2015). The instrument can be in a form of contract which

imposes a contractual obligation on one entity, either to give cash or any other financial

instrument to a other entity or to exchange any financial instrument on unfavourable terms with

the other entity.

IAS 32 lays down principles for distinguishing between the financial instruments like

equity and liabilities. The classification of the financial instrument is governed by the contractual

terms rather than its legal form. IAS 32 outlines the requirement of accounting for presenting

financial instrument, particularly while classifying such instrument as a financial asset, financial

liabilities or equity instrument (Iasplus.com. 2020). An important feature which distinguishes a

liability from equity is that while issuing an instrument, if the issuer is required to issue cash or

any other financial asset to the bearer or holder than the instrument represents liability.

Introduction

Accounting for financial instruments is complex under IFRS. A broad review has been

provided considering IAS 32, ‘Financial Instrument: Presentation’, IFRS 7, ‘Financial

Instrument Disclosure’, and IAS 39. ‘Financial Instrument: Recognition and Measurement’. The

following chapters have been addressed among which includes classification of debt and equity

and scope of the requirement (Uyar, Kılıç and Gökçen, 2016). Financial Instrument can also be

interpret as any contract which gives an addition in the asset of one entity and a financial liability

or an instrument of equity to the other entity.

Discussion

General Accepted Accounting Principal (GAAP) explains the financial instrument as

money in form of cash or any other evidence of ownership interest in the company or an entity

(Wild, Creighton and Simmonds, 2015). The instrument can be in a form of contract which

imposes a contractual obligation on one entity, either to give cash or any other financial

instrument to a other entity or to exchange any financial instrument on unfavourable terms with

the other entity.

IAS 32 lays down principles for distinguishing between the financial instruments like

equity and liabilities. The classification of the financial instrument is governed by the contractual

terms rather than its legal form. IAS 32 outlines the requirement of accounting for presenting

financial instrument, particularly while classifying such instrument as a financial asset, financial

liabilities or equity instrument (Iasplus.com. 2020). An important feature which distinguishes a

liability from equity is that while issuing an instrument, if the issuer is required to issue cash or

any other financial asset to the bearer or holder than the instrument represents liability.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ADVANCE ACCOUNTING

Classification of net asset is done when a residual interest is represented in the net asset of the

issuer (Pwc.com. 2020).

The financial instrument comprises of a financial asset, equity instrument and financial

liability (Mullinova, 2016). This instrument can be categorized into two groups:

Cash Instrument: These are those instrument which is directly influenced by the market

and the market also determines the value. This instrument can be in the form of

securities, that is liquid i.e. readily transferable, and loans and deposits in which the

borrowers and lenders agree on the transfer.

Derivative Instrument: These are those instrument which derives their value and

characteristics based on the vehicles underlying components such as interest rates, assets

or index. The instruments are over-the-counter (OTC) derivatives or can be exchange-

traded derivatives. The derivative on equity is accounted under IAS 39.

While considering any item in the balance sheet, it is important to understand the following

terms (Fabozzi, 2018):

Financial Asset: These are non-existing asset the value of which is derived from a

contractual term like bonds, stocks and bank deposits. These assets are highly liquid as

compared to other tangible asset. Assets which are in the form of cash or cash equivalent

(Tan and Low, 2017) and includes a contract that will or may be settled from the equity

instrument of the entity and which is a non-derivative, and for which the entity will

receive a variable number of the other entity’s equity instrument is a financial asset.

Financial assets are different from non-financial assets as it includes tangible and

intangible assets.

Classification of net asset is done when a residual interest is represented in the net asset of the

issuer (Pwc.com. 2020).

The financial instrument comprises of a financial asset, equity instrument and financial

liability (Mullinova, 2016). This instrument can be categorized into two groups:

Cash Instrument: These are those instrument which is directly influenced by the market

and the market also determines the value. This instrument can be in the form of

securities, that is liquid i.e. readily transferable, and loans and deposits in which the

borrowers and lenders agree on the transfer.

Derivative Instrument: These are those instrument which derives their value and

characteristics based on the vehicles underlying components such as interest rates, assets

or index. The instruments are over-the-counter (OTC) derivatives or can be exchange-

traded derivatives. The derivative on equity is accounted under IAS 39.

While considering any item in the balance sheet, it is important to understand the following

terms (Fabozzi, 2018):

Financial Asset: These are non-existing asset the value of which is derived from a

contractual term like bonds, stocks and bank deposits. These assets are highly liquid as

compared to other tangible asset. Assets which are in the form of cash or cash equivalent

(Tan and Low, 2017) and includes a contract that will or may be settled from the equity

instrument of the entity and which is a non-derivative, and for which the entity will

receive a variable number of the other entity’s equity instrument is a financial asset.

Financial assets are different from non-financial assets as it includes tangible and

intangible assets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ADVANCE ACCOUNTING

Financial Liability: Financial liabilities are those future sacrifices that an entity is

required to make in terms of economic benefits which arises due to some past transaction

or any other activity in the past. This sacrifices that are required to be made in the future

can be in the form of money or services owed to the other entity or party (Skoglund and

Chen, 2015). It can also be defined as any liability that is a contractual obligation to give

cash or any other financial instrument to the other party, or to change the financial asset

to write off the liability under conditions that may be potentially unfavourable for the

entity. Financial liability includes interest and debt payables which arises as a result of

using other’s money in the past and accounts payable such as rent, purchases and lease

payable to the other parties for the use of their products and spaces in the past.

Equity Instrument: It refers to any documents which serve as legal evidence to individual

or entity for proving their right in the firm. The instrument is primarily used to fund the

business, and the individual who holds an equity instrument in the entity is called a

shareholder. It can also be explained as a contract that shows the interest of an individual

in the assets of the entity remaining after subtracting all the liabilities. There are various

categories of equity instrument which are (Das, 2015):

Common Stock: It is a common instrument issued by a public company to raise

funds from the public. Under this stock the shareholders have the right to vote and is

entitled to co-ownership of the company. The holder is also entitled to receive

dividend and is entitled to receive entire share value acquired by them at the time of

winding up of the company.

Convertible Debentures: The unique feature of this bond is that it entitles the holder

to convert such bonds into the common stock. Holder of the convertible debentures is

Financial Liability: Financial liabilities are those future sacrifices that an entity is

required to make in terms of economic benefits which arises due to some past transaction

or any other activity in the past. This sacrifices that are required to be made in the future

can be in the form of money or services owed to the other entity or party (Skoglund and

Chen, 2015). It can also be defined as any liability that is a contractual obligation to give

cash or any other financial instrument to the other party, or to change the financial asset

to write off the liability under conditions that may be potentially unfavourable for the

entity. Financial liability includes interest and debt payables which arises as a result of

using other’s money in the past and accounts payable such as rent, purchases and lease

payable to the other parties for the use of their products and spaces in the past.

Equity Instrument: It refers to any documents which serve as legal evidence to individual

or entity for proving their right in the firm. The instrument is primarily used to fund the

business, and the individual who holds an equity instrument in the entity is called a

shareholder. It can also be explained as a contract that shows the interest of an individual

in the assets of the entity remaining after subtracting all the liabilities. There are various

categories of equity instrument which are (Das, 2015):

Common Stock: It is a common instrument issued by a public company to raise

funds from the public. Under this stock the shareholders have the right to vote and is

entitled to co-ownership of the company. The holder is also entitled to receive

dividend and is entitled to receive entire share value acquired by them at the time of

winding up of the company.

Convertible Debentures: The unique feature of this bond is that it entitles the holder

to convert such bonds into the common stock. Holder of the convertible debentures is

5ADVANCE ACCOUNTING

entitled to a defined rate of interest irrespective of the profit of the company. These

bonds are popular for their profitable returns.

Preferred Stock: It is also a common stock which involves the holder’s participation

in the ownership of the company. The variation lies in the prior payments made at the

time of distribution of dividends or distribution at the time of winding up of the

company.

Depository Receipt: Investors holding the depository receipt has the benefits similar

to that of shareholder in every aspect.

Classification as liability or Equity.

As per IAS 32, the fundamental principal is to classify financial instrument either as an

equity instrument or financial liability according to the substance of the contract and from its

definition but not in its legal form. The decision regarding whether the item is financial liability

or equity should be made initially at the time of recognition and it should not be changed with

the change in the circumstances (Maglio, Agliata and Tuccillo, 2017).

Classification of the instrument as debt or equity is vital because it directly affects in the

valuation of gearing ratio, which is a critical measure that the financial user or stakeholders uses

to measure the financial risk of the entity. The distinction that will arise from improper

classification will also impact the profit of the company as the financial cost related with the

financial liabilities will be charged in the profit and statement which will result in an

understatement of profit and therefore lower will be the tax payable to the government.

Similarly, the dividends payable to the equity will be assigned from the profits, rather being

treated as an expense (Worthington, 2016). Treating the equity as liability will not only decrease

the profit but will also reduce the earning per share (EPS) of the company, thereby impacting the

entitled to a defined rate of interest irrespective of the profit of the company. These

bonds are popular for their profitable returns.

Preferred Stock: It is also a common stock which involves the holder’s participation

in the ownership of the company. The variation lies in the prior payments made at the

time of distribution of dividends or distribution at the time of winding up of the

company.

Depository Receipt: Investors holding the depository receipt has the benefits similar

to that of shareholder in every aspect.

Classification as liability or Equity.

As per IAS 32, the fundamental principal is to classify financial instrument either as an

equity instrument or financial liability according to the substance of the contract and from its

definition but not in its legal form. The decision regarding whether the item is financial liability

or equity should be made initially at the time of recognition and it should not be changed with

the change in the circumstances (Maglio, Agliata and Tuccillo, 2017).

Classification of the instrument as debt or equity is vital because it directly affects in the

valuation of gearing ratio, which is a critical measure that the financial user or stakeholders uses

to measure the financial risk of the entity. The distinction that will arise from improper

classification will also impact the profit of the company as the financial cost related with the

financial liabilities will be charged in the profit and statement which will result in an

understatement of profit and therefore lower will be the tax payable to the government.

Similarly, the dividends payable to the equity will be assigned from the profits, rather being

treated as an expense (Worthington, 2016). Treating the equity as liability will not only decrease

the profit but will also reduce the earning per share (EPS) of the company, thereby impacting the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ADVANCE ACCOUNTING

funding ability of the company since investors decide based on EPS of the company. A single

instrument issued may contain the qualities of both equity and liability, for example, a

convertible bond, it is the bond which comprises the feature of converting it into shares rather

than being repaid in cash than the accounting of such instrument will be done at the time when

such debentures are converted into common stock, thereby reducing the liability and increasing

the equity in the financial statement should be done. Equity Instrument cannot be re-measured.

Changes in the fair value of the shares are is not measured by the entity while preparing financial

statement, as the gain or loss will be experienced by the owner itself. The dividend is also paid

from the retained earnings so it does not affect the carrying value of the equity instrument. On

the other hand, if the shares issued are redeemable than the shares will be classified as a financial

liability (debt) as the issuer will be required to pay back the money in future. Moreover, if there

is a contractual right or obligation to deliver equity instrument to other entity for the benefits

received in some fixed monetary amount, then such obligation is a financial liability.

A new standard AASB 9 is applicable for the entities reporting from the period beginning

January 2018. This new standard provides classification and measurement of assets and

liabilities in the financial statement. This standard provided a new set of hedge accounting rules

and laid down new principal for the impairment of financial assets.

Conclusion

The above report focusses on the importance of the accounting classification of the

financial instrument and its consideration as a debt or equity. The classification plays a vital role

in the financial report as it changes the decision of the user if any measurement is not

appropriate. An inappropriate measure can lead to understatement or overstatement of profit and

other dividend related decisions which are material to the user of the financial statement. The

funding ability of the company since investors decide based on EPS of the company. A single

instrument issued may contain the qualities of both equity and liability, for example, a

convertible bond, it is the bond which comprises the feature of converting it into shares rather

than being repaid in cash than the accounting of such instrument will be done at the time when

such debentures are converted into common stock, thereby reducing the liability and increasing

the equity in the financial statement should be done. Equity Instrument cannot be re-measured.

Changes in the fair value of the shares are is not measured by the entity while preparing financial

statement, as the gain or loss will be experienced by the owner itself. The dividend is also paid

from the retained earnings so it does not affect the carrying value of the equity instrument. On

the other hand, if the shares issued are redeemable than the shares will be classified as a financial

liability (debt) as the issuer will be required to pay back the money in future. Moreover, if there

is a contractual right or obligation to deliver equity instrument to other entity for the benefits

received in some fixed monetary amount, then such obligation is a financial liability.

A new standard AASB 9 is applicable for the entities reporting from the period beginning

January 2018. This new standard provides classification and measurement of assets and

liabilities in the financial statement. This standard provided a new set of hedge accounting rules

and laid down new principal for the impairment of financial assets.

Conclusion

The above report focusses on the importance of the accounting classification of the

financial instrument and its consideration as a debt or equity. The classification plays a vital role

in the financial report as it changes the decision of the user if any measurement is not

appropriate. An inappropriate measure can lead to understatement or overstatement of profit and

other dividend related decisions which are material to the user of the financial statement. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ADVANCE ACCOUNTING

adverse impact has been highlighted which will affect the entity financial position if

classification is done inappropriately. The recent amendment of the new standard AASB 9 has

also been highlighted which provides a principal for the impairment of the asset.

adverse impact has been highlighted which will affect the entity financial position if

classification is done inappropriately. The recent amendment of the new standard AASB 9 has

also been highlighted which provides a principal for the impairment of the asset.

8ADVANCE ACCOUNTING

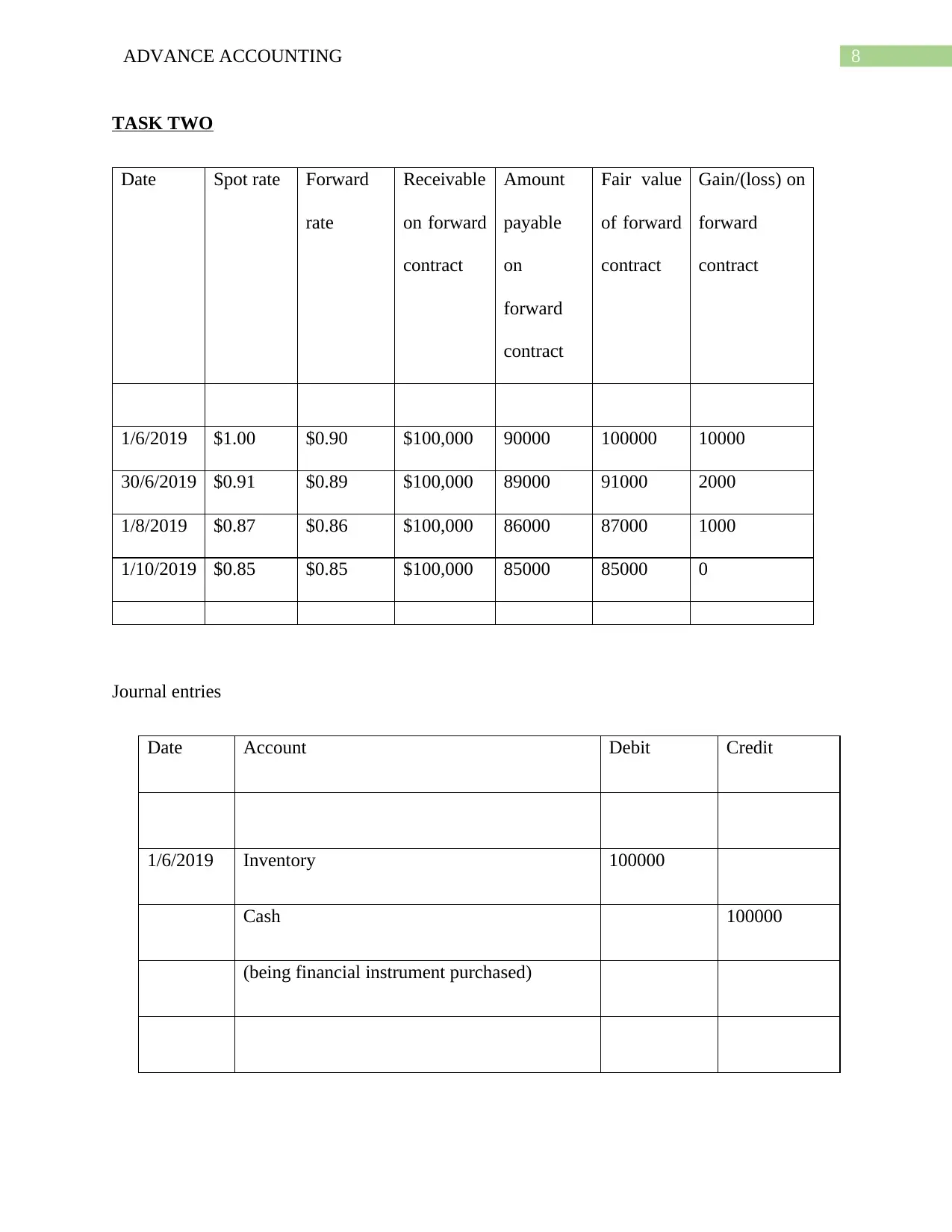

TASK TWO

Date Spot rate Forward

rate

Receivable

on forward

contract

Amount

payable

on

forward

contract

Fair value

of forward

contract

Gain/(loss) on

forward

contract

1/6/2019 $1.00 $0.90 $100,000 90000 100000 10000

30/6/2019 $0.91 $0.89 $100,000 89000 91000 2000

1/8/2019 $0.87 $0.86 $100,000 86000 87000 1000

1/10/2019 $0.85 $0.85 $100,000 85000 85000 0

Journal entries

Date Account Debit Credit

1/6/2019 Inventory 100000

Cash 100000

(being financial instrument purchased)

TASK TWO

Date Spot rate Forward

rate

Receivable

on forward

contract

Amount

payable

on

forward

contract

Fair value

of forward

contract

Gain/(loss) on

forward

contract

1/6/2019 $1.00 $0.90 $100,000 90000 100000 10000

30/6/2019 $0.91 $0.89 $100,000 89000 91000 2000

1/8/2019 $0.87 $0.86 $100,000 86000 87000 1000

1/10/2019 $0.85 $0.85 $100,000 85000 85000 0

Journal entries

Date Account Debit Credit

1/6/2019 Inventory 100000

Cash 100000

(being financial instrument purchased)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

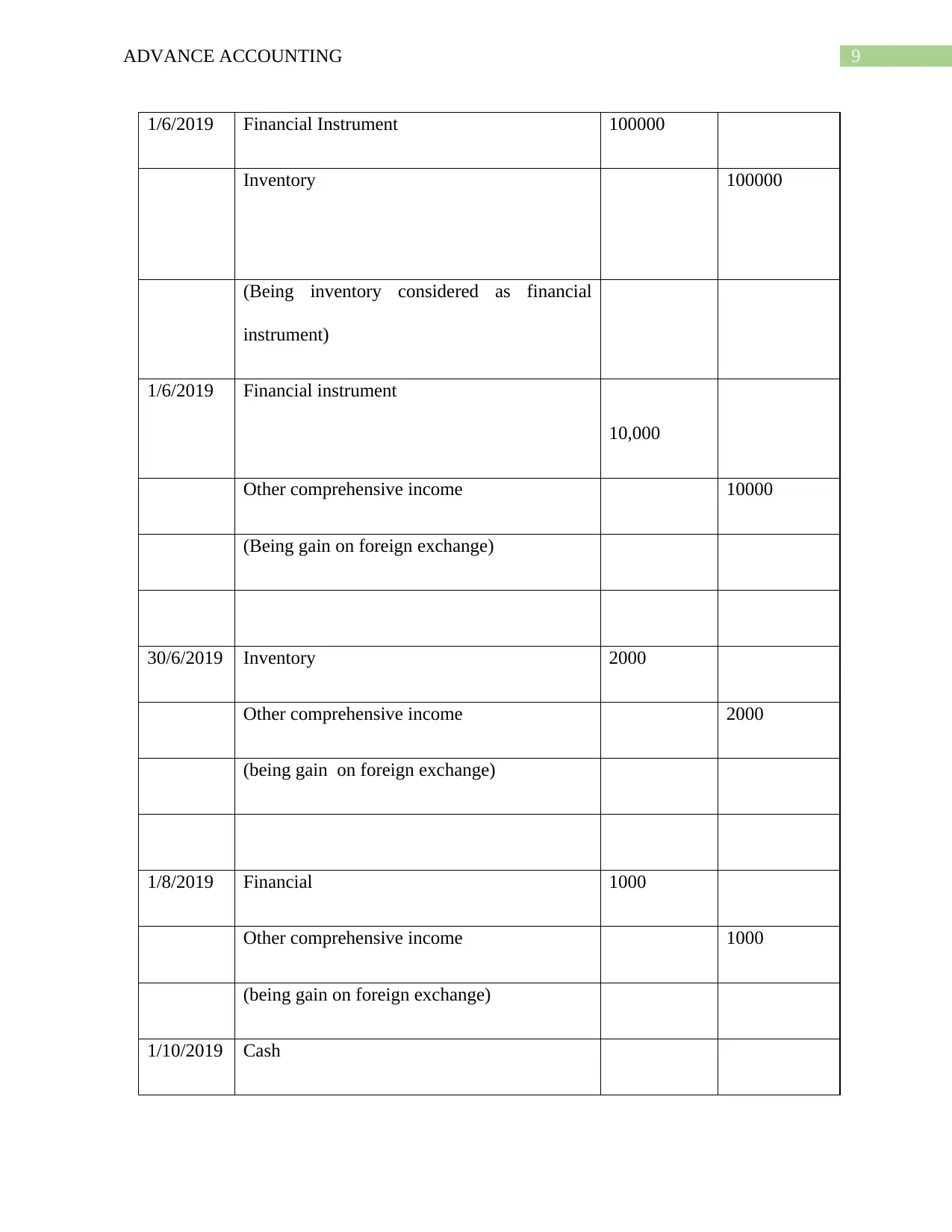

9ADVANCE ACCOUNTING

1/6/2019 Financial Instrument 100000

Inventory 100000

(Being inventory considered as financial

instrument)

1/6/2019 Financial instrument

10,000

Other comprehensive income 10000

(Being gain on foreign exchange)

30/6/2019 Inventory 2000

Other comprehensive income 2000

(being gain on foreign exchange)

1/8/2019 Financial 1000

Other comprehensive income 1000

(being gain on foreign exchange)

1/10/2019 Cash

1/6/2019 Financial Instrument 100000

Inventory 100000

(Being inventory considered as financial

instrument)

1/6/2019 Financial instrument

10,000

Other comprehensive income 10000

(Being gain on foreign exchange)

30/6/2019 Inventory 2000

Other comprehensive income 2000

(being gain on foreign exchange)

1/8/2019 Financial 1000

Other comprehensive income 1000

(being gain on foreign exchange)

1/10/2019 Cash

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

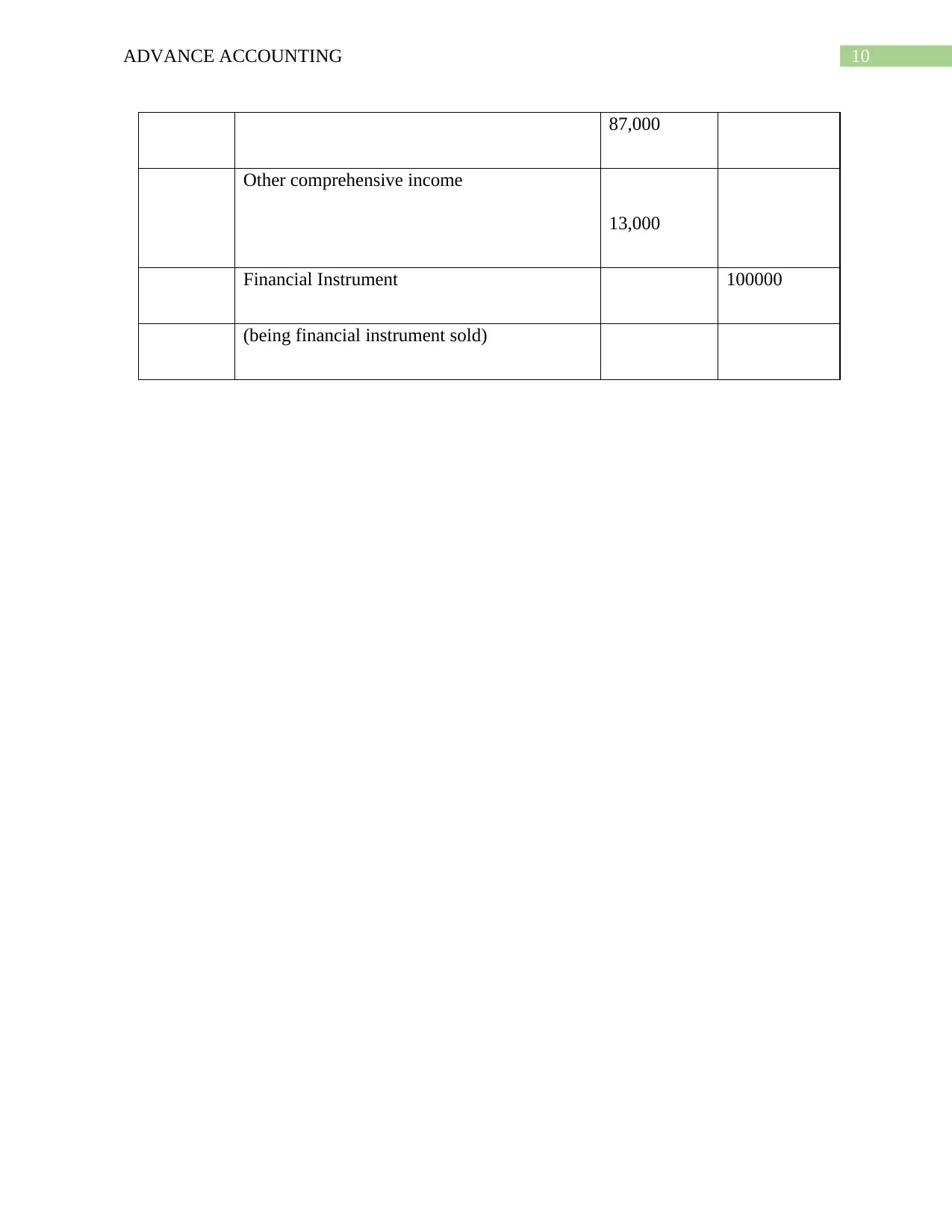

10ADVANCE ACCOUNTING

87,000

Other comprehensive income

13,000

Financial Instrument 100000

(being financial instrument sold)

87,000

Other comprehensive income

13,000

Financial Instrument 100000

(being financial instrument sold)

11ADVANCE ACCOUNTING

Reference

Das, S.C., 2015. The Financial System in India: Markets, Instruments, Institutions, Services and

Regulations. PHI Learning Pvt. Ltd.

Fabozzi, F.J. ed., 2018. The handbook of financial instruments. John Wiley & Sons.

Iasplus.com. (2020). IAS 32 — Financial Instruments: Presentation.

https://www.iasplus.com/en/standards/ias/ias32.

Maglio, R., Agliata, F. and Tuccillo, D., 2017. Trend of IASB Project on the Distinction between

Equity and Liabilities: The Case for Cooperatives and Continental European Firms.

Mullinova, S., 2016. Use of the principles of IFRS (IAS) 39" Financial instruments: recognition

and assessment" for bank financial accounting. Modern European Researches, (1), pp.60-64.

Pwc.com. (2020). Available at:

https://www.pwc.com/gx/en/ifrs-reporting/pdf/financial_instruments_guide_maze.pdf

Skoglund, J. and Chen, W., 2015. Financial risk management: Applications in market, credit,

asset and liability management and firmwide risk. John Wiley & Sons.

Tan, B.S. and Low, K.Y., 2017. Bitcoin–its economics for financial reporting. Australian

Accounting Review, 27(2), pp.220-227.

Uyar, A., Kılıç, M. and Gökçen, B.A., 2016. Compliance with IAS/IFRS and firm

characteristics: evidence from the emerging capital market of Turkey. Economic research-

Ekonomska istraživanja, 29(1), pp.148-161.

Wild, K., Creighton, B. and Simmonds, A., 2015. Gaap 2000: UK Financial Reporting. Springer.

Reference

Das, S.C., 2015. The Financial System in India: Markets, Instruments, Institutions, Services and

Regulations. PHI Learning Pvt. Ltd.

Fabozzi, F.J. ed., 2018. The handbook of financial instruments. John Wiley & Sons.

Iasplus.com. (2020). IAS 32 — Financial Instruments: Presentation.

https://www.iasplus.com/en/standards/ias/ias32.

Maglio, R., Agliata, F. and Tuccillo, D., 2017. Trend of IASB Project on the Distinction between

Equity and Liabilities: The Case for Cooperatives and Continental European Firms.

Mullinova, S., 2016. Use of the principles of IFRS (IAS) 39" Financial instruments: recognition

and assessment" for bank financial accounting. Modern European Researches, (1), pp.60-64.

Pwc.com. (2020). Available at:

https://www.pwc.com/gx/en/ifrs-reporting/pdf/financial_instruments_guide_maze.pdf

Skoglund, J. and Chen, W., 2015. Financial risk management: Applications in market, credit,

asset and liability management and firmwide risk. John Wiley & Sons.

Tan, B.S. and Low, K.Y., 2017. Bitcoin–its economics for financial reporting. Australian

Accounting Review, 27(2), pp.220-227.

Uyar, A., Kılıç, M. and Gökçen, B.A., 2016. Compliance with IAS/IFRS and firm

characteristics: evidence from the emerging capital market of Turkey. Economic research-

Ekonomska istraživanja, 29(1), pp.148-161.

Wild, K., Creighton, B. and Simmonds, A., 2015. Gaap 2000: UK Financial Reporting. Springer.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.