Financial Accounting Report: Impairment, Leasing Standards Analysis

VerifiedAdded on 2020/05/28

|11

|1965

|60

Report

AI Summary

This report delves into advanced financial accounting concepts, specifically focusing on impairment testing of goodwill and the implications of new lease accounting standards. Part A examines the impairment testing conducted by Worley Parsons Limited, detailing the methodologies, key assumptions, and sensitivity analyses employed. It addresses the extent of subjectivity in estimates and the transparency of the impairment testing process. Part B critically evaluates the former lease accounting standard, highlighting its shortcomings in reflecting economic reality and its impact on financial statement users. The analysis explores the controversies surrounding the distinction between financing and operating leases and the potential impact of the new leasing standard on organizations, including the associated costs and complexities. The report concludes by emphasizing the importance of the new standard in reflecting organizations' true financial state and facilitating informed decisions by investors. The report uses the Worley Parsons case study and reviews the literature on lease accounting and impairment.

Running head: ADVANCED FINANCIAL ACCOUNTING

Advanced financial accounting

Name of the university

Name of the student

Authors note

Advanced financial accounting

Name of the university

Name of the student

Authors note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Assessment Task Part A:.................................................................................................................2

Requirement i).................................................................................................................................2

Requirement ii)................................................................................................................................2

Requirement iii)...............................................................................................................................2

Requirement iv)...............................................................................................................................3

Requirement v)................................................................................................................................3

Requirement vi)...............................................................................................................................4

Requirement vii)..............................................................................................................................4

Requirement viii).............................................................................................................................5

Assessment Task Part B:.................................................................................................................5

Requirement i).................................................................................................................................5

Requirement ii)................................................................................................................................6

Requirement iii)...............................................................................................................................7

Requirement iv)...............................................................................................................................7

Requirement v)................................................................................................................................8

References list:...............................................................................................................................10

ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Assessment Task Part A:.................................................................................................................2

Requirement i).................................................................................................................................2

Requirement ii)................................................................................................................................2

Requirement iii)...............................................................................................................................2

Requirement iv)...............................................................................................................................3

Requirement v)................................................................................................................................3

Requirement vi)...............................................................................................................................4

Requirement vii)..............................................................................................................................4

Requirement viii).............................................................................................................................5

Assessment Task Part B:.................................................................................................................5

Requirement i).................................................................................................................................5

Requirement ii)................................................................................................................................6

Requirement iii)...............................................................................................................................7

Requirement iv)...............................................................................................................................7

Requirement v)................................................................................................................................8

References list:...............................................................................................................................10

2

ADVANCED FINANCIAL ACCOUNTING

Assessment Task Part A:

Requirement i)

Impairment testing of goodwill has been done unless there is an indication of impairment

and the carrying value of goodwill is done by deducting accumulated impairment. The

allocations of goodwill that are acquired are done to the cash generating units for impairment

testing. For the reporting date, 2015 Worley parsons limited has conducted an impairment testing

of goodwill of amount $ 198.6 million in financial year 2016 and there was recognition of

impairment of investment in associates of $ 12.1 million and the total amount of accumulated

impairment was recorded at $ 200.2 million (Worleyparsons.com, 2018).

Requirement ii)

The determination of impairment is done by assessing recoverable amount of cash

generating unit of group that is related to goodwill. Group recognizes impairment loss whenever

there is carrying amount of assets is more than their recoverable amount. The calculation of

impairment testing is done by using projections of cash flow that is based on financial forecast of

how the business will be performing consistently with external data and current and historical

experience. Organization is required to make assumptions about any uncertain future events for

estimating future cash flows (Worleyparsons.com, 2018).

ADVANCED FINANCIAL ACCOUNTING

Assessment Task Part A:

Requirement i)

Impairment testing of goodwill has been done unless there is an indication of impairment

and the carrying value of goodwill is done by deducting accumulated impairment. The

allocations of goodwill that are acquired are done to the cash generating units for impairment

testing. For the reporting date, 2015 Worley parsons limited has conducted an impairment testing

of goodwill of amount $ 198.6 million in financial year 2016 and there was recognition of

impairment of investment in associates of $ 12.1 million and the total amount of accumulated

impairment was recorded at $ 200.2 million (Worleyparsons.com, 2018).

Requirement ii)

The determination of impairment is done by assessing recoverable amount of cash

generating unit of group that is related to goodwill. Group recognizes impairment loss whenever

there is carrying amount of assets is more than their recoverable amount. The calculation of

impairment testing is done by using projections of cash flow that is based on financial forecast of

how the business will be performing consistently with external data and current and historical

experience. Organization is required to make assumptions about any uncertain future events for

estimating future cash flows (Worleyparsons.com, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ADVANCED FINANCIAL ACCOUNTING

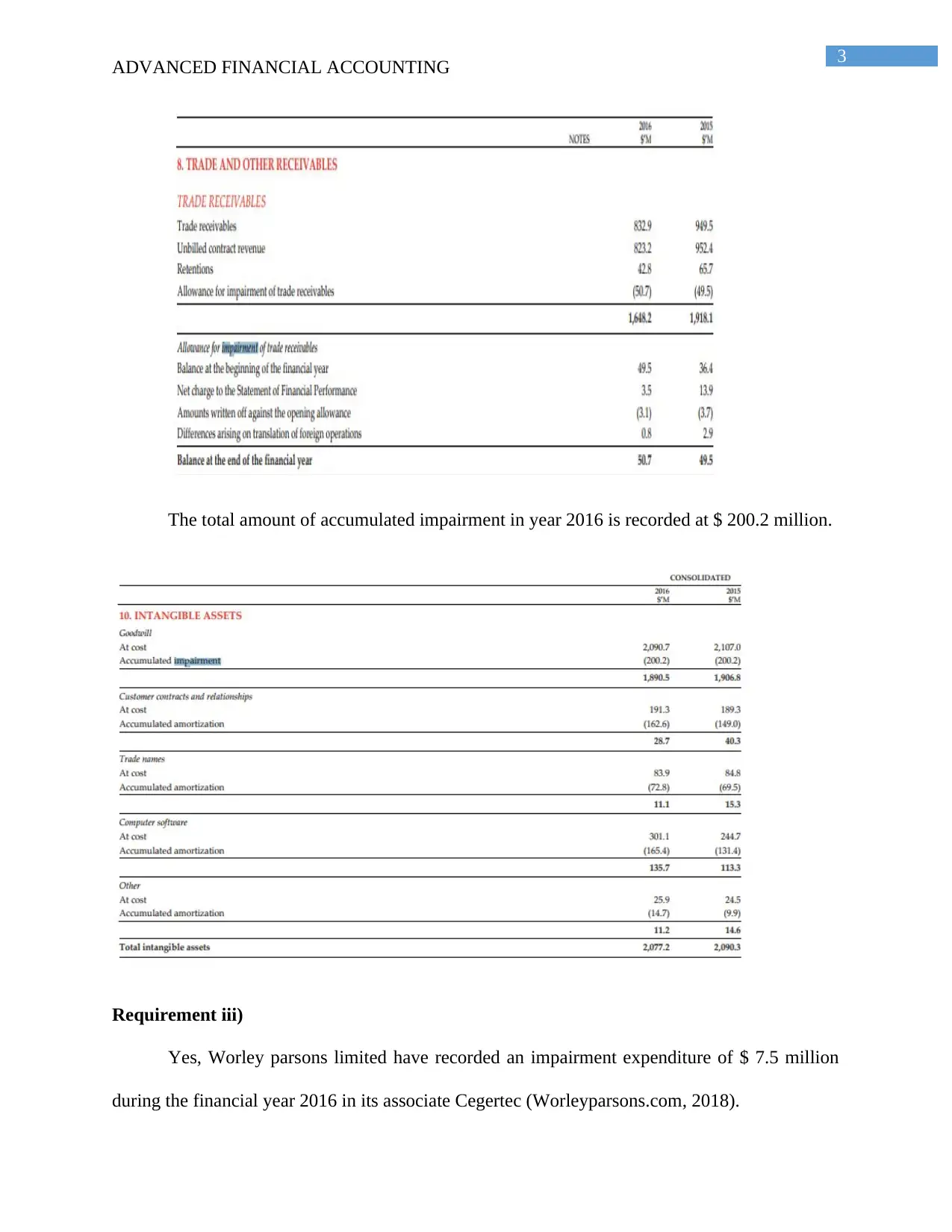

The total amount of accumulated impairment in year 2016 is recorded at $ 200.2 million.

Requirement iii)

Yes, Worley parsons limited have recorded an impairment expenditure of $ 7.5 million

during the financial year 2016 in its associate Cegertec (Worleyparsons.com, 2018).

ADVANCED FINANCIAL ACCOUNTING

The total amount of accumulated impairment in year 2016 is recorded at $ 200.2 million.

Requirement iii)

Yes, Worley parsons limited have recorded an impairment expenditure of $ 7.5 million

during the financial year 2016 in its associate Cegertec (Worleyparsons.com, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ADVANCED FINANCIAL ACCOUNTING

Requirement iv)

Organization makes use of key assumptions such as risk weighted pre discount tax rate

and growth rate beyond five years that is adjusted for risk in impairment testing for determining

value in use. Estimate of value in use is sensitive to long-term growth rate achievement, forecast

performance and discount rate. As part of impairment testing, group has performed sensitivity

analysis for ensuring that tests that have been carried out are reasonable. An allowance for

impairment has been established by the group through, which the estimated incurred loss

expenses are represented in respect of trade and other receivables (Worleyparsons.com, 2018).

Requirement v)

Extent and subjectivity of estimates along with judgment involved in collecting

information and inputs determines the accuracy of impairment testing. Impairment testing of

Worley parsons limited has involved certain degree of subjectivity. However, management of

organization has not acted opportunistically in determining resting of impairment.

Requirement vi)

Analysis of annual report of Worley parsons limited depicts that process of impairment

testing is quiet interesting. The method used for impairment testing by organization is presented

in a way that it can be well understood by users. Company uses sensitivity analysis for

determining the potential impacts of the risks associated with impairment testing

((Worleyparsons.com, 2018). There is segmented presentation of different concepts of

impairment testing presented in the annual report.

ADVANCED FINANCIAL ACCOUNTING

Requirement iv)

Organization makes use of key assumptions such as risk weighted pre discount tax rate

and growth rate beyond five years that is adjusted for risk in impairment testing for determining

value in use. Estimate of value in use is sensitive to long-term growth rate achievement, forecast

performance and discount rate. As part of impairment testing, group has performed sensitivity

analysis for ensuring that tests that have been carried out are reasonable. An allowance for

impairment has been established by the group through, which the estimated incurred loss

expenses are represented in respect of trade and other receivables (Worleyparsons.com, 2018).

Requirement v)

Extent and subjectivity of estimates along with judgment involved in collecting

information and inputs determines the accuracy of impairment testing. Impairment testing of

Worley parsons limited has involved certain degree of subjectivity. However, management of

organization has not acted opportunistically in determining resting of impairment.

Requirement vi)

Analysis of annual report of Worley parsons limited depicts that process of impairment

testing is quiet interesting. The method used for impairment testing by organization is presented

in a way that it can be well understood by users. Company uses sensitivity analysis for

determining the potential impacts of the risks associated with impairment testing

((Worleyparsons.com, 2018). There is segmented presentation of different concepts of

impairment testing presented in the annual report.

5

ADVANCED FINANCIAL ACCOUNTING

Requirement vii)

Users of financial statement of group are able to get new insights in terms of performance

of sensitivity analysis forming part of impairment testing. For the entire cash-generating unit,

group performance sensitivity analysis on related inputs such as post discount rate, terminal

growth rate and cash flow forecasting (Worleyparsons.com, 2018). Whether an organization

requires the group determines impairment allowance by making proper judgments.

Requirement viii)

The determination of fair value of both non-financial liabilities and assets are done as per

the disclosure and accounting policies of group. Notes to financial statements makes disclosures

about assumptions used in determining fair value of specific assets and liabilities. From the

analysis of annual report of the group, it is depicted that measurement of derivative financial

instruments are done at fair value. Measurement and recognition of revenue is performed at fair

value and group makes the amortization of fair value of rights over the performance period

(Miller & Upton, 2014). It has been identified from annual report that the carrying amount of all

cash-generating units is less than their combined fair value.

Assessment Task Part B:

Requirement i)

Former accounting standard is associated with several criticisms, as it did not provide

users with clear picture of the financial position reporting entity. For similar transactions, there is

different accounting due to application of different accounting models. Operating leases are not

mandated to be disclosed under the balance sheet under existing standard. Therefore, the actual

amount of liabilities of organization might be higher than liabilities represented on balance sheet

ADVANCED FINANCIAL ACCOUNTING

Requirement vii)

Users of financial statement of group are able to get new insights in terms of performance

of sensitivity analysis forming part of impairment testing. For the entire cash-generating unit,

group performance sensitivity analysis on related inputs such as post discount rate, terminal

growth rate and cash flow forecasting (Worleyparsons.com, 2018). Whether an organization

requires the group determines impairment allowance by making proper judgments.

Requirement viii)

The determination of fair value of both non-financial liabilities and assets are done as per

the disclosure and accounting policies of group. Notes to financial statements makes disclosures

about assumptions used in determining fair value of specific assets and liabilities. From the

analysis of annual report of the group, it is depicted that measurement of derivative financial

instruments are done at fair value. Measurement and recognition of revenue is performed at fair

value and group makes the amortization of fair value of rights over the performance period

(Miller & Upton, 2014). It has been identified from annual report that the carrying amount of all

cash-generating units is less than their combined fair value.

Assessment Task Part B:

Requirement i)

Former accounting standard is associated with several criticisms, as it did not provide

users with clear picture of the financial position reporting entity. For similar transactions, there is

different accounting due to application of different accounting models. Operating leases are not

mandated to be disclosed under the balance sheet under existing standard. Therefore, the actual

amount of liabilities of organization might be higher than liabilities represented on balance sheet

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ADVANCED FINANCIAL ACCOUNTING

(Sliwoski, 2017). Moreover, existing standard, there is loss of transparency as users find it

difficulties in estimating total liabilities and assets pertaining to leases. Hence, former accounting

standard does not reflect economic reality.

Requirement ii)

Former lease standard requires capital lease to be disclosed in the balance sheet while

operating leases are not mandated to be disclosed. It is certainly possible there will be thousands

of leased assets and liabilities that an organization might have and they are not disclosed on

balance sheet and are not associated with financial metrics. However, total debts reported by

organizations are disclosed in the balance sheet but this amount might be less than what are

actual liabilities off balance sheets (Asyaeva et al., 2016). Therefore, the off balance sheet

liabilities were up to 66 times more than debt reported in the balance sheet.

Requirement iii)

Controversies on the former lease accounting standard are associated with its

complications in creating distinction between financing and operating. Investors using financial

statements are not able to make decisions due to transparency and lack of absolute information.

Either companies operating within airline industries are buying most of its fleet or they are

leasing their most of aircraft fleets. It indicates the fact that financial positions of such companies

are different. However, in actual scenario, there is similarity between these airline companies.

This is a reason why there was no level playing field between airline companies. Issue of no

level playing field between companies will be solved with the new lease standard (Brouwer et

al., 2017).

ADVANCED FINANCIAL ACCOUNTING

(Sliwoski, 2017). Moreover, existing standard, there is loss of transparency as users find it

difficulties in estimating total liabilities and assets pertaining to leases. Hence, former accounting

standard does not reflect economic reality.

Requirement ii)

Former lease standard requires capital lease to be disclosed in the balance sheet while

operating leases are not mandated to be disclosed. It is certainly possible there will be thousands

of leased assets and liabilities that an organization might have and they are not disclosed on

balance sheet and are not associated with financial metrics. However, total debts reported by

organizations are disclosed in the balance sheet but this amount might be less than what are

actual liabilities off balance sheets (Asyaeva et al., 2016). Therefore, the off balance sheet

liabilities were up to 66 times more than debt reported in the balance sheet.

Requirement iii)

Controversies on the former lease accounting standard are associated with its

complications in creating distinction between financing and operating. Investors using financial

statements are not able to make decisions due to transparency and lack of absolute information.

Either companies operating within airline industries are buying most of its fleet or they are

leasing their most of aircraft fleets. It indicates the fact that financial positions of such companies

are different. However, in actual scenario, there is similarity between these airline companies.

This is a reason why there was no level playing field between airline companies. Issue of no

level playing field between companies will be solved with the new lease standard (Brouwer et

al., 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ADVANCED FINANCIAL ACCOUNTING

Requirement iv)

New leasing standard that have been introduced is also subjected to several criticisms in

relation to its costs and complexities of organizations. New standard is likely to make lessees’

balance sheet profile more leveraged and this will come with the consequence of increasing cost

of borrowing by lessee. Organizations adapting to this standard will have increased cost of their

reporting and complexities relating to small assets concerning lease. Moreover, management

needs to have adequate information and the areas where they will have impact; hence,

knowledge adequacy is the prerequisite of adopting lease standard. It might be required to make

some alteration in their financial metrics and accounting process (Wong & Joshi, 2015). Some of

the lenders makes an estimate about leased assets and liabilities, therefore, bringing on balance

sheet is not regarded as apt.

Requirement v)

The financial state of affairs of organizations will be reflected truly with the adoption of

this new lease standard. Credit risks of lessee will be informed truly and this will help lenders in

getting detailed information. Pricing risk of lenders will be better understood new standard will

be well prepared for dealing with such standard. Organizations are required to conduct

preliminary assessment for determining how accounting process relating to lease will be

impacted by the standard. The categorization of lease into lease contract and service contracts is

performed by following a detailed guidance incorporated under this standard (Bohusova &

Svoboda, 2015). New lease standard will heavily affect the organization having leases. Investors

are not required to make any rough estimates about amount of leased liabilities and assets and it

will be presented by organization themselves (Dye et al., 2014). Therefore, there will be

ADVANCED FINANCIAL ACCOUNTING

Requirement iv)

New leasing standard that have been introduced is also subjected to several criticisms in

relation to its costs and complexities of organizations. New standard is likely to make lessees’

balance sheet profile more leveraged and this will come with the consequence of increasing cost

of borrowing by lessee. Organizations adapting to this standard will have increased cost of their

reporting and complexities relating to small assets concerning lease. Moreover, management

needs to have adequate information and the areas where they will have impact; hence,

knowledge adequacy is the prerequisite of adopting lease standard. It might be required to make

some alteration in their financial metrics and accounting process (Wong & Joshi, 2015). Some of

the lenders makes an estimate about leased assets and liabilities, therefore, bringing on balance

sheet is not regarded as apt.

Requirement v)

The financial state of affairs of organizations will be reflected truly with the adoption of

this new lease standard. Credit risks of lessee will be informed truly and this will help lenders in

getting detailed information. Pricing risk of lenders will be better understood new standard will

be well prepared for dealing with such standard. Organizations are required to conduct

preliminary assessment for determining how accounting process relating to lease will be

impacted by the standard. The categorization of lease into lease contract and service contracts is

performed by following a detailed guidance incorporated under this standard (Bohusova &

Svoboda, 2015). New lease standard will heavily affect the organization having leases. Investors

are not required to make any rough estimates about amount of leased liabilities and assets and it

will be presented by organization themselves (Dye et al., 2014). Therefore, there will be

8

ADVANCED FINANCIAL ACCOUNTING

accuracy of information’s presented in the financial report and will facilitate informed decisions

by investors.

ADVANCED FINANCIAL ACCOUNTING

accuracy of information’s presented in the financial report and will facilitate informed decisions

by investors.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ADVANCED FINANCIAL ACCOUNTING

References list:

Asyaeva, E. A., Chizhankova, I. V., Bondaletova, N. F., & Makushkin, S. A. (2016). Methods

for assessing the credit risk of leasing assets. International Journal of Economics and

Financial Issues, 6(1S).

Barone, E., Birt, J., & Moya, S. (2014). Lease accounting: a review of recent

literature. Accounting in Europe, 11(1), 35-54.

Bohusova, H., & Svoboda, P. (2015). Possible Amendment to IFRS for SMEs due to New

Approach to Operating Lease Reporting in Full IFRS: Effect on Financial Analysis

Ratios in Air Cargo Transportation in the Czech Republic.

Bourjade, S., Huc, R., & Muller-Vibes, C. (2017). Leasing and profitability: Empirical evidence

from the airline industry. Transportation Research Part A: Policy and Practice, 97, 30-

46.

Brouwer, A., Hoogendoorn, M., & Naarding, E. (2015). Will the changes proposed to the

conceptual framework's definitions and recognition criteria provide a better basis for

IASB standard setting?. Accounting and Business Research, 45(5), 547-571.

Dye, R. A., Glover, J. C., & Sunder, S. (2014). Financial engineering and the arms race between

accounting standard setters and preparers. Accounting Horizons, 29(2), 265-295.

Miller, M. H., & Upton, C. W. (2014). LEASING, BUYING, HND THE COST OF CAPITAL

SERVICES. Financial Decision Making Under Uncertainty, 95.

ADVANCED FINANCIAL ACCOUNTING

References list:

Asyaeva, E. A., Chizhankova, I. V., Bondaletova, N. F., & Makushkin, S. A. (2016). Methods

for assessing the credit risk of leasing assets. International Journal of Economics and

Financial Issues, 6(1S).

Barone, E., Birt, J., & Moya, S. (2014). Lease accounting: a review of recent

literature. Accounting in Europe, 11(1), 35-54.

Bohusova, H., & Svoboda, P. (2015). Possible Amendment to IFRS for SMEs due to New

Approach to Operating Lease Reporting in Full IFRS: Effect on Financial Analysis

Ratios in Air Cargo Transportation in the Czech Republic.

Bourjade, S., Huc, R., & Muller-Vibes, C. (2017). Leasing and profitability: Empirical evidence

from the airline industry. Transportation Research Part A: Policy and Practice, 97, 30-

46.

Brouwer, A., Hoogendoorn, M., & Naarding, E. (2015). Will the changes proposed to the

conceptual framework's definitions and recognition criteria provide a better basis for

IASB standard setting?. Accounting and Business Research, 45(5), 547-571.

Dye, R. A., Glover, J. C., & Sunder, S. (2014). Financial engineering and the arms race between

accounting standard setters and preparers. Accounting Horizons, 29(2), 265-295.

Miller, M. H., & Upton, C. W. (2014). LEASING, BUYING, HND THE COST OF CAPITAL

SERVICES. Financial Decision Making Under Uncertainty, 95.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ADVANCED FINANCIAL ACCOUNTING

Sandblom, P., & Strandberg, A. (2015). The Value Relevance of the Proposed New Leasing

Standard. An event study of the European Stock Markets’ Reaction to the proposed

replacement of IAS17.

Sliwoski, L. J. (2017). Understanding the New Lease Accounting Guidance. Journal of

Corporate Accounting & Finance, 28(4), 48-52.

Sliwoski, L. J. (2017). Understanding the New Lease Accounting Guidance. Journal of

Corporate Accounting & Finance, 28(4), 48-52.

Wong, K., & Joshi, M. (2015). The impact of lease capitalisation on financial statements and key

ratios: Evidence from Australia. Australasian Accounting Business & Finance

Journal, 9(3), 27.

Worleyparsons.com. (2018). Retrieved 16 January 2018, from

http://www.worleyparsons.com/InvestorRelations/reports/Documents/00_WOR822_2016

_Combined.pdf

ADVANCED FINANCIAL ACCOUNTING

Sandblom, P., & Strandberg, A. (2015). The Value Relevance of the Proposed New Leasing

Standard. An event study of the European Stock Markets’ Reaction to the proposed

replacement of IAS17.

Sliwoski, L. J. (2017). Understanding the New Lease Accounting Guidance. Journal of

Corporate Accounting & Finance, 28(4), 48-52.

Sliwoski, L. J. (2017). Understanding the New Lease Accounting Guidance. Journal of

Corporate Accounting & Finance, 28(4), 48-52.

Wong, K., & Joshi, M. (2015). The impact of lease capitalisation on financial statements and key

ratios: Evidence from Australia. Australasian Accounting Business & Finance

Journal, 9(3), 27.

Worleyparsons.com. (2018). Retrieved 16 January 2018, from

http://www.worleyparsons.com/InvestorRelations/reports/Documents/00_WOR822_2016

_Combined.pdf

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.