Advanced Financial Accounting Assignment: Tabcorp, Leasing Standard

VerifiedAdded on 2020/05/16

|9

|1533

|43

Report

AI Summary

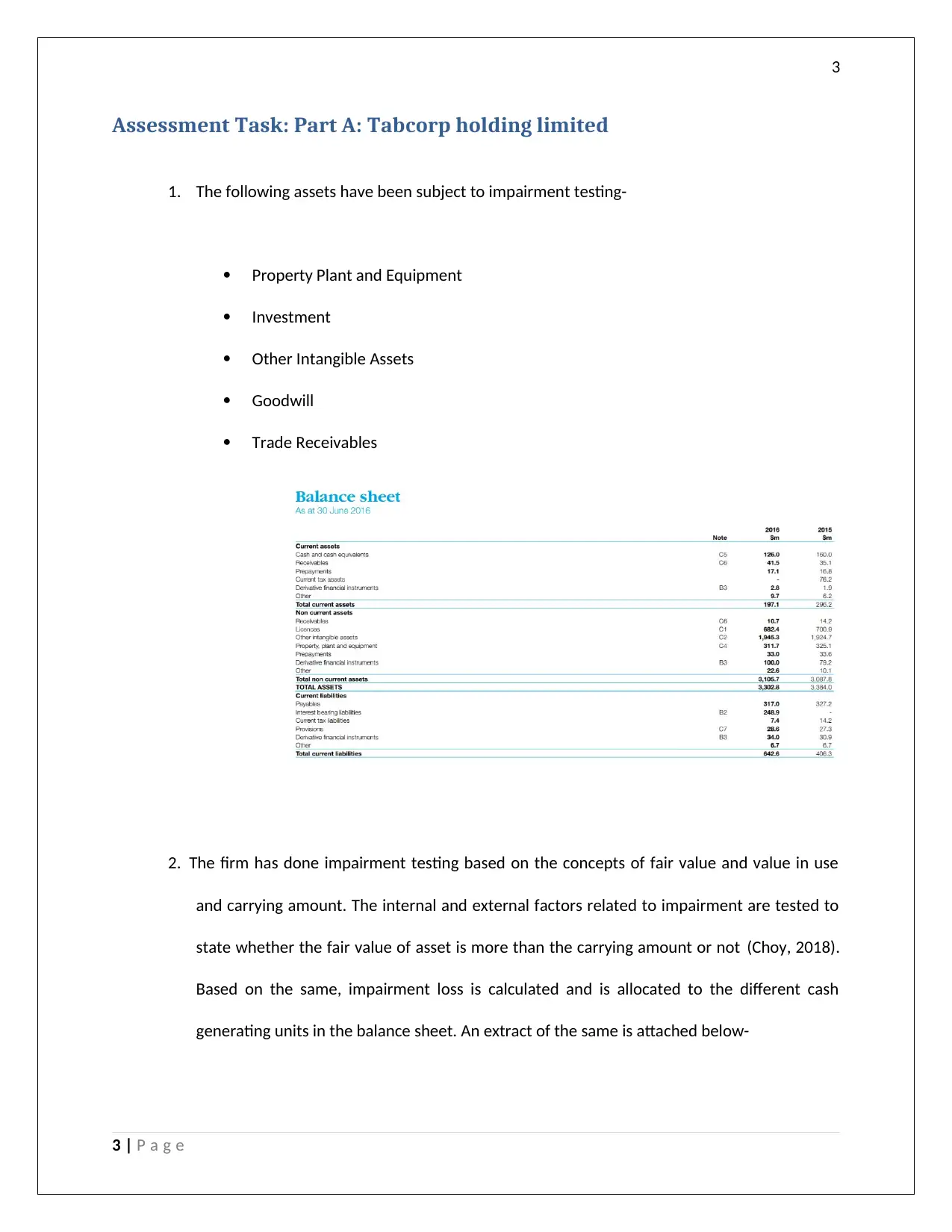

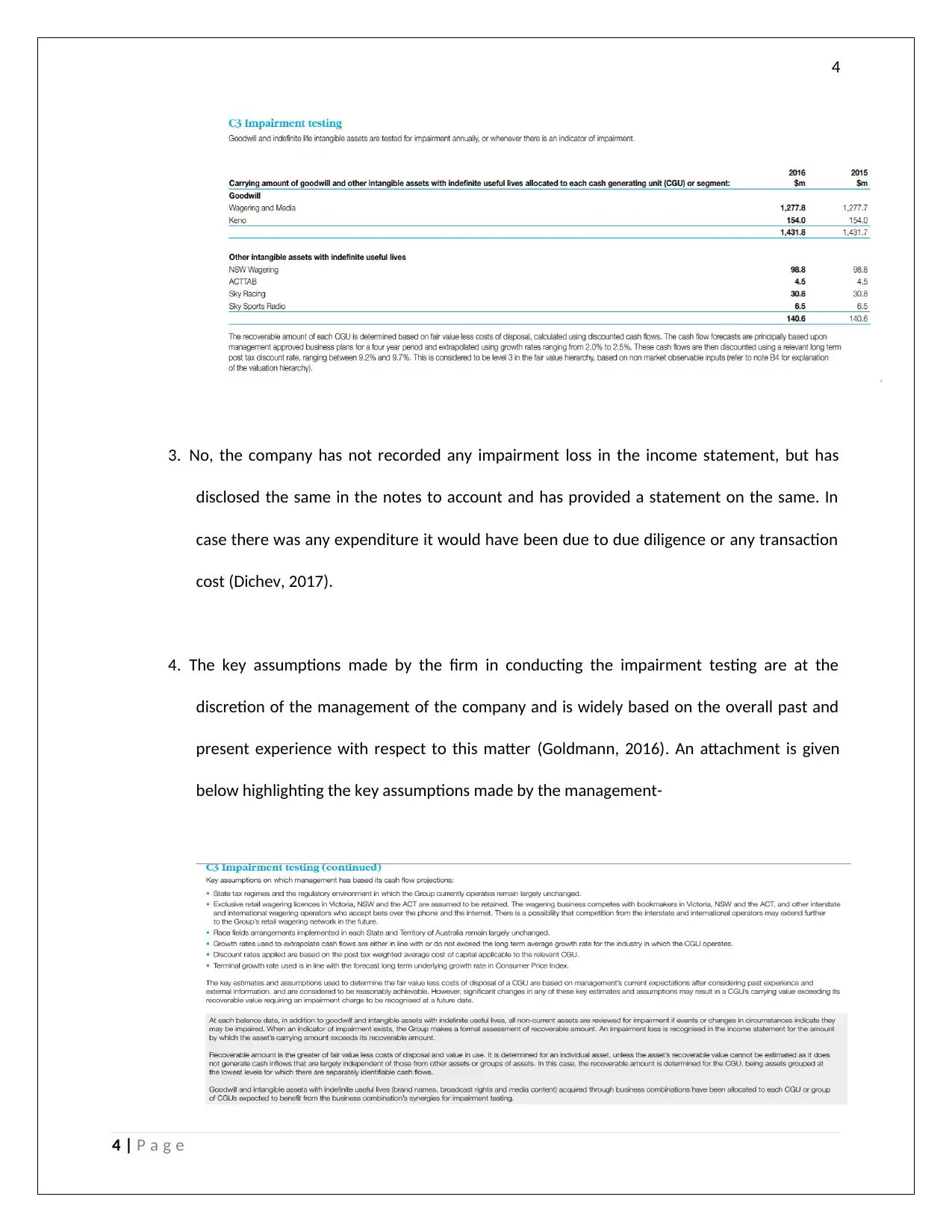

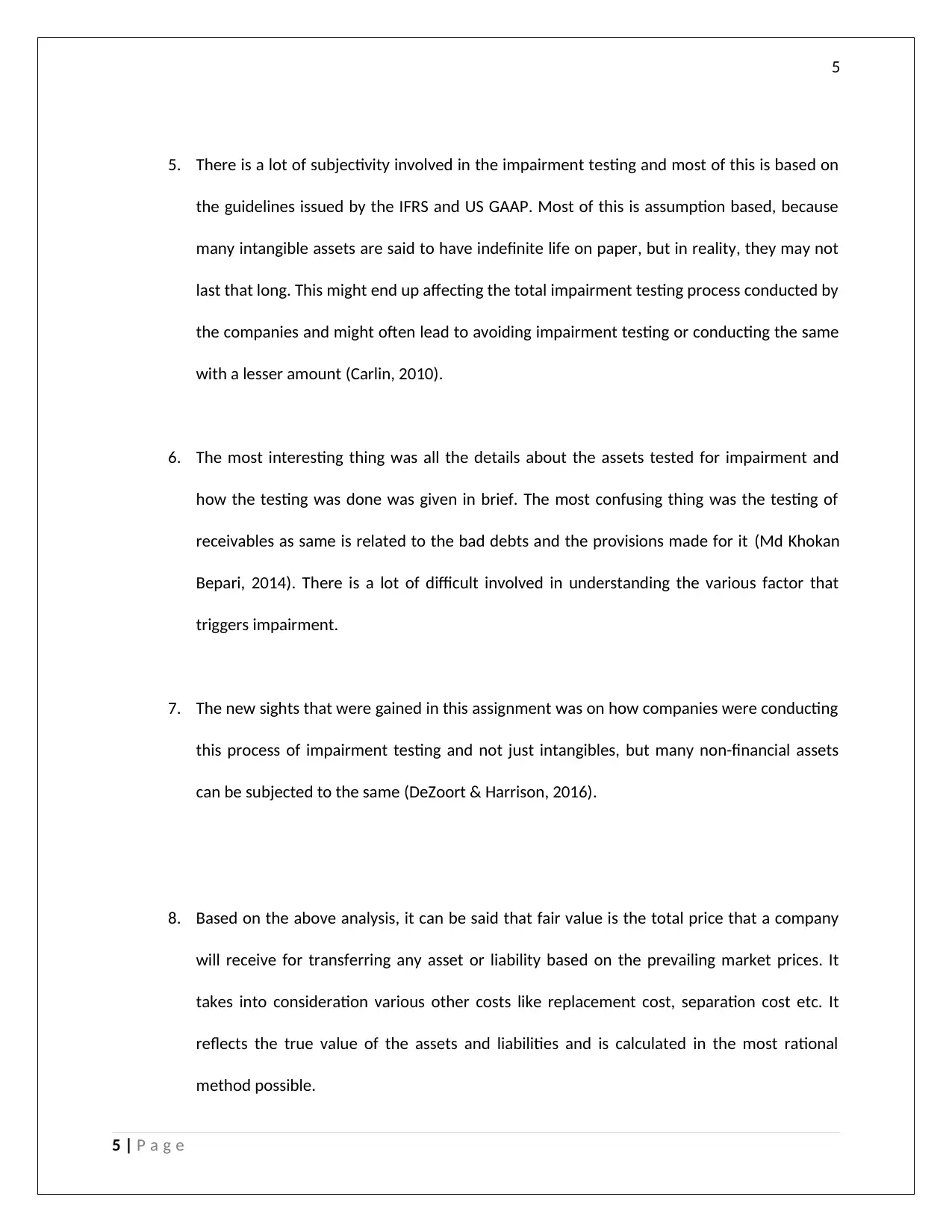

This report provides an in-depth analysis of advanced financial accounting topics. Part A focuses on Tabcorp Holdings Limited, examining impairment testing of various assets like Property Plant and Equipment, Investment, Other Intangible Assets, Goodwill, and Trade Receivables, based on fair value and value in use. It discusses the company's approach, key assumptions, and challenges in impairment testing, referencing IFRS and US GAAP guidelines. Part B evaluates the new leasing accounting standard, highlighting its advantages over the old standard. The analysis includes insights from IASB's chairperson, addressing the impact on financial statements, increased transparency, and the shift from operating to balance sheet liabilities. The report emphasizes the importance of the new standard for improved investor decisions and comparability across companies, while also acknowledging potential challenges in implementation.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.