HA3011: Advanced Financial Accounting Report on ASX Company

VerifiedAdded on 2022/10/17

|15

|3488

|13

Report

AI Summary

This report provides a comprehensive analysis of financial accounting principles and practices, focusing on the application of accounting concepts and the impact of the new accounting standard for leases, AASB 16. The report begins by identifying and describing key accounting concepts, such as the dual aspect, money measurement, accrual, going concern, and materiality concepts, as they are implemented by Costa Group Holdings Limited, an ASX-listed horticulture company. It then delves into the changes introduced by AASB 16, discussing the implications for the selected company and highlighting specific issues and complexities related to lease accounting. The analysis includes a discussion of the transition from AASB 117 to AASB 16, outlining the company's approach to compliance and the key disclosures made in its annual reports. The report examines how Costa Group Holdings Limited has recognized and disclosed leases under AASB 16, including right-of-use assets and lease liabilities. The report also considers the challenges faced in adopting the new standard, such as the need for comprehensive lease information, complex calculations, and changes in profit and expense recognition. The report concludes by summarizing the critical disclosures made by the company regarding its lease accounting practices, including the transition effects and implications for financial reporting. The analysis is based on the annual reports of Costa Group Holdings Limited and provides a practical understanding of financial accounting in the context of a real-world business.

1

HA3011 Advanced Financial Accounting

HA3011 Advanced Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Contents

Introduction......................................................................................................................................3

Part 1: Identification and Description of the Accounting Concepts Used by the Selected

Company..........................................................................................................................................3

Part 2: Discussion of Changes that have been incorporated in the new accounting standard for

lease AASB 16 in Relevance to Selected Company........................................................................6

Part 3: Key Disclosures made by Costa Holding Limited on accounting for leases (AASB 16.....8

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Contents

Introduction......................................................................................................................................3

Part 1: Identification and Description of the Accounting Concepts Used by the Selected

Company..........................................................................................................................................3

Part 2: Discussion of Changes that have been incorporated in the new accounting standard for

lease AASB 16 in Relevance to Selected Company........................................................................6

Part 3: Key Disclosures made by Costa Holding Limited on accounting for leases (AASB 16.....8

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

3

Introduction

The report has been developed for gaining an understanding of the key financial

accounting concepts. This has been carried out through examining the information published

within the annual report a selected ASX company. The analysis of the annual report is carried for

identifying the accounting concepts used by the company. This is followed by evaluating the

changes that have been introduced within the new accounting standard for lease AASB 16 within

the selected company in context of the relevant examples. Lastly, it summarizes the key

disclosures that the selected company has made in context of the leases accounting and the

impact of transition to AASB 16 from AASB 117. The company selected for the analysis

purpose is Costa Group Holdings Limited, a leading Australian horticulture company involved in

supplying products to the food retailers within the country.

Part 1: Identification and Description of the Accounting Concepts Used by the Selected

Company

The accounting concepts refer to the standardized principles and concepts that are used as

a basis for the development and presentation of annual accounts to the end-users. The accounting

concepts provides a basic framework for financial reporting by providing a set of necessary

assumptions and condition on which accounting of a firm needs to be carried out. As such, they

can also be referred to as postulates, assumptions or conditions that provide a basis for

development and presentation of the financial statements (Cunningham, 2014). The major

accounting concepts that have been used in development of annual report of Costa Holdings

Limited arte described as follows:

Dual Aspect Concept

This accounting concept states the recording of every business transaction in a dual

manner which means that each financial transaction will have two effect that is one on the debit

side while other on the credit side (Unegbu, 2014). The accounting concept is adequately

implemented within Costa Holdings Limited in the development and presentation of its various

financial statements. For example, issuing of an invoice to a customer leads to increase in the

Introduction

The report has been developed for gaining an understanding of the key financial

accounting concepts. This has been carried out through examining the information published

within the annual report a selected ASX company. The analysis of the annual report is carried for

identifying the accounting concepts used by the company. This is followed by evaluating the

changes that have been introduced within the new accounting standard for lease AASB 16 within

the selected company in context of the relevant examples. Lastly, it summarizes the key

disclosures that the selected company has made in context of the leases accounting and the

impact of transition to AASB 16 from AASB 117. The company selected for the analysis

purpose is Costa Group Holdings Limited, a leading Australian horticulture company involved in

supplying products to the food retailers within the country.

Part 1: Identification and Description of the Accounting Concepts Used by the Selected

Company

The accounting concepts refer to the standardized principles and concepts that are used as

a basis for the development and presentation of annual accounts to the end-users. The accounting

concepts provides a basic framework for financial reporting by providing a set of necessary

assumptions and condition on which accounting of a firm needs to be carried out. As such, they

can also be referred to as postulates, assumptions or conditions that provide a basis for

development and presentation of the financial statements (Cunningham, 2014). The major

accounting concepts that have been used in development of annual report of Costa Holdings

Limited arte described as follows:

Dual Aspect Concept

This accounting concept states the recording of every business transaction in a dual

manner which means that each financial transaction will have two effect that is one on the debit

side while other on the credit side (Unegbu, 2014). The accounting concept is adequately

implemented within Costa Holdings Limited in the development and presentation of its various

financial statements. For example, issuing of an invoice to a customer leads to increase in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

sales that are reflected within the income statement while accounts receivable is reflected as

assets within the balance sheet.

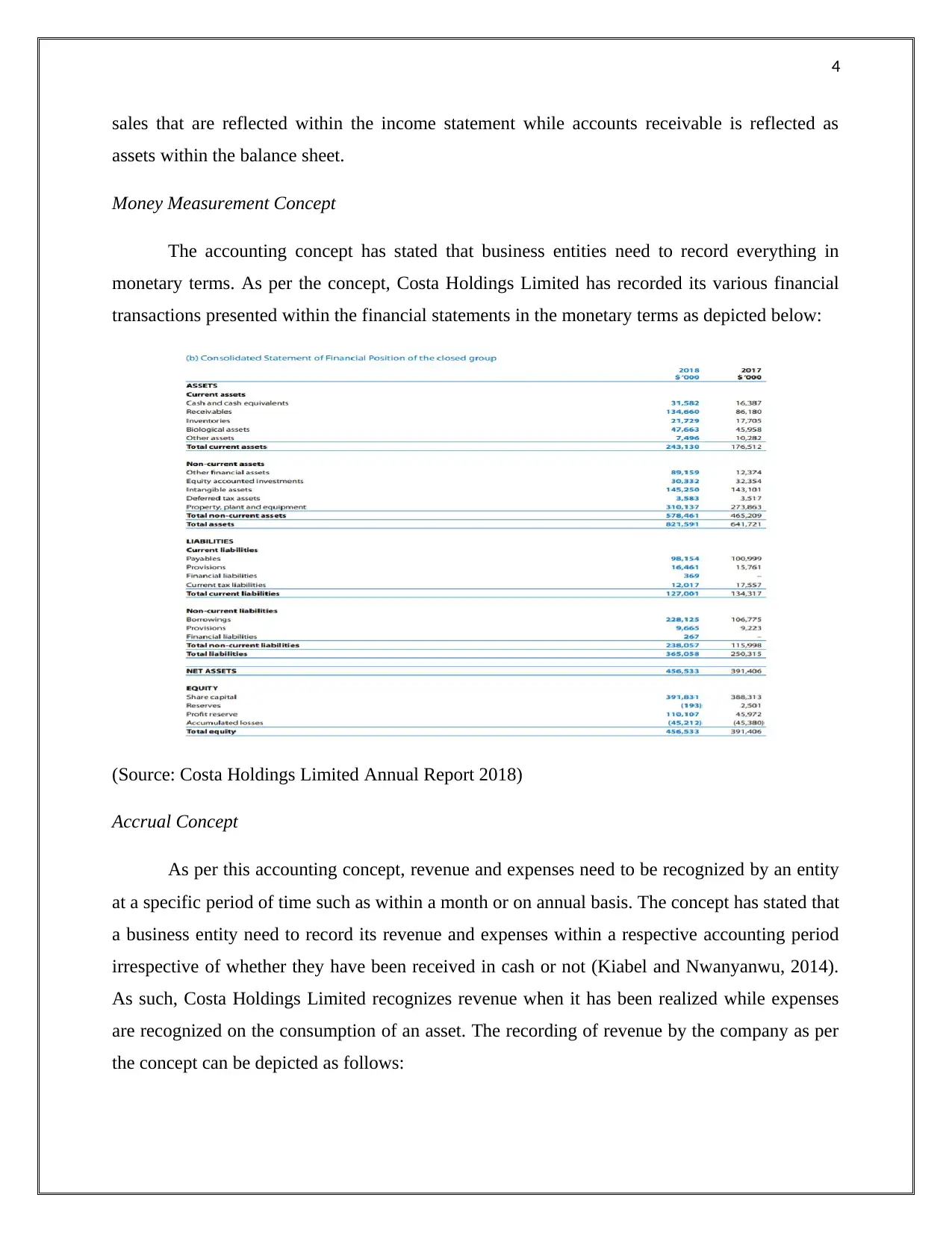

Money Measurement Concept

The accounting concept has stated that business entities need to record everything in

monetary terms. As per the concept, Costa Holdings Limited has recorded its various financial

transactions presented within the financial statements in the monetary terms as depicted below:

(Source: Costa Holdings Limited Annual Report 2018)

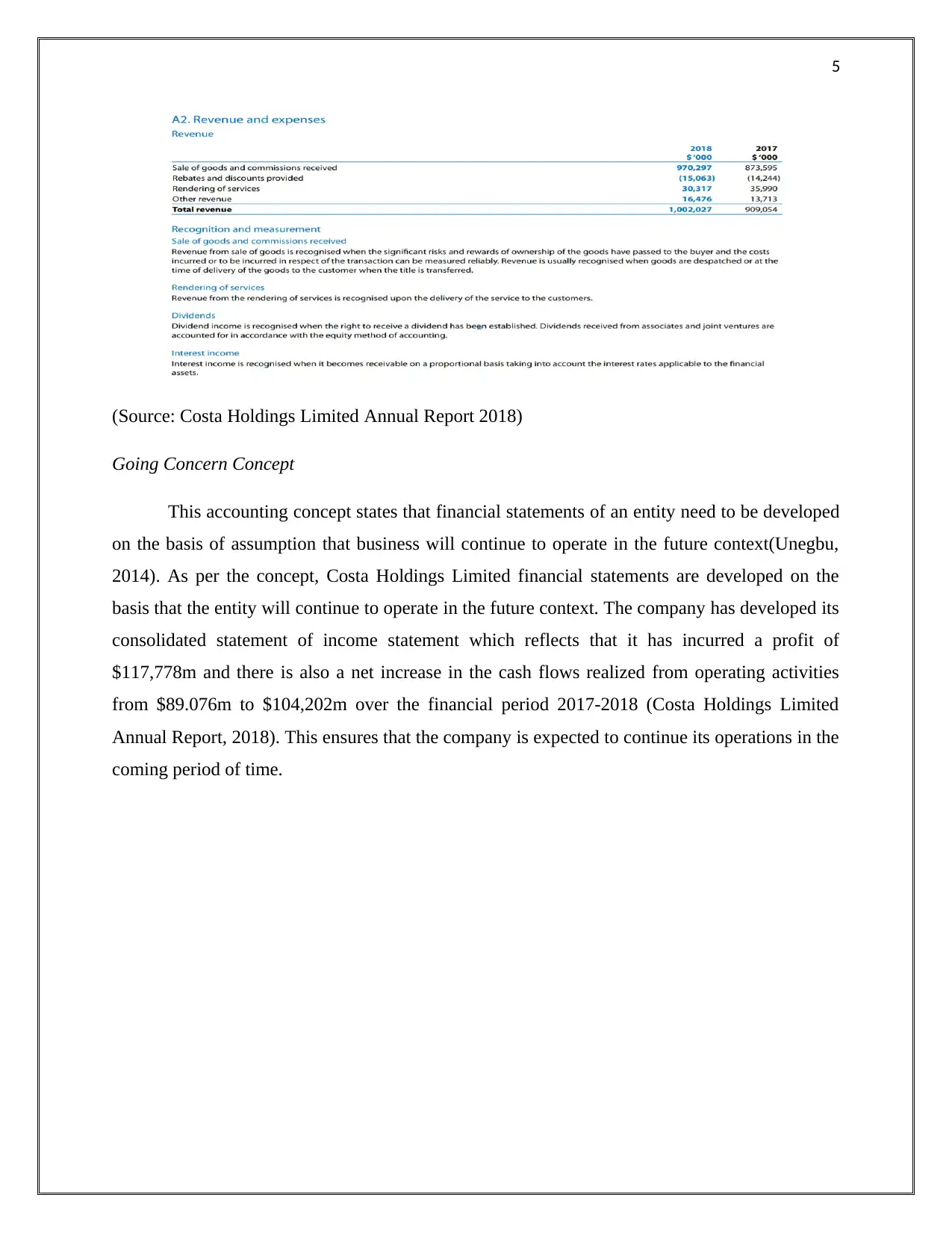

Accrual Concept

As per this accounting concept, revenue and expenses need to be recognized by an entity

at a specific period of time such as within a month or on annual basis. The concept has stated that

a business entity need to record its revenue and expenses within a respective accounting period

irrespective of whether they have been received in cash or not (Kiabel and Nwanyanwu, 2014).

As such, Costa Holdings Limited recognizes revenue when it has been realized while expenses

are recognized on the consumption of an asset. The recording of revenue by the company as per

the concept can be depicted as follows:

sales that are reflected within the income statement while accounts receivable is reflected as

assets within the balance sheet.

Money Measurement Concept

The accounting concept has stated that business entities need to record everything in

monetary terms. As per the concept, Costa Holdings Limited has recorded its various financial

transactions presented within the financial statements in the monetary terms as depicted below:

(Source: Costa Holdings Limited Annual Report 2018)

Accrual Concept

As per this accounting concept, revenue and expenses need to be recognized by an entity

at a specific period of time such as within a month or on annual basis. The concept has stated that

a business entity need to record its revenue and expenses within a respective accounting period

irrespective of whether they have been received in cash or not (Kiabel and Nwanyanwu, 2014).

As such, Costa Holdings Limited recognizes revenue when it has been realized while expenses

are recognized on the consumption of an asset. The recording of revenue by the company as per

the concept can be depicted as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

(Source: Costa Holdings Limited Annual Report 2018)

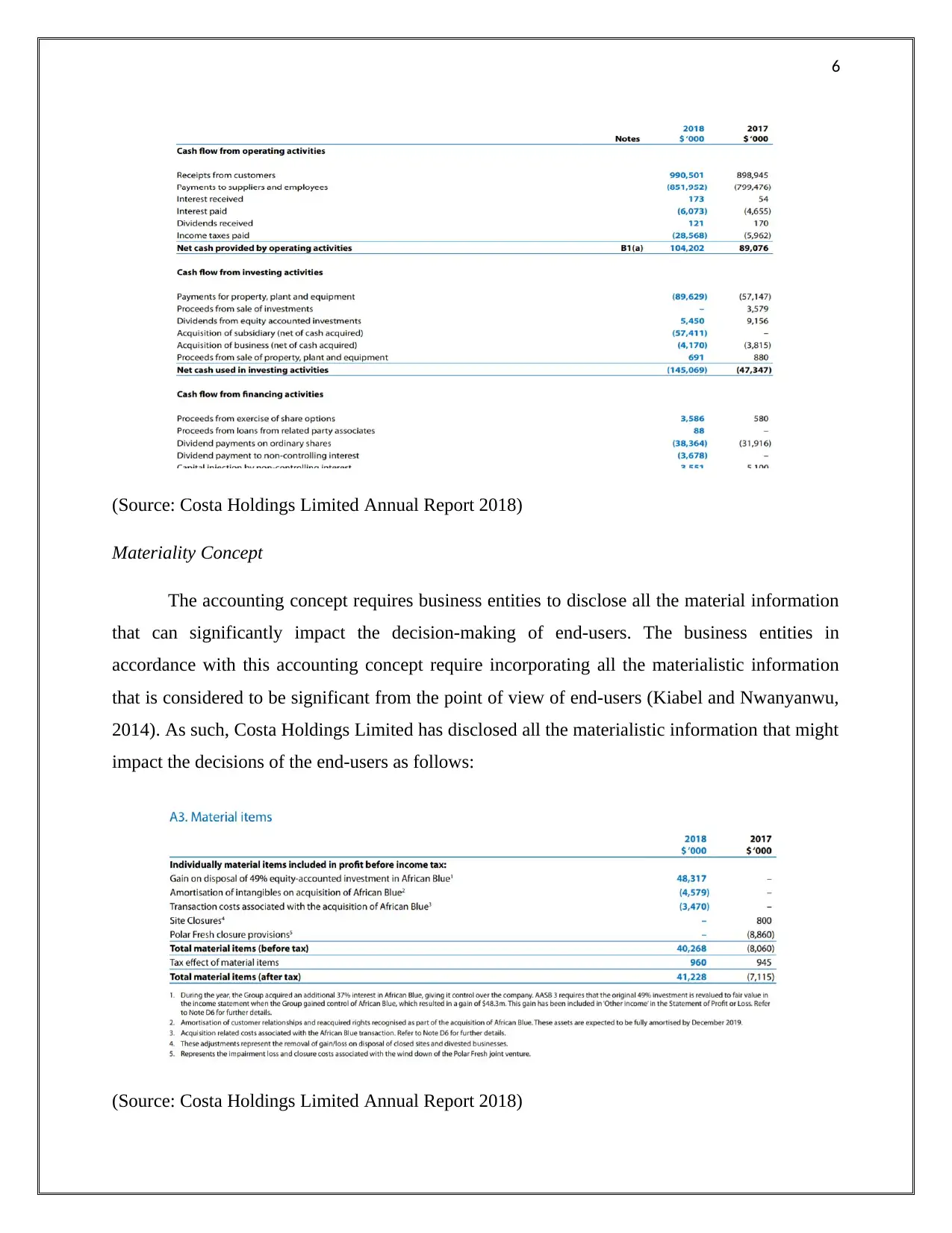

Going Concern Concept

This accounting concept states that financial statements of an entity need to be developed

on the basis of assumption that business will continue to operate in the future context(Unegbu,

2014). As per the concept, Costa Holdings Limited financial statements are developed on the

basis that the entity will continue to operate in the future context. The company has developed its

consolidated statement of income statement which reflects that it has incurred a profit of

$117,778m and there is also a net increase in the cash flows realized from operating activities

from $89.076m to $104,202m over the financial period 2017-2018 (Costa Holdings Limited

Annual Report, 2018). This ensures that the company is expected to continue its operations in the

coming period of time.

(Source: Costa Holdings Limited Annual Report 2018)

Going Concern Concept

This accounting concept states that financial statements of an entity need to be developed

on the basis of assumption that business will continue to operate in the future context(Unegbu,

2014). As per the concept, Costa Holdings Limited financial statements are developed on the

basis that the entity will continue to operate in the future context. The company has developed its

consolidated statement of income statement which reflects that it has incurred a profit of

$117,778m and there is also a net increase in the cash flows realized from operating activities

from $89.076m to $104,202m over the financial period 2017-2018 (Costa Holdings Limited

Annual Report, 2018). This ensures that the company is expected to continue its operations in the

coming period of time.

6

(Source: Costa Holdings Limited Annual Report 2018)

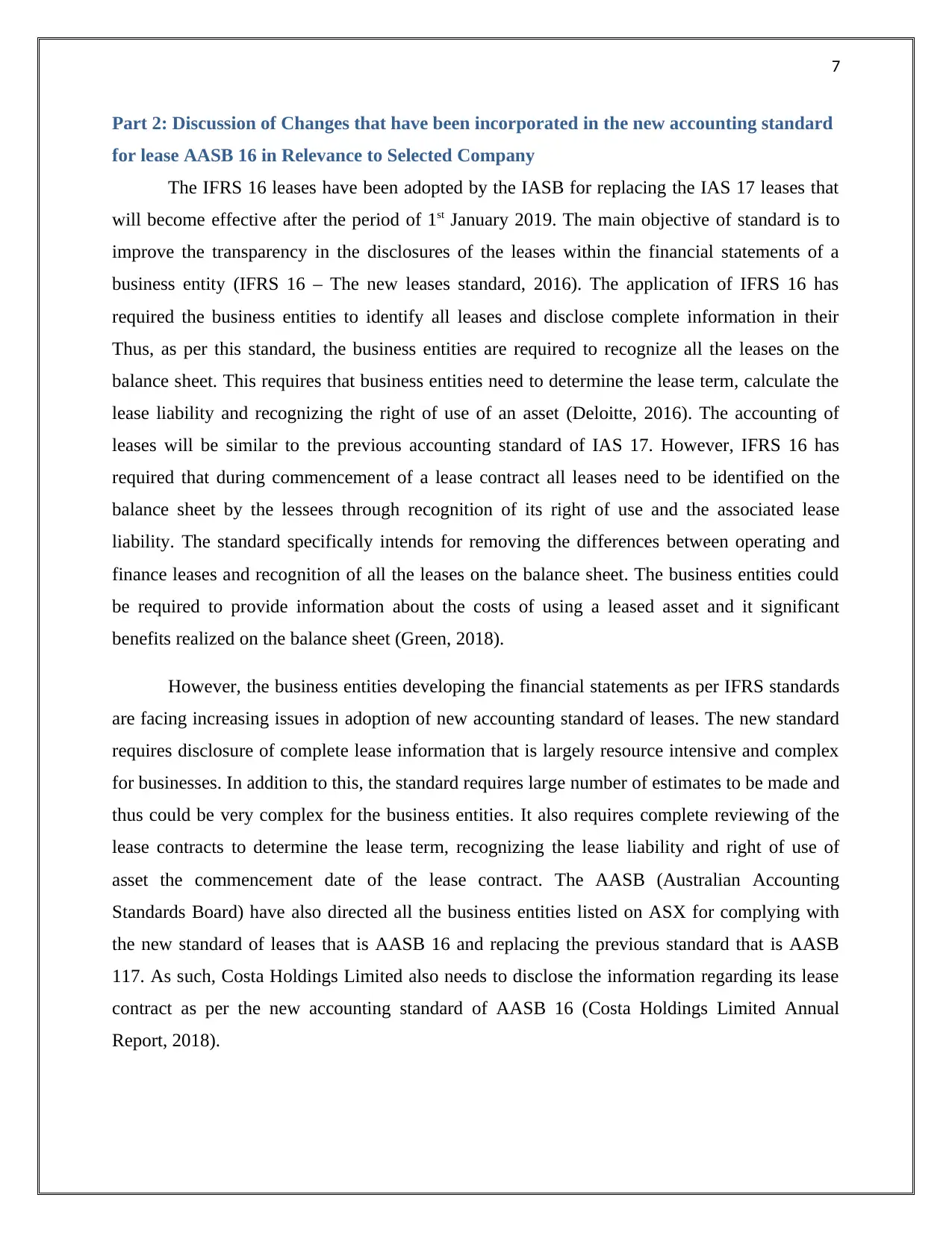

Materiality Concept

The accounting concept requires business entities to disclose all the material information

that can significantly impact the decision-making of end-users. The business entities in

accordance with this accounting concept require incorporating all the materialistic information

that is considered to be significant from the point of view of end-users (Kiabel and Nwanyanwu,

2014). As such, Costa Holdings Limited has disclosed all the materialistic information that might

impact the decisions of the end-users as follows:

(Source: Costa Holdings Limited Annual Report 2018)

(Source: Costa Holdings Limited Annual Report 2018)

Materiality Concept

The accounting concept requires business entities to disclose all the material information

that can significantly impact the decision-making of end-users. The business entities in

accordance with this accounting concept require incorporating all the materialistic information

that is considered to be significant from the point of view of end-users (Kiabel and Nwanyanwu,

2014). As such, Costa Holdings Limited has disclosed all the materialistic information that might

impact the decisions of the end-users as follows:

(Source: Costa Holdings Limited Annual Report 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Part 2: Discussion of Changes that have been incorporated in the new accounting standard

for lease AASB 16 in Relevance to Selected Company

The IFRS 16 leases have been adopted by the IASB for replacing the IAS 17 leases that

will become effective after the period of 1st January 2019. The main objective of standard is to

improve the transparency in the disclosures of the leases within the financial statements of a

business entity (IFRS 16 – The new leases standard, 2016). The application of IFRS 16 has

required the business entities to identify all leases and disclose complete information in their

Thus, as per this standard, the business entities are required to recognize all the leases on the

balance sheet. This requires that business entities need to determine the lease term, calculate the

lease liability and recognizing the right of use of an asset (Deloitte, 2016). The accounting of

leases will be similar to the previous accounting standard of IAS 17. However, IFRS 16 has

required that during commencement of a lease contract all leases need to be identified on the

balance sheet by the lessees through recognition of its right of use and the associated lease

liability. The standard specifically intends for removing the differences between operating and

finance leases and recognition of all the leases on the balance sheet. The business entities could

be required to provide information about the costs of using a leased asset and it significant

benefits realized on the balance sheet (Green, 2018).

However, the business entities developing the financial statements as per IFRS standards

are facing increasing issues in adoption of new accounting standard of leases. The new standard

requires disclosure of complete lease information that is largely resource intensive and complex

for businesses. In addition to this, the standard requires large number of estimates to be made and

thus could be very complex for the business entities. It also requires complete reviewing of the

lease contracts to determine the lease term, recognizing the lease liability and right of use of

asset the commencement date of the lease contract. The AASB (Australian Accounting

Standards Board) have also directed all the business entities listed on ASX for complying with

the new standard of leases that is AASB 16 and replacing the previous standard that is AASB

117. As such, Costa Holdings Limited also needs to disclose the information regarding its lease

contract as per the new accounting standard of AASB 16 (Costa Holdings Limited Annual

Report, 2018).

Part 2: Discussion of Changes that have been incorporated in the new accounting standard

for lease AASB 16 in Relevance to Selected Company

The IFRS 16 leases have been adopted by the IASB for replacing the IAS 17 leases that

will become effective after the period of 1st January 2019. The main objective of standard is to

improve the transparency in the disclosures of the leases within the financial statements of a

business entity (IFRS 16 – The new leases standard, 2016). The application of IFRS 16 has

required the business entities to identify all leases and disclose complete information in their

Thus, as per this standard, the business entities are required to recognize all the leases on the

balance sheet. This requires that business entities need to determine the lease term, calculate the

lease liability and recognizing the right of use of an asset (Deloitte, 2016). The accounting of

leases will be similar to the previous accounting standard of IAS 17. However, IFRS 16 has

required that during commencement of a lease contract all leases need to be identified on the

balance sheet by the lessees through recognition of its right of use and the associated lease

liability. The standard specifically intends for removing the differences between operating and

finance leases and recognition of all the leases on the balance sheet. The business entities could

be required to provide information about the costs of using a leased asset and it significant

benefits realized on the balance sheet (Green, 2018).

However, the business entities developing the financial statements as per IFRS standards

are facing increasing issues in adoption of new accounting standard of leases. The new standard

requires disclosure of complete lease information that is largely resource intensive and complex

for businesses. In addition to this, the standard requires large number of estimates to be made and

thus could be very complex for the business entities. It also requires complete reviewing of the

lease contracts to determine the lease term, recognizing the lease liability and right of use of

asset the commencement date of the lease contract. The AASB (Australian Accounting

Standards Board) have also directed all the business entities listed on ASX for complying with

the new standard of leases that is AASB 16 and replacing the previous standard that is AASB

117. As such, Costa Holdings Limited also needs to disclose the information regarding its lease

contract as per the new accounting standard of AASB 16 (Costa Holdings Limited Annual

Report, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

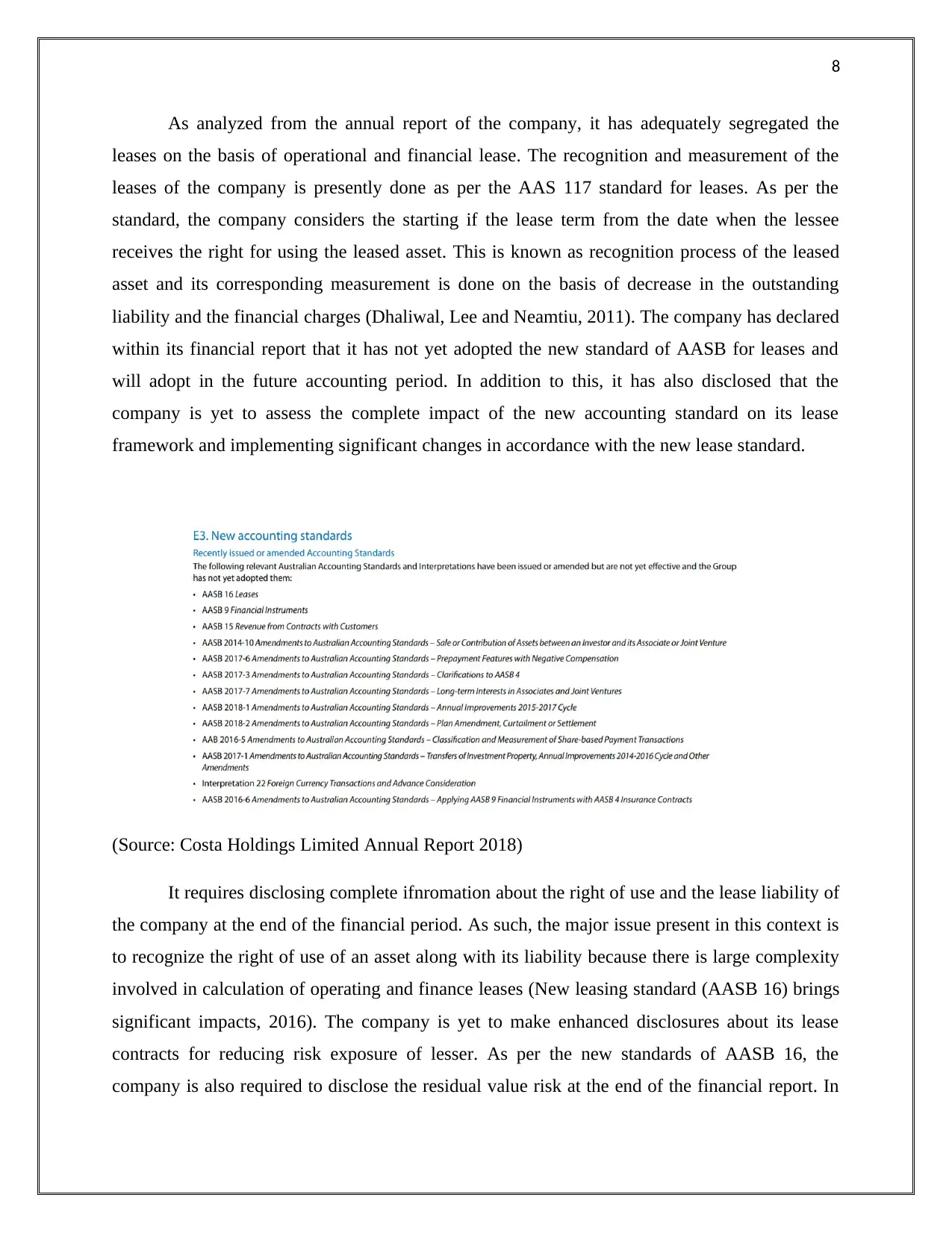

As analyzed from the annual report of the company, it has adequately segregated the

leases on the basis of operational and financial lease. The recognition and measurement of the

leases of the company is presently done as per the AAS 117 standard for leases. As per the

standard, the company considers the starting if the lease term from the date when the lessee

receives the right for using the leased asset. This is known as recognition process of the leased

asset and its corresponding measurement is done on the basis of decrease in the outstanding

liability and the financial charges (Dhaliwal, Lee and Neamtiu, 2011). The company has declared

within its financial report that it has not yet adopted the new standard of AASB for leases and

will adopt in the future accounting period. In addition to this, it has also disclosed that the

company is yet to assess the complete impact of the new accounting standard on its lease

framework and implementing significant changes in accordance with the new lease standard.

(Source: Costa Holdings Limited Annual Report 2018)

It requires disclosing complete ifnromation about the right of use and the lease liability of

the company at the end of the financial period. As such, the major issue present in this context is

to recognize the right of use of an asset along with its liability because there is large complexity

involved in calculation of operating and finance leases (New leasing standard (AASB 16) brings

significant impacts, 2016). The company is yet to make enhanced disclosures about its lease

contracts for reducing risk exposure of lesser. As per the new standards of AASB 16, the

company is also required to disclose the residual value risk at the end of the financial report. In

As analyzed from the annual report of the company, it has adequately segregated the

leases on the basis of operational and financial lease. The recognition and measurement of the

leases of the company is presently done as per the AAS 117 standard for leases. As per the

standard, the company considers the starting if the lease term from the date when the lessee

receives the right for using the leased asset. This is known as recognition process of the leased

asset and its corresponding measurement is done on the basis of decrease in the outstanding

liability and the financial charges (Dhaliwal, Lee and Neamtiu, 2011). The company has declared

within its financial report that it has not yet adopted the new standard of AASB for leases and

will adopt in the future accounting period. In addition to this, it has also disclosed that the

company is yet to assess the complete impact of the new accounting standard on its lease

framework and implementing significant changes in accordance with the new lease standard.

(Source: Costa Holdings Limited Annual Report 2018)

It requires disclosing complete ifnromation about the right of use and the lease liability of

the company at the end of the financial period. As such, the major issue present in this context is

to recognize the right of use of an asset along with its liability because there is large complexity

involved in calculation of operating and finance leases (New leasing standard (AASB 16) brings

significant impacts, 2016). The company is yet to make enhanced disclosures about its lease

contracts for reducing risk exposure of lesser. As per the new standards of AASB 16, the

company is also required to disclose the residual value risk at the end of the financial report. In

9

addition to this, the company also needs to integrate the information regarding accounting of

leaseback as per the new accounting standard of AASB 16. Thus, the company has to face larger

issues while complying with the new standard requirements and this can significantly alter the

reporting process of leases of the company. In addition to this, the major issue that the company

is facing to comply effectively with the new accounting standard of AASB 16 is that it would

result in implementing significant changes in the profit of the expenses. It would not adopt the

use of straight line method (Grossman and Grossman, 2010). There is also requirement of

adopting changes in the development and presentation of information regarding the assets

position within the balance sheet. This is because right of use of an asset should be segregated

within the non-current assets whereas lease liability need to be segregated between the current

and non-current liabilities on the balance sheet. Further, it has been stated within the annual

report of the company that it has undertaken a project for ensuring to disclose high quality of

financial information as per the new lease standard of AASB 16(Costa Holdings Limited Annual

Report, 2018). The project involves all the significant members from different departments such

as finance, IT and Chief Financial Officer for developing the accounting policy, assessing the

impact of the new standards and effectively implementing the new standard (Jose and

Constancio, 2018).

Part 3: Key Disclosures made by Costa Holding Limited on accounting for leases (AASB 16

As per the information mentioned in annual report 2018, Costa Holding Limited has

adopted IFRS 16/AASB 16 with effect from 1 January, 2019. Transition effect of

implementation of AASB 16 will be first seen in annual report of year 2019 for the year ending

29 December, 2019. It has been decided to make use of half yearly report to year 2019, to

discuss the key disclosures made by Costa Holding Limited. There has been no information on

transitional provisions and impact of change from AASB 117 to AASB 16 in annual report 2018

and half yearly report 2019 (Annual Report, 2018).

AASB 16 has mandated to reflect all the leases using single on-balance sheet accounting

model by Lessees. To give effect to change in accounting procedure of AASB 16, Costa Holding

Limited as a lessee has recognised lease liabilities in balance sheet. On the other hand, lease

accounting related to lessor remains same as it was in case of AASB 117. Therefore, there was

no change in lease accounting performed on part of lessor. It has been observed from the annual

addition to this, the company also needs to integrate the information regarding accounting of

leaseback as per the new accounting standard of AASB 16. Thus, the company has to face larger

issues while complying with the new standard requirements and this can significantly alter the

reporting process of leases of the company. In addition to this, the major issue that the company

is facing to comply effectively with the new accounting standard of AASB 16 is that it would

result in implementing significant changes in the profit of the expenses. It would not adopt the

use of straight line method (Grossman and Grossman, 2010). There is also requirement of

adopting changes in the development and presentation of information regarding the assets

position within the balance sheet. This is because right of use of an asset should be segregated

within the non-current assets whereas lease liability need to be segregated between the current

and non-current liabilities on the balance sheet. Further, it has been stated within the annual

report of the company that it has undertaken a project for ensuring to disclose high quality of

financial information as per the new lease standard of AASB 16(Costa Holdings Limited Annual

Report, 2018). The project involves all the significant members from different departments such

as finance, IT and Chief Financial Officer for developing the accounting policy, assessing the

impact of the new standards and effectively implementing the new standard (Jose and

Constancio, 2018).

Part 3: Key Disclosures made by Costa Holding Limited on accounting for leases (AASB 16

As per the information mentioned in annual report 2018, Costa Holding Limited has

adopted IFRS 16/AASB 16 with effect from 1 January, 2019. Transition effect of

implementation of AASB 16 will be first seen in annual report of year 2019 for the year ending

29 December, 2019. It has been decided to make use of half yearly report to year 2019, to

discuss the key disclosures made by Costa Holding Limited. There has been no information on

transitional provisions and impact of change from AASB 117 to AASB 16 in annual report 2018

and half yearly report 2019 (Annual Report, 2018).

AASB 16 has mandated to reflect all the leases using single on-balance sheet accounting

model by Lessees. To give effect to change in accounting procedure of AASB 16, Costa Holding

Limited as a lessee has recognised lease liabilities in balance sheet. On the other hand, lease

accounting related to lessor remains same as it was in case of AASB 117. Therefore, there was

no change in lease accounting performed on part of lessor. It has been observed from the annual

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

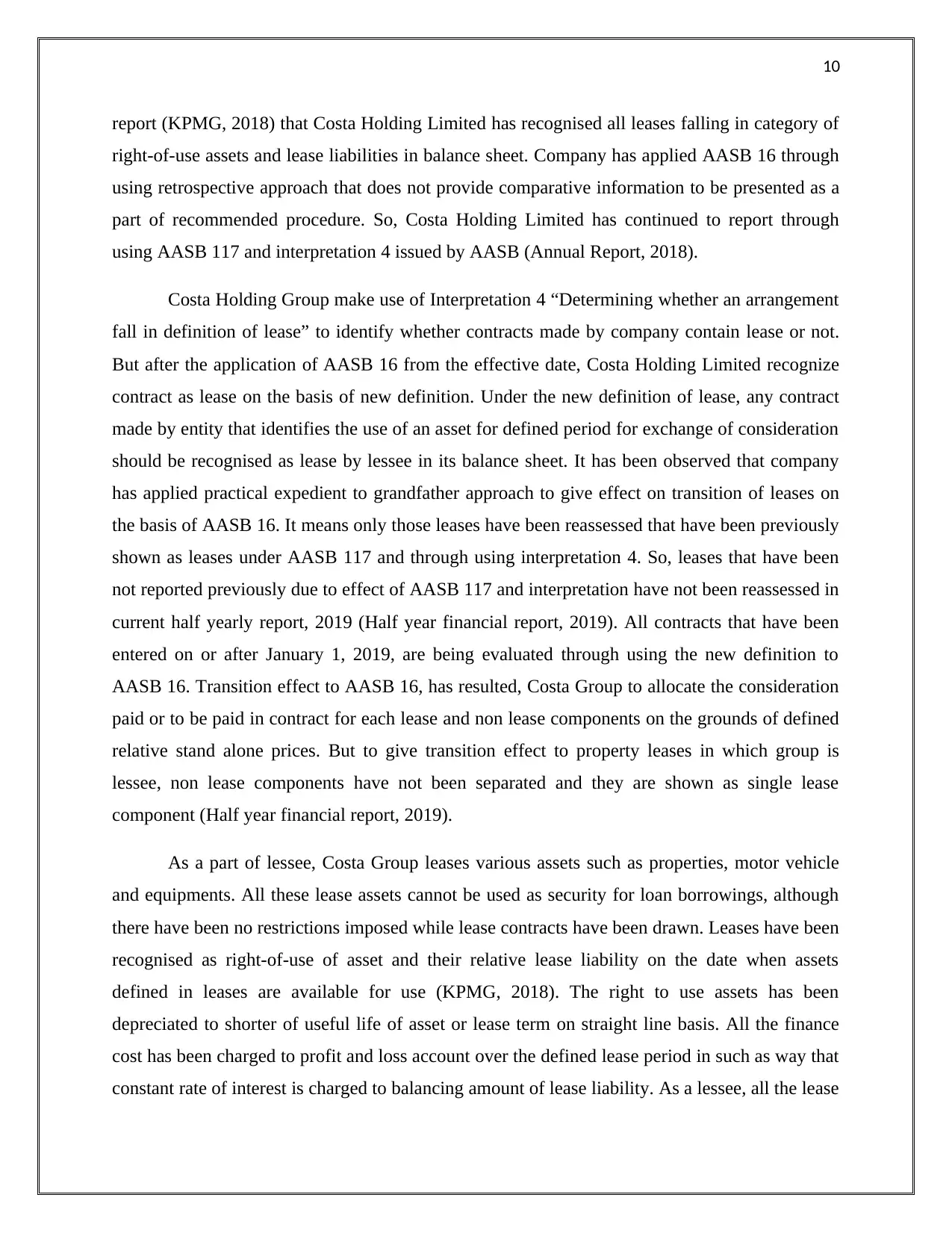

report (KPMG, 2018) that Costa Holding Limited has recognised all leases falling in category of

right-of-use assets and lease liabilities in balance sheet. Company has applied AASB 16 through

using retrospective approach that does not provide comparative information to be presented as a

part of recommended procedure. So, Costa Holding Limited has continued to report through

using AASB 117 and interpretation 4 issued by AASB (Annual Report, 2018).

Costa Holding Group make use of Interpretation 4 “Determining whether an arrangement

fall in definition of lease” to identify whether contracts made by company contain lease or not.

But after the application of AASB 16 from the effective date, Costa Holding Limited recognize

contract as lease on the basis of new definition. Under the new definition of lease, any contract

made by entity that identifies the use of an asset for defined period for exchange of consideration

should be recognised as lease by lessee in its balance sheet. It has been observed that company

has applied practical expedient to grandfather approach to give effect on transition of leases on

the basis of AASB 16. It means only those leases have been reassessed that have been previously

shown as leases under AASB 117 and through using interpretation 4. So, leases that have been

not reported previously due to effect of AASB 117 and interpretation have not been reassessed in

current half yearly report, 2019 (Half year financial report, 2019). All contracts that have been

entered on or after January 1, 2019, are being evaluated through using the new definition to

AASB 16. Transition effect to AASB 16, has resulted, Costa Group to allocate the consideration

paid or to be paid in contract for each lease and non lease components on the grounds of defined

relative stand alone prices. But to give transition effect to property leases in which group is

lessee, non lease components have not been separated and they are shown as single lease

component (Half year financial report, 2019).

As a part of lessee, Costa Group leases various assets such as properties, motor vehicle

and equipments. All these lease assets cannot be used as security for loan borrowings, although

there have been no restrictions imposed while lease contracts have been drawn. Leases have been

recognised as right-of-use of asset and their relative lease liability on the date when assets

defined in leases are available for use (KPMG, 2018). The right to use assets has been

depreciated to shorter of useful life of asset or lease term on straight line basis. All the finance

cost has been charged to profit and loss account over the defined lease period in such as way that

constant rate of interest is charged to balancing amount of lease liability. As a lessee, all the lease

report (KPMG, 2018) that Costa Holding Limited has recognised all leases falling in category of

right-of-use assets and lease liabilities in balance sheet. Company has applied AASB 16 through

using retrospective approach that does not provide comparative information to be presented as a

part of recommended procedure. So, Costa Holding Limited has continued to report through

using AASB 117 and interpretation 4 issued by AASB (Annual Report, 2018).

Costa Holding Group make use of Interpretation 4 “Determining whether an arrangement

fall in definition of lease” to identify whether contracts made by company contain lease or not.

But after the application of AASB 16 from the effective date, Costa Holding Limited recognize

contract as lease on the basis of new definition. Under the new definition of lease, any contract

made by entity that identifies the use of an asset for defined period for exchange of consideration

should be recognised as lease by lessee in its balance sheet. It has been observed that company

has applied practical expedient to grandfather approach to give effect on transition of leases on

the basis of AASB 16. It means only those leases have been reassessed that have been previously

shown as leases under AASB 117 and through using interpretation 4. So, leases that have been

not reported previously due to effect of AASB 117 and interpretation have not been reassessed in

current half yearly report, 2019 (Half year financial report, 2019). All contracts that have been

entered on or after January 1, 2019, are being evaluated through using the new definition to

AASB 16. Transition effect to AASB 16, has resulted, Costa Group to allocate the consideration

paid or to be paid in contract for each lease and non lease components on the grounds of defined

relative stand alone prices. But to give transition effect to property leases in which group is

lessee, non lease components have not been separated and they are shown as single lease

component (Half year financial report, 2019).

As a part of lessee, Costa Group leases various assets such as properties, motor vehicle

and equipments. All these lease assets cannot be used as security for loan borrowings, although

there have been no restrictions imposed while lease contracts have been drawn. Leases have been

recognised as right-of-use of asset and their relative lease liability on the date when assets

defined in leases are available for use (KPMG, 2018). The right to use assets has been

depreciated to shorter of useful life of asset or lease term on straight line basis. All the finance

cost has been charged to profit and loss account over the defined lease period in such as way that

constant rate of interest is charged to balancing amount of lease liability. As a lessee, all the lease

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

payments are being discounted through using interest rate defined in lease in case such rate is

provided otherwise incremental borrowing rate can be used (Half year financial report, 2019).

Costa Holding Limited measures right-of-use assets on cost basis and it comprises of

following values:

Lease liability measured initially

Any lease payment paid before the contract commencement date

Lease incentives received should be subtracted

Direct cost paid initially

All restoration cost provided in lease contract (Half year financial report, 2019)

Following is reconciliation statement providing effect of change from operating lease

commitments to lease liabilities as the part of transition effect of lease liabilities:

(Source: Half year financial report, 2019)

Following information has been disclosed in balance sheet and profit & loss statement to

provide for the new accounting standard AASB 16:

payments are being discounted through using interest rate defined in lease in case such rate is

provided otherwise incremental borrowing rate can be used (Half year financial report, 2019).

Costa Holding Limited measures right-of-use assets on cost basis and it comprises of

following values:

Lease liability measured initially

Any lease payment paid before the contract commencement date

Lease incentives received should be subtracted

Direct cost paid initially

All restoration cost provided in lease contract (Half year financial report, 2019)

Following is reconciliation statement providing effect of change from operating lease

commitments to lease liabilities as the part of transition effect of lease liabilities:

(Source: Half year financial report, 2019)

Following information has been disclosed in balance sheet and profit & loss statement to

provide for the new accounting standard AASB 16:

12

(Source: Half year financial report, 2019)

(Source: Half year financial report, 2019)

Conclusion

The overall analysis held in the report has inferred that business entities need to adopt the

use of significant accounting concepts provided by the IFRS to develop and present high quality

information within their financial reports. The selected company, that is, Costa Holdings Limited

has adopted the use of all relevant accounting concepts to adequately prepare and disclose the

significant financial information. Also, it has been identified from analyzing the information

provided within the annual report of the selected company that it has not yet adopted the new

accounting standard of leases that is AASB 16. The company is yet to make changes in its

accounting framework as per the standard but the major issues present before the company in

(Source: Half year financial report, 2019)

(Source: Half year financial report, 2019)

Conclusion

The overall analysis held in the report has inferred that business entities need to adopt the

use of significant accounting concepts provided by the IFRS to develop and present high quality

information within their financial reports. The selected company, that is, Costa Holdings Limited

has adopted the use of all relevant accounting concepts to adequately prepare and disclose the

significant financial information. Also, it has been identified from analyzing the information

provided within the annual report of the selected company that it has not yet adopted the new

accounting standard of leases that is AASB 16. The company is yet to make changes in its

accounting framework as per the standard but the major issues present before the company in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.