Advanced Corporate Accounting: Tesco's Financial Reporting Analysis

VerifiedAdded on 2023/01/05

|10

|2808

|73

Report

AI Summary

This report provides an in-depth analysis of Tesco's corporate accounting policies, focusing on impairment testing, financial instruments, and post-employment benefits. It begins with an introduction to Tesco's operations and regulatory framework, highlighting its investments in joint ventures and associates. The report then examines impairment testing practices, adhering to IAS 36, including the use of cash-generating units and sensitivity analysis. It discusses financial instruments and risk management, including derivative financial instruments, foreign exchange risk, and interest rate risks, referencing IFRS 9. Finally, the report analyzes Tesco's post-employment benefit policies, detailing the calculation of obligations, financial assumptions, and sensitivity analyses. The conclusion summarizes the key findings and emphasizes the company's adherence to accounting standards.

1

Advanced corporate accounting

Advanced corporate accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Table of Contents

Introduction......................................................................................................................................3

Analyzation and discussion of accounting policies.........................................................................3

a) Policies for impairment testing................................................................................................3

b) Financial instruments and risk.................................................................................................5

c) Post-employment benefits.......................................................................................................7

Conclusion.......................................................................................................................................8

References......................................................................................................................................10

Table of Contents

Introduction......................................................................................................................................3

Analyzation and discussion of accounting policies.........................................................................3

a) Policies for impairment testing................................................................................................3

b) Financial instruments and risk.................................................................................................5

c) Post-employment benefits.......................................................................................................7

Conclusion.......................................................................................................................................8

References......................................................................................................................................10

3

Introduction

In the world, there are various grocery retailers and out of them, Tesco is the largest retailer

which is established in the British market. It is the company which is carrying out its operations

in various parts such as the USA, Asia, and Europe. The company was established in 1919 and is

dealing in the groceries. The company has various associates and joint ventures and it is making

the investment in them. There is a total of £689 m which is invested in joint ventures and

associates by the company. There are various legal and regulatory requirements and all of them

have been taken into consideration by the company. The regulatory framework is established in

which various standards are provided and they will be understood in the report so that proper

reporting is made. The main aspects of the company in relation to the impairment and various

financial instruments including the financial risk will be discussed in the report. the polices in

respect of the post-employment benefits will also be identified and at last, the disclosures about

the quality will be made in which conceptual framework will be taken into consideration.

Analyzation and discussion of accounting policies

a) Policies for impairment testing

Impairment testing is performed by the business to ensure that they comply with all the

requirements of the accounting standards. This is also performed by Tesco and in that various

assets for which is the test is done have been identified and they include property, plant, and

equipment, goodwill, non-financial assets. There are several rules which are prescribed in IAS 36

in this respect and are to be considered (Coste, Tudor and Pali-Pista, 2014). Tesco is also

involving various cash generating units and in that each store is considered as separate CGU.

The value in use is taken as the basis for the impairment review and that is done with the help of

directors assumptions and cash flow projections on the estimates. The recoverable amount and

value in use of the assets are tested on the balance sheet date and by that, the decision for

impairment is taken (Avallone and Quagli, 2015). In that review, the reversal of impairment is

ascertained and it is amounting to £187m which is because of the changes in the discount rates

and fair value modifications. The discount rate has declined and by that there is an increase in the

present value of asset and so the reversal for the impairment has been made. It is necessary that

Introduction

In the world, there are various grocery retailers and out of them, Tesco is the largest retailer

which is established in the British market. It is the company which is carrying out its operations

in various parts such as the USA, Asia, and Europe. The company was established in 1919 and is

dealing in the groceries. The company has various associates and joint ventures and it is making

the investment in them. There is a total of £689 m which is invested in joint ventures and

associates by the company. There are various legal and regulatory requirements and all of them

have been taken into consideration by the company. The regulatory framework is established in

which various standards are provided and they will be understood in the report so that proper

reporting is made. The main aspects of the company in relation to the impairment and various

financial instruments including the financial risk will be discussed in the report. the polices in

respect of the post-employment benefits will also be identified and at last, the disclosures about

the quality will be made in which conceptual framework will be taken into consideration.

Analyzation and discussion of accounting policies

a) Policies for impairment testing

Impairment testing is performed by the business to ensure that they comply with all the

requirements of the accounting standards. This is also performed by Tesco and in that various

assets for which is the test is done have been identified and they include property, plant, and

equipment, goodwill, non-financial assets. There are several rules which are prescribed in IAS 36

in this respect and are to be considered (Coste, Tudor and Pali-Pista, 2014). Tesco is also

involving various cash generating units and in that each store is considered as separate CGU.

The value in use is taken as the basis for the impairment review and that is done with the help of

directors assumptions and cash flow projections on the estimates. The recoverable amount and

value in use of the assets are tested on the balance sheet date and by that, the decision for

impairment is taken (Avallone and Quagli, 2015). In that review, the reversal of impairment is

ascertained and it is amounting to £187m which is because of the changes in the discount rates

and fair value modifications. The discount rate has declined and by that there is an increase in the

present value of asset and so the reversal for the impairment has been made. It is necessary that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

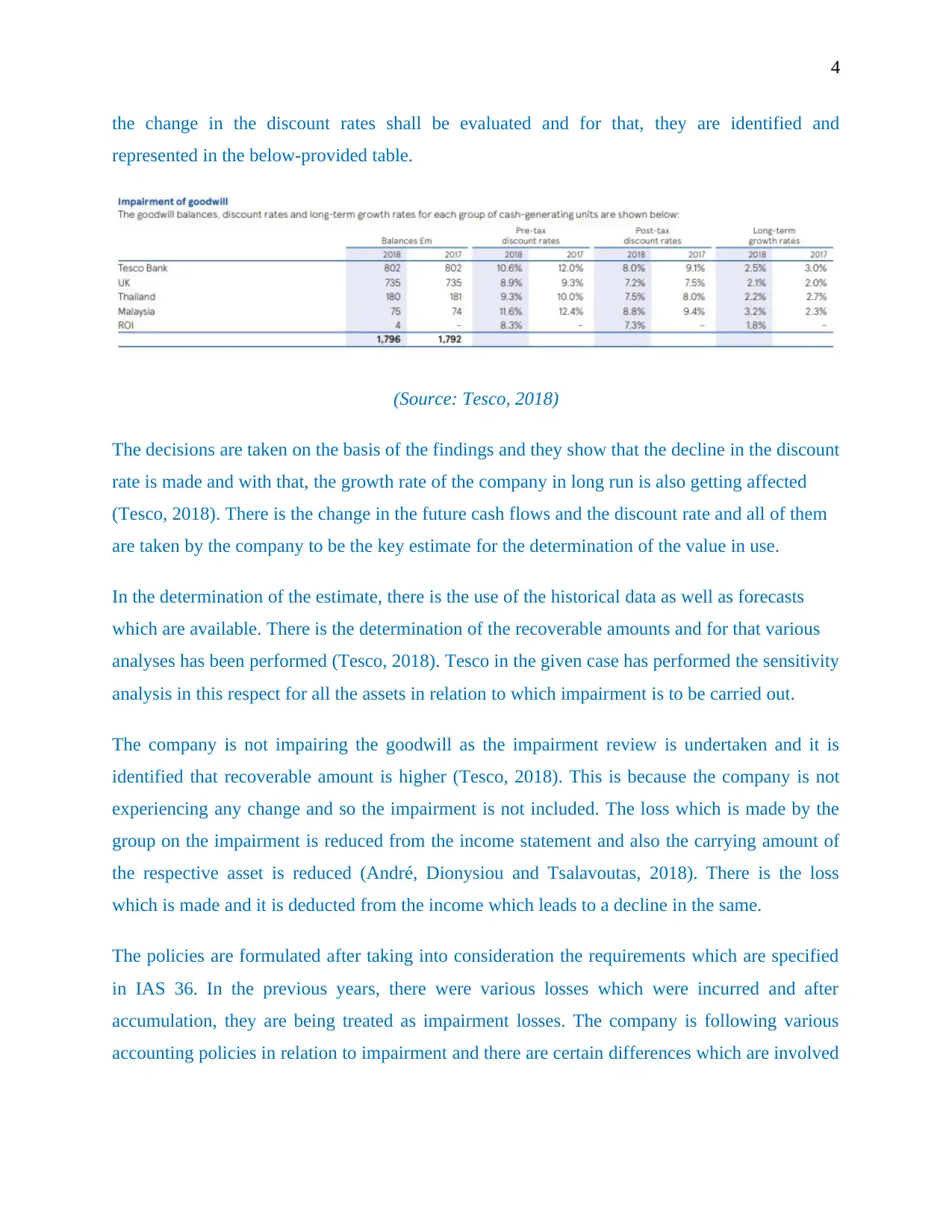

the change in the discount rates shall be evaluated and for that, they are identified and

represented in the below-provided table.

(Source: Tesco, 2018)

The decisions are taken on the basis of the findings and they show that the decline in the discount

rate is made and with that, the growth rate of the company in long run is also getting affected

(Tesco, 2018). There is the change in the future cash flows and the discount rate and all of them

are taken by the company to be the key estimate for the determination of the value in use.

In the determination of the estimate, there is the use of the historical data as well as forecasts

which are available. There is the determination of the recoverable amounts and for that various

analyses has been performed (Tesco, 2018). Tesco in the given case has performed the sensitivity

analysis in this respect for all the assets in relation to which impairment is to be carried out.

The company is not impairing the goodwill as the impairment review is undertaken and it is

identified that recoverable amount is higher (Tesco, 2018). This is because the company is not

experiencing any change and so the impairment is not included. The loss which is made by the

group on the impairment is reduced from the income statement and also the carrying amount of

the respective asset is reduced (André, Dionysiou and Tsalavoutas, 2018). There is the loss

which is made and it is deducted from the income which leads to a decline in the same.

The policies are formulated after taking into consideration the requirements which are specified

in IAS 36. In the previous years, there were various losses which were incurred and after

accumulation, they are being treated as impairment losses. The company is following various

accounting policies in relation to impairment and there are certain differences which are involved

the change in the discount rates shall be evaluated and for that, they are identified and

represented in the below-provided table.

(Source: Tesco, 2018)

The decisions are taken on the basis of the findings and they show that the decline in the discount

rate is made and with that, the growth rate of the company in long run is also getting affected

(Tesco, 2018). There is the change in the future cash flows and the discount rate and all of them

are taken by the company to be the key estimate for the determination of the value in use.

In the determination of the estimate, there is the use of the historical data as well as forecasts

which are available. There is the determination of the recoverable amounts and for that various

analyses has been performed (Tesco, 2018). Tesco in the given case has performed the sensitivity

analysis in this respect for all the assets in relation to which impairment is to be carried out.

The company is not impairing the goodwill as the impairment review is undertaken and it is

identified that recoverable amount is higher (Tesco, 2018). This is because the company is not

experiencing any change and so the impairment is not included. The loss which is made by the

group on the impairment is reduced from the income statement and also the carrying amount of

the respective asset is reduced (André, Dionysiou and Tsalavoutas, 2018). There is the loss

which is made and it is deducted from the income which leads to a decline in the same.

The policies are formulated after taking into consideration the requirements which are specified

in IAS 36. In the previous years, there were various losses which were incurred and after

accumulation, they are being treated as impairment losses. The company is following various

accounting policies in relation to impairment and there are certain differences which are involved

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

in them. Risk is the important factor and it is involved and shall be taken into consideration so

that required steps are used for effective dealing.

b) Financial instruments and risk

In the financial statements, there is the disclosure of the financial instruments which is made and

in that all of the types which are present are taken into account. In the given case Tesco has

included the derivative financial instruments in the making of financial statements which

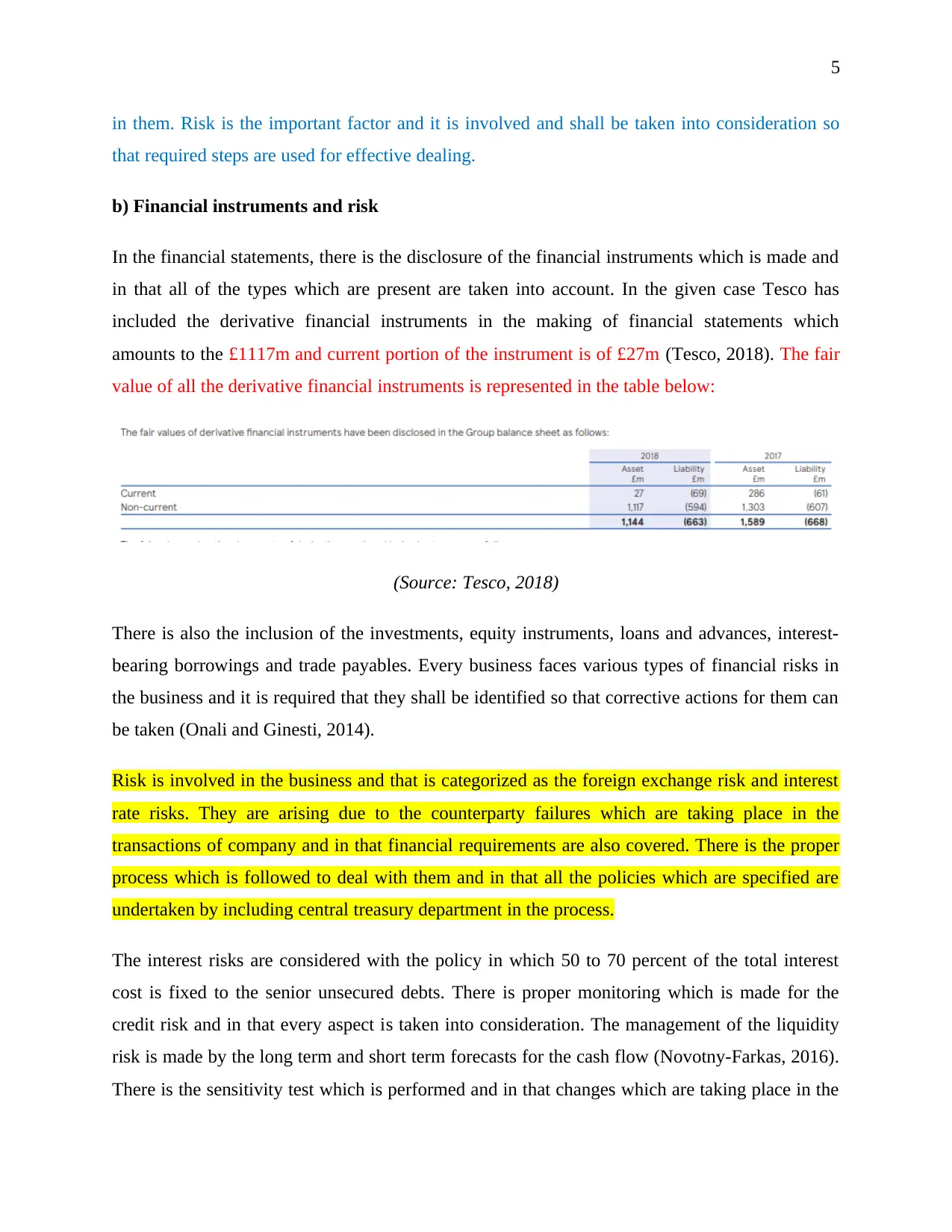

amounts to the £1117m and current portion of the instrument is of £27m (Tesco, 2018). The fair

value of all the derivative financial instruments is represented in the table below:

(Source: Tesco, 2018)

There is also the inclusion of the investments, equity instruments, loans and advances, interest-

bearing borrowings and trade payables. Every business faces various types of financial risks in

the business and it is required that they shall be identified so that corrective actions for them can

be taken (Onali and Ginesti, 2014).

Risk is involved in the business and that is categorized as the foreign exchange risk and interest

rate risks. They are arising due to the counterparty failures which are taking place in the

transactions of company and in that financial requirements are also covered. There is the proper

process which is followed to deal with them and in that all the policies which are specified are

undertaken by including central treasury department in the process.

The interest risks are considered with the policy in which 50 to 70 percent of the total interest

cost is fixed to the senior unsecured debts. There is proper monitoring which is made for the

credit risk and in that every aspect is taken into consideration. The management of the liquidity

risk is made by the long term and short term forecasts for the cash flow (Novotny-Farkas, 2016).

There is the sensitivity test which is performed and in that changes which are taking place in the

in them. Risk is the important factor and it is involved and shall be taken into consideration so

that required steps are used for effective dealing.

b) Financial instruments and risk

In the financial statements, there is the disclosure of the financial instruments which is made and

in that all of the types which are present are taken into account. In the given case Tesco has

included the derivative financial instruments in the making of financial statements which

amounts to the £1117m and current portion of the instrument is of £27m (Tesco, 2018). The fair

value of all the derivative financial instruments is represented in the table below:

(Source: Tesco, 2018)

There is also the inclusion of the investments, equity instruments, loans and advances, interest-

bearing borrowings and trade payables. Every business faces various types of financial risks in

the business and it is required that they shall be identified so that corrective actions for them can

be taken (Onali and Ginesti, 2014).

Risk is involved in the business and that is categorized as the foreign exchange risk and interest

rate risks. They are arising due to the counterparty failures which are taking place in the

transactions of company and in that financial requirements are also covered. There is the proper

process which is followed to deal with them and in that all the policies which are specified are

undertaken by including central treasury department in the process.

The interest risks are considered with the policy in which 50 to 70 percent of the total interest

cost is fixed to the senior unsecured debts. There is proper monitoring which is made for the

credit risk and in that every aspect is taken into consideration. The management of the liquidity

risk is made by the long term and short term forecasts for the cash flow (Novotny-Farkas, 2016).

There is the sensitivity test which is performed and in that changes which are taking place in the

6

foreign exchange rates are considered as by that change in the accounts is made for the equity

and income.

All the loans and receivables are measured at amortized cost and for the measurement of

instruments that are available for sale, the FVOCI is taken into use. It has been assumed by the

company that all the receivables and loans will have to be measured under IFRS 9 at amortized

cost. The instruments for which the fair value is not available will be valued with the help of the

discounted future cash flows which have been projected (Tesco, 2018).

The provision has been made for the impairment of the financial instruments which are involved.

If there are any impairment losses on the financial instruments then the provision is set for the

same. The carrying amount is reviewed at each balance sheet date and if there is any impairment

loss is there then the same is identified.

There is the use of the statistical methodology for the making of the provision in which all the

arrears, past losses, defaults and credit quality is taken into account. All of them affect the

financial position as they are included in the making of the accounts and provisions reduce the

amount of the financial instrument.

The company uses the hedging and there are policies which are set in this respect. In fair value

hedge, the contract of the cross currency and interest rate is maintained and changes in them are

considered as a hedge for which reporting is made. For the foreign currency, the forward

contracts are used and in case of net investment, the currency dominated borrowing is used so

that exposure can be hedged.

All of them are prepared in accordance with the procedure that is followed by all the other

companies. IFRS 9 is adopted by the company and there are various changes which will be made

due to the same. The financial statements will be affected as the now the financial instruments

will be measured and classified according to amortized cost. The credit losses which are

expected will have to be applied to the related undertakings and associates (Tesco, 2018). The

hedge related accounting will also be made according to IFRS 9. By all of these changes, the

financial statements will also be affected as the modifications will have to be made.

foreign exchange rates are considered as by that change in the accounts is made for the equity

and income.

All the loans and receivables are measured at amortized cost and for the measurement of

instruments that are available for sale, the FVOCI is taken into use. It has been assumed by the

company that all the receivables and loans will have to be measured under IFRS 9 at amortized

cost. The instruments for which the fair value is not available will be valued with the help of the

discounted future cash flows which have been projected (Tesco, 2018).

The provision has been made for the impairment of the financial instruments which are involved.

If there are any impairment losses on the financial instruments then the provision is set for the

same. The carrying amount is reviewed at each balance sheet date and if there is any impairment

loss is there then the same is identified.

There is the use of the statistical methodology for the making of the provision in which all the

arrears, past losses, defaults and credit quality is taken into account. All of them affect the

financial position as they are included in the making of the accounts and provisions reduce the

amount of the financial instrument.

The company uses the hedging and there are policies which are set in this respect. In fair value

hedge, the contract of the cross currency and interest rate is maintained and changes in them are

considered as a hedge for which reporting is made. For the foreign currency, the forward

contracts are used and in case of net investment, the currency dominated borrowing is used so

that exposure can be hedged.

All of them are prepared in accordance with the procedure that is followed by all the other

companies. IFRS 9 is adopted by the company and there are various changes which will be made

due to the same. The financial statements will be affected as the now the financial instruments

will be measured and classified according to amortized cost. The credit losses which are

expected will have to be applied to the related undertakings and associates (Tesco, 2018). The

hedge related accounting will also be made according to IFRS 9. By all of these changes, the

financial statements will also be affected as the modifications will have to be made.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

c) Post-employment benefits

The company has made certain policies for the defined benefit plans and in that the obligation

that is required to be met will have to be measured. The calculation will be made at the

discounted present value and all the plan assets will be required to be included at the fair value

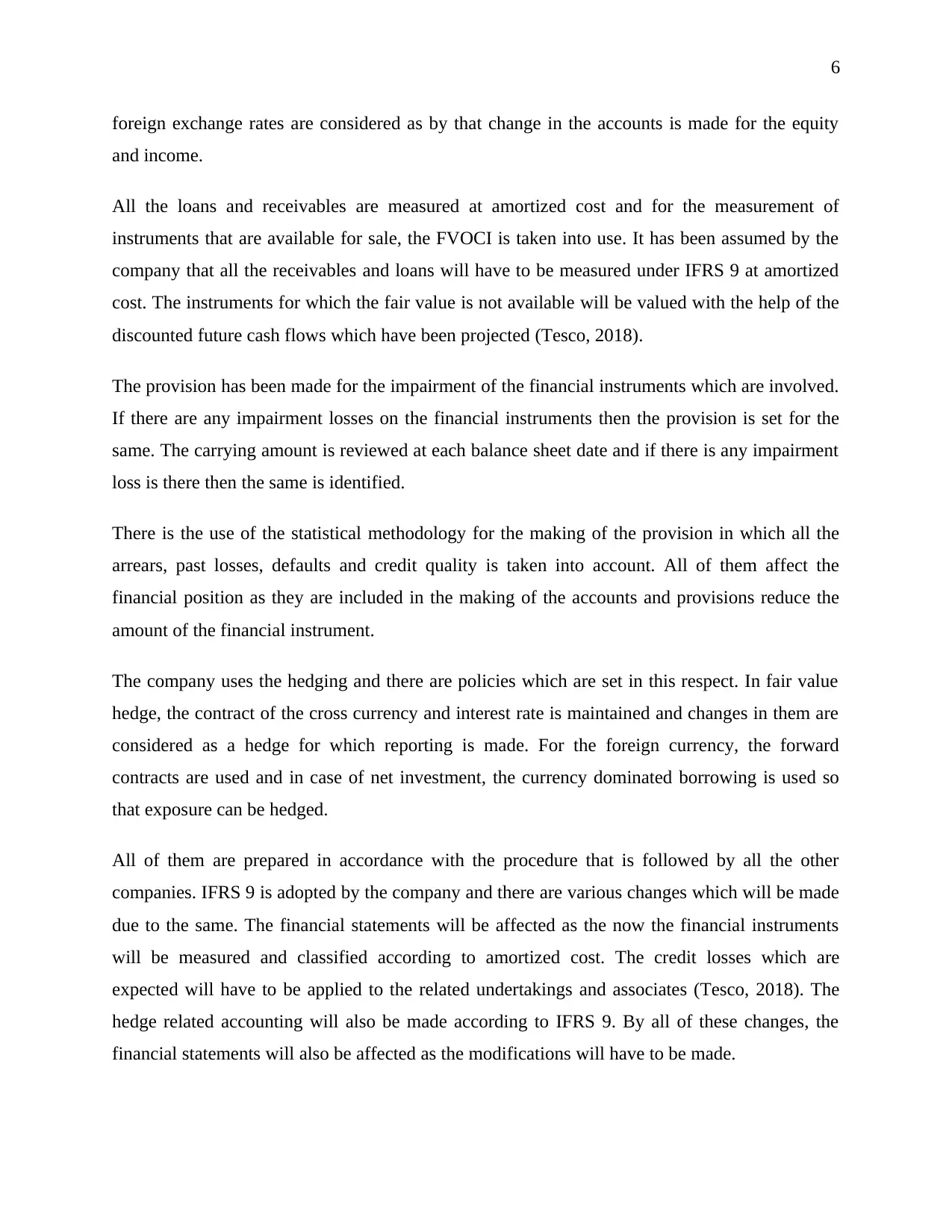

(Tesco, 2018). The undiscounted benefit payments which are estimated to be made in the total

life of scheme are as follows:

(Source: Tesco, 2018)

The costs which are incurred by the company for the operations and finances have been

recognized by the company in separate manner (Mohan and Zhang, 2014). There is the proper

basis which is used for the making of allocation of service cost and it is taken to be the expected

service lives of the employees. The recognition in respect of finance cost is made on the periodic

basis so that they can be correctly recorded.

In this policy, there are several assumptions which are made and in terms of financial

assumptions it is considered trend observables will be used for the corporate bond yields. In this,

it is taken that the discount rate will be taken from the market yields for the corporate bonds of

high quality. Another assumption is the mortality assumption in which the best estimate

assumption is considered so that the pension liability under IAS 19 can be calculated.

The table which is made in 2017 after the improvement in CMI 2016 is taken into use under the

assumptions (Tesco, 2018). By the help of the assumption, the gain has been increased and that

is represented in the financial statements. The discount rate is determined on the basis of the

high-quality corporate bonds and the market yield which is gained on them in relation to the

c) Post-employment benefits

The company has made certain policies for the defined benefit plans and in that the obligation

that is required to be met will have to be measured. The calculation will be made at the

discounted present value and all the plan assets will be required to be included at the fair value

(Tesco, 2018). The undiscounted benefit payments which are estimated to be made in the total

life of scheme are as follows:

(Source: Tesco, 2018)

The costs which are incurred by the company for the operations and finances have been

recognized by the company in separate manner (Mohan and Zhang, 2014). There is the proper

basis which is used for the making of allocation of service cost and it is taken to be the expected

service lives of the employees. The recognition in respect of finance cost is made on the periodic

basis so that they can be correctly recorded.

In this policy, there are several assumptions which are made and in terms of financial

assumptions it is considered trend observables will be used for the corporate bond yields. In this,

it is taken that the discount rate will be taken from the market yields for the corporate bonds of

high quality. Another assumption is the mortality assumption in which the best estimate

assumption is considered so that the pension liability under IAS 19 can be calculated.

The table which is made in 2017 after the improvement in CMI 2016 is taken into use under the

assumptions (Tesco, 2018). By the help of the assumption, the gain has been increased and that

is represented in the financial statements. The discount rate is determined on the basis of the

high-quality corporate bonds and the market yield which is gained on them in relation to the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

suitable currency (Han and Hung, 2012). It is not much realistic as the specifications for the

situation in which bond will not be available is not provided.

The sensitivity test is conducted and it is identified that there is no linear movement in the

sensitivities. The changes which are taking place in the inflation rate and discount rate will be off

settled from the movements in assets in a partial manner (Tesco, 2018). The current status of the

plan is good and there is the improvement which is made in the same as the gain from the same

has increased.

There is the defined contribution which is to be met and in the current case it is £316m and the

same has been considered in the income statement which is presented in the group. In this, the

pension contribution has also been considered and the same is amounting to £108m (Tesco,

2018). The amount of the defined pension assets has increased and that will be beneficial for the

company. The financial position of the company is improving by this and there will be no

adverse impact which will be faced. The policies which have been set in this respect have

complied in the most effective manner.

Conclusion

In the report, all the major policies which are framed and the manner in which they have been

taken into account by the Tesco have been considered. All the disclosures which are made will

be beneficial for the future period. The complete review is made in which all the aspects which

are involved in relation to the policies for the defined benefit plans, impairment, and financial

instruments have been included. The company has maintained the complete and appropriate

disclosure policies in which all the information is provided in a clear manner. The quality of the

information that is included is maintained and it is true to the best of the knowledge which

provides the appropriate position of the business. The conceptual framework is established and in

that various characteristics are involved which needs to be considered. The main among them in

relation to the qualitative characteristics are relevance, materiality, and faithful representation.

All of them have been considered by the company and have been followed in the most effective

manner. The information which is presented is in the best quality and in that all the relevant

aspects have been given the required importance. The information about the impairment testing

is provided and in that the assumptions have been made and all of them are in context with the

suitable currency (Han and Hung, 2012). It is not much realistic as the specifications for the

situation in which bond will not be available is not provided.

The sensitivity test is conducted and it is identified that there is no linear movement in the

sensitivities. The changes which are taking place in the inflation rate and discount rate will be off

settled from the movements in assets in a partial manner (Tesco, 2018). The current status of the

plan is good and there is the improvement which is made in the same as the gain from the same

has increased.

There is the defined contribution which is to be met and in the current case it is £316m and the

same has been considered in the income statement which is presented in the group. In this, the

pension contribution has also been considered and the same is amounting to £108m (Tesco,

2018). The amount of the defined pension assets has increased and that will be beneficial for the

company. The financial position of the company is improving by this and there will be no

adverse impact which will be faced. The policies which have been set in this respect have

complied in the most effective manner.

Conclusion

In the report, all the major policies which are framed and the manner in which they have been

taken into account by the Tesco have been considered. All the disclosures which are made will

be beneficial for the future period. The complete review is made in which all the aspects which

are involved in relation to the policies for the defined benefit plans, impairment, and financial

instruments have been included. The company has maintained the complete and appropriate

disclosure policies in which all the information is provided in a clear manner. The quality of the

information that is included is maintained and it is true to the best of the knowledge which

provides the appropriate position of the business. The conceptual framework is established and in

that various characteristics are involved which needs to be considered. The main among them in

relation to the qualitative characteristics are relevance, materiality, and faithful representation.

All of them have been considered by the company and have been followed in the most effective

manner. The information which is presented is in the best quality and in that all the relevant

aspects have been given the required importance. The information about the impairment testing

is provided and in that the assumptions have been made and all of them are in context with the

9

historical data. The calculation which is made for the financial instruments have been done with

the help of discounting cash flow method by which future aspects have also been considered.

There is the inclusion of the material information which will be useful in the making of further

decisions and analyzation. The representation is made in such manner that the faith will be

established and all will be willing to accept the information that is provided and take that in use

for further actions.

historical data. The calculation which is made for the financial instruments have been done with

the help of discounting cash flow method by which future aspects have also been considered.

There is the inclusion of the material information which will be useful in the making of further

decisions and analyzation. The representation is made in such manner that the faith will be

established and all will be willing to accept the information that is provided and take that in use

for further actions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

References

André, P., Dionysiou, D. and Tsalavoutas, I. (2018) Mandated disclosures under IAS 36

Impairment of Assets and IAS 38 Intangible Assets: value relevance and impact on analysts’

forecasts. Applied Economics, 50(7), pp.707-725.

Avallone, F. and Quagli, A. (2015) Insight into the variables used to manage the goodwill

impairment test under IAS 36. Advances in accounting, 31(1), pp.107-114.

Coste, A.I., Tudor, A.T. and Pali-Pista, S.F. (2014) Compliance of Non-current Assets with IFRS

Requirements Concerning the Information Disclosure–Case Study. Procedia Economics and

Finance, 15, pp.1391-1395.

D'Alauro, G. (2013) The impact of IAS 36 on goodwill disclosure: Evidence of the write-offs

and performance effects. Intangible capital, 9(3), pp.754-799.

Han, N.W. and Hung, M.W. (2012) Optimal asset allocation for DC pension plans under

inflation. Insurance: Mathematics and Economics, 51(1), pp.172-181.

Mohan, N. and Zhang, T. (2014) An analysis of risk-taking behavior for public defined benefit

pension plans. Journal of Banking & Finance, 40, pp.403-419.

Novotny-Farkas, Z. (2016) The interaction of the IFRS 9 expected loss approach with

supervisory rules and implications for financial stability. Accounting in Europe, 13(2), pp.197-

227.

Onali, E. and Ginesti, G. (2014) Pre-adoption market reaction to IFRS 9: A cross-country event-

study. Journal of Accounting and Public Policy, 33(6), pp.628-637.

Tesco. (2018) Annual report 2018. [Online] Available at:

https://www.tescoplc.com/media/474793/tesco_ar_2018.pdf [Accessed 11 June 2019]

References

André, P., Dionysiou, D. and Tsalavoutas, I. (2018) Mandated disclosures under IAS 36

Impairment of Assets and IAS 38 Intangible Assets: value relevance and impact on analysts’

forecasts. Applied Economics, 50(7), pp.707-725.

Avallone, F. and Quagli, A. (2015) Insight into the variables used to manage the goodwill

impairment test under IAS 36. Advances in accounting, 31(1), pp.107-114.

Coste, A.I., Tudor, A.T. and Pali-Pista, S.F. (2014) Compliance of Non-current Assets with IFRS

Requirements Concerning the Information Disclosure–Case Study. Procedia Economics and

Finance, 15, pp.1391-1395.

D'Alauro, G. (2013) The impact of IAS 36 on goodwill disclosure: Evidence of the write-offs

and performance effects. Intangible capital, 9(3), pp.754-799.

Han, N.W. and Hung, M.W. (2012) Optimal asset allocation for DC pension plans under

inflation. Insurance: Mathematics and Economics, 51(1), pp.172-181.

Mohan, N. and Zhang, T. (2014) An analysis of risk-taking behavior for public defined benefit

pension plans. Journal of Banking & Finance, 40, pp.403-419.

Novotny-Farkas, Z. (2016) The interaction of the IFRS 9 expected loss approach with

supervisory rules and implications for financial stability. Accounting in Europe, 13(2), pp.197-

227.

Onali, E. and Ginesti, G. (2014) Pre-adoption market reaction to IFRS 9: A cross-country event-

study. Journal of Accounting and Public Policy, 33(6), pp.628-637.

Tesco. (2018) Annual report 2018. [Online] Available at:

https://www.tescoplc.com/media/474793/tesco_ar_2018.pdf [Accessed 11 June 2019]

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.