University Report: Advanced Corporate Reporting and Share Performance

VerifiedAdded on 2021/04/24

|18

|3675

|180

Report

AI Summary

This report analyzes the impact of earnings announcements on share price performance. It begins with an introduction to the relevance of earnings announcements and provides empirical evidence from various research papers. The methodology involves collecting data from Yahoo Finance and analyzing abnormal returns, Steyx Squared, and T-tests. The analysis includes examining the average abnormal returns for companies with both good and bad earnings announcements. The report presents detailed calculations of test statistics, including Steyx and Steyx Squared, to determine the significance of earnings announcements on share price movement. The findings highlight the positive correlation between good earnings announcements and increased share value and the negative impact of bad earnings announcements. The report concludes by summarizing the impact of earnings announcements on the stock market, offering valuable insights for investors and financial analysts.

Running head: ADVANCED CORPORATE REPORTING

Advanced Corporate Reporting

Name of the Student:

Name of the University:

Authors Note:

Advanced Corporate Reporting

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED CORPORATE REPORTING

1

Table of Contents

4.0 Report/Essay:.......................................................................................................................2

Introduction:...............................................................................................................................2

Importance/relevance of earnings announcements:...................................................................2

Empirical evidence on the wealth effects of earnings announcements:.....................................3

Methodology:.............................................................................................................................5

Analysis of the result:.................................................................................................................5

Conclusion:..............................................................................................................................11

Reference and Bibliography:....................................................................................................12

Appendices:..............................................................................................................................15

1

Table of Contents

4.0 Report/Essay:.......................................................................................................................2

Introduction:...............................................................................................................................2

Importance/relevance of earnings announcements:...................................................................2

Empirical evidence on the wealth effects of earnings announcements:.....................................3

Methodology:.............................................................................................................................5

Analysis of the result:.................................................................................................................5

Conclusion:..............................................................................................................................11

Reference and Bibliography:....................................................................................................12

Appendices:..............................................................................................................................15

ADVANCED CORPORATE REPORTING

2

4.0 Report/Essay:

Introduction:

The overall assessment mainly focuses in deriving the impact of earnings report on

share price performance of the company. In addition, the assessment focuses on detecting the

abnormal returns, which is achieved by the company. Moreover, the importance or relevance

of earnings announcement is effectively depicted in the report, which could allow investor to

understanding the impact of announcements on share price. The valuation of abnormal

returns, Steyx Squared and T-Test is being conducted to identify the calculation and position

of the company to generate high return. Moreover, the impact of good announcement and bad

announcement on shar price of the company is appropriately evaluated. Furthermore, the

calculation will allow investor to investigate the wealth effects of earnings announcement

made by firms. The use of slope, intercept, Steyx and Rsquared is used in detecting the

abnormal returns and expected return of the 10 shares.

Importance/relevance of earnings announcements:

Earnings announcement is detected to be the most viable information, which could

depict the financial position of the company. In addition, financial performance of the

company is identified with the help of announcement, which relatively depicts their actual

financial condition. The investors use of fundamental and technical analysis to derive the

valuation of their share price, which might help in detecting its actual share price (Marshall,

Schroeder and Yohn 2017). According to IFRS, the companies mainly need to provide all the

relevant details regarding the financial progress on all quarters. Moreover, with the whelp in

earning announcement the investors can confirm the management’s forecasting. The earnings

announcement is essential, as it portrays the path way, which has been adopted by the

2

4.0 Report/Essay:

Introduction:

The overall assessment mainly focuses in deriving the impact of earnings report on

share price performance of the company. In addition, the assessment focuses on detecting the

abnormal returns, which is achieved by the company. Moreover, the importance or relevance

of earnings announcement is effectively depicted in the report, which could allow investor to

understanding the impact of announcements on share price. The valuation of abnormal

returns, Steyx Squared and T-Test is being conducted to identify the calculation and position

of the company to generate high return. Moreover, the impact of good announcement and bad

announcement on shar price of the company is appropriately evaluated. Furthermore, the

calculation will allow investor to investigate the wealth effects of earnings announcement

made by firms. The use of slope, intercept, Steyx and Rsquared is used in detecting the

abnormal returns and expected return of the 10 shares.

Importance/relevance of earnings announcements:

Earnings announcement is detected to be the most viable information, which could

depict the financial position of the company. In addition, financial performance of the

company is identified with the help of announcement, which relatively depicts their actual

financial condition. The investors use of fundamental and technical analysis to derive the

valuation of their share price, which might help in detecting its actual share price (Marshall,

Schroeder and Yohn 2017). According to IFRS, the companies mainly need to provide all the

relevant details regarding the financial progress on all quarters. Moreover, with the whelp in

earning announcement the investors can confirm the management’s forecasting. The earnings

announcement is essential, as it portrays the path way, which has been adopted by the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED CORPORATE REPORTING

3

company to achieve sustainable growth. Lastly, companies by depicting the announcements

can portray their operational capability to the investor, which might help in mentioning their

operations.

Empirical evidence on the wealth effects of earnings announcements:

The empirical evidence on effectiveness of earnings announcements on wealth are

depicted as follows.

According to Ball and Shivakumar (2008), the relevant information presented in the

earnings report are effectively depicted. The journal states the impact and significance of

earning announcements, where all the new information is presented in the annual report. The

earnings announcement evaluation in the journal indicates the financial performance, which

could improve profits of the company. Therefore, the journal evaluates the performance of

earnings announcement in improving shar price of the company.

According to MacKinlay (1997), the impact of announcement is relatively evaluated,

which might help investors in generating high level of returns. Moreover, the author indicated

the positive attribute of announcement, which helps in improving its share valuation.

Furthermore, the author stated that announcement having positive market power could

increase shar price of the organisation. The empirical research indicates the power of positive

announcement, which could improve demand of shares among potential investors.

According to Afego (2013), the impact of annual report announcements on stock

market performance is evaluated. In addition, the journal sheds light on the impact of

earnings announcement and how share price of the company increases due to rising financial

position. The positive and adverse impact of financial announcement is effectively evaluated

by the paper, which indicates the influence of announcement earnings on share price of the

3

company to achieve sustainable growth. Lastly, companies by depicting the announcements

can portray their operational capability to the investor, which might help in mentioning their

operations.

Empirical evidence on the wealth effects of earnings announcements:

The empirical evidence on effectiveness of earnings announcements on wealth are

depicted as follows.

According to Ball and Shivakumar (2008), the relevant information presented in the

earnings report are effectively depicted. The journal states the impact and significance of

earning announcements, where all the new information is presented in the annual report. The

earnings announcement evaluation in the journal indicates the financial performance, which

could improve profits of the company. Therefore, the journal evaluates the performance of

earnings announcement in improving shar price of the company.

According to MacKinlay (1997), the impact of announcement is relatively evaluated,

which might help investors in generating high level of returns. Moreover, the author indicated

the positive attribute of announcement, which helps in improving its share valuation.

Furthermore, the author stated that announcement having positive market power could

increase shar price of the organisation. The empirical research indicates the power of positive

announcement, which could improve demand of shares among potential investors.

According to Afego (2013), the impact of annual report announcements on stock

market performance is evaluated. In addition, the journal sheds light on the impact of

earnings announcement and how share price of the company increases due to rising financial

position. The positive and adverse impact of financial announcement is effectively evaluated

by the paper, which indicates the influence of announcement earnings on share price of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED CORPORATE REPORTING

4

company. The journal evaluates the impact of share price from 20 days before and after the

announcement. This relevantly depicts the actual change in share price of the company due to

rise in its earnings.

Mlonzi, Kruger and Nthoesane (2011) indicates the duty of the company towards its

shareholders and investor, which could increase their share price valuation. In addition, the

researcher indicates the relation of financial performance and increment in share value, which

is been conducted after the announcement. In addition, the researcher indicates substantial

decline in share price, which is conducted after the announcement conducted by Nigerian

companies. The study indicates negative impact of announcement in share price of the

company, due to weak form of market efficiency. The journal mainly states the negative

attributes of the announcement measure, which is been used by companies in Nigeria.

Eleke-Aboagye and Opoku (2013) stated that earnings announcement indicates the

financial performance and share price movement of the company. Moreover, the research

evaluated 21 days share price movement during and after the announcement, which could

help in depicting effectiveness of the announcement. The results depicted in the research

indicates that the price movement of the stock was according to the news of the

announcement. Good news mainly increased share price of the company, while the decline in

value is seen when bad announcement is conducted.

Su (2003) mentioned in the journal about the changes in share price of the company

due to relevant announcements conducted in Chinese stock market. In addition, the journal

indicates the achievement of abnormal returns, which is generated after the earnings

announcements. Moreover, the journal also indicates that shareholder with the help in

earnings announcement can increase their return from investment.

4

company. The journal evaluates the impact of share price from 20 days before and after the

announcement. This relevantly depicts the actual change in share price of the company due to

rise in its earnings.

Mlonzi, Kruger and Nthoesane (2011) indicates the duty of the company towards its

shareholders and investor, which could increase their share price valuation. In addition, the

researcher indicates the relation of financial performance and increment in share value, which

is been conducted after the announcement. In addition, the researcher indicates substantial

decline in share price, which is conducted after the announcement conducted by Nigerian

companies. The study indicates negative impact of announcement in share price of the

company, due to weak form of market efficiency. The journal mainly states the negative

attributes of the announcement measure, which is been used by companies in Nigeria.

Eleke-Aboagye and Opoku (2013) stated that earnings announcement indicates the

financial performance and share price movement of the company. Moreover, the research

evaluated 21 days share price movement during and after the announcement, which could

help in depicting effectiveness of the announcement. The results depicted in the research

indicates that the price movement of the stock was according to the news of the

announcement. Good news mainly increased share price of the company, while the decline in

value is seen when bad announcement is conducted.

Su (2003) mentioned in the journal about the changes in share price of the company

due to relevant announcements conducted in Chinese stock market. In addition, the journal

indicates the achievement of abnormal returns, which is generated after the earnings

announcements. Moreover, the journal also indicates that shareholder with the help in

earnings announcement can increase their return from investment.

ADVANCED CORPORATE REPORTING

5

The relevant journals, depicted above mentions the positive and negative attributes of

earnings announcements. In addition, the journal sheds light on the impact of earning

announcements on share price valuation of the company.

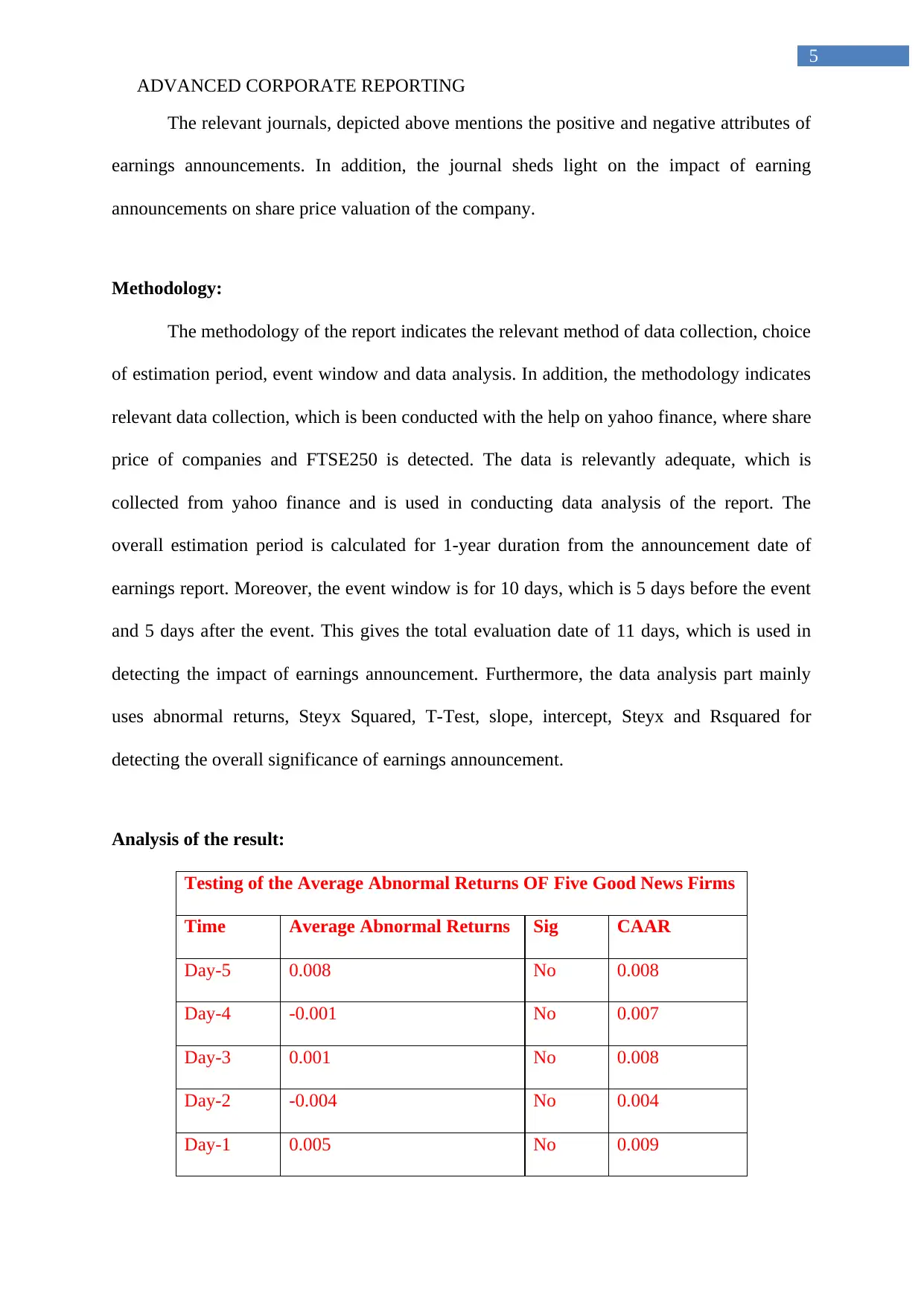

Methodology:

The methodology of the report indicates the relevant method of data collection, choice

of estimation period, event window and data analysis. In addition, the methodology indicates

relevant data collection, which is been conducted with the help on yahoo finance, where share

price of companies and FTSE250 is detected. The data is relevantly adequate, which is

collected from yahoo finance and is used in conducting data analysis of the report. The

overall estimation period is calculated for 1-year duration from the announcement date of

earnings report. Moreover, the event window is for 10 days, which is 5 days before the event

and 5 days after the event. This gives the total evaluation date of 11 days, which is used in

detecting the impact of earnings announcement. Furthermore, the data analysis part mainly

uses abnormal returns, Steyx Squared, T-Test, slope, intercept, Steyx and Rsquared for

detecting the overall significance of earnings announcement.

Analysis of the result:

Testing of the Average Abnormal Returns OF Five Good News Firms

Time Average Abnormal Returns Sig CAAR

Day-5 0.008 No 0.008

Day-4 -0.001 No 0.007

Day-3 0.001 No 0.008

Day-2 -0.004 No 0.004

Day-1 0.005 No 0.009

5

The relevant journals, depicted above mentions the positive and negative attributes of

earnings announcements. In addition, the journal sheds light on the impact of earning

announcements on share price valuation of the company.

Methodology:

The methodology of the report indicates the relevant method of data collection, choice

of estimation period, event window and data analysis. In addition, the methodology indicates

relevant data collection, which is been conducted with the help on yahoo finance, where share

price of companies and FTSE250 is detected. The data is relevantly adequate, which is

collected from yahoo finance and is used in conducting data analysis of the report. The

overall estimation period is calculated for 1-year duration from the announcement date of

earnings report. Moreover, the event window is for 10 days, which is 5 days before the event

and 5 days after the event. This gives the total evaluation date of 11 days, which is used in

detecting the impact of earnings announcement. Furthermore, the data analysis part mainly

uses abnormal returns, Steyx Squared, T-Test, slope, intercept, Steyx and Rsquared for

detecting the overall significance of earnings announcement.

Analysis of the result:

Testing of the Average Abnormal Returns OF Five Good News Firms

Time Average Abnormal Returns Sig CAAR

Day-5 0.008 No 0.008

Day-4 -0.001 No 0.007

Day-3 0.001 No 0.008

Day-2 -0.004 No 0.004

Day-1 0.005 No 0.009

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED CORPORATE REPORTING

6

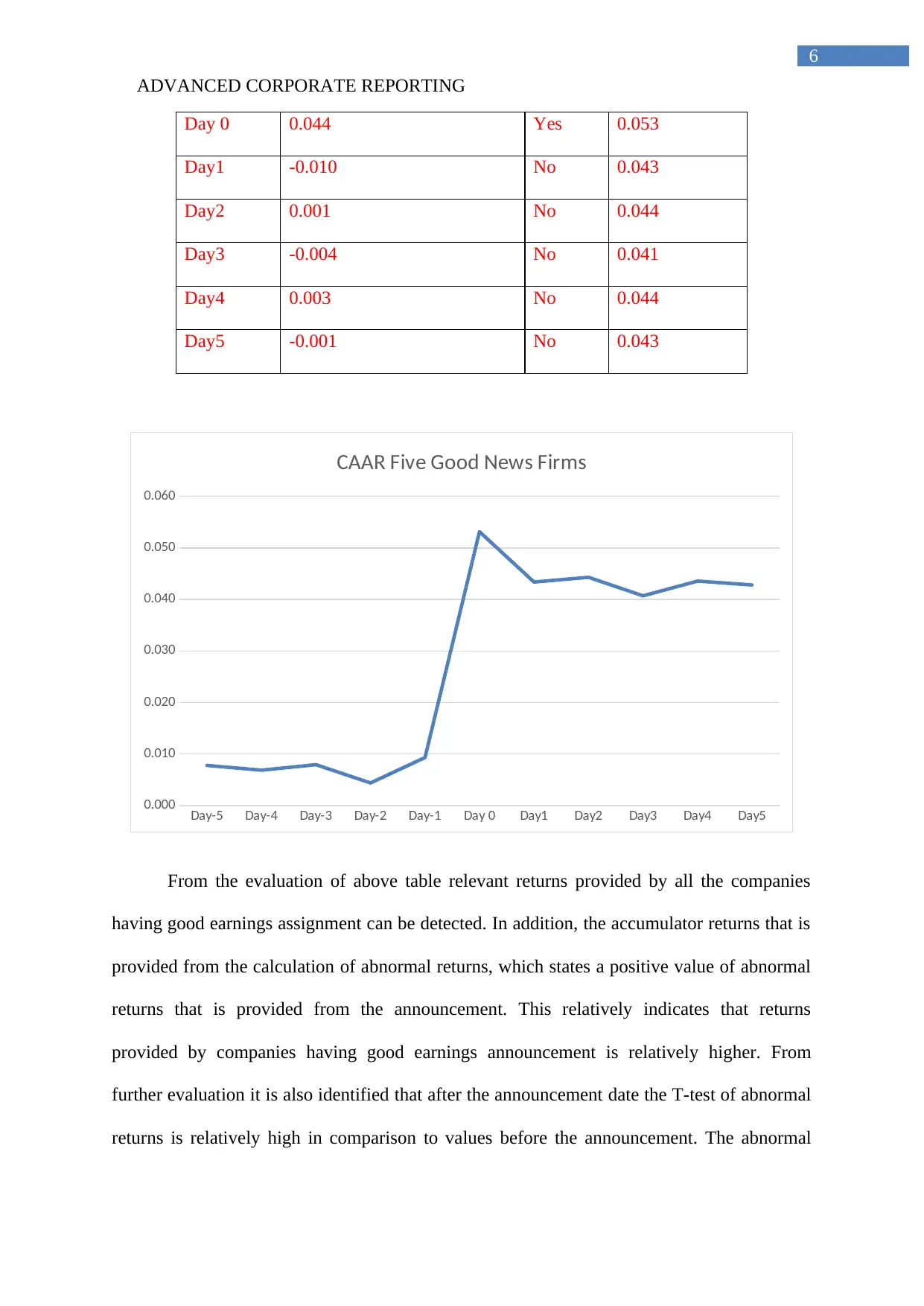

Day 0 0.044 Yes 0.053

Day1 -0.010 No 0.043

Day2 0.001 No 0.044

Day3 -0.004 No 0.041

Day4 0.003 No 0.044

Day5 -0.001 No 0.043

Day-5 Day-4 Day-3 Day-2 Day-1 Day 0 Day1 Day2 Day3 Day4 Day5

0.000

0.010

0.020

0.030

0.040

0.050

0.060

CAAR Five Good News Firms

From the evaluation of above table relevant returns provided by all the companies

having good earnings assignment can be detected. In addition, the accumulator returns that is

provided from the calculation of abnormal returns, which states a positive value of abnormal

returns that is provided from the announcement. This relatively indicates that returns

provided by companies having good earnings announcement is relatively higher. From

further evaluation it is also identified that after the announcement date the T-test of abnormal

returns is relatively high in comparison to values before the announcement. The abnormal

6

Day 0 0.044 Yes 0.053

Day1 -0.010 No 0.043

Day2 0.001 No 0.044

Day3 -0.004 No 0.041

Day4 0.003 No 0.044

Day5 -0.001 No 0.043

Day-5 Day-4 Day-3 Day-2 Day-1 Day 0 Day1 Day2 Day3 Day4 Day5

0.000

0.010

0.020

0.030

0.040

0.050

0.060

CAAR Five Good News Firms

From the evaluation of above table relevant returns provided by all the companies

having good earnings assignment can be detected. In addition, the accumulator returns that is

provided from the calculation of abnormal returns, which states a positive value of abnormal

returns that is provided from the announcement. This relatively indicates that returns

provided by companies having good earnings announcement is relatively higher. From

further evaluation it is also identified that after the announcement date the T-test of abnormal

returns is relatively high in comparison to values before the announcement. The abnormal

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED CORPORATE REPORTING

7

returns during the announcement is relatively higher income parents to all the other days,

which is supported by the signal provider from T-test of abnormal returns.

The calculation also indicates a high CAAR of 0.043, which is derived from the

abnormal returns. This directly indicates the positive attributes of good earnings

announcement, which is conducted by the companies. The highest average abnormal returns

were only detected on the day of the announcement, which was conducted by the company.

This relatively indicates that positive earnings announcement increases the value of shares

and provides investors with abnormal returns. In this context, Frederickson and Zolotoy

(2015) argued that increment in abnormal returns relatively indicates the wrong pricing of

shares, which is conducted by investors.

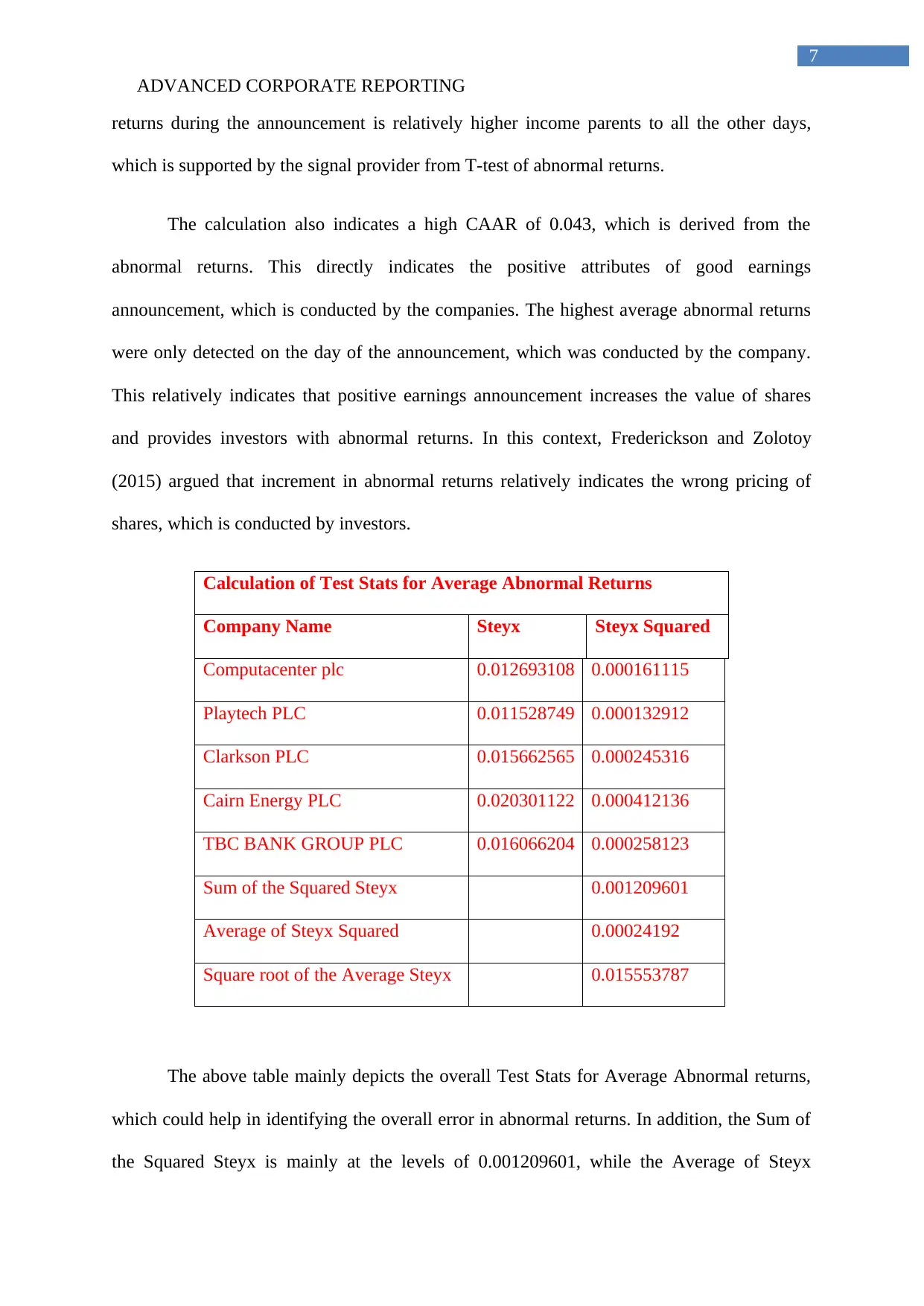

Calculation of Test Stats for Average Abnormal Returns

Company Name Steyx Steyx Squared

Computacenter plc 0.012693108 0.000161115

Playtech PLC 0.011528749 0.000132912

Clarkson PLC 0.015662565 0.000245316

Cairn Energy PLC 0.020301122 0.000412136

TBC BANK GROUP PLC 0.016066204 0.000258123

Sum of the Squared Steyx 0.001209601

Average of Steyx Squared 0.00024192

Square root of the Average Steyx 0.015553787

The above table mainly depicts the overall Test Stats for Average Abnormal returns,

which could help in identifying the overall error in abnormal returns. In addition, the Sum of

the Squared Steyx is mainly at the levels of 0.001209601, while the Average of Steyx

7

returns during the announcement is relatively higher income parents to all the other days,

which is supported by the signal provider from T-test of abnormal returns.

The calculation also indicates a high CAAR of 0.043, which is derived from the

abnormal returns. This directly indicates the positive attributes of good earnings

announcement, which is conducted by the companies. The highest average abnormal returns

were only detected on the day of the announcement, which was conducted by the company.

This relatively indicates that positive earnings announcement increases the value of shares

and provides investors with abnormal returns. In this context, Frederickson and Zolotoy

(2015) argued that increment in abnormal returns relatively indicates the wrong pricing of

shares, which is conducted by investors.

Calculation of Test Stats for Average Abnormal Returns

Company Name Steyx Steyx Squared

Computacenter plc 0.012693108 0.000161115

Playtech PLC 0.011528749 0.000132912

Clarkson PLC 0.015662565 0.000245316

Cairn Energy PLC 0.020301122 0.000412136

TBC BANK GROUP PLC 0.016066204 0.000258123

Sum of the Squared Steyx 0.001209601

Average of Steyx Squared 0.00024192

Square root of the Average Steyx 0.015553787

The above table mainly depicts the overall Test Stats for Average Abnormal returns,

which could help in identifying the overall error in abnormal returns. In addition, the Sum of

the Squared Steyx is mainly at the levels of 0.001209601, while the Average of Steyx

ADVANCED CORPORATE REPORTING

8

Squared is at 0.00024192. Moreover, the Square root of the Average Steyx directly indicate

the minimum error in returns from investment. Furthermore, Square root of the Average

Steyx is at the levels of 0.015553787, which is used in detective CAAR. Jenkins, Kimbrough

and Wang (2016) mentioned that with the help of Steyx functions investor can identify the

abnormal returns, which is generated from stocks.

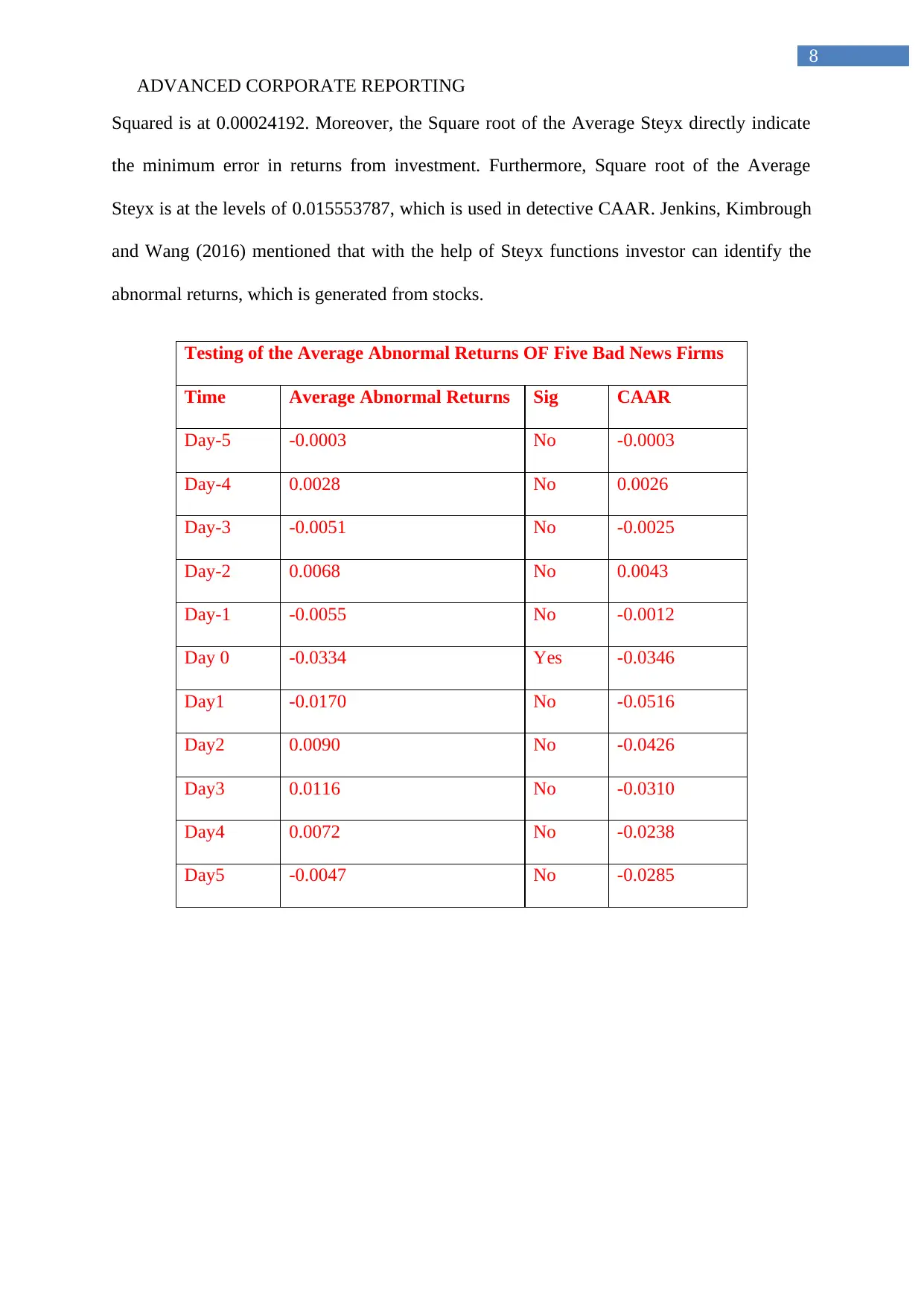

Testing of the Average Abnormal Returns OF Five Bad News Firms

Time Average Abnormal Returns Sig CAAR

Day-5 -0.0003 No -0.0003

Day-4 0.0028 No 0.0026

Day-3 -0.0051 No -0.0025

Day-2 0.0068 No 0.0043

Day-1 -0.0055 No -0.0012

Day 0 -0.0334 Yes -0.0346

Day1 -0.0170 No -0.0516

Day2 0.0090 No -0.0426

Day3 0.0116 No -0.0310

Day4 0.0072 No -0.0238

Day5 -0.0047 No -0.0285

8

Squared is at 0.00024192. Moreover, the Square root of the Average Steyx directly indicate

the minimum error in returns from investment. Furthermore, Square root of the Average

Steyx is at the levels of 0.015553787, which is used in detective CAAR. Jenkins, Kimbrough

and Wang (2016) mentioned that with the help of Steyx functions investor can identify the

abnormal returns, which is generated from stocks.

Testing of the Average Abnormal Returns OF Five Bad News Firms

Time Average Abnormal Returns Sig CAAR

Day-5 -0.0003 No -0.0003

Day-4 0.0028 No 0.0026

Day-3 -0.0051 No -0.0025

Day-2 0.0068 No 0.0043

Day-1 -0.0055 No -0.0012

Day 0 -0.0334 Yes -0.0346

Day1 -0.0170 No -0.0516

Day2 0.0090 No -0.0426

Day3 0.0116 No -0.0310

Day4 0.0072 No -0.0238

Day5 -0.0047 No -0.0285

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED CORPORATE REPORTING

9

Day-5 Day-4 Day-3 Day-2 Day-1 Day 0 Day1 Day2 Day3 Day4 Day5

-0.0600

-0.0500

-0.0400

-0.0300

-0.0200

-0.0100

0.0000

0.0100

CAAR Five Bad News Firms

CAAR

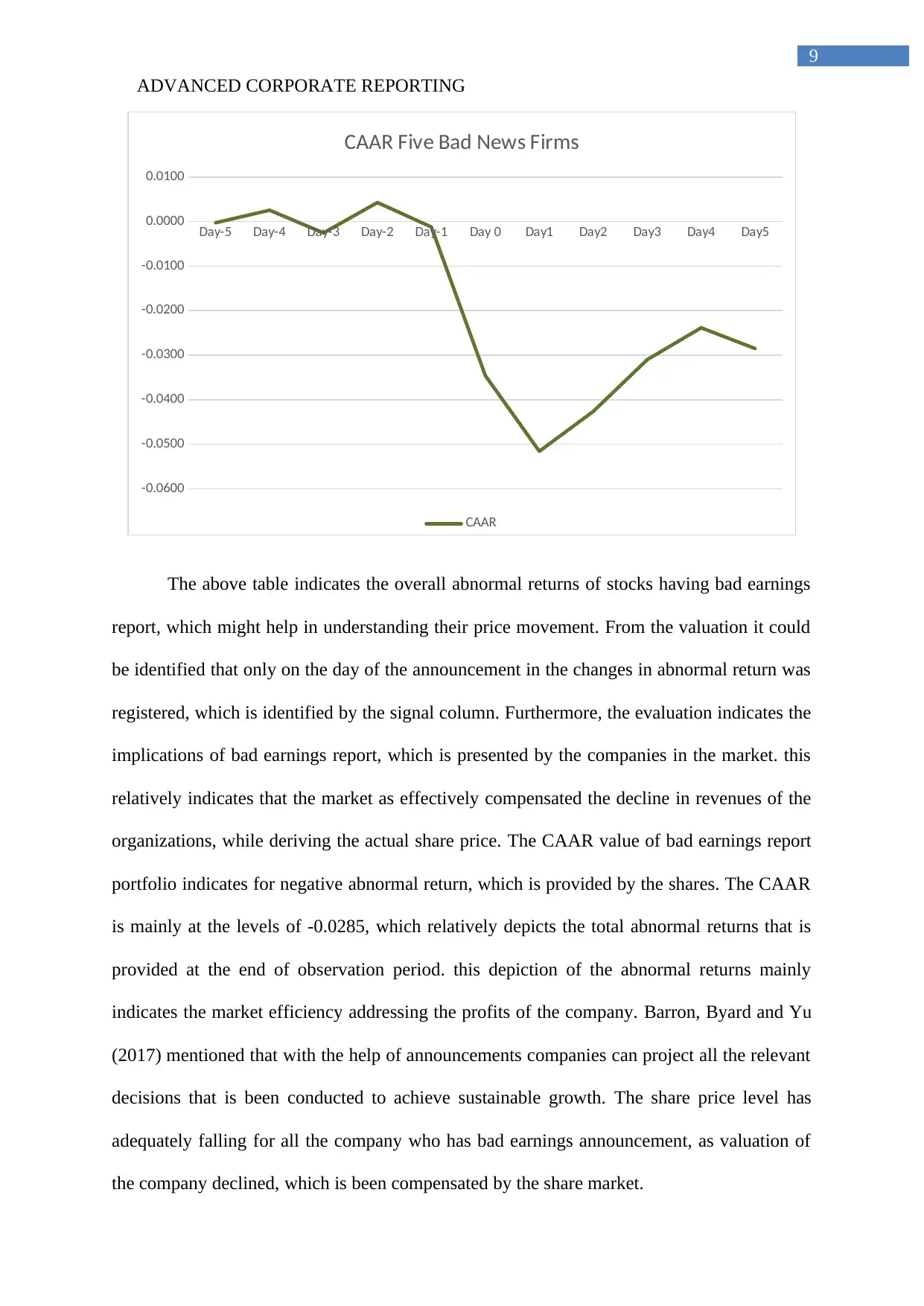

The above table indicates the overall abnormal returns of stocks having bad earnings

report, which might help in understanding their price movement. From the valuation it could

be identified that only on the day of the announcement in the changes in abnormal return was

registered, which is identified by the signal column. Furthermore, the evaluation indicates the

implications of bad earnings report, which is presented by the companies in the market. this

relatively indicates that the market as effectively compensated the decline in revenues of the

organizations, while deriving the actual share price. The CAAR value of bad earnings report

portfolio indicates for negative abnormal return, which is provided by the shares. The CAAR

is mainly at the levels of -0.0285, which relatively depicts the total abnormal returns that is

provided at the end of observation period. this depiction of the abnormal returns mainly

indicates the market efficiency addressing the profits of the company. Barron, Byard and Yu

(2017) mentioned that with the help of announcements companies can project all the relevant

decisions that is been conducted to achieve sustainable growth. The share price level has

adequately falling for all the company who has bad earnings announcement, as valuation of

the company declined, which is been compensated by the share market.

9

Day-5 Day-4 Day-3 Day-2 Day-1 Day 0 Day1 Day2 Day3 Day4 Day5

-0.0600

-0.0500

-0.0400

-0.0300

-0.0200

-0.0100

0.0000

0.0100

CAAR Five Bad News Firms

CAAR

The above table indicates the overall abnormal returns of stocks having bad earnings

report, which might help in understanding their price movement. From the valuation it could

be identified that only on the day of the announcement in the changes in abnormal return was

registered, which is identified by the signal column. Furthermore, the evaluation indicates the

implications of bad earnings report, which is presented by the companies in the market. this

relatively indicates that the market as effectively compensated the decline in revenues of the

organizations, while deriving the actual share price. The CAAR value of bad earnings report

portfolio indicates for negative abnormal return, which is provided by the shares. The CAAR

is mainly at the levels of -0.0285, which relatively depicts the total abnormal returns that is

provided at the end of observation period. this depiction of the abnormal returns mainly

indicates the market efficiency addressing the profits of the company. Barron, Byard and Yu

(2017) mentioned that with the help of announcements companies can project all the relevant

decisions that is been conducted to achieve sustainable growth. The share price level has

adequately falling for all the company who has bad earnings announcement, as valuation of

the company declined, which is been compensated by the share market.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED CORPORATE REPORTING

10

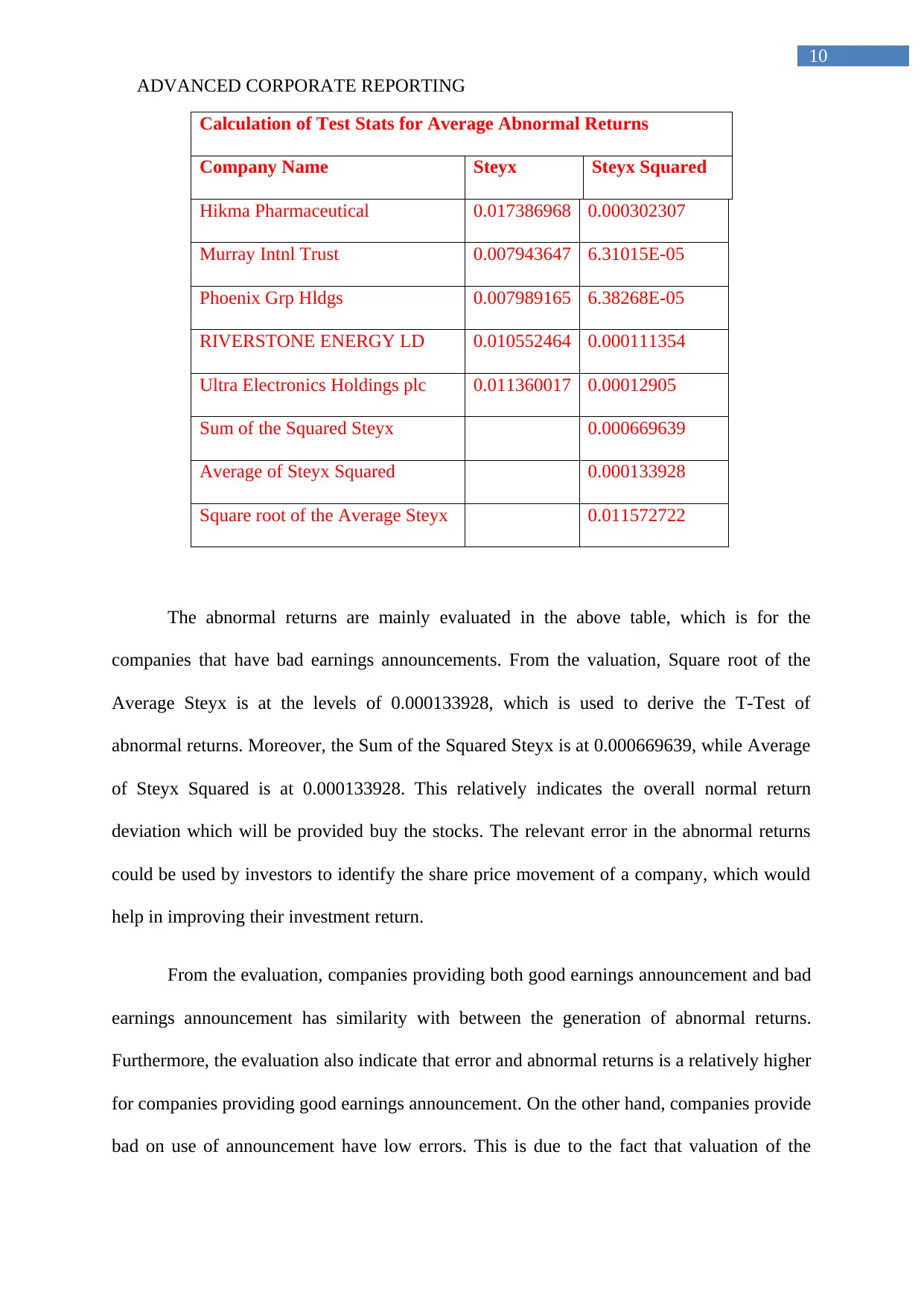

Calculation of Test Stats for Average Abnormal Returns

Company Name Steyx Steyx Squared

Hikma Pharmaceutical 0.017386968 0.000302307

Murray Intnl Trust 0.007943647 6.31015E-05

Phoenix Grp Hldgs 0.007989165 6.38268E-05

RIVERSTONE ENERGY LD 0.010552464 0.000111354

Ultra Electronics Holdings plc 0.011360017 0.00012905

Sum of the Squared Steyx 0.000669639

Average of Steyx Squared 0.000133928

Square root of the Average Steyx 0.011572722

The abnormal returns are mainly evaluated in the above table, which is for the

companies that have bad earnings announcements. From the valuation, Square root of the

Average Steyx is at the levels of 0.000133928, which is used to derive the T-Test of

abnormal returns. Moreover, the Sum of the Squared Steyx is at 0.000669639, while Average

of Steyx Squared is at 0.000133928. This relatively indicates the overall normal return

deviation which will be provided buy the stocks. The relevant error in the abnormal returns

could be used by investors to identify the share price movement of a company, which would

help in improving their investment return.

From the evaluation, companies providing both good earnings announcement and bad

earnings announcement has similarity with between the generation of abnormal returns.

Furthermore, the evaluation also indicate that error and abnormal returns is a relatively higher

for companies providing good earnings announcement. On the other hand, companies provide

bad on use of announcement have low errors. This is due to the fact that valuation of the

10

Calculation of Test Stats for Average Abnormal Returns

Company Name Steyx Steyx Squared

Hikma Pharmaceutical 0.017386968 0.000302307

Murray Intnl Trust 0.007943647 6.31015E-05

Phoenix Grp Hldgs 0.007989165 6.38268E-05

RIVERSTONE ENERGY LD 0.010552464 0.000111354

Ultra Electronics Holdings plc 0.011360017 0.00012905

Sum of the Squared Steyx 0.000669639

Average of Steyx Squared 0.000133928

Square root of the Average Steyx 0.011572722

The abnormal returns are mainly evaluated in the above table, which is for the

companies that have bad earnings announcements. From the valuation, Square root of the

Average Steyx is at the levels of 0.000133928, which is used to derive the T-Test of

abnormal returns. Moreover, the Sum of the Squared Steyx is at 0.000669639, while Average

of Steyx Squared is at 0.000133928. This relatively indicates the overall normal return

deviation which will be provided buy the stocks. The relevant error in the abnormal returns

could be used by investors to identify the share price movement of a company, which would

help in improving their investment return.

From the evaluation, companies providing both good earnings announcement and bad

earnings announcement has similarity with between the generation of abnormal returns.

Furthermore, the evaluation also indicate that error and abnormal returns is a relatively higher

for companies providing good earnings announcement. On the other hand, companies provide

bad on use of announcement have low errors. This is due to the fact that valuation of the

ADVANCED CORPORATE REPORTING

11

company with increase profitability is not easy to comprehend by the investors. Nevertheless,

CAAR of companies having good earnings announcement is a relatively higher in

comparison to the companies having bad earnings announcement. In addition, it is due to the

impact of shareholders sentiments, which derives the actual value of the stock. the companies

provide an expected return, which will be achieved in the fiscal year (Efendi, Park and Smith

2014). However, the non-completion of the projected returns would result in drastic changes

in the share price of the company. Therefore, the good earnings announcement indicated a

more valuation for the company, which increased the chances of abnormal returns and errors.

Though, valuation of bad earnings announcement is effectively conducted by investors,

where the abnormal returns are high.

Conclusion:

From the evaluation of assessment impact of earnings announcement is evaluated,

which might allow investors to obtain abnormal gains from investment. devaluation of good

and bad awnings announcement is conducted within the assessment, which helps in deriving

the chances of error and abnormal returns provided from investment. Furthermore, the use of

statistical tool mainly indicated that abnormal returns are achieved during the announcement

of earnings that is conducted by companies. In addition, the abnormal returns are relatively

positive if news is good, while it is negative during bad announcements. Additionally, the

imperial research is being defected in the assessment, which the mechanism of abnormal

returns during positive earnings announcement. Moreover, the error during the bad earnings

announcement is relatively low, as investors would anticipate the value negative

announcement.

11

company with increase profitability is not easy to comprehend by the investors. Nevertheless,

CAAR of companies having good earnings announcement is a relatively higher in

comparison to the companies having bad earnings announcement. In addition, it is due to the

impact of shareholders sentiments, which derives the actual value of the stock. the companies

provide an expected return, which will be achieved in the fiscal year (Efendi, Park and Smith

2014). However, the non-completion of the projected returns would result in drastic changes

in the share price of the company. Therefore, the good earnings announcement indicated a

more valuation for the company, which increased the chances of abnormal returns and errors.

Though, valuation of bad earnings announcement is effectively conducted by investors,

where the abnormal returns are high.

Conclusion:

From the evaluation of assessment impact of earnings announcement is evaluated,

which might allow investors to obtain abnormal gains from investment. devaluation of good

and bad awnings announcement is conducted within the assessment, which helps in deriving

the chances of error and abnormal returns provided from investment. Furthermore, the use of

statistical tool mainly indicated that abnormal returns are achieved during the announcement

of earnings that is conducted by companies. In addition, the abnormal returns are relatively

positive if news is good, while it is negative during bad announcements. Additionally, the

imperial research is being defected in the assessment, which the mechanism of abnormal

returns during positive earnings announcement. Moreover, the error during the bad earnings

announcement is relatively low, as investors would anticipate the value negative

announcement.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.