UMACTF-15-M: Advanced Corporate Reporting in Financial Strategy

VerifiedAdded on 2023/06/18

|8

|1872

|361

Report

AI Summary

This document presents solutions to questions related to advanced corporate reporting, covering topics such as consolidated statements of financial position, fair value accounting, hedge effectiveness, and the role of financial statements from the perspective of equity and debt stakeholders. It includes calculations for goodwill, non-controlling interest, and retained earnings, along with discussions on the advantages and disadvantages of fair value accounting. The report also addresses the impact of hedge effectiveness under IFRS 9 and provides insights into investment valuation and inventory consolidation. Desklib is your go-to platform for accessing a wide range of study resources, including past papers and solved assignments to support your academic journey.

ADVANCED CORPORATE

REPORTING

REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

QUESTION 1...................................................................................................................................3

QUESTION 4...................................................................................................................................4

a)..................................................................................................................................................4

b)..................................................................................................................................................5

c)..................................................................................................................................................5

Question 5........................................................................................................................................6

a) .................................................................................................................................................6

b)..................................................................................................................................................7

c)..................................................................................................................................................7

REFERENCES................................................................................................................................8

QUESTION 1...................................................................................................................................3

QUESTION 4...................................................................................................................................4

a)..................................................................................................................................................4

b)..................................................................................................................................................5

c)..................................................................................................................................................5

Question 5........................................................................................................................................6

a) .................................................................................................................................................6

b)..................................................................................................................................................7

c)..................................................................................................................................................7

REFERENCES................................................................................................................................8

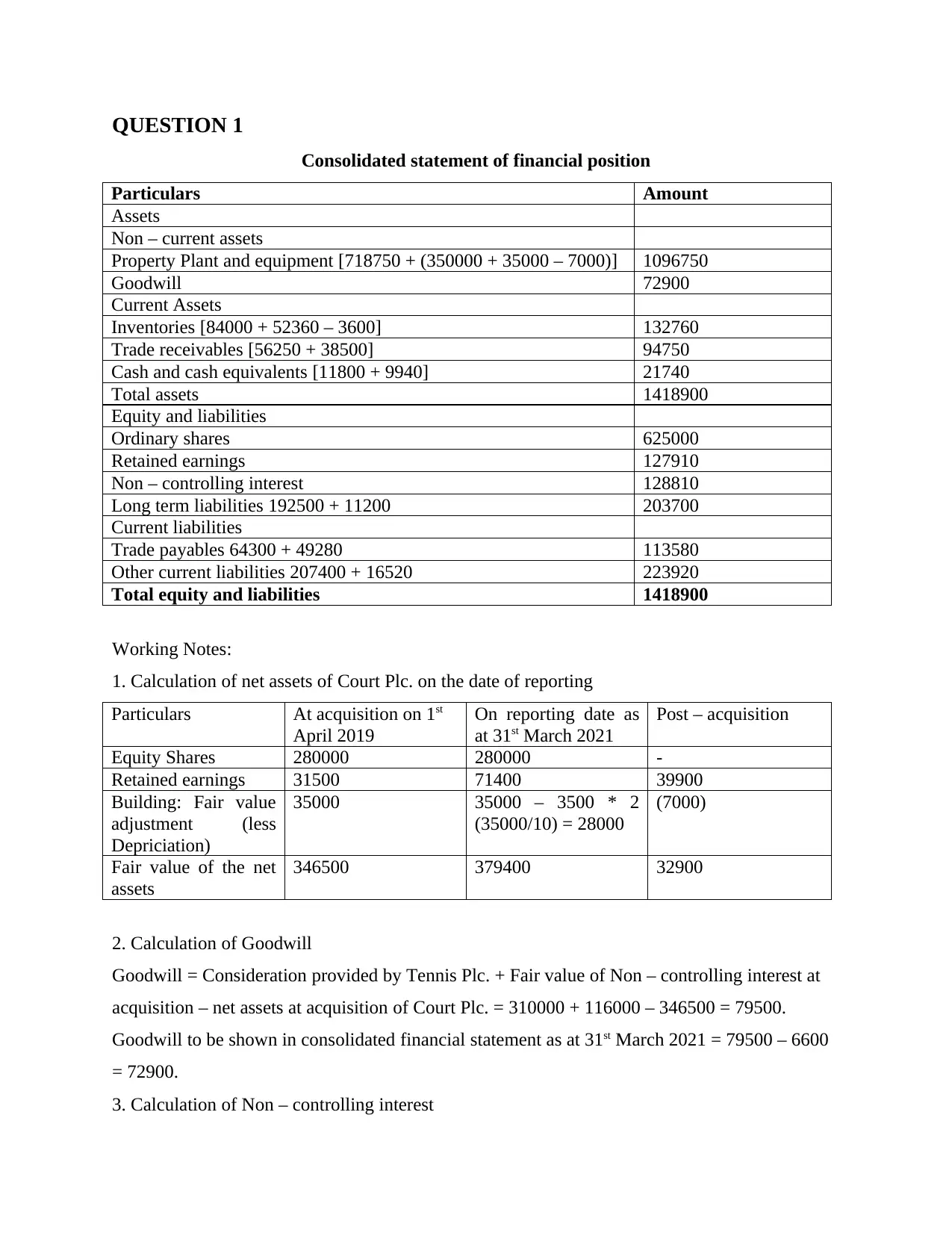

QUESTION 1

Consolidated statement of financial position

Particulars Amount

Assets

Non – current assets

Property Plant and equipment [718750 + (350000 + 35000 – 7000)] 1096750

Goodwill 72900

Current Assets

Inventories [84000 + 52360 – 3600] 132760

Trade receivables [56250 + 38500] 94750

Cash and cash equivalents [11800 + 9940] 21740

Total assets 1418900

Equity and liabilities

Ordinary shares 625000

Retained earnings 127910

Non – controlling interest 128810

Long term liabilities 192500 + 11200 203700

Current liabilities

Trade payables 64300 + 49280 113580

Other current liabilities 207400 + 16520 223920

Total equity and liabilities 1418900

Working Notes:

1. Calculation of net assets of Court Plc. on the date of reporting

Particulars At acquisition on 1st

April 2019

On reporting date as

at 31st March 2021

Post – acquisition

Equity Shares 280000 280000 -

Retained earnings 31500 71400 39900

Building: Fair value

adjustment (less

Depriciation)

35000 35000 – 3500 * 2

(35000/10) = 28000

(7000)

Fair value of the net

assets

346500 379400 32900

2. Calculation of Goodwill

Goodwill = Consideration provided by Tennis Plc. + Fair value of Non – controlling interest at

acquisition – net assets at acquisition of Court Plc. = 310000 + 116000 – 346500 = 79500.

Goodwill to be shown in consolidated financial statement as at 31st March 2021 = 79500 – 6600

= 72900.

3. Calculation of Non – controlling interest

Consolidated statement of financial position

Particulars Amount

Assets

Non – current assets

Property Plant and equipment [718750 + (350000 + 35000 – 7000)] 1096750

Goodwill 72900

Current Assets

Inventories [84000 + 52360 – 3600] 132760

Trade receivables [56250 + 38500] 94750

Cash and cash equivalents [11800 + 9940] 21740

Total assets 1418900

Equity and liabilities

Ordinary shares 625000

Retained earnings 127910

Non – controlling interest 128810

Long term liabilities 192500 + 11200 203700

Current liabilities

Trade payables 64300 + 49280 113580

Other current liabilities 207400 + 16520 223920

Total equity and liabilities 1418900

Working Notes:

1. Calculation of net assets of Court Plc. on the date of reporting

Particulars At acquisition on 1st

April 2019

On reporting date as

at 31st March 2021

Post – acquisition

Equity Shares 280000 280000 -

Retained earnings 31500 71400 39900

Building: Fair value

adjustment (less

Depriciation)

35000 35000 – 3500 * 2

(35000/10) = 28000

(7000)

Fair value of the net

assets

346500 379400 32900

2. Calculation of Goodwill

Goodwill = Consideration provided by Tennis Plc. + Fair value of Non – controlling interest at

acquisition – net assets at acquisition of Court Plc. = 310000 + 116000 – 346500 = 79500.

Goodwill to be shown in consolidated financial statement as at 31st March 2021 = 79500 – 6600

= 72900.

3. Calculation of Non – controlling interest

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= Non – Controlling interest at acquisition + 30% Share of post – Acquisition profit – 30% Share

of Impaired goodwill = 116000 + 9870 (30% of 32900) – 1980 (30% of 6600) = 127850

4. Calculation of retained earnings of Tennis Plc.

Retained earnings on the date of acquisition + 70% of the post – acquisition profit – 70 of

goodwill impaired – unrealized profit = 114000 + 23030 (70% of 32900) – 4620 (70% of 6600)

– (22500 * 80% * 20%) = 114000 + 23030 – 4620 – 3600 = 128810.

QUESTION 4

a)

fair value accounting limits the organizations ability to potentially manipulate the net income

while increasing assets and decreasing liabilities. It provides several kinds of advantages and

disadvantages which are crucial to highlight in order to have proper knowledge regarding the

same.

There are different kinds of advantages which si essential to highlight in order to make

proper evaluation and implementation of same. This provides assistance in gaining an accurate

information by removing the discrepancies. The measurement of true income can be ascertained

by applying this particular method of accounting . Fair value approach enables to reflect the final

net income numbers so that suitable course of action can be taken. It basically avoids making

changes that can influence gain & loss of organization. It is usually cope up with standard of

accounting instead of historical cost value that are not accurate after long period of time. It

provides a method of survival in difficult economy by giving emphasis on fair practices.

With help of fair value accounting firm can get several kinds of drawback which require to

focus in order to make proper discussion. It can create large swings that can happen several

times in year which fluctuate and volatile assets that leads to create in income that is perfectly

not accurate according to the both longer and short term picture. It basically leads to create the

dissatisfaction among the investors and tend to impact the performance of organization by

affecting its liquidity & sustainability (Abernathy and et.al., 2019). These mentioned courses

largely impact fair value accounting on analyst forecast accuracy. The reason behind is that it

measures the overall quality of financial disclosure. It provides assistance in gaining significant

knowledge to forecast the proper position of company in turn better decision can be taken for

of Impaired goodwill = 116000 + 9870 (30% of 32900) – 1980 (30% of 6600) = 127850

4. Calculation of retained earnings of Tennis Plc.

Retained earnings on the date of acquisition + 70% of the post – acquisition profit – 70 of

goodwill impaired – unrealized profit = 114000 + 23030 (70% of 32900) – 4620 (70% of 6600)

– (22500 * 80% * 20%) = 114000 + 23030 – 4620 – 3600 = 128810.

QUESTION 4

a)

fair value accounting limits the organizations ability to potentially manipulate the net income

while increasing assets and decreasing liabilities. It provides several kinds of advantages and

disadvantages which are crucial to highlight in order to have proper knowledge regarding the

same.

There are different kinds of advantages which si essential to highlight in order to make

proper evaluation and implementation of same. This provides assistance in gaining an accurate

information by removing the discrepancies. The measurement of true income can be ascertained

by applying this particular method of accounting . Fair value approach enables to reflect the final

net income numbers so that suitable course of action can be taken. It basically avoids making

changes that can influence gain & loss of organization. It is usually cope up with standard of

accounting instead of historical cost value that are not accurate after long period of time. It

provides a method of survival in difficult economy by giving emphasis on fair practices.

With help of fair value accounting firm can get several kinds of drawback which require to

focus in order to make proper discussion. It can create large swings that can happen several

times in year which fluctuate and volatile assets that leads to create in income that is perfectly

not accurate according to the both longer and short term picture. It basically leads to create the

dissatisfaction among the investors and tend to impact the performance of organization by

affecting its liquidity & sustainability (Abernathy and et.al., 2019). These mentioned courses

largely impact fair value accounting on analyst forecast accuracy. The reason behind is that it

measures the overall quality of financial disclosure. It provides assistance in gaining significant

knowledge to forecast the proper position of company in turn better decision can be taken for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

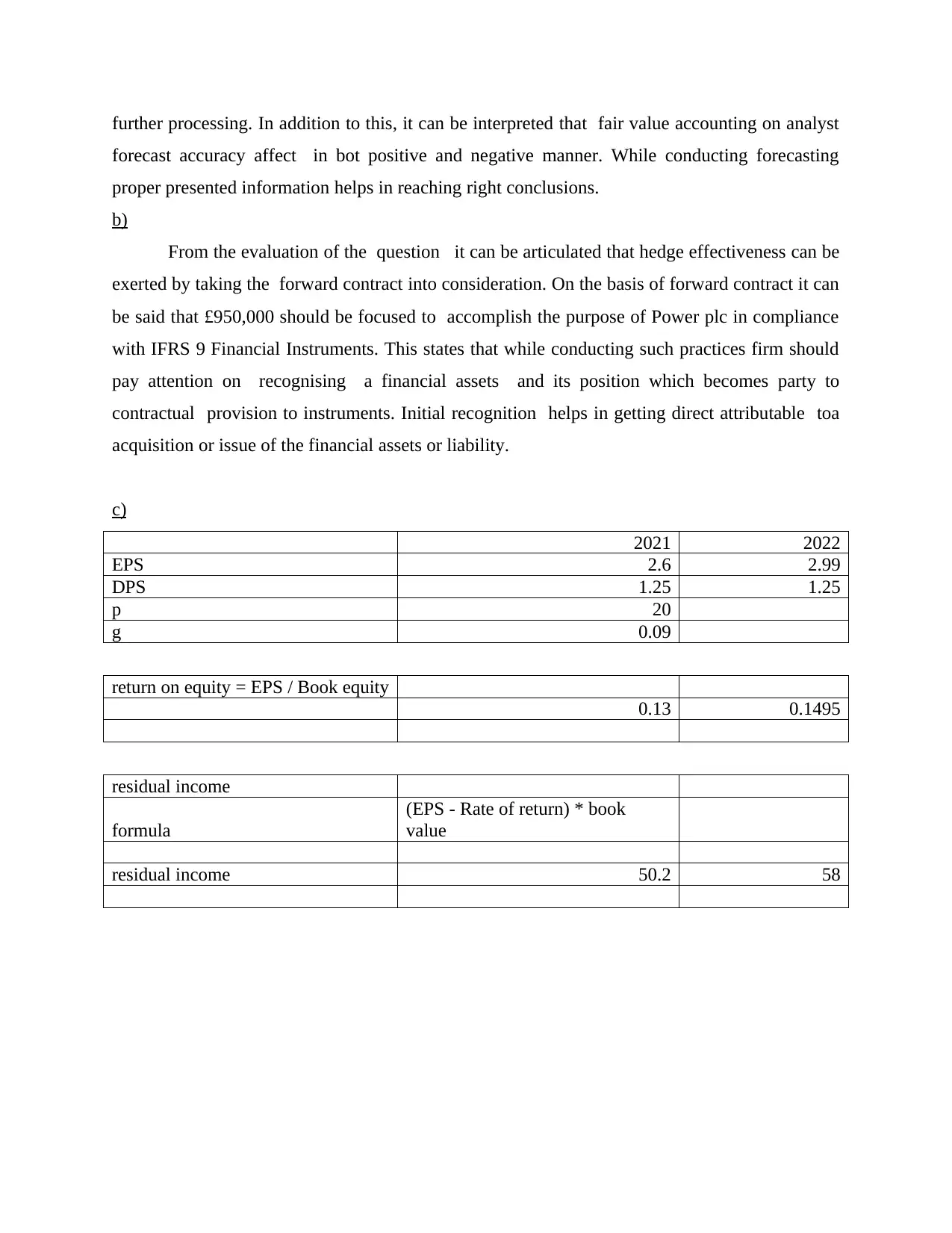

further processing. In addition to this, it can be interpreted that fair value accounting on analyst

forecast accuracy affect in bot positive and negative manner. While conducting forecasting

proper presented information helps in reaching right conclusions.

b)

From the evaluation of the question it can be articulated that hedge effectiveness can be

exerted by taking the forward contract into consideration. On the basis of forward contract it can

be said that £950,000 should be focused to accomplish the purpose of Power plc in compliance

with IFRS 9 Financial Instruments. This states that while conducting such practices firm should

pay attention on recognising a financial assets and its position which becomes party to

contractual provision to instruments. Initial recognition helps in getting direct attributable toa

acquisition or issue of the financial assets or liability.

c)

2021 2022

EPS 2.6 2.99

DPS 1.25 1.25

p 20

g 0.09

return on equity = EPS / Book equity

0.13 0.1495

residual income

formula

(EPS - Rate of return) * book

value

residual income 50.2 58

forecast accuracy affect in bot positive and negative manner. While conducting forecasting

proper presented information helps in reaching right conclusions.

b)

From the evaluation of the question it can be articulated that hedge effectiveness can be

exerted by taking the forward contract into consideration. On the basis of forward contract it can

be said that £950,000 should be focused to accomplish the purpose of Power plc in compliance

with IFRS 9 Financial Instruments. This states that while conducting such practices firm should

pay attention on recognising a financial assets and its position which becomes party to

contractual provision to instruments. Initial recognition helps in getting direct attributable toa

acquisition or issue of the financial assets or liability.

c)

2021 2022

EPS 2.6 2.99

DPS 1.25 1.25

p 20

g 0.09

return on equity = EPS / Book equity

0.13 0.1495

residual income

formula

(EPS - Rate of return) * book

value

residual income 50.2 58

QUESTION 5

a)

Financial statement play important role in providing the critical information to different

kinds of stakeholders. There are two types of stakeholder in organization which includes equity

and debt and both have distinct manner of viewing company's financial position. As per the

view of Dudycz and Praźników (2020) debt providers usually give emphasis on the aspects that

can affect the interest on fund provided by them. The main reason behind evaluation is to

ascertain the components that can influence firm's ability to pay all loaned funds and related

interest charges. The lenders of organization largely pay attention on income statement to view

the profitability with the intention to assess capability to incur the expenses regarding interest.

Lower profitability indicates the poor financial health. On the other side Mora and et.al., (2019)

depicted that This is essential to signify importance regarding the solvency and insolvent

position to make proper evaluation that their provided fund will be provided back or not it

provides assistance in making proper decision in respect to period of collection by lenders via

analysing company's transaction with suppliers, financial institutions, etc to determine

credibility & trustworthiness.

In the opinion of Monahan (2018) equity investors are crucial part of organization

which largely contributes in achieving the success by maintaining proper level of liquidity for

processing. Financial statement are sued by equity investors to have proper information

regarding revenue, expenses, profitability. Enterprise publishes the financial statement like

cash flow, income statement, balance sheet, etc so that investors can properly gain insights

about the company internal processing to assess its financial growth & development. In against

to this, Robinson (2020) articulated that equity investor large pay attention on information

published by enterprise to get data regarding its cost structure, loaned funds, etc for making

evaluation what are the profit margins so that higher level of profits can be attained. In addition

to this, account receivables & payables are invested to identify its potential growth for having

stable working environment. Demand of products, supplying capacity, technological up

gradation are evaluated by investors to get longer sustainability via getting information from

financials statement.

a)

Financial statement play important role in providing the critical information to different

kinds of stakeholders. There are two types of stakeholder in organization which includes equity

and debt and both have distinct manner of viewing company's financial position. As per the

view of Dudycz and Praźników (2020) debt providers usually give emphasis on the aspects that

can affect the interest on fund provided by them. The main reason behind evaluation is to

ascertain the components that can influence firm's ability to pay all loaned funds and related

interest charges. The lenders of organization largely pay attention on income statement to view

the profitability with the intention to assess capability to incur the expenses regarding interest.

Lower profitability indicates the poor financial health. On the other side Mora and et.al., (2019)

depicted that This is essential to signify importance regarding the solvency and insolvent

position to make proper evaluation that their provided fund will be provided back or not it

provides assistance in making proper decision in respect to period of collection by lenders via

analysing company's transaction with suppliers, financial institutions, etc to determine

credibility & trustworthiness.

In the opinion of Monahan (2018) equity investors are crucial part of organization

which largely contributes in achieving the success by maintaining proper level of liquidity for

processing. Financial statement are sued by equity investors to have proper information

regarding revenue, expenses, profitability. Enterprise publishes the financial statement like

cash flow, income statement, balance sheet, etc so that investors can properly gain insights

about the company internal processing to assess its financial growth & development. In against

to this, Robinson (2020) articulated that equity investor large pay attention on information

published by enterprise to get data regarding its cost structure, loaned funds, etc for making

evaluation what are the profit margins so that higher level of profits can be attained. In addition

to this, account receivables & payables are invested to identify its potential growth for having

stable working environment. Demand of products, supplying capacity, technological up

gradation are evaluated by investors to get longer sustainability via getting information from

financials statement.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

b)

As per the IAS 28, the value of investment recognized in the consolidated financial statement of

Road Plc would be equivalent to the amount paid in the form of consideration to the subsidiary

company towards acquiring the shareholding in it. In the present case the value of investment

would be 2350000, which the Road Plc. has paid to

Bridge Plc. for acquiring 35% of its ordinary shares.

For calculating the inventory to be shown in the consolidated financial statement, the amount of

inventory would be equivalent to the unsold inventory remain with the Road Plc. at cost.

Profit earned by Bridge Plc. on transferring inventory to Road Plc. = 650000 – 520000 = 130000.

% of profit = 130000 /520000 *100 = 25%.

Inventory to be shown in the consolidated financial statement

= 650000 * 85% * 75% (at

cost) = 552500 * 75% = 414375.

c)

i)

Historical cost is the transaction price or the acquisition value at which the assets was

acquired. This is globally accepted value which is utilized to record property and plant,

equipment, etc. Fair value is actual worth of assets as per the market trend prevailing in the

current time. Impairment is always calculated on a fair value basis which are needed to

disclosed in the balance sheet. Fair value is complex as compared to the historical worth as it

requires to focus on various factor affecting valuation of assets. These are the basis difference

between these as per the 2018 IASB Conceptual Framework categorises.

ii)

IFRS 5 helsp in specifying the treatment for assets while indulging into the transactions

of making sale. The specified company can sell the building at its fair value by taking the

instructions given by IFRS 5 which articulates that non current asset held for sale by including

the deferred tax assets, employees benefits, financial assets, financials assets, etc (Seifzadeh, M

and et.al., 2020). continuous measurements by having considering these crucial factors in turn

better functioning can be attained. On the basis of this it can be articulated that carrying amount

for fair value less cost to distribute for measuring assets held fro sale.

As per the IAS 28, the value of investment recognized in the consolidated financial statement of

Road Plc would be equivalent to the amount paid in the form of consideration to the subsidiary

company towards acquiring the shareholding in it. In the present case the value of investment

would be 2350000, which the Road Plc. has paid to

Bridge Plc. for acquiring 35% of its ordinary shares.

For calculating the inventory to be shown in the consolidated financial statement, the amount of

inventory would be equivalent to the unsold inventory remain with the Road Plc. at cost.

Profit earned by Bridge Plc. on transferring inventory to Road Plc. = 650000 – 520000 = 130000.

% of profit = 130000 /520000 *100 = 25%.

Inventory to be shown in the consolidated financial statement

= 650000 * 85% * 75% (at

cost) = 552500 * 75% = 414375.

c)

i)

Historical cost is the transaction price or the acquisition value at which the assets was

acquired. This is globally accepted value which is utilized to record property and plant,

equipment, etc. Fair value is actual worth of assets as per the market trend prevailing in the

current time. Impairment is always calculated on a fair value basis which are needed to

disclosed in the balance sheet. Fair value is complex as compared to the historical worth as it

requires to focus on various factor affecting valuation of assets. These are the basis difference

between these as per the 2018 IASB Conceptual Framework categorises.

ii)

IFRS 5 helsp in specifying the treatment for assets while indulging into the transactions

of making sale. The specified company can sell the building at its fair value by taking the

instructions given by IFRS 5 which articulates that non current asset held for sale by including

the deferred tax assets, employees benefits, financial assets, financials assets, etc (Seifzadeh, M

and et.al., 2020). continuous measurements by having considering these crucial factors in turn

better functioning can be attained. On the basis of this it can be articulated that carrying amount

for fair value less cost to distribute for measuring assets held fro sale.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Abernathy, J.L and et.al., 2019. Financial statement footnote readability and corporate audit

outcomes. Auditing: A Journal of Practice & Theory. 38(2). pp.1-26.

Dudycz, T. and Praźników, J., 2020. Does the mark-to-model fair value measure make assets

impairment noisy?: A literature review. Sustainability. 12(4). p.1504.

Monahan, S. J., 2018. Financial statement analysis and earnings forecasting. Foundations and

Trends® in Accounting. 12(2). pp.105-215.

Mora, A. and et.al., 2019. Fair value accounting: the eternal debate–AinE EAA Symposium,

May 2018. Accounting in Europe. 16(3). pp.237-255.

Robinson, T. R., 2020. International financial statement analysis. John Wiley & Sons.

Seifzadeh, M and et.al., 2020. The relationship between management characteristics and

financial statement readability. EuroMed Journal of Business.

Books and journals

Abernathy, J.L and et.al., 2019. Financial statement footnote readability and corporate audit

outcomes. Auditing: A Journal of Practice & Theory. 38(2). pp.1-26.

Dudycz, T. and Praźników, J., 2020. Does the mark-to-model fair value measure make assets

impairment noisy?: A literature review. Sustainability. 12(4). p.1504.

Monahan, S. J., 2018. Financial statement analysis and earnings forecasting. Foundations and

Trends® in Accounting. 12(2). pp.105-215.

Mora, A. and et.al., 2019. Fair value accounting: the eternal debate–AinE EAA Symposium,

May 2018. Accounting in Europe. 16(3). pp.237-255.

Robinson, T. R., 2020. International financial statement analysis. John Wiley & Sons.

Seifzadeh, M and et.al., 2020. The relationship between management characteristics and

financial statement readability. EuroMed Journal of Business.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.