Advanced Diploma of Program Management: Financial Management Portfolio

VerifiedAdded on 2022/08/12

|25

|6836

|21

Portfolio

AI Summary

This portfolio assignment assesses a student's understanding of financial management principles within the context of the BSB61218 Advanced Diploma of Program Management, specifically the BSBFIM601 unit. The assessment is divided into three parts: written responses (25%), a project simulating a work organization (65%), and a presentation on Australian Hardware's financial analysis (10%). Part A requires answering questions on financial management systems, budgeting, budget implementation, financial probity, and relevant legislation. Part B involves applying financial management skills to a simulated business environment, including budgeting, forecasting, and resource allocation. Part C requires analyzing and presenting financial data for Australian Hardware. The assessment evaluates the student's ability to review financial data, prepare budgets, manage resources, and report on financial activities, ensuring compliance with organizational and statutory requirements. The portfolio also requires the student to demonstrate their understanding of financial probity and relevant legislation. The aim is to assess the student's comprehensive understanding of financial management concepts and their practical application in a business context.

T-1.8.1_v3

Details of Assessment

Term and Year Time allowed 7 Weeks

Assessment No 1 Assessment Weighting 100%

Assessment Type Portfolio

Due Date Week 7 Room

Details of Subject

Qualification BSB61218 Advanced Diploma of Program Management

Subject Name Financial Management

Details of Unit(s) of competency

Unit Code (s) and

Names BSBFIM601 Manage finances

Details of Student

Student Name

College Student ID

Student Declaration: I declare that the work submitted is my

own and has not been copied or plagiarised from any person

or source. I acknowledge that I understand the requirements

to complete the assessment tasks. I am also aware of my

right to appeal. The feedback session schedule and

reassessment procedure were explained to me.

Student’s

Signature: ____________________

Date: _____/_____/_________

Details of Assessor

Assessor’s Name

Assessment Outcome

Assessment

Result Competent Not Yet Competent Marks /100

Feedback to Student

Progressive feedback to students, identifying gaps in competency and comments on positive

improvements:

Assessor Declaration: I declare that I have conducted

a fair, valid, reliable and flexible assessment with this

student.

Student attended the feedback session.

Student did not attend the feedback session.

Assessor’s

Signature: ___________________

Date: _____/_____/________

Financial Management, Assessment I v2.0 Last updated on 11/06/2019 by NC Page 1

Details of Assessment

Term and Year Time allowed 7 Weeks

Assessment No 1 Assessment Weighting 100%

Assessment Type Portfolio

Due Date Week 7 Room

Details of Subject

Qualification BSB61218 Advanced Diploma of Program Management

Subject Name Financial Management

Details of Unit(s) of competency

Unit Code (s) and

Names BSBFIM601 Manage finances

Details of Student

Student Name

College Student ID

Student Declaration: I declare that the work submitted is my

own and has not been copied or plagiarised from any person

or source. I acknowledge that I understand the requirements

to complete the assessment tasks. I am also aware of my

right to appeal. The feedback session schedule and

reassessment procedure were explained to me.

Student’s

Signature: ____________________

Date: _____/_____/_________

Details of Assessor

Assessor’s Name

Assessment Outcome

Assessment

Result Competent Not Yet Competent Marks /100

Feedback to Student

Progressive feedback to students, identifying gaps in competency and comments on positive

improvements:

Assessor Declaration: I declare that I have conducted

a fair, valid, reliable and flexible assessment with this

student.

Student attended the feedback session.

Student did not attend the feedback session.

Assessor’s

Signature: ___________________

Date: _____/_____/________

Financial Management, Assessment I v2.0 Last updated on 11/06/2019 by NC Page 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

T-1.8.1_v3

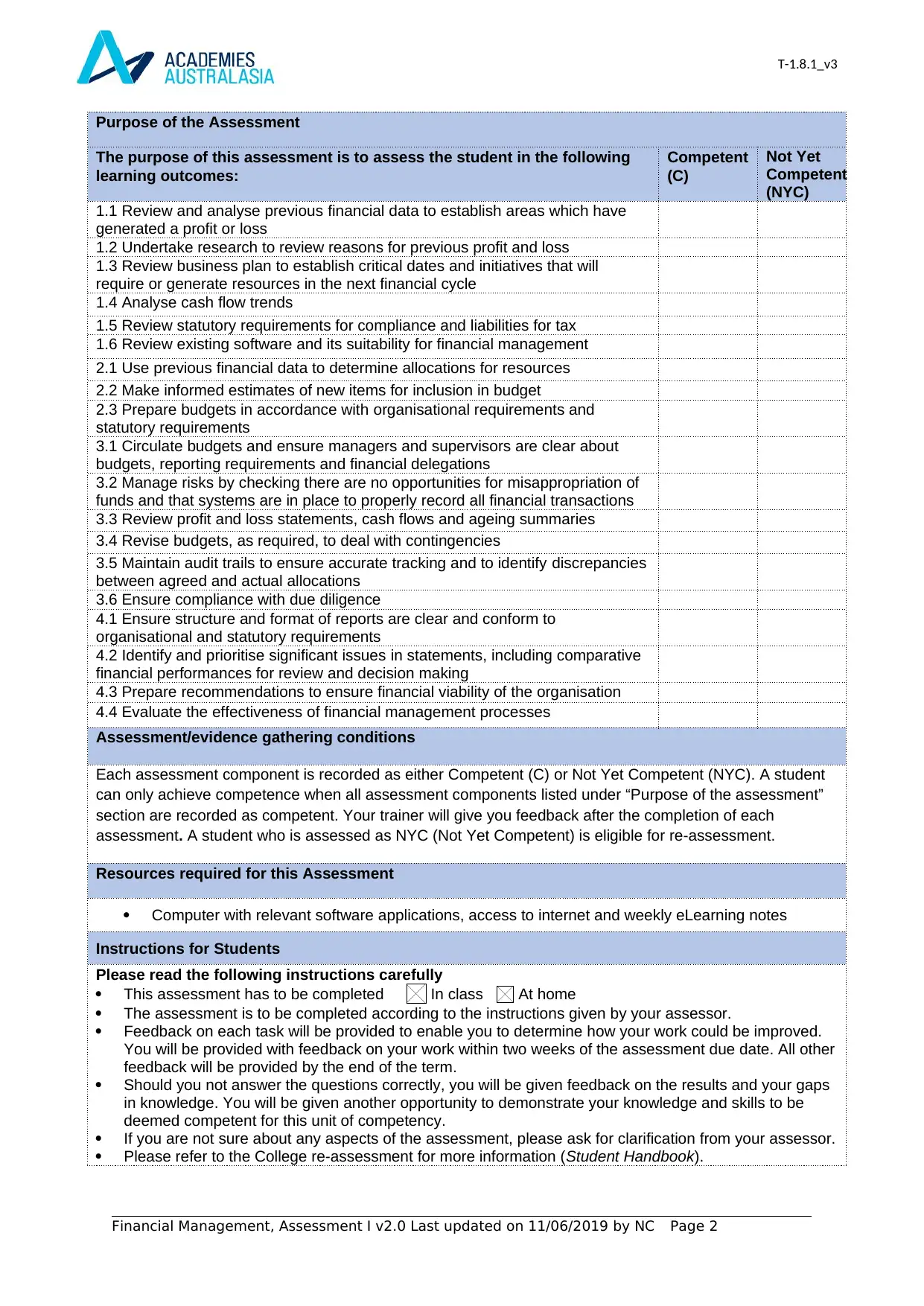

Purpose of the Assessment

The purpose of this assessment is to assess the student in the following

learning outcomes:

Competent

(C)

Not Yet

Competent

(NYC)

1.1 Review and analyse previous financial data to establish areas which have

generated a profit or loss

1.2 Undertake research to review reasons for previous profit and loss

1.3 Review business plan to establish critical dates and initiatives that will

require or generate resources in the next financial cycle

1.4 Analyse cash flow trends

1.5 Review statutory requirements for compliance and liabilities for tax

1.6 Review existing software and its suitability for financial management

2.1 Use previous financial data to determine allocations for resources

2.2 Make informed estimates of new items for inclusion in budget

2.3 Prepare budgets in accordance with organisational requirements and

statutory requirements

3.1 Circulate budgets and ensure managers and supervisors are clear about

budgets, reporting requirements and financial delegations

3.2 Manage risks by checking there are no opportunities for misappropriation of

funds and that systems are in place to properly record all financial transactions

3.3 Review profit and loss statements, cash flows and ageing summaries

3.4 Revise budgets, as required, to deal with contingencies

3.5 Maintain audit trails to ensure accurate tracking and to identify discrepancies

between agreed and actual allocations

3.6 Ensure compliance with due diligence

4.1 Ensure structure and format of reports are clear and conform to

organisational and statutory requirements

4.2 Identify and prioritise significant issues in statements, including comparative

financial performances for review and decision making

4.3 Prepare recommendations to ensure financial viability of the organisation

4.4 Evaluate the effectiveness of financial management processes

Assessment/evidence gathering conditions

Each assessment component is recorded as either Competent (C) or Not Yet Competent (NYC). A student

can only achieve competence when all assessment components listed under “Purpose of the assessment”

section are recorded as competent. Your trainer will give you feedback after the completion of each

assessment. A student who is assessed as NYC (Not Yet Competent) is eligible for re-assessment.

Resources required for this Assessment

Computer with relevant software applications, access to internet and weekly eLearning notes

Instructions for Students

Please read the following instructions carefully

This assessment has to be completed In class At home

The assessment is to be completed according to the instructions given by your assessor.

Feedback on each task will be provided to enable you to determine how your work could be improved.

You will be provided with feedback on your work within two weeks of the assessment due date. All other

feedback will be provided by the end of the term.

Should you not answer the questions correctly, you will be given feedback on the results and your gaps

in knowledge. You will be given another opportunity to demonstrate your knowledge and skills to be

deemed competent for this unit of competency.

If you are not sure about any aspects of the assessment, please ask for clarification from your assessor.

Please refer to the College re-assessment for more information (Student Handbook).

Financial Management, Assessment I v2.0 Last updated on 11/06/2019 by NC Page 2

Purpose of the Assessment

The purpose of this assessment is to assess the student in the following

learning outcomes:

Competent

(C)

Not Yet

Competent

(NYC)

1.1 Review and analyse previous financial data to establish areas which have

generated a profit or loss

1.2 Undertake research to review reasons for previous profit and loss

1.3 Review business plan to establish critical dates and initiatives that will

require or generate resources in the next financial cycle

1.4 Analyse cash flow trends

1.5 Review statutory requirements for compliance and liabilities for tax

1.6 Review existing software and its suitability for financial management

2.1 Use previous financial data to determine allocations for resources

2.2 Make informed estimates of new items for inclusion in budget

2.3 Prepare budgets in accordance with organisational requirements and

statutory requirements

3.1 Circulate budgets and ensure managers and supervisors are clear about

budgets, reporting requirements and financial delegations

3.2 Manage risks by checking there are no opportunities for misappropriation of

funds and that systems are in place to properly record all financial transactions

3.3 Review profit and loss statements, cash flows and ageing summaries

3.4 Revise budgets, as required, to deal with contingencies

3.5 Maintain audit trails to ensure accurate tracking and to identify discrepancies

between agreed and actual allocations

3.6 Ensure compliance with due diligence

4.1 Ensure structure and format of reports are clear and conform to

organisational and statutory requirements

4.2 Identify and prioritise significant issues in statements, including comparative

financial performances for review and decision making

4.3 Prepare recommendations to ensure financial viability of the organisation

4.4 Evaluate the effectiveness of financial management processes

Assessment/evidence gathering conditions

Each assessment component is recorded as either Competent (C) or Not Yet Competent (NYC). A student

can only achieve competence when all assessment components listed under “Purpose of the assessment”

section are recorded as competent. Your trainer will give you feedback after the completion of each

assessment. A student who is assessed as NYC (Not Yet Competent) is eligible for re-assessment.

Resources required for this Assessment

Computer with relevant software applications, access to internet and weekly eLearning notes

Instructions for Students

Please read the following instructions carefully

This assessment has to be completed In class At home

The assessment is to be completed according to the instructions given by your assessor.

Feedback on each task will be provided to enable you to determine how your work could be improved.

You will be provided with feedback on your work within two weeks of the assessment due date. All other

feedback will be provided by the end of the term.

Should you not answer the questions correctly, you will be given feedback on the results and your gaps

in knowledge. You will be given another opportunity to demonstrate your knowledge and skills to be

deemed competent for this unit of competency.

If you are not sure about any aspects of the assessment, please ask for clarification from your assessor.

Please refer to the College re-assessment for more information (Student Handbook).

Financial Management, Assessment I v2.0 Last updated on 11/06/2019 by NC Page 2

T-1.8.1_v3

ASSESSMENT BRIEF

In this assessment task, you will use your skills and knowledge to undertake budgeting,

financial forecasting and reporting and to allocate and manage resources to achieve the

required outputs for the business unit. You work will also include contributing to financial bids

and estimates, allocating funds, managing budgets and reporting on financial activity.

The assessment is divided into three parts and weight allocations as below:

PART A: WRITTEN REPONSES – 25%

PART B: MANAGE FINANCES PROJECT ON A SIMULATED WORK ORGANISATION – 65%

PART C: PRESENTATION OF AUSTRALIAN HARDWARE FINANCIAL ANALYSIS – 10%

Financial Management, Assessment I v2.0 Last updated on 11/06/2019 by NC Page 3

ASSESSMENT BRIEF

In this assessment task, you will use your skills and knowledge to undertake budgeting,

financial forecasting and reporting and to allocate and manage resources to achieve the

required outputs for the business unit. You work will also include contributing to financial bids

and estimates, allocating funds, managing budgets and reporting on financial activity.

The assessment is divided into three parts and weight allocations as below:

PART A: WRITTEN REPONSES – 25%

PART B: MANAGE FINANCES PROJECT ON A SIMULATED WORK ORGANISATION – 65%

PART C: PRESENTATION OF AUSTRALIAN HARDWARE FINANCIAL ANALYSIS – 10%

Financial Management, Assessment I v2.0 Last updated on 11/06/2019 by NC Page 3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

T-1.8.1_v3

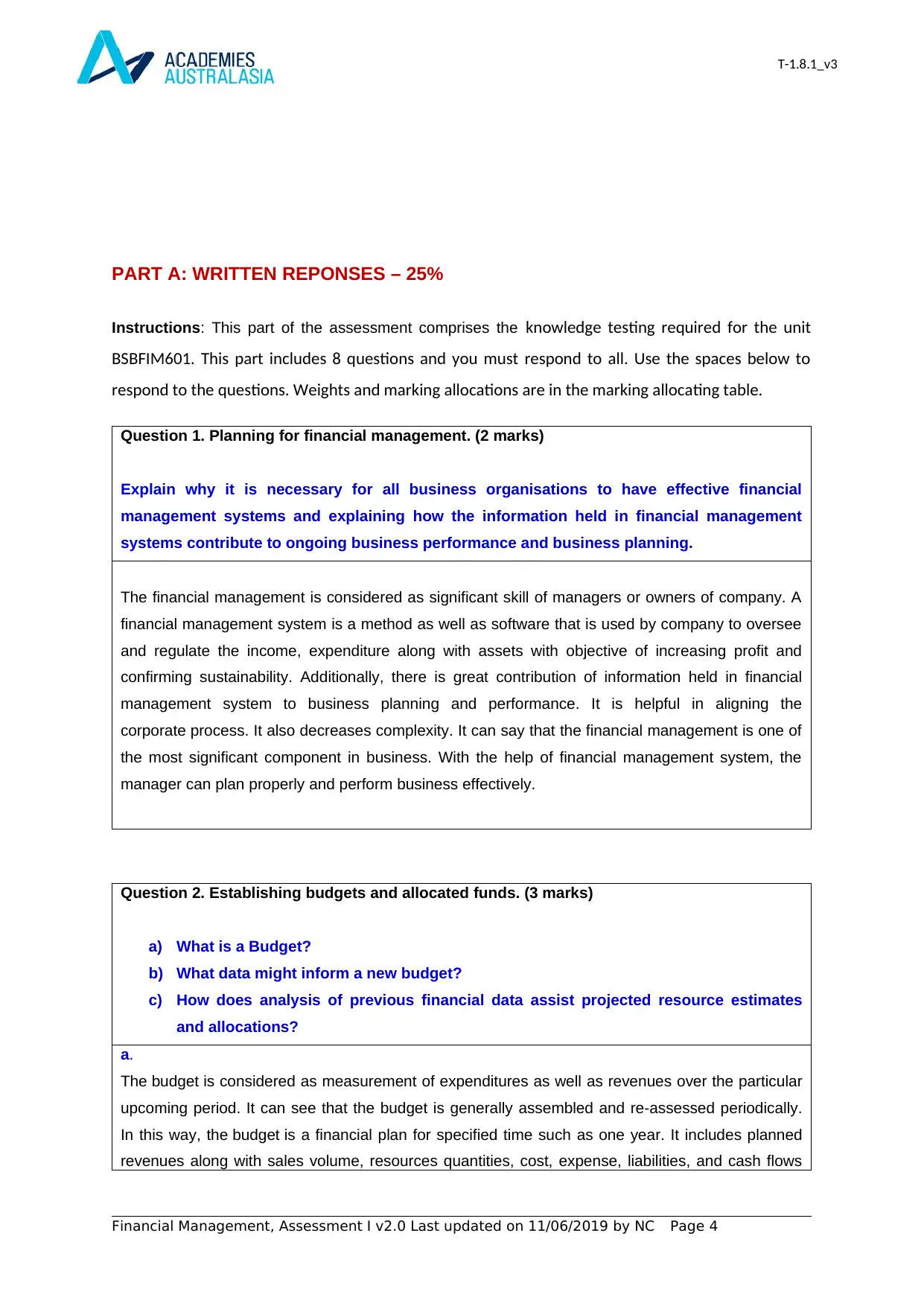

PART A: WRITTEN REPONSES – 25%

Instructions: This part of the assessment comprises the knowledge testing required for the unit

BSBFIM601. This part includes 8 questions and you must respond to all. Use the spaces below to

respond to the questions. Weights and marking allocations are in the marking allocating table.

Question 1. Planning for financial management. (2 marks)

Explain why it is necessary for all business organisations to have effective financial

management systems and explaining how the information held in financial management

systems contribute to ongoing business performance and business planning.

The financial management is considered as significant skill of managers or owners of company. A

financial management system is a method as well as software that is used by company to oversee

and regulate the income, expenditure along with assets with objective of increasing profit and

confirming sustainability. Additionally, there is great contribution of information held in financial

management system to business planning and performance. It is helpful in aligning the

corporate process. It also decreases complexity. It can say that the financial management is one of

the most significant component in business. With the help of financial management system, the

manager can plan properly and perform business effectively.

Question 2. Establishing budgets and allocated funds. (3 marks)

a) What is a Budget?

b) What data might inform a new budget?

c) How does analysis of previous financial data assist projected resource estimates

and allocations?

a.

The budget is considered as measurement of expenditures as well as revenues over the particular

upcoming period. It can see that the budget is generally assembled and re-assessed periodically.

In this way, the budget is a financial plan for specified time such as one year. It includes planned

revenues along with sales volume, resources quantities, cost, expense, liabilities, and cash flows

Financial Management, Assessment I v2.0 Last updated on 11/06/2019 by NC Page 4

PART A: WRITTEN REPONSES – 25%

Instructions: This part of the assessment comprises the knowledge testing required for the unit

BSBFIM601. This part includes 8 questions and you must respond to all. Use the spaces below to

respond to the questions. Weights and marking allocations are in the marking allocating table.

Question 1. Planning for financial management. (2 marks)

Explain why it is necessary for all business organisations to have effective financial

management systems and explaining how the information held in financial management

systems contribute to ongoing business performance and business planning.

The financial management is considered as significant skill of managers or owners of company. A

financial management system is a method as well as software that is used by company to oversee

and regulate the income, expenditure along with assets with objective of increasing profit and

confirming sustainability. Additionally, there is great contribution of information held in financial

management system to business planning and performance. It is helpful in aligning the

corporate process. It also decreases complexity. It can say that the financial management is one of

the most significant component in business. With the help of financial management system, the

manager can plan properly and perform business effectively.

Question 2. Establishing budgets and allocated funds. (3 marks)

a) What is a Budget?

b) What data might inform a new budget?

c) How does analysis of previous financial data assist projected resource estimates

and allocations?

a.

The budget is considered as measurement of expenditures as well as revenues over the particular

upcoming period. It can see that the budget is generally assembled and re-assessed periodically.

In this way, the budget is a financial plan for specified time such as one year. It includes planned

revenues along with sales volume, resources quantities, cost, expense, liabilities, and cash flows

Financial Management, Assessment I v2.0 Last updated on 11/06/2019 by NC Page 4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

T-1.8.1_v3

along with assets. It may include deficit in which expenses are more than income or budget surplus

stating cash for utilisation at the upcoming period.

b.

This is significant to weigh the benefit and cost before requiring resources. It is required to consider

crucial strategies at the time of preparing new strategies. It is essential to use past financial data to

inform the assumptions pricing, competitor, fixed cost, variable cost, analysis, new selling channels

as well as different related issues. In this way, the budget should be merged as well as compared

with others in the entity. So it is essential to consider these data to prepare new budget.

c.

The financial statement is backbone of company. The previous data of financial statement are

helpful in assisting allocation of resources. The financial statements are composed by

Cash flow statement

Balance sheet

Income statement

Value added statement

Report on accumulated profit

Explanatory note

Analytical table

Question 3. Implement Budgets. (4 marks)

a) How do profit and loss statements cash flow and using aging summaries contribute

to new budgets?

b) How can you ensure that managers and supervisors in the organisation understand

the budget and understand their reporting requirements with regard to financial

management?

c) Budgets are used to identify and track discrepancies between agreed and actual

allocations. Explain.

d) How do budgets contribute to analysis of existing financial management

approaches?

a. There is great contribution of P&L and cash flow in making new budgets. The cash flow

eases preparation of new budget by providing that –

There is visibility of financial result

Financial Management, Assessment I v2.0 Last updated on 11/06/2019 by NC Page 5

along with assets. It may include deficit in which expenses are more than income or budget surplus

stating cash for utilisation at the upcoming period.

b.

This is significant to weigh the benefit and cost before requiring resources. It is required to consider

crucial strategies at the time of preparing new strategies. It is essential to use past financial data to

inform the assumptions pricing, competitor, fixed cost, variable cost, analysis, new selling channels

as well as different related issues. In this way, the budget should be merged as well as compared

with others in the entity. So it is essential to consider these data to prepare new budget.

c.

The financial statement is backbone of company. The previous data of financial statement are

helpful in assisting allocation of resources. The financial statements are composed by

Cash flow statement

Balance sheet

Income statement

Value added statement

Report on accumulated profit

Explanatory note

Analytical table

Question 3. Implement Budgets. (4 marks)

a) How do profit and loss statements cash flow and using aging summaries contribute

to new budgets?

b) How can you ensure that managers and supervisors in the organisation understand

the budget and understand their reporting requirements with regard to financial

management?

c) Budgets are used to identify and track discrepancies between agreed and actual

allocations. Explain.

d) How do budgets contribute to analysis of existing financial management

approaches?

a. There is great contribution of P&L and cash flow in making new budgets. The cash flow

eases preparation of new budget by providing that –

There is visibility of financial result

Financial Management, Assessment I v2.0 Last updated on 11/06/2019 by NC Page 5

T-1.8.1_v3

It can state upcoming issues with future working capital.

The main drawback of cash flow is that it has lower amount of data. In addition, there is no

any particular method for the flow.

b. The functions of manager, objectives of business as well as objective reports are helpful in

maintaining the value of company. It is essentially required by supervisors and managers to

have proper understanding about the report as well as updated budgets.

c. The proper formation of budget can be ensured by –

Develop understanding about cost reduction in some accountable areas

Review and control finance

Ensure avaikbikity for the investigation of particular area

Authorise expenses

d. There is great contribution of budget in analysing the current approach of the financial

management. It can say that budget tells about finance as well as operations. It enables

the manager to utilise money in better way.

Question 4. Explain financial probity. (3 marks)

The financial probity refers to the strict obedience to the code of ethics depended on absolute

morality, particularly commercial subjects and beyond judicial needs. The requirement for financial

probity as worker or entity is discussed below -

Officials should perform in ethical manner according to the APS Values

Handle tender members in equal as well as fair way, and ignore rendering one tender member an

inappropriate advantages over other tender member.

Keep secrecy of confidential data of members, including commercially sensitive data as well as

intellectual properties.

Make sure procedure of tender, negotiation, process of assessment, as well as contract

management process is auditable, clear and responsible.

Proactively recognise as well as handle conflict of interest whether real, prospective or apparent

properly and in accordance with needs of judicial policies, involving applicable Victorian Public

Sector code of conduct.

Financial Management, Assessment I v2.0 Last updated on 11/06/2019 by NC Page 6

It can state upcoming issues with future working capital.

The main drawback of cash flow is that it has lower amount of data. In addition, there is no

any particular method for the flow.

b. The functions of manager, objectives of business as well as objective reports are helpful in

maintaining the value of company. It is essentially required by supervisors and managers to

have proper understanding about the report as well as updated budgets.

c. The proper formation of budget can be ensured by –

Develop understanding about cost reduction in some accountable areas

Review and control finance

Ensure avaikbikity for the investigation of particular area

Authorise expenses

d. There is great contribution of budget in analysing the current approach of the financial

management. It can say that budget tells about finance as well as operations. It enables

the manager to utilise money in better way.

Question 4. Explain financial probity. (3 marks)

The financial probity refers to the strict obedience to the code of ethics depended on absolute

morality, particularly commercial subjects and beyond judicial needs. The requirement for financial

probity as worker or entity is discussed below -

Officials should perform in ethical manner according to the APS Values

Handle tender members in equal as well as fair way, and ignore rendering one tender member an

inappropriate advantages over other tender member.

Keep secrecy of confidential data of members, including commercially sensitive data as well as

intellectual properties.

Make sure procedure of tender, negotiation, process of assessment, as well as contract

management process is auditable, clear and responsible.

Proactively recognise as well as handle conflict of interest whether real, prospective or apparent

properly and in accordance with needs of judicial policies, involving applicable Victorian Public

Sector code of conduct.

Financial Management, Assessment I v2.0 Last updated on 11/06/2019 by NC Page 6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

T-1.8.1_v3

Question 5. List at least 10 forms of legislations and conventions (Australian, international

and/or local) that could apply to financial management. (3 marks)

Following are the forms of laws and conventions applied at financial management –

1. Equal Remuneration convention 1951

2. Fair work act 1994

3. Discrimination Convention, 1958

4. Disability Discrimination Act 1992

5. Convention on right of person with disabilities

6. Equal Opportunity Act 1984

7. Occupation Safety and Health Act 1984

8. Privacy act 1998

9. Small Business Fair Dismissal Code

10. Minimum Age convention 1973

11. Fair trading law

12. Australian standards

13. Codes of practice

14. Australian consumer law

Question 6. Personnel working in the financial services division of a company need to

understand and be able to explain principles of accounting and financial systems

(Accounting and Financial Information Systems- AIS and FIS). What are accounting and

financial management systems and how do they assist business operations (2

marks)

The accounting information system is considered as collection, storing and handling of accounting

along with financial information utilised by internal user for reporting data to investor, creditor as

well as taxation authority. AIS combines’ conventional accounting practices like Generally Accepted

Accounting Principles with new sources of IT. The financial function of the enterprise consists in

taking stock of the flows of money and other assets into and out of an organization, ensuring that

its available resources are properly used and that the organization is financially fit. Following are

the elements of accounting system -

Financial Management, Assessment I v2.0 Last updated on 11/06/2019 by NC Page 7

Question 5. List at least 10 forms of legislations and conventions (Australian, international

and/or local) that could apply to financial management. (3 marks)

Following are the forms of laws and conventions applied at financial management –

1. Equal Remuneration convention 1951

2. Fair work act 1994

3. Discrimination Convention, 1958

4. Disability Discrimination Act 1992

5. Convention on right of person with disabilities

6. Equal Opportunity Act 1984

7. Occupation Safety and Health Act 1984

8. Privacy act 1998

9. Small Business Fair Dismissal Code

10. Minimum Age convention 1973

11. Fair trading law

12. Australian standards

13. Codes of practice

14. Australian consumer law

Question 6. Personnel working in the financial services division of a company need to

understand and be able to explain principles of accounting and financial systems

(Accounting and Financial Information Systems- AIS and FIS). What are accounting and

financial management systems and how do they assist business operations (2

marks)

The accounting information system is considered as collection, storing and handling of accounting

along with financial information utilised by internal user for reporting data to investor, creditor as

well as taxation authority. AIS combines’ conventional accounting practices like Generally Accepted

Accounting Principles with new sources of IT. The financial function of the enterprise consists in

taking stock of the flows of money and other assets into and out of an organization, ensuring that

its available resources are properly used and that the organization is financially fit. Following are

the elements of accounting system -

Financial Management, Assessment I v2.0 Last updated on 11/06/2019 by NC Page 7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

T-1.8.1_v3

1. Accounts payable record

2. Accounts receivable record

3. Pay-roll record

4. General ledger

5. Inventory controlling record

Further, financial information system gathers as well as measures financial information utilised for

optimal financial planning and decisions related to forecasting along with results. It can say that it is

used in the conjunction with decisional support system. Additionally, it is also helpful for the

company to get the financial objectives because they utilise minimal amount of means in relation to

prearranged margin of security. Following are financial information system -

1. Working capital report

2. Accounting report

3. Cash flow forecasting

4. Operating as well as capital budget

Question 7. Explain the requirements for each of the following: (3 marks)

a. Goods and Services Tax

b. Company Tax

c. PAYG

a. The goods and services tax is considered as the value-added tax. GST is applied on the

services as well as products sold for local consumption. The goods and services tax is paid

by consumer. However, this is remitted to government through the business selling

services along with products. In this way it can say that goods and services tax has great

contribution in rendering income for government. Goods and services tax is considered as

tax of 10 % on products as well as services, and other products sold in Australia.

b. The company tax is known as corporate tax or corporation tax. The company tax is

considered as direct tax levied by jurisdiction on capital or earning of companies or legal

corporations. Some nations levy this tax at central level. Some nations may impose

company tax at the domestic level or state level. Australian company tax is applicable at

flat rate of 27.5% on the chargeable incomes.

c. PAYG is known as ‘Pay as you go’. It is known as withholding tax that needs a person to

pay incremental amount of the income of business to Australian Taxation Office. This

mechanism includes systematic payment made by workers and different payers, such as

Financial Management, Assessment I v2.0 Last updated on 11/06/2019 by NC Page 8

1. Accounts payable record

2. Accounts receivable record

3. Pay-roll record

4. General ledger

5. Inventory controlling record

Further, financial information system gathers as well as measures financial information utilised for

optimal financial planning and decisions related to forecasting along with results. It can say that it is

used in the conjunction with decisional support system. Additionally, it is also helpful for the

company to get the financial objectives because they utilise minimal amount of means in relation to

prearranged margin of security. Following are financial information system -

1. Working capital report

2. Accounting report

3. Cash flow forecasting

4. Operating as well as capital budget

Question 7. Explain the requirements for each of the following: (3 marks)

a. Goods and Services Tax

b. Company Tax

c. PAYG

a. The goods and services tax is considered as the value-added tax. GST is applied on the

services as well as products sold for local consumption. The goods and services tax is paid

by consumer. However, this is remitted to government through the business selling

services along with products. In this way it can say that goods and services tax has great

contribution in rendering income for government. Goods and services tax is considered as

tax of 10 % on products as well as services, and other products sold in Australia.

b. The company tax is known as corporate tax or corporation tax. The company tax is

considered as direct tax levied by jurisdiction on capital or earning of companies or legal

corporations. Some nations levy this tax at central level. Some nations may impose

company tax at the domestic level or state level. Australian company tax is applicable at

flat rate of 27.5% on the chargeable incomes.

c. PAYG is known as ‘Pay as you go’. It is known as withholding tax that needs a person to

pay incremental amount of the income of business to Australian Taxation Office. This

mechanism includes systematic payment made by workers and different payers, such as

Financial Management, Assessment I v2.0 Last updated on 11/06/2019 by NC Page 8

T-1.8.1_v3

superannuation fund. This is utilised to collect by instalment income tax, Medicare, HELP

repayment, as well as other modes of payment. In this way, PAYG system is helpful in

improving effectiveness because it reduces request from payee for accounting record.

Question 8. Scenario for audit reporting. (5 marks)

You have been asked to act as a project manager to assist with data collection, provide

data, ensure that any other assistance is provided and collaborate with regard to writing the

audit report

During the year the organisation transacted a number of mergers and acquisitions. You

have been asked to pay special attention to the acquisitions and to check the due diligence

processes. You also need to determine whether any changes and adjustments need to be

made to the current budgets.

Explain what all this means and how you will manage the process.

In answering those questions, you will need to also address the following questions:

a. What is an internal audit?

The internal auditing is considered as independent, objective assurance as well as accessing

activity developed to add value to and advance functions of entity. A main function of the internal

audit is to render independent declaration that governance, risk management of company, internal

control procedures are functioning in effective manner. It renders board members along with top

level administration with guarantee that helps them to perform obligations to company as well as

and stakeholder of company.

b. How does it mitigate the risk of management frauds?

Following are five ways to mitigate the risk of management frauds –

1. Review the information

2. Develop proactive communication with workers who did fraud

3. Implement company policies on confidentiality and nondisclosure

4. Create the whistle blower hotline

5. Employ correct person

c. Are there particular statutory requirements that should be followed?

Financial Management, Assessment I v2.0 Last updated on 11/06/2019 by NC Page 9

superannuation fund. This is utilised to collect by instalment income tax, Medicare, HELP

repayment, as well as other modes of payment. In this way, PAYG system is helpful in

improving effectiveness because it reduces request from payee for accounting record.

Question 8. Scenario for audit reporting. (5 marks)

You have been asked to act as a project manager to assist with data collection, provide

data, ensure that any other assistance is provided and collaborate with regard to writing the

audit report

During the year the organisation transacted a number of mergers and acquisitions. You

have been asked to pay special attention to the acquisitions and to check the due diligence

processes. You also need to determine whether any changes and adjustments need to be

made to the current budgets.

Explain what all this means and how you will manage the process.

In answering those questions, you will need to also address the following questions:

a. What is an internal audit?

The internal auditing is considered as independent, objective assurance as well as accessing

activity developed to add value to and advance functions of entity. A main function of the internal

audit is to render independent declaration that governance, risk management of company, internal

control procedures are functioning in effective manner. It renders board members along with top

level administration with guarantee that helps them to perform obligations to company as well as

and stakeholder of company.

b. How does it mitigate the risk of management frauds?

Following are five ways to mitigate the risk of management frauds –

1. Review the information

2. Develop proactive communication with workers who did fraud

3. Implement company policies on confidentiality and nondisclosure

4. Create the whistle blower hotline

5. Employ correct person

c. Are there particular statutory requirements that should be followed?

Financial Management, Assessment I v2.0 Last updated on 11/06/2019 by NC Page 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

T-1.8.1_v3

The company should follow auditing standards. Following are certain auditing standards under

Section 336 of the Corporations Act 2001 -

ASQC 1

Auditing Standard ASQC 1 Quality Control for

Firms that Perform Audits and Reviews of

Financial Reports and Other Financial

Information, Other Assurance Engagements

and Related Services Engagements

ASA 100 Preamble to AUASB Standard

ASA 101 Preamble to Australian Auditing Standards

ASA 102

Compliance with Ethical Requirements when

Performing Audits, Reviews and Other

Assurance Engagements

ASA 200

overall Objectives of the Independent Auditor

and the Conduct of an Audit in Accordance

with Australian Auditing Standards

ASA 210 Agreeing terms of Audit Engagement

ASA 220

Quality Control for an Audit of a Financial

Report and Other Historical Financial

Information

ASA 230 Audit Documentation

ASA 300 Planning an Audit of a Financial Report

ASA 402

Audit Considerations Relating to an Entity

Using a Service Organisation

ASA 500 Audit Evidence

ASA 580 Written Representations

In addition, following requirements are required to review –

1. Registered name of business

2. License to conduct business

3. Federal tax, and local tax (state tax)

4. Business rules and regulations

d. What does due diligence mean in terms of finances and financial reporting?

The due diligence is considered as audit or examination of the potential investments or

products to confirm each data, which may involve review of financial record. In this way,

the due diligence is considered as investigation conducted before taking entry in

agreement or the financial dealing with other contracting person.

Financial Management, Assessment I v2.0 Last updated on 11/06/2019 by NC Page 10

The company should follow auditing standards. Following are certain auditing standards under

Section 336 of the Corporations Act 2001 -

ASQC 1

Auditing Standard ASQC 1 Quality Control for

Firms that Perform Audits and Reviews of

Financial Reports and Other Financial

Information, Other Assurance Engagements

and Related Services Engagements

ASA 100 Preamble to AUASB Standard

ASA 101 Preamble to Australian Auditing Standards

ASA 102

Compliance with Ethical Requirements when

Performing Audits, Reviews and Other

Assurance Engagements

ASA 200

overall Objectives of the Independent Auditor

and the Conduct of an Audit in Accordance

with Australian Auditing Standards

ASA 210 Agreeing terms of Audit Engagement

ASA 220

Quality Control for an Audit of a Financial

Report and Other Historical Financial

Information

ASA 230 Audit Documentation

ASA 300 Planning an Audit of a Financial Report

ASA 402

Audit Considerations Relating to an Entity

Using a Service Organisation

ASA 500 Audit Evidence

ASA 580 Written Representations

In addition, following requirements are required to review –

1. Registered name of business

2. License to conduct business

3. Federal tax, and local tax (state tax)

4. Business rules and regulations

d. What does due diligence mean in terms of finances and financial reporting?

The due diligence is considered as audit or examination of the potential investments or

products to confirm each data, which may involve review of financial record. In this way,

the due diligence is considered as investigation conducted before taking entry in

agreement or the financial dealing with other contracting person.

Financial Management, Assessment I v2.0 Last updated on 11/06/2019 by NC Page 10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

T-1.8.1_v3

e. What reports might be prepared for the ATO?

Following reports may be prepared for ATO –

5. Annual income tax return to report business income

6. PAYG withholding annual report

7. GST annual tax return

8. Taxable payment annual report

9. Business activity statement

PART A: MARKING TABLE (for trainer use only)

The assessor needs to use judgment in providing marks for the tasks based on learner performance.

Question/Task Number Marks Allocated Marks received

Q1 2

Q2 3

Q3 4

Q4 3

Q5 3

Q6 2

Q7 3

Q8 5

Total

Financial Management, Assessment I v2.0 Last updated on 11/06/2019 by NC Page 11

e. What reports might be prepared for the ATO?

Following reports may be prepared for ATO –

5. Annual income tax return to report business income

6. PAYG withholding annual report

7. GST annual tax return

8. Taxable payment annual report

9. Business activity statement

PART A: MARKING TABLE (for trainer use only)

The assessor needs to use judgment in providing marks for the tasks based on learner performance.

Question/Task Number Marks Allocated Marks received

Q1 2

Q2 3

Q3 4

Q4 3

Q5 3

Q6 2

Q7 3

Q8 5

Total

Financial Management, Assessment I v2.0 Last updated on 11/06/2019 by NC Page 11

T-1.8.1_v3

PART B: MANAGE FINANCES PROJECT – 65%

SIMULATED WORK ORGANISATION & BRIEF ON THE FINANCE PROJECT

This is a series of practical and theory activities that will enable you to demonstrate skill and

knowledge – and produce end products suitable for use in the workplace. In this PART, you are

required to work on a finance management project to determine the financial condition for “Australian

Hardware” the simulated case study below. Click on the icon that includes the information on the

Simulated Work Organisation.

CONTEXT

In the simulated organisational context you will assume responsibility as a newly hired finance manger

of the simulated workplace environment who leads a team of finance. Your trainer will act as your

supervisor in this simulated work task. You will be progressively completing all the tasks relating to

planning for financial management; reviewing profit and loss statements; cash flows and aging

summaries; reviewing and revising the budget of this organisation, allocating funds, communicating

with your team and other stakeholders, meet compliance requirements and analysing the

effectiveness of existing financial management by providing your own recommendations.

To demonstrate competency you will need to complete all the tasks assigned to you in relation to your

personal development portfolio.

What is required?

You are required to explore the simulated organisational documents (CoffeeVille) or use your own

workplace documents, analyse the various situations mentioned within the tasks and respond to those

tasks. You are also required to

plan for financial management

read and review profit and loss statements, cash flows and aging summaries

prepare, implement and revise a budget which aligns with the business plan, is based on

research and analysis of previous financial data and cash flow trends, and meets all

compliance requirements

contribute to financial bids and estimates

Financial Management, Assessment I v2.0 Last updated on 11/06/2019 by NC Page 12

PART B: MANAGE FINANCES PROJECT – 65%

SIMULATED WORK ORGANISATION & BRIEF ON THE FINANCE PROJECT

This is a series of practical and theory activities that will enable you to demonstrate skill and

knowledge – and produce end products suitable for use in the workplace. In this PART, you are

required to work on a finance management project to determine the financial condition for “Australian

Hardware” the simulated case study below. Click on the icon that includes the information on the

Simulated Work Organisation.

CONTEXT

In the simulated organisational context you will assume responsibility as a newly hired finance manger

of the simulated workplace environment who leads a team of finance. Your trainer will act as your

supervisor in this simulated work task. You will be progressively completing all the tasks relating to

planning for financial management; reviewing profit and loss statements; cash flows and aging

summaries; reviewing and revising the budget of this organisation, allocating funds, communicating

with your team and other stakeholders, meet compliance requirements and analysing the

effectiveness of existing financial management by providing your own recommendations.

To demonstrate competency you will need to complete all the tasks assigned to you in relation to your

personal development portfolio.

What is required?

You are required to explore the simulated organisational documents (CoffeeVille) or use your own

workplace documents, analyse the various situations mentioned within the tasks and respond to those

tasks. You are also required to

plan for financial management

read and review profit and loss statements, cash flows and aging summaries

prepare, implement and revise a budget which aligns with the business plan, is based on

research and analysis of previous financial data and cash flow trends, and meets all

compliance requirements

contribute to financial bids and estimates

Financial Management, Assessment I v2.0 Last updated on 11/06/2019 by NC Page 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.