Advanced Financial Accounting Report: Japara Healthcare Analysis

VerifiedAdded on 2022/12/29

|9

|2806

|72

Report

AI Summary

This report delves into advanced financial accounting, focusing on key elements of financial reporting. It begins with an introduction to the conceptual framework for accounting, highlighting its nature and benefits, and providing examples from Japara Healthcare Limited, an Australian-based aged care provider. The report then critically discusses whether Japara is a reporting entity, supporting the argument with detailed examples. It further examines the company's revenues and gains, analyzing the benefits of differentiating between them for financial statement users. A significant portion of the report is dedicated to the analysis of Property, Plant, and Equipment (PP&E), including impairment assessments and valuation methods. The report concludes with a comprehensive overview of the financial accounting topics covered, providing valuable insights into financial reporting practices and asset management. This report is a comprehensive resource for students studying advanced financial accounting, offering practical examples and critical analysis of key concepts.

Advanced Financial

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Elements of financial report with relevant examples and critically discuss the nature and the

benefits of the conceptual framework for accounting.................................................................1

2. Identify and critically discuss if allocated company is a reporting entity, provide detailed

and relevant examples and factors to support argument.............................................................3

3. Identify and discuss if allocated company show revenues and gains? In your view, do you

think differentiating revenues and gains is of a benefit to the users of the financial statements?

Explain and provide examples....................................................................................................3

4 Explain and discuss the list of Property, Plant and Equipment, including impairment

assessments in the financial statements and the related notes. How are these assets measured

and valued?..................................................................................................................................4

CONCLUSION ...............................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Elements of financial report with relevant examples and critically discuss the nature and the

benefits of the conceptual framework for accounting.................................................................1

2. Identify and critically discuss if allocated company is a reporting entity, provide detailed

and relevant examples and factors to support argument.............................................................3

3. Identify and discuss if allocated company show revenues and gains? In your view, do you

think differentiating revenues and gains is of a benefit to the users of the financial statements?

Explain and provide examples....................................................................................................3

4 Explain and discuss the list of Property, Plant and Equipment, including impairment

assessments in the financial statements and the related notes. How are these assets measured

and valued?..................................................................................................................................4

CONCLUSION ...............................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION

Advanced financial accounting is studied with financial reporting and business ability

which are applied by the organisations to deal with international business entities. The members

of company who provides assurance about the financial reports and prepare all the financial

statements as per the IFRSs. In this accounting consist of transaction, structure, merger of public

holding companies, changing financial statement designed as foreign and local currencies (Chen

and Komal, 2018). This report based on the Japara healthcare limited. It is a Australian based

company that listed into Australian securities exchange and provide services to aged people. In

this report consist of nature and benefits of conceptual framework for accounting and analysis

allocated entry in detailed manner with examples. Along with identify revenues and gains of

selected organisation and benefits for users of the financial statements. Moreover, make a list of

plant and property from financial statement and measurement of assets.

MAIN BODY

1. Elements of financial report with relevant examples and critically discuss the nature and the

benefits of the conceptual framework for accounting

Japara is one of Australia's leading business that provides and design of residential aged

care where deliver better living standard to elderly Australians. After the analysis of annual

report of company it is getting that company prepare different types of financial statements

prepare by the business to present the actual financial position of business. It supports board of

directors to take right decision for future investments. There are mentioned different elements of

financial report of Japara such as:

Assets: It is categorised into current and non current assets. In the section of current

assets consist of different items such as, in 2019 cash was 31472, trade and other

variables 14640, current tax receivables nil and other assets were 6216. In the other

section of non current assets consist of in the year of 2019 was trade and other

receivables was 2347, property plan and equipment was 787767, intangible assets was

555319 (ÖZCAN, 2019).

In the year 2020, current assets and non current items are some decreased and some are increased

due to flexible situation. In the section of current assets, cash was 48286, trade and other

receivables was 15326, current tax receivables was 1860 and other assets was 3681. In the

1

Advanced financial accounting is studied with financial reporting and business ability

which are applied by the organisations to deal with international business entities. The members

of company who provides assurance about the financial reports and prepare all the financial

statements as per the IFRSs. In this accounting consist of transaction, structure, merger of public

holding companies, changing financial statement designed as foreign and local currencies (Chen

and Komal, 2018). This report based on the Japara healthcare limited. It is a Australian based

company that listed into Australian securities exchange and provide services to aged people. In

this report consist of nature and benefits of conceptual framework for accounting and analysis

allocated entry in detailed manner with examples. Along with identify revenues and gains of

selected organisation and benefits for users of the financial statements. Moreover, make a list of

plant and property from financial statement and measurement of assets.

MAIN BODY

1. Elements of financial report with relevant examples and critically discuss the nature and the

benefits of the conceptual framework for accounting

Japara is one of Australia's leading business that provides and design of residential aged

care where deliver better living standard to elderly Australians. After the analysis of annual

report of company it is getting that company prepare different types of financial statements

prepare by the business to present the actual financial position of business. It supports board of

directors to take right decision for future investments. There are mentioned different elements of

financial report of Japara such as:

Assets: It is categorised into current and non current assets. In the section of current

assets consist of different items such as, in 2019 cash was 31472, trade and other

variables 14640, current tax receivables nil and other assets were 6216. In the other

section of non current assets consist of in the year of 2019 was trade and other

receivables was 2347, property plan and equipment was 787767, intangible assets was

555319 (ÖZCAN, 2019).

In the year 2020, current assets and non current items are some decreased and some are increased

due to flexible situation. In the section of current assets, cash was 48286, trade and other

receivables was 15326, current tax receivables was 1860 and other assets was 3681. In the

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

section of non current assets concentrate on the trade and other receivables was 2574, property,

plant and equipment was 833202 and intangible assets was 265761.

Liabilities: In the year 2020 analysis the current and non current liabilities. In both

sections includes different items such as, trade payable which was 34104, borrowings

was 58250, lease liabilities was 2338 and many others. In non current consist of

borrowings was 180750, employee provisions was 5608 and other financial liabilities was

5039 (Chychyla, Leone and Minutti-Meza, 2019).

Profit & loss: In this statement consist of revenues of company which was 422242 in the

year 2020 and profit before income tax was (292882) and profit for the year was

(292087).

A conceptual framework is defined as a system of ideas and objectives that helps to make

consistency in business and helps to set effective financial standards.

Nature: The nature of conceptual framework to assist in the improvement of potential

activities that based on IFRS and analysis of currently standards by setting out underlying

concepts. Along with it promote harmonisation of accounting regulations and standard use to

reduce the number of errors that occur in set framework.

Benefits: There are mentioned different benefits of conceptual framework which are used

by the Japara healthcare limited:

This framework beneficial to develop and set up established body of concepts and

objectives

It is providing a particular structure for sort out new and emerging practical difficulties of

accounting (Hairston and Brooks, 2019).

To increase comparability among entities financial reports. Along with it helps to leading

to the improvement of accounting standards that are internally consistent with each other.

Enhance financial statement users to understand of financial reporting

It is beneficial to ignore the situation that based on the standards and accounting

problems is identified on basis of having emerged then channeled into standardization.

In this framework setting particular accounting standards on basis of sort out accounting

disputes and do not repeated accounting standards (Ng, 2018).

2

plant and equipment was 833202 and intangible assets was 265761.

Liabilities: In the year 2020 analysis the current and non current liabilities. In both

sections includes different items such as, trade payable which was 34104, borrowings

was 58250, lease liabilities was 2338 and many others. In non current consist of

borrowings was 180750, employee provisions was 5608 and other financial liabilities was

5039 (Chychyla, Leone and Minutti-Meza, 2019).

Profit & loss: In this statement consist of revenues of company which was 422242 in the

year 2020 and profit before income tax was (292882) and profit for the year was

(292087).

A conceptual framework is defined as a system of ideas and objectives that helps to make

consistency in business and helps to set effective financial standards.

Nature: The nature of conceptual framework to assist in the improvement of potential

activities that based on IFRS and analysis of currently standards by setting out underlying

concepts. Along with it promote harmonisation of accounting regulations and standard use to

reduce the number of errors that occur in set framework.

Benefits: There are mentioned different benefits of conceptual framework which are used

by the Japara healthcare limited:

This framework beneficial to develop and set up established body of concepts and

objectives

It is providing a particular structure for sort out new and emerging practical difficulties of

accounting (Hairston and Brooks, 2019).

To increase comparability among entities financial reports. Along with it helps to leading

to the improvement of accounting standards that are internally consistent with each other.

Enhance financial statement users to understand of financial reporting

It is beneficial to ignore the situation that based on the standards and accounting

problems is identified on basis of having emerged then channeled into standardization.

In this framework setting particular accounting standards on basis of sort out accounting

disputes and do not repeated accounting standards (Ng, 2018).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Identify and critically discuss if allocated company is a reporting entity, provide detailed and

relevant examples and factors to support argument

Reporting entity is an entity where expect that users depend on the general purpose report

to analysis the effective financial position and performance of the business. On the basis of

results make effective decisions and collect all the financial report. The Japara healthcare limited

is a reporting entity who depends on the general purpose financial reporting. On the basis of

these purposes company meet with the objectives of management and determining decisions in

regard of the allocation of resources. The company is responsible to maintain all the financial

accounts and contains a record in which specified of particular financial transactions to the

income tax authority (Han, He, Pan and Shi, 2018).

It is reporting entity because it is prepared a GPFR that means Australian accounting

standards applied at the preparation of financial report. Therefore, when an entity is considering

as non entity so that time requires to prepare a special reason of financial report that does not

require to apply all the Australian accounting standards. There are many benefits that occur for

the reporting entity that every reporting framework is addressing all the risk whether all incorrect

Australian securities and investment commission will examine those charges with commission

and breaching the reporting requirements.

For example, Japara prepare different types of financial statements such as., profit and

loss statement, cash flow statements. These are based on the GPFR Australian accounting

standards (Himick and Brivot, 2018).

3. Identify and discuss if allocated company show revenues and gains? In your view, do you

think differentiating revenues and gains is of a benefit to the users of the financial

statements? Explain and provide examples.

The revenues and gains of the company presents the actual financial health and helps in

decision making procedure. For the revenues requires to prepare statement of profit and loss in

which mention all the income and expenses after that get the amount of net gain. There are

analysing five year revenues and gains of the company such as

Particular 2019/20 2018/19 2017/18 2016/17 2015/16

Operating revues 427.5 399.8 373.2 362.2 327.3

Net Gains (Profit) -292.1 16.4 23.3 29.7 30.4

3

relevant examples and factors to support argument

Reporting entity is an entity where expect that users depend on the general purpose report

to analysis the effective financial position and performance of the business. On the basis of

results make effective decisions and collect all the financial report. The Japara healthcare limited

is a reporting entity who depends on the general purpose financial reporting. On the basis of

these purposes company meet with the objectives of management and determining decisions in

regard of the allocation of resources. The company is responsible to maintain all the financial

accounts and contains a record in which specified of particular financial transactions to the

income tax authority (Han, He, Pan and Shi, 2018).

It is reporting entity because it is prepared a GPFR that means Australian accounting

standards applied at the preparation of financial report. Therefore, when an entity is considering

as non entity so that time requires to prepare a special reason of financial report that does not

require to apply all the Australian accounting standards. There are many benefits that occur for

the reporting entity that every reporting framework is addressing all the risk whether all incorrect

Australian securities and investment commission will examine those charges with commission

and breaching the reporting requirements.

For example, Japara prepare different types of financial statements such as., profit and

loss statement, cash flow statements. These are based on the GPFR Australian accounting

standards (Himick and Brivot, 2018).

3. Identify and discuss if allocated company show revenues and gains? In your view, do you

think differentiating revenues and gains is of a benefit to the users of the financial

statements? Explain and provide examples.

The revenues and gains of the company presents the actual financial health and helps in

decision making procedure. For the revenues requires to prepare statement of profit and loss in

which mention all the income and expenses after that get the amount of net gain. There are

analysing five year revenues and gains of the company such as

Particular 2019/20 2018/19 2017/18 2016/17 2015/16

Operating revues 427.5 399.8 373.2 362.2 327.3

Net Gains (Profit) -292.1 16.4 23.3 29.7 30.4

3

As per the above data it has been analysed that company generate different revenues and

gains in every year. The data presenting in increasing manner it means company has effective

financial performance. Net gains of the Japara fall down due to face pandemic situation and it

impacts on the business in direct manner. In the year of 2020 company has 422,242 revenues and

in 2019 have 394937.

Most of the organisations record different items like gains, revenues, expenditure and

losses that record in the income statements. These items are sounding same but it is different in

practice use for gains and revenues. As per the my point of view it is saying that revenues and

gains are differentiated is profit because in revenues includes all taxes and interests that need to

pay. On the other side in gains less taxes, interest that use to present the actual position of the

business. Thus, it is saying that it is right for the accounting users to differentiate of the revenues

and gains (Kozlowski, Issa and Appelbaum, 2018).

Revenue is amount which is generated by the business entity after complementation of

main operating activities like retailer selling merchandise of effective law that providing legal

services. On the other side Gain is defined as outcome of marginal operations like retailer

selling of the old delivery trucks. A gain arise when the cash amount received and it is noticed in

excess manner and referred to as the asset's book value. For example, when an organisation

receives $5000 for old delivery truck and the carry amount noticed at the book value so sales

was $800, the company will have a gain $4200.

Differentiation of gains and revenues is beneficial for users because they are easily record

all the transactions and less operating expenses from the revenues. After all the deductions get

the amount of the gains that presents actual position and take right decision in regard of future

investments.

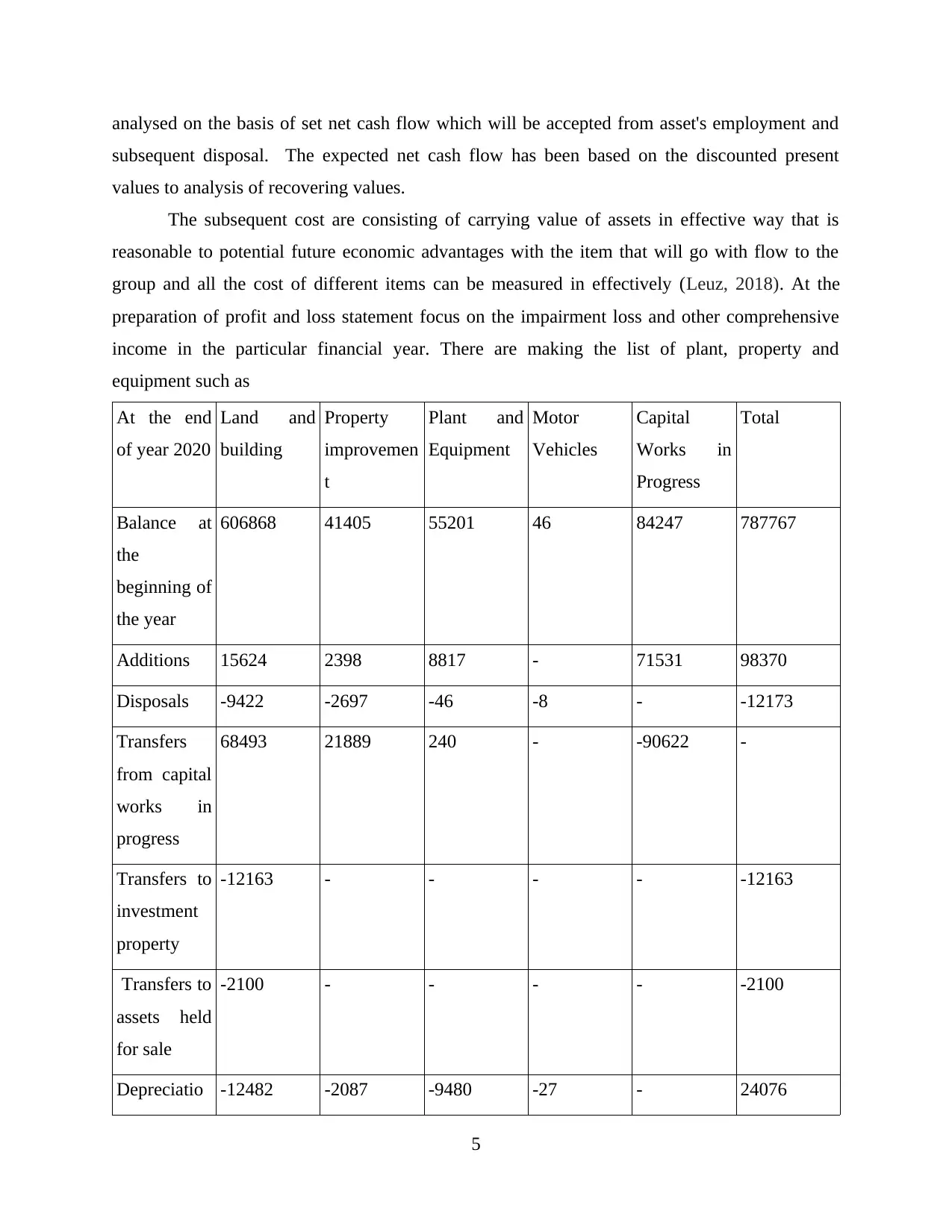

4 Explain and discuss the list of Property, Plant and Equipment, including impairment

assessments in the financial statements and the related notes. How are these assets

measured and valued?

Property, plant and equipment is mentioned at the cost and from the amount less

depreciation amount and impairment losses. The carrying amount of property, plant and

equipment is analysis on yearly basis as per the guidance of organisation directors to guaranteed

about the excess of the recoverable amount from these assets. The recoverable amount has been

4

gains in every year. The data presenting in increasing manner it means company has effective

financial performance. Net gains of the Japara fall down due to face pandemic situation and it

impacts on the business in direct manner. In the year of 2020 company has 422,242 revenues and

in 2019 have 394937.

Most of the organisations record different items like gains, revenues, expenditure and

losses that record in the income statements. These items are sounding same but it is different in

practice use for gains and revenues. As per the my point of view it is saying that revenues and

gains are differentiated is profit because in revenues includes all taxes and interests that need to

pay. On the other side in gains less taxes, interest that use to present the actual position of the

business. Thus, it is saying that it is right for the accounting users to differentiate of the revenues

and gains (Kozlowski, Issa and Appelbaum, 2018).

Revenue is amount which is generated by the business entity after complementation of

main operating activities like retailer selling merchandise of effective law that providing legal

services. On the other side Gain is defined as outcome of marginal operations like retailer

selling of the old delivery trucks. A gain arise when the cash amount received and it is noticed in

excess manner and referred to as the asset's book value. For example, when an organisation

receives $5000 for old delivery truck and the carry amount noticed at the book value so sales

was $800, the company will have a gain $4200.

Differentiation of gains and revenues is beneficial for users because they are easily record

all the transactions and less operating expenses from the revenues. After all the deductions get

the amount of the gains that presents actual position and take right decision in regard of future

investments.

4 Explain and discuss the list of Property, Plant and Equipment, including impairment

assessments in the financial statements and the related notes. How are these assets

measured and valued?

Property, plant and equipment is mentioned at the cost and from the amount less

depreciation amount and impairment losses. The carrying amount of property, plant and

equipment is analysis on yearly basis as per the guidance of organisation directors to guaranteed

about the excess of the recoverable amount from these assets. The recoverable amount has been

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

analysed on the basis of set net cash flow which will be accepted from asset's employment and

subsequent disposal. The expected net cash flow has been based on the discounted present

values to analysis of recovering values.

The subsequent cost are consisting of carrying value of assets in effective way that is

reasonable to potential future economic advantages with the item that will go with flow to the

group and all the cost of different items can be measured in effectively (Leuz, 2018). At the

preparation of profit and loss statement focus on the impairment loss and other comprehensive

income in the particular financial year. There are making the list of plant, property and

equipment such as

At the end

of year 2020

Land and

building

Property

improvemen

t

Plant and

Equipment

Motor

Vehicles

Capital

Works in

Progress

Total

Balance at

the

beginning of

the year

606868 41405 55201 46 84247 787767

Additions 15624 2398 8817 - 71531 98370

Disposals -9422 -2697 -46 -8 - -12173

Transfers

from capital

works in

progress

68493 21889 240 - -90622 -

Transfers to

investment

property

-12163 - - - - -12163

Transfers to

assets held

for sale

-2100 - - - - -2100

Depreciatio -12482 -2087 -9480 -27 - 24076

5

subsequent disposal. The expected net cash flow has been based on the discounted present

values to analysis of recovering values.

The subsequent cost are consisting of carrying value of assets in effective way that is

reasonable to potential future economic advantages with the item that will go with flow to the

group and all the cost of different items can be measured in effectively (Leuz, 2018). At the

preparation of profit and loss statement focus on the impairment loss and other comprehensive

income in the particular financial year. There are making the list of plant, property and

equipment such as

At the end

of year 2020

Land and

building

Property

improvemen

t

Plant and

Equipment

Motor

Vehicles

Capital

Works in

Progress

Total

Balance at

the

beginning of

the year

606868 41405 55201 46 84247 787767

Additions 15624 2398 8817 - 71531 98370

Disposals -9422 -2697 -46 -8 - -12173

Transfers

from capital

works in

progress

68493 21889 240 - -90622 -

Transfers to

investment

property

-12163 - - - - -12163

Transfers to

assets held

for sale

-2100 - - - - -2100

Depreciatio -12482 -2087 -9480 -27 - 24076

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

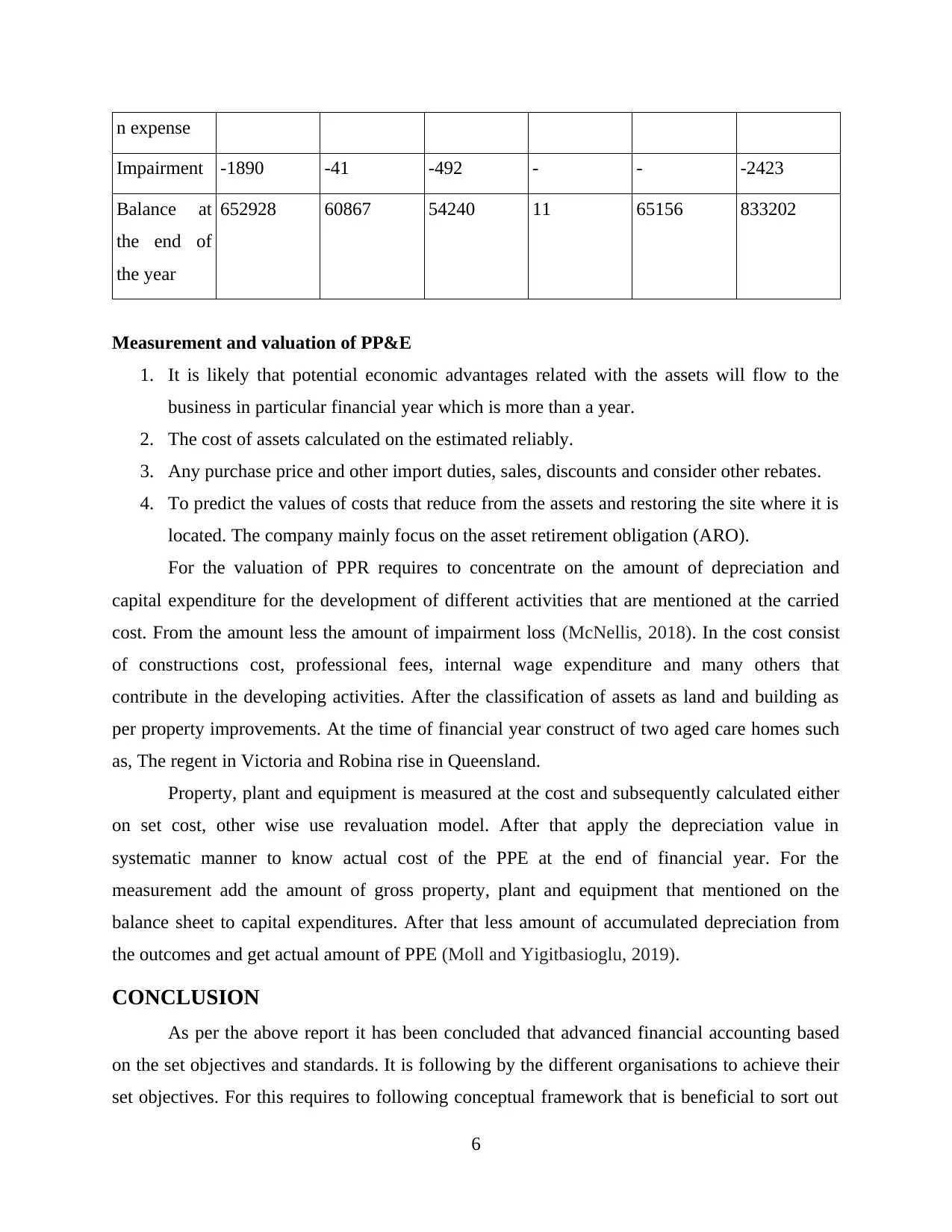

n expense

Impairment -1890 -41 -492 - - -2423

Balance at

the end of

the year

652928 60867 54240 11 65156 833202

Measurement and valuation of PP&E

1. It is likely that potential economic advantages related with the assets will flow to the

business in particular financial year which is more than a year.

2. The cost of assets calculated on the estimated reliably.

3. Any purchase price and other import duties, sales, discounts and consider other rebates.

4. To predict the values of costs that reduce from the assets and restoring the site where it is

located. The company mainly focus on the asset retirement obligation (ARO).

For the valuation of PPR requires to concentrate on the amount of depreciation and

capital expenditure for the development of different activities that are mentioned at the carried

cost. From the amount less the amount of impairment loss (McNellis, 2018). In the cost consist

of constructions cost, professional fees, internal wage expenditure and many others that

contribute in the developing activities. After the classification of assets as land and building as

per property improvements. At the time of financial year construct of two aged care homes such

as, The regent in Victoria and Robina rise in Queensland.

Property, plant and equipment is measured at the cost and subsequently calculated either

on set cost, other wise use revaluation model. After that apply the depreciation value in

systematic manner to know actual cost of the PPE at the end of financial year. For the

measurement add the amount of gross property, plant and equipment that mentioned on the

balance sheet to capital expenditures. After that less amount of accumulated depreciation from

the outcomes and get actual amount of PPE (Moll and Yigitbasioglu, 2019).

CONCLUSION

As per the above report it has been concluded that advanced financial accounting based

on the set objectives and standards. It is following by the different organisations to achieve their

set objectives. For this requires to following conceptual framework that is beneficial to sort out

6

Impairment -1890 -41 -492 - - -2423

Balance at

the end of

the year

652928 60867 54240 11 65156 833202

Measurement and valuation of PP&E

1. It is likely that potential economic advantages related with the assets will flow to the

business in particular financial year which is more than a year.

2. The cost of assets calculated on the estimated reliably.

3. Any purchase price and other import duties, sales, discounts and consider other rebates.

4. To predict the values of costs that reduce from the assets and restoring the site where it is

located. The company mainly focus on the asset retirement obligation (ARO).

For the valuation of PPR requires to concentrate on the amount of depreciation and

capital expenditure for the development of different activities that are mentioned at the carried

cost. From the amount less the amount of impairment loss (McNellis, 2018). In the cost consist

of constructions cost, professional fees, internal wage expenditure and many others that

contribute in the developing activities. After the classification of assets as land and building as

per property improvements. At the time of financial year construct of two aged care homes such

as, The regent in Victoria and Robina rise in Queensland.

Property, plant and equipment is measured at the cost and subsequently calculated either

on set cost, other wise use revaluation model. After that apply the depreciation value in

systematic manner to know actual cost of the PPE at the end of financial year. For the

measurement add the amount of gross property, plant and equipment that mentioned on the

balance sheet to capital expenditures. After that less amount of accumulated depreciation from

the outcomes and get actual amount of PPE (Moll and Yigitbasioglu, 2019).

CONCLUSION

As per the above report it has been concluded that advanced financial accounting based

on the set objectives and standards. It is following by the different organisations to achieve their

set objectives. For this requires to following conceptual framework that is beneficial to sort out

6

accounting errors in shorter period of time. Along with analysis of reporting entity which is

based on the general purpose and complete all the task in particular period of time.

REFERENCES

Books and Journals

Chen, S. and Komal, B., 2018. Audit committee financial expertise and earnings quality: A meta-

analysis. Journal of Business Research. 84. pp.253-270.

Chychyla, R., Leone, A. J. and Minutti-Meza, M., 2019. Complexity of financial reporting

standards and accounting expertise. Journal of Accounting and Economics. 67(1).

pp.226-253.

Hairston, S. A. and Brooks, M. R., 2019. Derivative accounting and financial reporting quality:

A review of the literature. Advances in accounting. 44. pp.81-94.

Han, J., He, J., Pan, Z. and Shi, J., 2018. Twenty years of accounting and finance research on the

Chinese capital market. Abacus. 54(4). pp.576-599.

Himick, D. and Brivot, M., 2018. Carriers of ideas in accounting standard-setting and

financialization: The role of epistemic communities. Accounting, Organizations and

Society. 66. pp.29-44.

Kozlowski, S., Issa, H. and Appelbaum, D., 2018. Making government data valuable for

constituents: The case for the advanced data analytics capabilities of the ENHANCE

framework. Journal of Emerging Technologies in Accounting. 15(1). pp.155-167.

Leuz, C., 2018. Evidence-based policymaking: promise, challenges and opportunities for

accounting and financial markets research. Accounting and Business Research. 48(5).

pp.582-608.

McNellis, C. J., 2018. Dynamic Divestures: A codification exercise on the reporting of

discontinued operations. Issues in Accounting Education. 33(1). pp.53-63.

Moll, J. and Yigitbasioglu, O., 2019. The role of internet-related technologies in shaping the

work of accountants: New directions for accounting research. The British Accounting

Review. 51(6). p.100833.

Ng, A. W., 2018. From sustainability accounting to a green financing system: Institutional

legitimacy and market heterogeneity in a global financial centre. Journal of Cleaner

Production. 195. pp.585-592.

ÖZCAN, A., 2019. Analyzing the impact of forensic accounting on the detection of financial

information manipulation. Manas Sosyal Araştırmalar Dergisi. 8(2). pp.1744-1760.

7

based on the general purpose and complete all the task in particular period of time.

REFERENCES

Books and Journals

Chen, S. and Komal, B., 2018. Audit committee financial expertise and earnings quality: A meta-

analysis. Journal of Business Research. 84. pp.253-270.

Chychyla, R., Leone, A. J. and Minutti-Meza, M., 2019. Complexity of financial reporting

standards and accounting expertise. Journal of Accounting and Economics. 67(1).

pp.226-253.

Hairston, S. A. and Brooks, M. R., 2019. Derivative accounting and financial reporting quality:

A review of the literature. Advances in accounting. 44. pp.81-94.

Han, J., He, J., Pan, Z. and Shi, J., 2018. Twenty years of accounting and finance research on the

Chinese capital market. Abacus. 54(4). pp.576-599.

Himick, D. and Brivot, M., 2018. Carriers of ideas in accounting standard-setting and

financialization: The role of epistemic communities. Accounting, Organizations and

Society. 66. pp.29-44.

Kozlowski, S., Issa, H. and Appelbaum, D., 2018. Making government data valuable for

constituents: The case for the advanced data analytics capabilities of the ENHANCE

framework. Journal of Emerging Technologies in Accounting. 15(1). pp.155-167.

Leuz, C., 2018. Evidence-based policymaking: promise, challenges and opportunities for

accounting and financial markets research. Accounting and Business Research. 48(5).

pp.582-608.

McNellis, C. J., 2018. Dynamic Divestures: A codification exercise on the reporting of

discontinued operations. Issues in Accounting Education. 33(1). pp.53-63.

Moll, J. and Yigitbasioglu, O., 2019. The role of internet-related technologies in shaping the

work of accountants: New directions for accounting research. The British Accounting

Review. 51(6). p.100833.

Ng, A. W., 2018. From sustainability accounting to a green financing system: Institutional

legitimacy and market heterogeneity in a global financial centre. Journal of Cleaner

Production. 195. pp.585-592.

ÖZCAN, A., 2019. Analyzing the impact of forensic accounting on the detection of financial

information manipulation. Manas Sosyal Araştırmalar Dergisi. 8(2). pp.1744-1760.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.