Advanced Financial Accounting Report: Goodwill, IFRS, and NCI Analysis

VerifiedAdded on 2020/07/22

|12

|2726

|134

Report

AI Summary

This report delves into the complexities of goodwill calculation within the context of mergers and acquisitions. It begins by explaining how the nature of consideration impacts goodwill valuation, differentiating between partial and full consideration approaches. The report then provides a detailed comparison of the full and partial goodwill methods, examining their implications under IFRS 3 Business Combinations, and discussing whether the full goodwill method is mandatory. Furthermore, it clarifies the effects of selecting the full goodwill method over the proportion of net asset method. Finally, the report offers recommendations to the board of Expander regarding the appropriate accounting policy for measuring non-controlling interest at acquisition, covering valuation methods such as share price-based valuation and the Discount for Lack of Marketability (DLOM) method when applicable. The report concludes by emphasizing the importance of accurate goodwill calculation and appropriate accounting policies in financial reporting.

ADVANCED FINANCIAL

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................... 3

(a)Explain how the nature of the consideration affects the calculation of goodwill.......................3

(b) Discuss whether the use of the “full goodwill” as preferred by IFRS 3 Business Combinations

is mandatory.................................................................................................................................. 4

© Explain what the effect of selecting the “full goodwill” method rather than the proportion of

net asset method would be.............................................................................................................5

(d)Advice the board of Expander as to the appropriate accounting policy to adopt in respect of

measuring non-controlling interest at acquisition..........................................................................6

CONCLUSION............................................................................................................................. 7

REFERENCES..........................................................................................................................................8

INTRODUCTION......................................................................................................................... 3

(a)Explain how the nature of the consideration affects the calculation of goodwill.......................3

(b) Discuss whether the use of the “full goodwill” as preferred by IFRS 3 Business Combinations

is mandatory.................................................................................................................................. 4

© Explain what the effect of selecting the “full goodwill” method rather than the proportion of

net asset method would be.............................................................................................................5

(d)Advice the board of Expander as to the appropriate accounting policy to adopt in respect of

measuring non-controlling interest at acquisition..........................................................................6

CONCLUSION............................................................................................................................. 7

REFERENCES..........................................................................................................................................8

INTRODUCTION

Merger and acquisition is done by most of business firms to expand their business at

rapid pace. In current time period varied small and big deals are happening in varied nations of

the world. Accounting in merger and acquisition deals become more complex. In the current

report, nature of consideration and its impact on calculation of goodwill is explained in detail. In

middle part of the report, full and partial goodwill methods are discussed in detail. Apart from

this, accounting policy that is adopted in respect to measurement of non-controlling interest are

also discussed in detail. At end of the report, conclusion section is developed in the report.

(a)Explain how the nature of the consideration affects the calculation of

goodwill

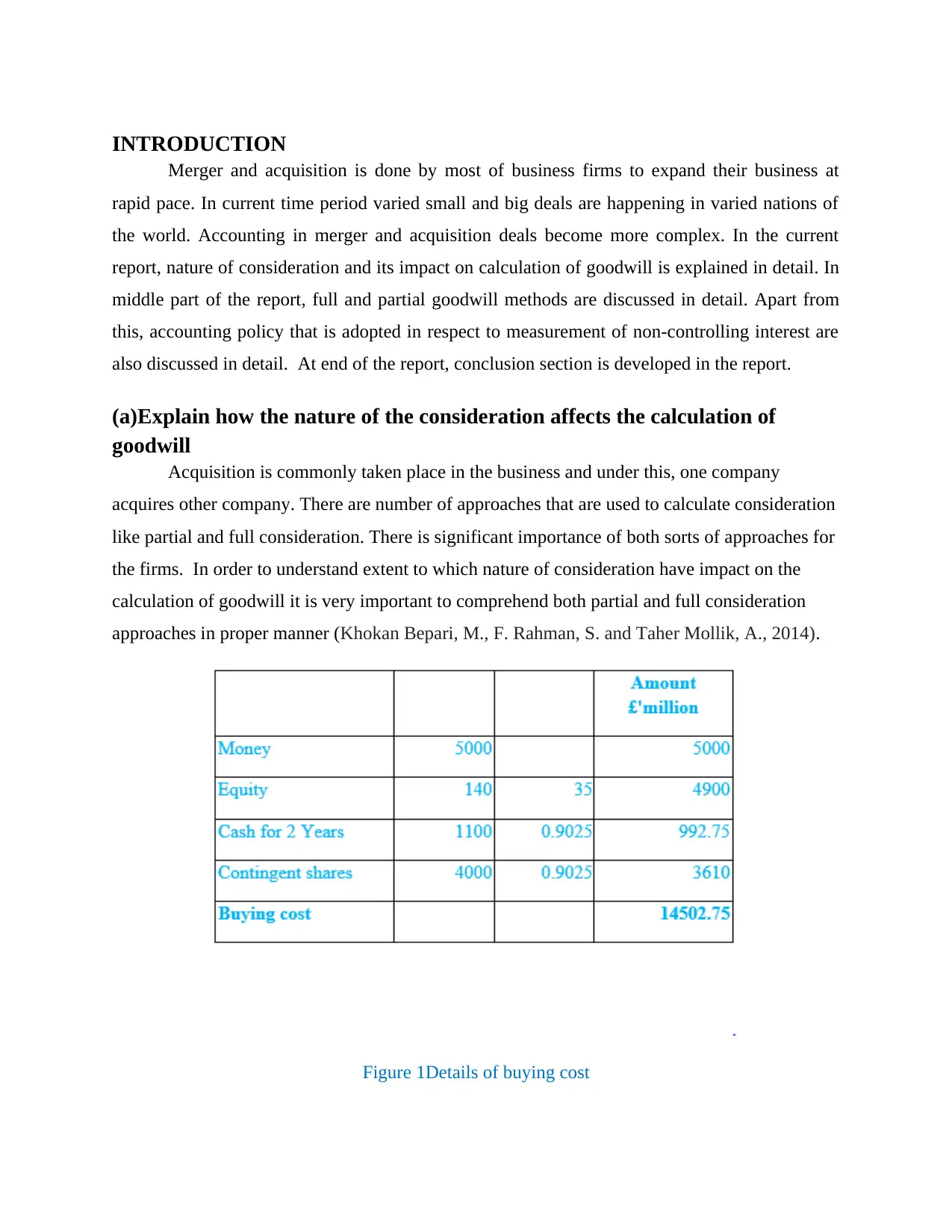

Acquisition is commonly taken place in the business and under this, one company

acquires other company. There are number of approaches that are used to calculate consideration

like partial and full consideration. There is significant importance of both sorts of approaches for

the firms. In order to understand extent to which nature of consideration have impact on the

calculation of goodwill it is very important to comprehend both partial and full consideration

approaches in proper manner (Khokan Bepari, M., F. Rahman, S. and Taher Mollik, A., 2014).

Figure 1Details of buying cost

Merger and acquisition is done by most of business firms to expand their business at

rapid pace. In current time period varied small and big deals are happening in varied nations of

the world. Accounting in merger and acquisition deals become more complex. In the current

report, nature of consideration and its impact on calculation of goodwill is explained in detail. In

middle part of the report, full and partial goodwill methods are discussed in detail. Apart from

this, accounting policy that is adopted in respect to measurement of non-controlling interest are

also discussed in detail. At end of the report, conclusion section is developed in the report.

(a)Explain how the nature of the consideration affects the calculation of

goodwill

Acquisition is commonly taken place in the business and under this, one company

acquires other company. There are number of approaches that are used to calculate consideration

like partial and full consideration. There is significant importance of both sorts of approaches for

the firms. In order to understand extent to which nature of consideration have impact on the

calculation of goodwill it is very important to comprehend both partial and full consideration

approaches in proper manner (Khokan Bepari, M., F. Rahman, S. and Taher Mollik, A., 2014).

Figure 1Details of buying cost

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Figure 2Partial Goodwill Calculation

Figure 3Full Goodwill calculation

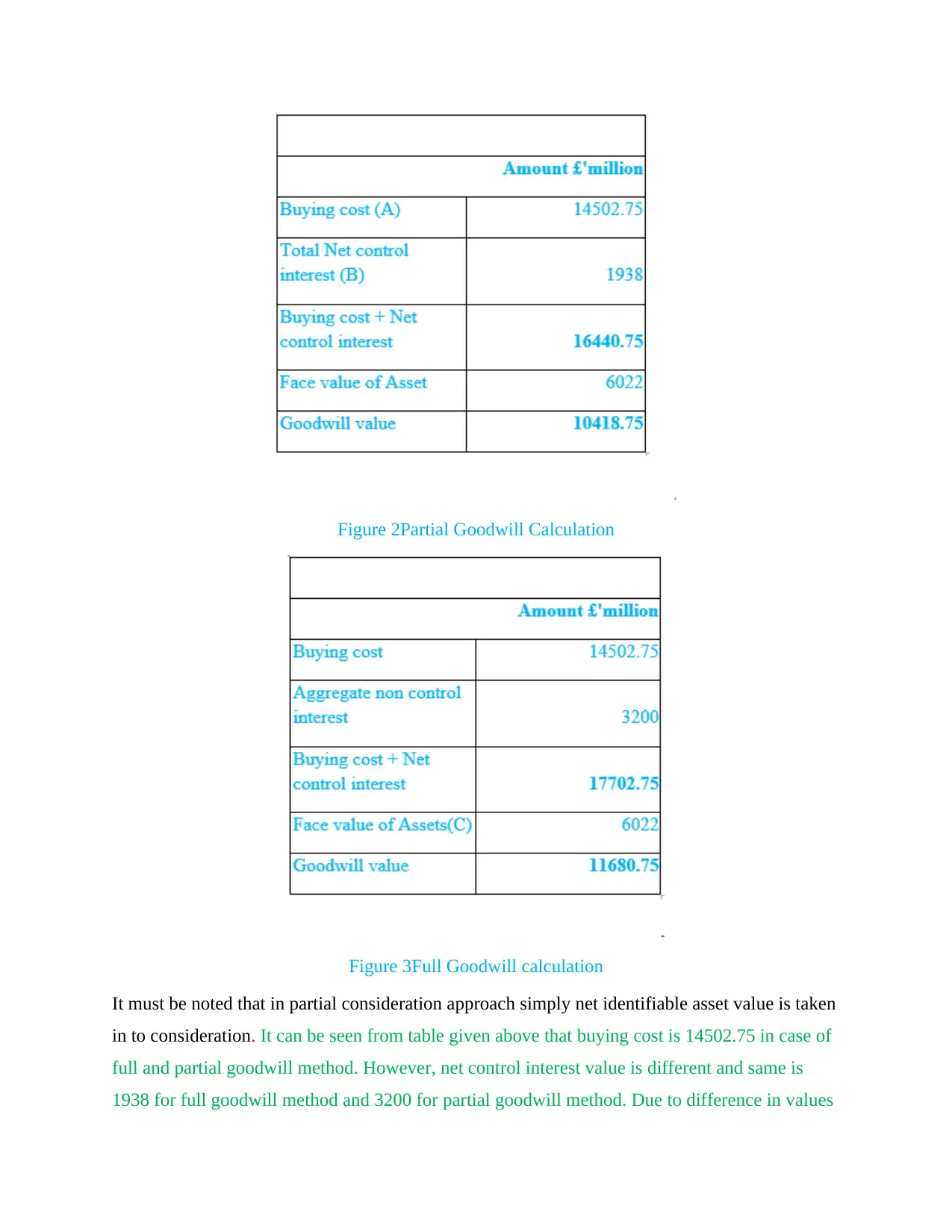

It must be noted that in partial consideration approach simply net identifiable asset value is taken

in to consideration. It can be seen from table given above that buying cost is 14502.75 in case of

full and partial goodwill method. However, net control interest value is different and same is

1938 for full goodwill method and 3200 for partial goodwill method. Due to difference in values

Figure 3Full Goodwill calculation

It must be noted that in partial consideration approach simply net identifiable asset value is taken

in to consideration. It can be seen from table given above that buying cost is 14502.75 in case of

full and partial goodwill method. However, net control interest value is different and same is

1938 for full goodwill method and 3200 for partial goodwill method. Due to difference in values

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

buying cost plus net control interest value is different for both as 16440 in case of full goodwill

and 17702 for partial goodwill method. Goodwill amount is increasing in case of full goodwill

method as it can be observed that value of goodwill is 11680 million and in case of partial

goodwill value is 10418 million. Total assets that firm have in its business are equal to 5 Value

for which company acquired is 280 million. It must be noted that in case of full goodwill full

amount is taken in to account not merely 70% of overall value of the company. It can be

assumed that accurate approach is followed to compute value of goodwill in the business and by

considering all values of assets and liability in proper manner goodwill is computed in partial

and full method. It can be said that goodwill value is high in case of full approach then partial.

In order to compute value of net identifiable asset simply from asset impairment asset amount is

subtracted if there is any in business. Then from computed value amount of liability is subtracted

and in this way, value of net identifiable asset is computed in this method. On other hand, in case

of full consideration method, simply book value of net identifiable asset is taken in to account

and from same if, there is any amount of impairment then it is deducted (Full goodwill method,

2017). In this way, in case of partial consideration value of net identifiable asset is computed. It

can be said that there is big difference in calculation of both partial and full consideration

approach for calculation of goodwill. It can be assumed that nature of considerations have impact

on calculation of goodwill (Bepari and Mollik, 2015). It can be observed that in partial method

only that part is considered for consideration which will be acquired by on company in another

but in full consideration entire value of Target Company is taken in to account. This is the major

difference between both approaches, which have impact on the calculation of goodwill amount.

It can be said that full goodwill and partial goodwill method both are important for the firms and

according to their requirements and way in which they intend to do acquisition, appropriate

method must be used (Johansson, Hjelström and Hellman, 2016). Hence, the firms can use it in

order to identify that if they enter in to any deal that what amount of goodwill they can observe

in balance sheet.

(b) Discuss whether the use of the “full goodwill” as preferred by IFRS 3

Business Combinations is mandatory

In the IFRS it is not mandatory to use full goodwill method for valuation of mentioned

asset. It is the preferred but is available as option to the business firms under IFRS. There are

many reasons behind this and one of them is that if by using full goodwill method entire

and 17702 for partial goodwill method. Goodwill amount is increasing in case of full goodwill

method as it can be observed that value of goodwill is 11680 million and in case of partial

goodwill value is 10418 million. Total assets that firm have in its business are equal to 5 Value

for which company acquired is 280 million. It must be noted that in case of full goodwill full

amount is taken in to account not merely 70% of overall value of the company. It can be

assumed that accurate approach is followed to compute value of goodwill in the business and by

considering all values of assets and liability in proper manner goodwill is computed in partial

and full method. It can be said that goodwill value is high in case of full approach then partial.

In order to compute value of net identifiable asset simply from asset impairment asset amount is

subtracted if there is any in business. Then from computed value amount of liability is subtracted

and in this way, value of net identifiable asset is computed in this method. On other hand, in case

of full consideration method, simply book value of net identifiable asset is taken in to account

and from same if, there is any amount of impairment then it is deducted (Full goodwill method,

2017). In this way, in case of partial consideration value of net identifiable asset is computed. It

can be said that there is big difference in calculation of both partial and full consideration

approach for calculation of goodwill. It can be assumed that nature of considerations have impact

on calculation of goodwill (Bepari and Mollik, 2015). It can be observed that in partial method

only that part is considered for consideration which will be acquired by on company in another

but in full consideration entire value of Target Company is taken in to account. This is the major

difference between both approaches, which have impact on the calculation of goodwill amount.

It can be said that full goodwill and partial goodwill method both are important for the firms and

according to their requirements and way in which they intend to do acquisition, appropriate

method must be used (Johansson, Hjelström and Hellman, 2016). Hence, the firms can use it in

order to identify that if they enter in to any deal that what amount of goodwill they can observe

in balance sheet.

(b) Discuss whether the use of the “full goodwill” as preferred by IFRS 3

Business Combinations is mandatory

In the IFRS it is not mandatory to use full goodwill method for valuation of mentioned

asset. It is the preferred but is available as option to the business firms under IFRS. There are

many reasons behind this and one of them is that if by using full goodwill method entire

calculation will be done then in that case assets will be reported at very high value in balance

sheet. In case impairment of asset happened in business then in that case assets value may

decline by high percentage. Due to all things assets value will decline at fast rate and financial

position of an organization will shrink sharply. Hence, this is the one of the main reason due to

which full goodwill method is used as optional by the business firms. There are certain factors.

Other main reason behind no considering full consideration as preferred option is that for

goodwill computation entire asset amount is taken in to account even firms does not purchase it.

This cannot be considered good by the business firm because inclusion of portion of asset for

which no amount is paid cannot be considered appropriate from any angel in the business. On

other hand, in case of partial goodwill this thing does not happened because in this case only that

portion of asset is included for which payment is made (Hatipoglu, Biba and Backaliden, 2016).

This is the reason due to which full goodwill is not considered better then partial consideration in

IFRS. Main aim of IFRS 3 is to ensure that there is transparency in recording of operations and

there is high reliability of recording of transactions in books of accounts. This is the one of the

main factor due to which full goodwill is not considered as one of the best option in the IFRS

and by business firms. These are the one of the main reasons due to which most of firms are

using partial goodwill method in their books of accounts because it give true representation of

the value of the asset that firm acquire and accurately goodwill is calculated. Moreover, if any

firm include value of goodwill on basis of full goodwill method then in that case it is assumed by

other entities like investors and peers that there is lack of transparency in firm operations. It can

be said that firms must use partial goodwill method in its business (Klimczak, Dynel and

Językowej, 2015). It is very important to ensure that peer firms and other entities like investors

are fully confident and have belief that firm accounting statements are revealing true financial

position and decisions can be taken on that basis. Hence, it can be said that partial goodwill

method is assumed better than full goodwill method because it is the more perfect approach and

ensured that all transactions will be recoded accurately in the books of accounts. It can be said

that there is huge significance of partial goodwill approach then full goodwill approach.

© Explain what the effect of selecting the “full goodwill” method rather than

the proportion of net asset method would be

Net asset in case of partial goodwill method= Value of asset-value of liability

=5-11= -6

sheet. In case impairment of asset happened in business then in that case assets value may

decline by high percentage. Due to all things assets value will decline at fast rate and financial

position of an organization will shrink sharply. Hence, this is the one of the main reason due to

which full goodwill method is used as optional by the business firms. There are certain factors.

Other main reason behind no considering full consideration as preferred option is that for

goodwill computation entire asset amount is taken in to account even firms does not purchase it.

This cannot be considered good by the business firm because inclusion of portion of asset for

which no amount is paid cannot be considered appropriate from any angel in the business. On

other hand, in case of partial goodwill this thing does not happened because in this case only that

portion of asset is included for which payment is made (Hatipoglu, Biba and Backaliden, 2016).

This is the reason due to which full goodwill is not considered better then partial consideration in

IFRS. Main aim of IFRS 3 is to ensure that there is transparency in recording of operations and

there is high reliability of recording of transactions in books of accounts. This is the one of the

main factor due to which full goodwill is not considered as one of the best option in the IFRS

and by business firms. These are the one of the main reasons due to which most of firms are

using partial goodwill method in their books of accounts because it give true representation of

the value of the asset that firm acquire and accurately goodwill is calculated. Moreover, if any

firm include value of goodwill on basis of full goodwill method then in that case it is assumed by

other entities like investors and peers that there is lack of transparency in firm operations. It can

be said that firms must use partial goodwill method in its business (Klimczak, Dynel and

Językowej, 2015). It is very important to ensure that peer firms and other entities like investors

are fully confident and have belief that firm accounting statements are revealing true financial

position and decisions can be taken on that basis. Hence, it can be said that partial goodwill

method is assumed better than full goodwill method because it is the more perfect approach and

ensured that all transactions will be recoded accurately in the books of accounts. It can be said

that there is huge significance of partial goodwill approach then full goodwill approach.

© Explain what the effect of selecting the “full goodwill” method rather than

the proportion of net asset method would be

Net asset in case of partial goodwill method= Value of asset-value of liability

=5-11= -6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

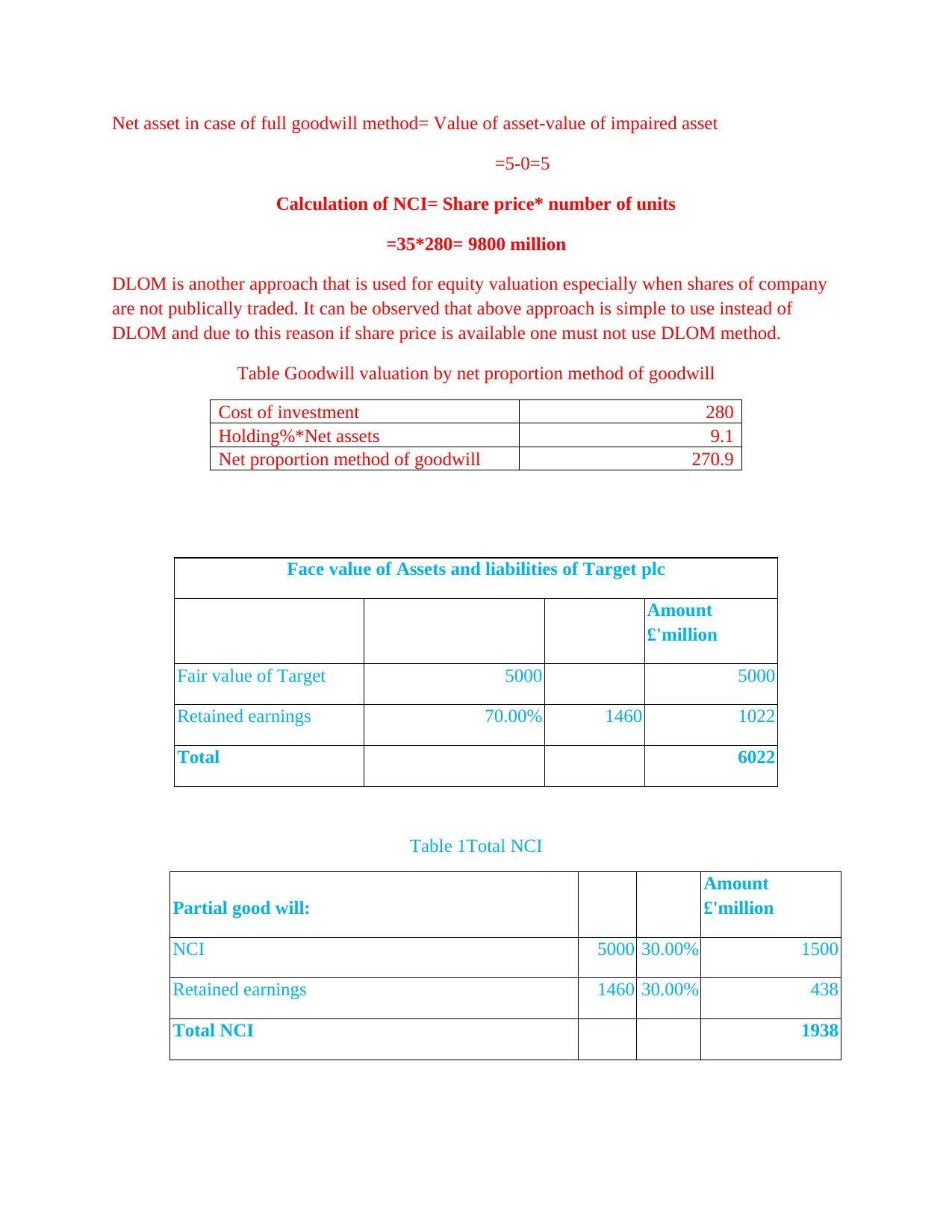

Net asset in case of full goodwill method= Value of asset-value of impaired asset

=5-0=5

Calculation of NCI= Share price* number of units

=35*280= 9800 million

DLOM is another approach that is used for equity valuation especially when shares of company

are not publically traded. It can be observed that above approach is simple to use instead of

DLOM and due to this reason if share price is available one must not use DLOM method.

Table Goodwill valuation by net proportion method of goodwill

Cost of investment 280

Holding%*Net assets 9.1

Net proportion method of goodwill 270.9

Face value of Assets and liabilities of Target plc

Amount

£'million

Fair value of Target 5000 5000

Retained earnings 70.00% 1460 1022

Total 6022

Table 1Total NCI

Partial good will:

Amount

£'million

NCI 5000 30.00% 1500

Retained earnings 1460 30.00% 438

Total NCI 1938

=5-0=5

Calculation of NCI= Share price* number of units

=35*280= 9800 million

DLOM is another approach that is used for equity valuation especially when shares of company

are not publically traded. It can be observed that above approach is simple to use instead of

DLOM and due to this reason if share price is available one must not use DLOM method.

Table Goodwill valuation by net proportion method of goodwill

Cost of investment 280

Holding%*Net assets 9.1

Net proportion method of goodwill 270.9

Face value of Assets and liabilities of Target plc

Amount

£'million

Fair value of Target 5000 5000

Retained earnings 70.00% 1460 1022

Total 6022

Table 1Total NCI

Partial good will:

Amount

£'million

NCI 5000 30.00% 1500

Retained earnings 1460 30.00% 438

Total NCI 1938

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total NCI in case of firm is 1938 and in order to computer this NCI amount 30% value is taken

in to account and retained earnings is added to it in order to compute final value of NCI. It can be

seen from table that goodwill computed by using net proportion method is 27.09 and value of

same computed by using full goodwill method is 395 million. Full goodwill and proportion of

net assets are two different approaches that are available to the firms in respect to performing

calculation in respect to goodwill. It can be observed that before full goodwill method was

developed net proportion method of goodwill was widely used for computation of goodwill in

the business (Jackson, 2016). It can be observed that in partial proportion method simply first of

all acquisition value is determined and then specific amount is subtracted from it. In this specific

amount holding percentage is charged on value of net assets and in this way goodwill amount is

computed. It can be said that it is the one of easy approach of computation of goodwill. On other

hand, there is another approach which is known as full goodwill approach under which number

of things are taken in to account. In this approach book value of net identifiable asset is taken in

to account and along with it book value of asset and liability is taken in to account. Apart from

this, amount of money that is spend or proposed to be spend on acquisition deal is also taken in

to account. By using relevant variables goodwill amount is computed in the business

(Baboukardos and Rimmel, 2014).

(d)Advice the board of Expander as to the appropriate accounting policy to

adopt in respect of measuring non-controlling interest at acquisition

Specific accounting policy must be followed under which shares must be valued by using

share price and number of units one receive under NCI. In case shares are not traded in stock

exchange then DLOM method must be used (International Accounting Standards Board

[IASB]2003). Non-controlling interest refers to ownership stake that is in cooperation where

investors have less interest and they less participate in managing firm. Business combination

required that in case 100% stake is not acquired in any firm in order to measure NCI transactions

must be selected transaction by transaction. Initial recognition can be made by considering value

of asset on date of acquisition. It must be noted that this accounting policy is related only to

initial measurement of ordinary NCI. While developing cash flow statement while doing

accounting for NCI it is very important to identify some practical applications of accounting in

relevant areas so that in proper manner recording of transactions can be done in the business. An

entity is need to attribute profit and loss and it need to be ensure that same is done in respect to

in to account and retained earnings is added to it in order to compute final value of NCI. It can be

seen from table that goodwill computed by using net proportion method is 27.09 and value of

same computed by using full goodwill method is 395 million. Full goodwill and proportion of

net assets are two different approaches that are available to the firms in respect to performing

calculation in respect to goodwill. It can be observed that before full goodwill method was

developed net proportion method of goodwill was widely used for computation of goodwill in

the business (Jackson, 2016). It can be observed that in partial proportion method simply first of

all acquisition value is determined and then specific amount is subtracted from it. In this specific

amount holding percentage is charged on value of net assets and in this way goodwill amount is

computed. It can be said that it is the one of easy approach of computation of goodwill. On other

hand, there is another approach which is known as full goodwill approach under which number

of things are taken in to account. In this approach book value of net identifiable asset is taken in

to account and along with it book value of asset and liability is taken in to account. Apart from

this, amount of money that is spend or proposed to be spend on acquisition deal is also taken in

to account. By using relevant variables goodwill amount is computed in the business

(Baboukardos and Rimmel, 2014).

(d)Advice the board of Expander as to the appropriate accounting policy to

adopt in respect of measuring non-controlling interest at acquisition

Specific accounting policy must be followed under which shares must be valued by using

share price and number of units one receive under NCI. In case shares are not traded in stock

exchange then DLOM method must be used (International Accounting Standards Board

[IASB]2003). Non-controlling interest refers to ownership stake that is in cooperation where

investors have less interest and they less participate in managing firm. Business combination

required that in case 100% stake is not acquired in any firm in order to measure NCI transactions

must be selected transaction by transaction. Initial recognition can be made by considering value

of asset on date of acquisition. It must be noted that this accounting policy is related only to

initial measurement of ordinary NCI. While developing cash flow statement while doing

accounting for NCI it is very important to identify some practical applications of accounting in

relevant areas so that in proper manner recording of transactions can be done in the business. An

entity is need to attribute profit and loss and it need to be ensure that same is done in respect to

each component of income owners of parent company and NCI. An entity required to allocate

loss that is faced by subsidiary between parent company and NCI even it ultimately result in

negative balance of NCI (Glaum, Landsman and Wyrwa, 2015). It can be said that consolidated

equity amount need to be used to compute non-controlling interest in respect to acquisition deals

rather than recorded amount of equity in the business. It can be said that relevant accounting

policy need to be used and in proper manner so that non-controlling interest can be measured in

proper manner.

CONCLUSION

On basis of above discussion it is concluded that there is significant importance of

accounting standards for the business firms because it ensured that all transactions will be

recorded accurately and in proper manner. It is also concluded that partial goodwill method is

better than full goodwill method and due to this reason it is widely adopted by IFRS and

suggested to firm to use it in practice in respect to recording of merger and acquisition deals in

the business.

loss that is faced by subsidiary between parent company and NCI even it ultimately result in

negative balance of NCI (Glaum, Landsman and Wyrwa, 2015). It can be said that consolidated

equity amount need to be used to compute non-controlling interest in respect to acquisition deals

rather than recorded amount of equity in the business. It can be said that relevant accounting

policy need to be used and in proper manner so that non-controlling interest can be measured in

proper manner.

CONCLUSION

On basis of above discussion it is concluded that there is significant importance of

accounting standards for the business firms because it ensured that all transactions will be

recorded accurately and in proper manner. It is also concluded that partial goodwill method is

better than full goodwill method and due to this reason it is widely adopted by IFRS and

suggested to firm to use it in practice in respect to recording of merger and acquisition deals in

the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Baboukardos, D. and Rimmel, G., 2014, March. Goodwill under IFRS: Relevance and

disclosures in an unfavorable environment. In Accounting Forum (Vol. 38, No. 1, pp. 1-

17). Elsevier.

Bepari, M.K. and Mollik, A.T., 2015. Effect of audit quality and accounting and finance

backgrounds of audit committee members on firms’ compliance with IFRS for goodwill

impairment testing. Journal of Applied Accounting Research. 16(2). pp.196-220.

Glaum, M., Landsman, W.R. and Wyrwa, S., 2015. Determinants of Goodwill Impairment under

IFRS: International Evidence. Working Paper, available at: http://ssrn. com/abstract=

2608425.

Hatipoglu, S., Biba, N. and Backaliden, D., 2016. Goodwill impairment-Who cares? An event

study about IFRS 3 value creation on the Swedish stock market.

Jackson, A., 2016. The Impact of IFRS Goodwill Reporting on Financial Analysts' Equity

Valuation Judgements: Some Experimental Evidence (Digest Summary): N. Hellman, P.

Andersson & E. Fröberg, Accounting & Finance, Vol. 56, No. 1 (March 2016), 113-

157. CFA Digest. 46(8).

Johansson, S.E., Hjelström, T. and Hellman, N., 2016. Accounting for goodwill under IFRS: A

critical analysis. Journal of International Accounting, Auditing and Taxation. 27. pp.13-

25.

Khokan Bepari, M., F. Rahman, S. and Taher Mollik, A., 2014. Firms' compliance with the

disclosure requirements of IFRS for goodwill impairment testing: Effect of the global

financial crisis and other firm characteristics. Journal of Accounting & Organizational

Change. 10(1). pp.116-149.

Klimczak, K.M., Dynel, M. and Językowej, Z.P., 2015. Uncertainty in the financial statements:

the study of goodwill disclosures in Polish. J. Krasodomska, K. Świetla (red.),

Współczesne uwarunkowania sprawozdawczości i rewizji finansowej. pp.217-226.

Online

Full goodwill method, 2017. [Online]. Available through:<

https://accountingexplained.com/financial/business-combinations/full-goodwill-method>.

Books and Journals

Baboukardos, D. and Rimmel, G., 2014, March. Goodwill under IFRS: Relevance and

disclosures in an unfavorable environment. In Accounting Forum (Vol. 38, No. 1, pp. 1-

17). Elsevier.

Bepari, M.K. and Mollik, A.T., 2015. Effect of audit quality and accounting and finance

backgrounds of audit committee members on firms’ compliance with IFRS for goodwill

impairment testing. Journal of Applied Accounting Research. 16(2). pp.196-220.

Glaum, M., Landsman, W.R. and Wyrwa, S., 2015. Determinants of Goodwill Impairment under

IFRS: International Evidence. Working Paper, available at: http://ssrn. com/abstract=

2608425.

Hatipoglu, S., Biba, N. and Backaliden, D., 2016. Goodwill impairment-Who cares? An event

study about IFRS 3 value creation on the Swedish stock market.

Jackson, A., 2016. The Impact of IFRS Goodwill Reporting on Financial Analysts' Equity

Valuation Judgements: Some Experimental Evidence (Digest Summary): N. Hellman, P.

Andersson & E. Fröberg, Accounting & Finance, Vol. 56, No. 1 (March 2016), 113-

157. CFA Digest. 46(8).

Johansson, S.E., Hjelström, T. and Hellman, N., 2016. Accounting for goodwill under IFRS: A

critical analysis. Journal of International Accounting, Auditing and Taxation. 27. pp.13-

25.

Khokan Bepari, M., F. Rahman, S. and Taher Mollik, A., 2014. Firms' compliance with the

disclosure requirements of IFRS for goodwill impairment testing: Effect of the global

financial crisis and other firm characteristics. Journal of Accounting & Organizational

Change. 10(1). pp.116-149.

Klimczak, K.M., Dynel, M. and Językowej, Z.P., 2015. Uncertainty in the financial statements:

the study of goodwill disclosures in Polish. J. Krasodomska, K. Świetla (red.),

Współczesne uwarunkowania sprawozdawczości i rewizji finansowej. pp.217-226.

Online

Full goodwill method, 2017. [Online]. Available through:<

https://accountingexplained.com/financial/business-combinations/full-goodwill-method>.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

International Accounting Standards Board [IASB]. 2003.

[PDF]. International accounting standard 2: Inventories. Available online

at http://eifrs.ifrs.org/eifrs/bnstandards/en/IAS2.pdf .

[PDF]. International accounting standard 2: Inventories. Available online

at http://eifrs.ifrs.org/eifrs/bnstandards/en/IAS2.pdf .

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.