Financial Accounting Report: Depreciation and Valuation

VerifiedAdded on 2020/11/23

|10

|2202

|98

Report

AI Summary

This report delves into advanced financial accounting principles. It begins by calculating depreciation expense using the sum of digits method, followed by related journal entries. The report then explores the revaluation of assets and the subsequent depreciation using the revalued net amount method. Further, it addresses goodwill, determining if any was acquired and whether it can be revalued upwards. Finally, the report analyzes lease payments, calculating the Net Present Value (NPV) and proving the implicit interest rate within the lease agreement. The report offers detailed calculations, journal entries, and explanations, covering key concepts in financial accounting like depreciation, asset valuation, and lease analysis. This report is a comprehensive analysis of financial accounting topics.

Advanced Financial

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

QUESTION 1...................................................................................................................................3

Calculation of depreciation expense and gain/loss on machinery..........................................3

QUESTION 2 ..................................................................................................................................4

Journal entries for passing effect on revaluation of asset and the subsequent depreciation of

the revalued net- amount method...........................................................................................4

QUESTION 3 ..................................................................................................................................6

a)Any goodwill acquired and if so then how much?.............................................................6

b) can Tamarama can revalue the goodwill upwards in subsequent periods.........................7

QUESTION 4 ..................................................................................................................................7

a) Determining the Net Present Value (NPV) of lease payment ...........................................7

b) Proving that rate of interest is implicit in the lease is 6 %.................................................8

CONCLUSION ...............................................................................................................................8

REFERENCES ...............................................................................................................................9

INTRODUCTION ..........................................................................................................................3

QUESTION 1...................................................................................................................................3

Calculation of depreciation expense and gain/loss on machinery..........................................3

QUESTION 2 ..................................................................................................................................4

Journal entries for passing effect on revaluation of asset and the subsequent depreciation of

the revalued net- amount method...........................................................................................4

QUESTION 3 ..................................................................................................................................6

a)Any goodwill acquired and if so then how much?.............................................................6

b) can Tamarama can revalue the goodwill upwards in subsequent periods.........................7

QUESTION 4 ..................................................................................................................................7

a) Determining the Net Present Value (NPV) of lease payment ...........................................7

b) Proving that rate of interest is implicit in the lease is 6 %.................................................8

CONCLUSION ...............................................................................................................................8

REFERENCES ...............................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is a branch of accounting which is concerned with keeping the

records of the financial transactions of a business entity in a systematic manner. It deals with

recording, processing, summarising and reporting of the financial transactions in the form of

financial statements. Financial accounting is carried out by organisations in accordance with the

accounting standards and other legal requirements (Introduction to Financial Accounting, 2019).

The present project report is about the calculation of depreciation by applying sum of digits

methods along with its journal entries. In other section, it will also cover the revaluation journal

entries for the asset. In the last, the study will present the net present value calculations regrading

the lease payments.

QUESTION 1

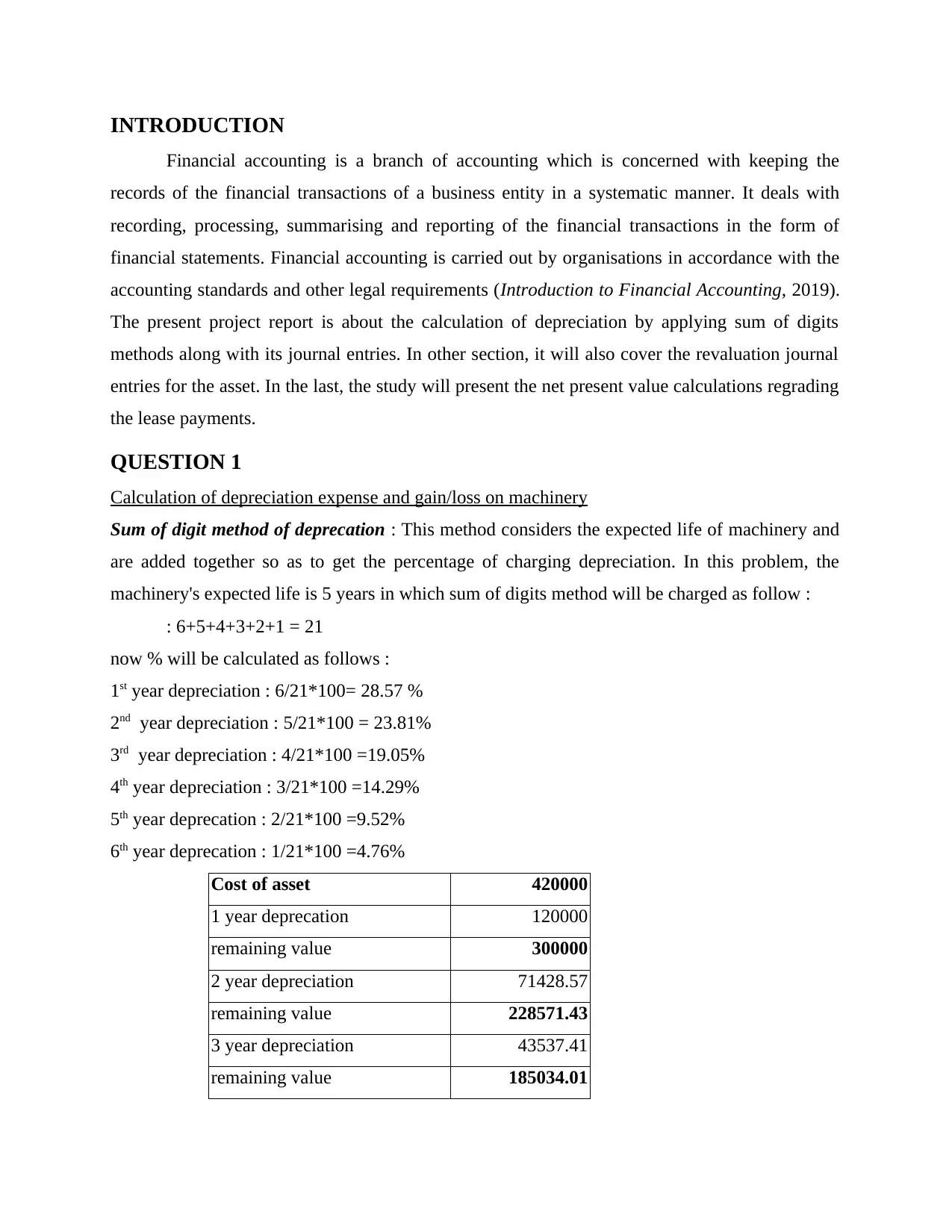

Calculation of depreciation expense and gain/loss on machinery

Sum of digit method of deprecation : This method considers the expected life of machinery and

are added together so as to get the percentage of charging depreciation. In this problem, the

machinery's expected life is 5 years in which sum of digits method will be charged as follow :

: 6+5+4+3+2+1 = 21

now % will be calculated as follows :

1st year depreciation : 6/21*100= 28.57 %

2nd year depreciation : 5/21*100 = 23.81%

3rd year depreciation : 4/21*100 =19.05%

4th year depreciation : 3/21*100 =14.29%

5th year deprecation : 2/21*100 =9.52%

6th year deprecation : 1/21*100 =4.76%

Cost of asset 420000

1 year deprecation 120000

remaining value 300000

2 year depreciation 71428.57

remaining value 228571.43

3 year depreciation 43537.41

remaining value 185034.01

Financial accounting is a branch of accounting which is concerned with keeping the

records of the financial transactions of a business entity in a systematic manner. It deals with

recording, processing, summarising and reporting of the financial transactions in the form of

financial statements. Financial accounting is carried out by organisations in accordance with the

accounting standards and other legal requirements (Introduction to Financial Accounting, 2019).

The present project report is about the calculation of depreciation by applying sum of digits

methods along with its journal entries. In other section, it will also cover the revaluation journal

entries for the asset. In the last, the study will present the net present value calculations regrading

the lease payments.

QUESTION 1

Calculation of depreciation expense and gain/loss on machinery

Sum of digit method of deprecation : This method considers the expected life of machinery and

are added together so as to get the percentage of charging depreciation. In this problem, the

machinery's expected life is 5 years in which sum of digits method will be charged as follow :

: 6+5+4+3+2+1 = 21

now % will be calculated as follows :

1st year depreciation : 6/21*100= 28.57 %

2nd year depreciation : 5/21*100 = 23.81%

3rd year depreciation : 4/21*100 =19.05%

4th year depreciation : 3/21*100 =14.29%

5th year deprecation : 2/21*100 =9.52%

6th year deprecation : 1/21*100 =4.76%

Cost of asset 420000

1 year deprecation 120000

remaining value 300000

2 year depreciation 71428.57

remaining value 228571.43

3 year depreciation 43537.41

remaining value 185034.01

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

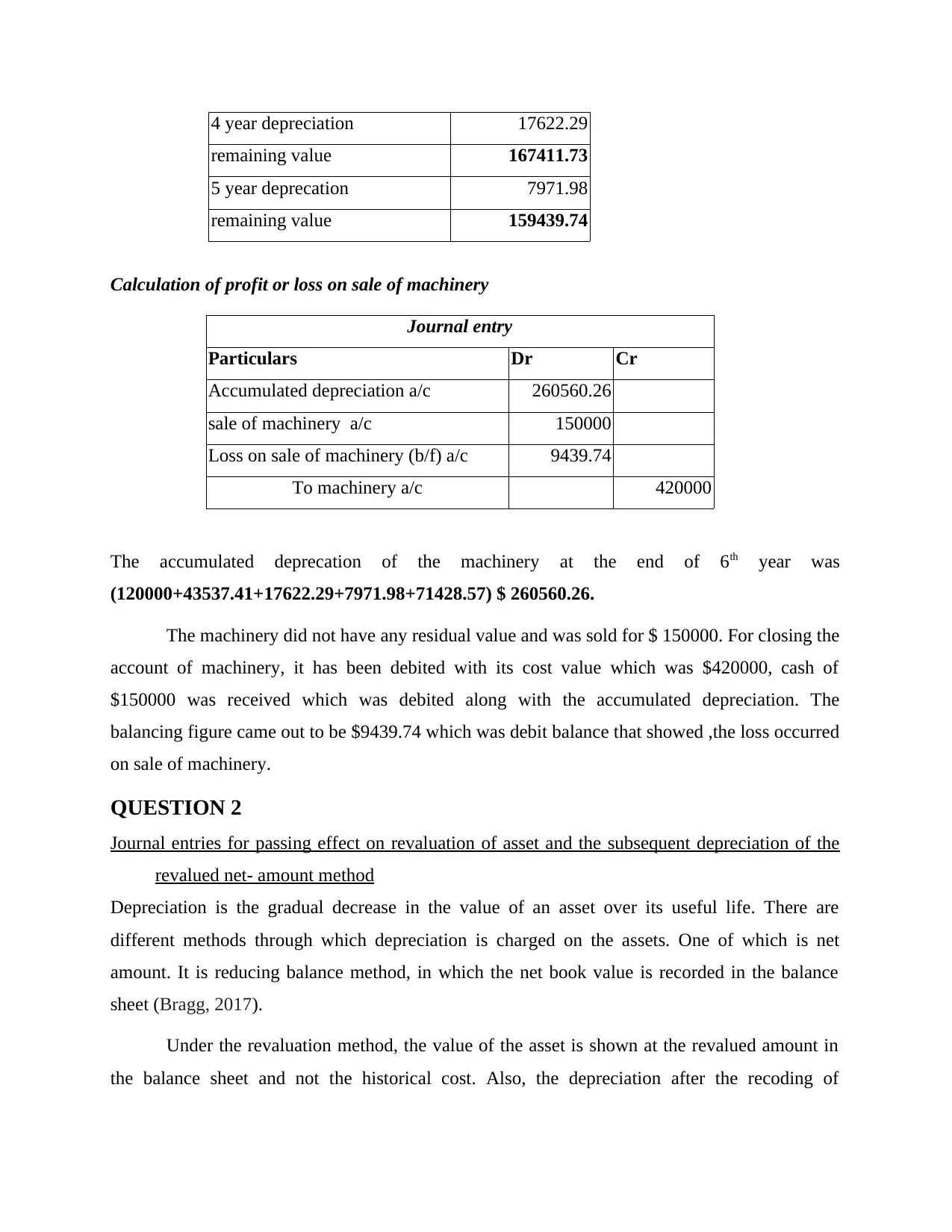

4 year depreciation 17622.29

remaining value 167411.73

5 year deprecation 7971.98

remaining value 159439.74

Calculation of profit or loss on sale of machinery

Journal entry

Particulars Dr Cr

Accumulated depreciation a/c 260560.26

sale of machinery a/c 150000

Loss on sale of machinery (b/f) a/c 9439.74

To machinery a/c 420000

The accumulated deprecation of the machinery at the end of 6th year was

(120000+43537.41+17622.29+7971.98+71428.57) $ 260560.26.

The machinery did not have any residual value and was sold for $ 150000. For closing the

account of machinery, it has been debited with its cost value which was $420000, cash of

$150000 was received which was debited along with the accumulated depreciation. The

balancing figure came out to be $9439.74 which was debit balance that showed ,the loss occurred

on sale of machinery.

QUESTION 2

Journal entries for passing effect on revaluation of asset and the subsequent depreciation of the

revalued net- amount method

Depreciation is the gradual decrease in the value of an asset over its useful life. There are

different methods through which depreciation is charged on the assets. One of which is net

amount. It is reducing balance method, in which the net book value is recorded in the balance

sheet (Bragg, 2017).

Under the revaluation method, the value of the asset is shown at the revalued amount in

the balance sheet and not the historical cost. Also, the depreciation after the recoding of

remaining value 167411.73

5 year deprecation 7971.98

remaining value 159439.74

Calculation of profit or loss on sale of machinery

Journal entry

Particulars Dr Cr

Accumulated depreciation a/c 260560.26

sale of machinery a/c 150000

Loss on sale of machinery (b/f) a/c 9439.74

To machinery a/c 420000

The accumulated deprecation of the machinery at the end of 6th year was

(120000+43537.41+17622.29+7971.98+71428.57) $ 260560.26.

The machinery did not have any residual value and was sold for $ 150000. For closing the

account of machinery, it has been debited with its cost value which was $420000, cash of

$150000 was received which was debited along with the accumulated depreciation. The

balancing figure came out to be $9439.74 which was debit balance that showed ,the loss occurred

on sale of machinery.

QUESTION 2

Journal entries for passing effect on revaluation of asset and the subsequent depreciation of the

revalued net- amount method

Depreciation is the gradual decrease in the value of an asset over its useful life. There are

different methods through which depreciation is charged on the assets. One of which is net

amount. It is reducing balance method, in which the net book value is recorded in the balance

sheet (Bragg, 2017).

Under the revaluation method, the value of the asset is shown at the revalued amount in

the balance sheet and not the historical cost. Also, the depreciation after the recoding of

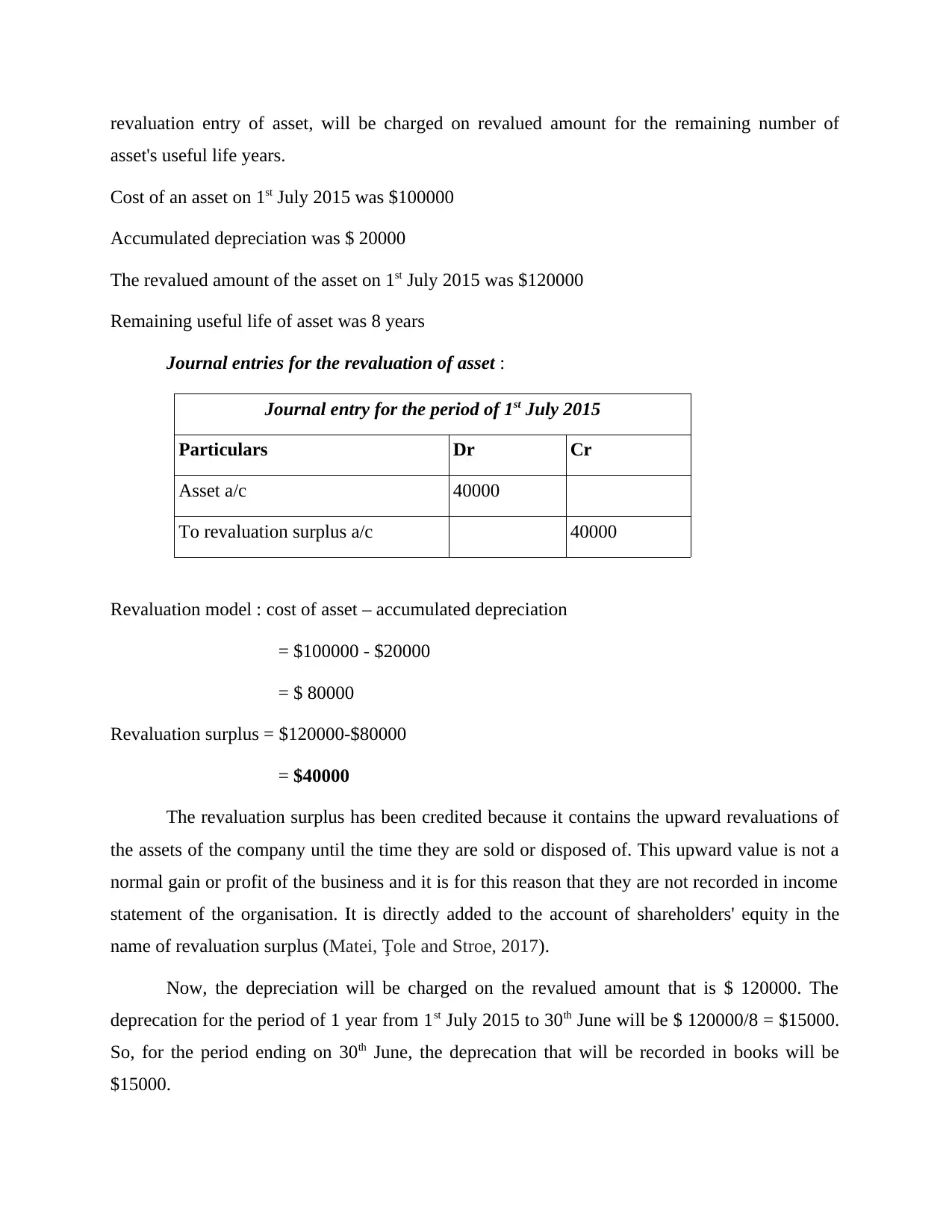

revaluation entry of asset, will be charged on revalued amount for the remaining number of

asset's useful life years.

Cost of an asset on 1st July 2015 was $100000

Accumulated depreciation was $ 20000

The revalued amount of the asset on 1st July 2015 was $120000

Remaining useful life of asset was 8 years

Journal entries for the revaluation of asset :

Journal entry for the period of 1st July 2015

Particulars Dr Cr

Asset a/c 40000

To revaluation surplus a/c 40000

Revaluation model : cost of asset – accumulated depreciation

= $100000 - $20000

= $ 80000

Revaluation surplus = $120000-$80000

= $40000

The revaluation surplus has been credited because it contains the upward revaluations of

the assets of the company until the time they are sold or disposed of. This upward value is not a

normal gain or profit of the business and it is for this reason that they are not recorded in income

statement of the organisation. It is directly added to the account of shareholders' equity in the

name of revaluation surplus (Matei, Ţole and Stroe, 2017).

Now, the depreciation will be charged on the revalued amount that is $ 120000. The

deprecation for the period of 1 year from 1st July 2015 to 30th June will be $ 120000/8 = $15000.

So, for the period ending on 30th June, the deprecation that will be recorded in books will be

$15000.

asset's useful life years.

Cost of an asset on 1st July 2015 was $100000

Accumulated depreciation was $ 20000

The revalued amount of the asset on 1st July 2015 was $120000

Remaining useful life of asset was 8 years

Journal entries for the revaluation of asset :

Journal entry for the period of 1st July 2015

Particulars Dr Cr

Asset a/c 40000

To revaluation surplus a/c 40000

Revaluation model : cost of asset – accumulated depreciation

= $100000 - $20000

= $ 80000

Revaluation surplus = $120000-$80000

= $40000

The revaluation surplus has been credited because it contains the upward revaluations of

the assets of the company until the time they are sold or disposed of. This upward value is not a

normal gain or profit of the business and it is for this reason that they are not recorded in income

statement of the organisation. It is directly added to the account of shareholders' equity in the

name of revaluation surplus (Matei, Ţole and Stroe, 2017).

Now, the depreciation will be charged on the revalued amount that is $ 120000. The

deprecation for the period of 1 year from 1st July 2015 to 30th June will be $ 120000/8 = $15000.

So, for the period ending on 30th June, the deprecation that will be recorded in books will be

$15000.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

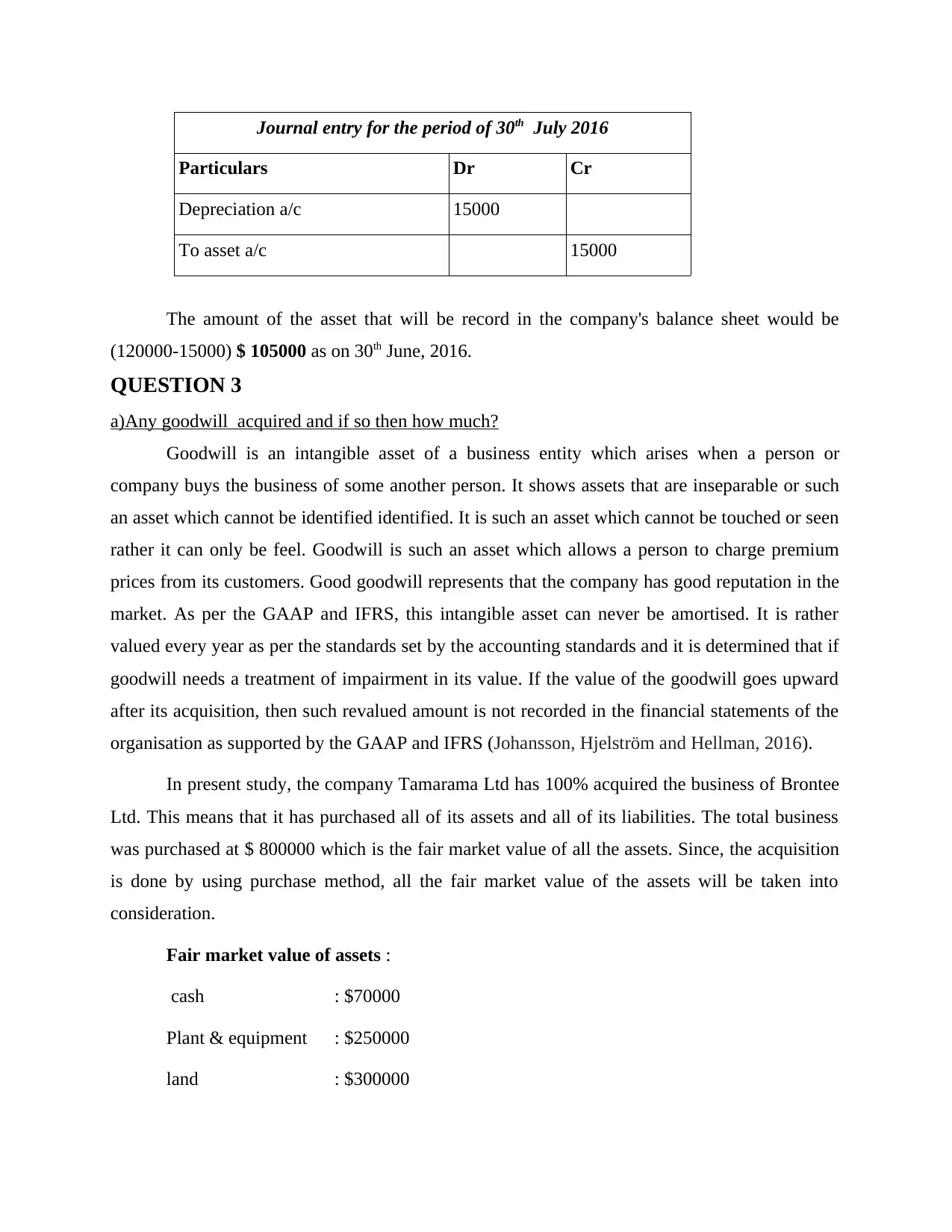

Journal entry for the period of 30th July 2016

Particulars Dr Cr

Depreciation a/c 15000

To asset a/c 15000

The amount of the asset that will be record in the company's balance sheet would be

(120000-15000) $ 105000 as on 30th June, 2016.

QUESTION 3

a)Any goodwill acquired and if so then how much?

Goodwill is an intangible asset of a business entity which arises when a person or

company buys the business of some another person. It shows assets that are inseparable or such

an asset which cannot be identified identified. It is such an asset which cannot be touched or seen

rather it can only be feel. Goodwill is such an asset which allows a person to charge premium

prices from its customers. Good goodwill represents that the company has good reputation in the

market. As per the GAAP and IFRS, this intangible asset can never be amortised. It is rather

valued every year as per the standards set by the accounting standards and it is determined that if

goodwill needs a treatment of impairment in its value. If the value of the goodwill goes upward

after its acquisition, then such revalued amount is not recorded in the financial statements of the

organisation as supported by the GAAP and IFRS (Johansson, Hjelström and Hellman, 2016).

In present study, the company Tamarama Ltd has 100% acquired the business of Brontee

Ltd. This means that it has purchased all of its assets and all of its liabilities. The total business

was purchased at $ 800000 which is the fair market value of all the assets. Since, the acquisition

is done by using purchase method, all the fair market value of the assets will be taken into

consideration.

Fair market value of assets :

cash : $70000

Plant & equipment : $250000

land : $300000

Particulars Dr Cr

Depreciation a/c 15000

To asset a/c 15000

The amount of the asset that will be record in the company's balance sheet would be

(120000-15000) $ 105000 as on 30th June, 2016.

QUESTION 3

a)Any goodwill acquired and if so then how much?

Goodwill is an intangible asset of a business entity which arises when a person or

company buys the business of some another person. It shows assets that are inseparable or such

an asset which cannot be identified identified. It is such an asset which cannot be touched or seen

rather it can only be feel. Goodwill is such an asset which allows a person to charge premium

prices from its customers. Good goodwill represents that the company has good reputation in the

market. As per the GAAP and IFRS, this intangible asset can never be amortised. It is rather

valued every year as per the standards set by the accounting standards and it is determined that if

goodwill needs a treatment of impairment in its value. If the value of the goodwill goes upward

after its acquisition, then such revalued amount is not recorded in the financial statements of the

organisation as supported by the GAAP and IFRS (Johansson, Hjelström and Hellman, 2016).

In present study, the company Tamarama Ltd has 100% acquired the business of Brontee

Ltd. This means that it has purchased all of its assets and all of its liabilities. The total business

was purchased at $ 800000 which is the fair market value of all the assets. Since, the acquisition

is done by using purchase method, all the fair market value of the assets will be taken into

consideration.

Fair market value of assets :

cash : $70000

Plant & equipment : $250000

land : $300000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

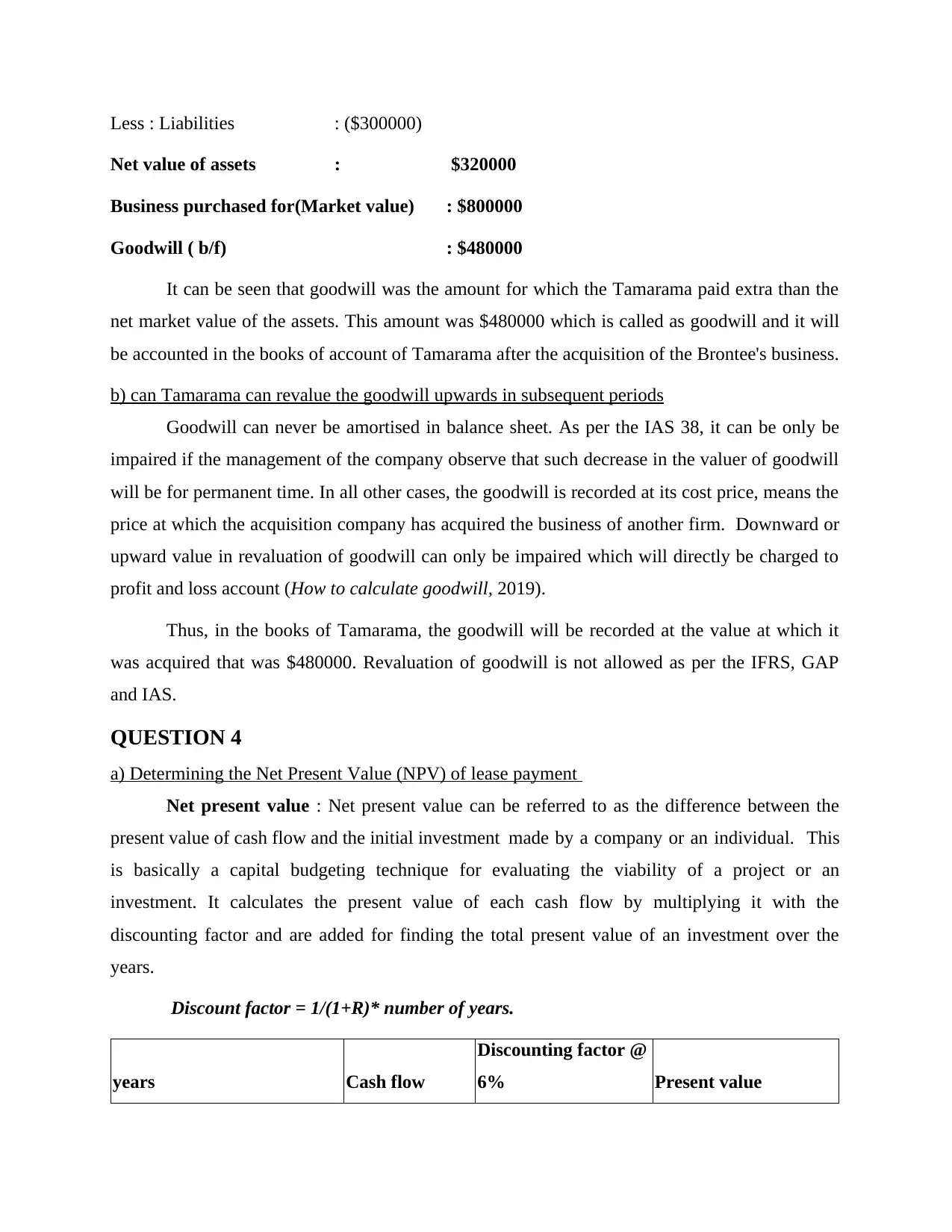

Less : Liabilities : ($300000)

Net value of assets : $320000

Business purchased for(Market value) : $800000

Goodwill ( b/f) : $480000

It can be seen that goodwill was the amount for which the Tamarama paid extra than the

net market value of the assets. This amount was $480000 which is called as goodwill and it will

be accounted in the books of account of Tamarama after the acquisition of the Brontee's business.

b) can Tamarama can revalue the goodwill upwards in subsequent periods

Goodwill can never be amortised in balance sheet. As per the IAS 38, it can be only be

impaired if the management of the company observe that such decrease in the valuer of goodwill

will be for permanent time. In all other cases, the goodwill is recorded at its cost price, means the

price at which the acquisition company has acquired the business of another firm. Downward or

upward value in revaluation of goodwill can only be impaired which will directly be charged to

profit and loss account (How to calculate goodwill, 2019).

Thus, in the books of Tamarama, the goodwill will be recorded at the value at which it

was acquired that was $480000. Revaluation of goodwill is not allowed as per the IFRS, GAP

and IAS.

QUESTION 4

a) Determining the Net Present Value (NPV) of lease payment

Net present value : Net present value can be referred to as the difference between the

present value of cash flow and the initial investment made by a company or an individual. This

is basically a capital budgeting technique for evaluating the viability of a project or an

investment. It calculates the present value of each cash flow by multiplying it with the

discounting factor and are added for finding the total present value of an investment over the

years.

Discount factor = 1/(1+R)* number of years.

years Cash flow

Discounting factor @

6% Present value

Net value of assets : $320000

Business purchased for(Market value) : $800000

Goodwill ( b/f) : $480000

It can be seen that goodwill was the amount for which the Tamarama paid extra than the

net market value of the assets. This amount was $480000 which is called as goodwill and it will

be accounted in the books of account of Tamarama after the acquisition of the Brontee's business.

b) can Tamarama can revalue the goodwill upwards in subsequent periods

Goodwill can never be amortised in balance sheet. As per the IAS 38, it can be only be

impaired if the management of the company observe that such decrease in the valuer of goodwill

will be for permanent time. In all other cases, the goodwill is recorded at its cost price, means the

price at which the acquisition company has acquired the business of another firm. Downward or

upward value in revaluation of goodwill can only be impaired which will directly be charged to

profit and loss account (How to calculate goodwill, 2019).

Thus, in the books of Tamarama, the goodwill will be recorded at the value at which it

was acquired that was $480000. Revaluation of goodwill is not allowed as per the IFRS, GAP

and IAS.

QUESTION 4

a) Determining the Net Present Value (NPV) of lease payment

Net present value : Net present value can be referred to as the difference between the

present value of cash flow and the initial investment made by a company or an individual. This

is basically a capital budgeting technique for evaluating the viability of a project or an

investment. It calculates the present value of each cash flow by multiplying it with the

discounting factor and are added for finding the total present value of an investment over the

years.

Discount factor = 1/(1+R)* number of years.

years Cash flow

Discounting factor @

6% Present value

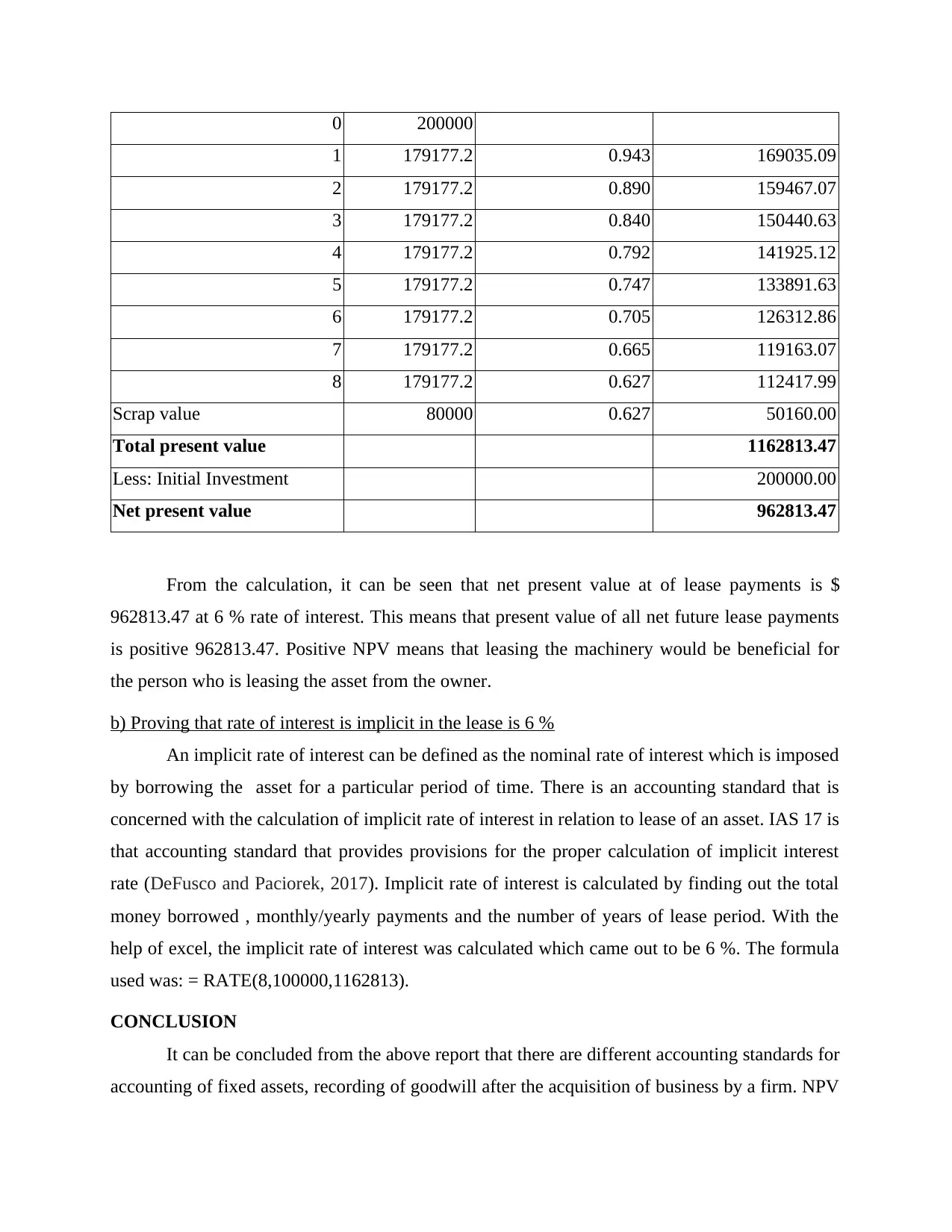

0 200000

1 179177.2 0.943 169035.09

2 179177.2 0.890 159467.07

3 179177.2 0.840 150440.63

4 179177.2 0.792 141925.12

5 179177.2 0.747 133891.63

6 179177.2 0.705 126312.86

7 179177.2 0.665 119163.07

8 179177.2 0.627 112417.99

Scrap value 80000 0.627 50160.00

Total present value 1162813.47

Less: Initial Investment 200000.00

Net present value 962813.47

From the calculation, it can be seen that net present value at of lease payments is $

962813.47 at 6 % rate of interest. This means that present value of all net future lease payments

is positive 962813.47. Positive NPV means that leasing the machinery would be beneficial for

the person who is leasing the asset from the owner.

b) Proving that rate of interest is implicit in the lease is 6 %

An implicit rate of interest can be defined as the nominal rate of interest which is imposed

by borrowing the asset for a particular period of time. There is an accounting standard that is

concerned with the calculation of implicit rate of interest in relation to lease of an asset. IAS 17 is

that accounting standard that provides provisions for the proper calculation of implicit interest

rate (DeFusco and Paciorek, 2017). Implicit rate of interest is calculated by finding out the total

money borrowed , monthly/yearly payments and the number of years of lease period. With the

help of excel, the implicit rate of interest was calculated which came out to be 6 %. The formula

used was: = RATE(8,100000,1162813).

CONCLUSION

It can be concluded from the above report that there are different accounting standards for

accounting of fixed assets, recording of goodwill after the acquisition of business by a firm. NPV

1 179177.2 0.943 169035.09

2 179177.2 0.890 159467.07

3 179177.2 0.840 150440.63

4 179177.2 0.792 141925.12

5 179177.2 0.747 133891.63

6 179177.2 0.705 126312.86

7 179177.2 0.665 119163.07

8 179177.2 0.627 112417.99

Scrap value 80000 0.627 50160.00

Total present value 1162813.47

Less: Initial Investment 200000.00

Net present value 962813.47

From the calculation, it can be seen that net present value at of lease payments is $

962813.47 at 6 % rate of interest. This means that present value of all net future lease payments

is positive 962813.47. Positive NPV means that leasing the machinery would be beneficial for

the person who is leasing the asset from the owner.

b) Proving that rate of interest is implicit in the lease is 6 %

An implicit rate of interest can be defined as the nominal rate of interest which is imposed

by borrowing the asset for a particular period of time. There is an accounting standard that is

concerned with the calculation of implicit rate of interest in relation to lease of an asset. IAS 17 is

that accounting standard that provides provisions for the proper calculation of implicit interest

rate (DeFusco and Paciorek, 2017). Implicit rate of interest is calculated by finding out the total

money borrowed , monthly/yearly payments and the number of years of lease period. With the

help of excel, the implicit rate of interest was calculated which came out to be 6 %. The formula

used was: = RATE(8,100000,1162813).

CONCLUSION

It can be concluded from the above report that there are different accounting standards for

accounting of fixed assets, recording of goodwill after the acquisition of business by a firm. NPV

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

in one of the question was calculated for evaluating viability of the lease of machinery. The NPV

came out to be positive which indicated that investment must be made in leasing the fixed asset.

came out to be positive which indicated that investment must be made in leasing the fixed asset.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.