Fall 2019 MGT2205: Financial Accounting Consolidation Assignment

VerifiedAdded on 2022/12/14

|10

|2024

|97

Homework Assignment

AI Summary

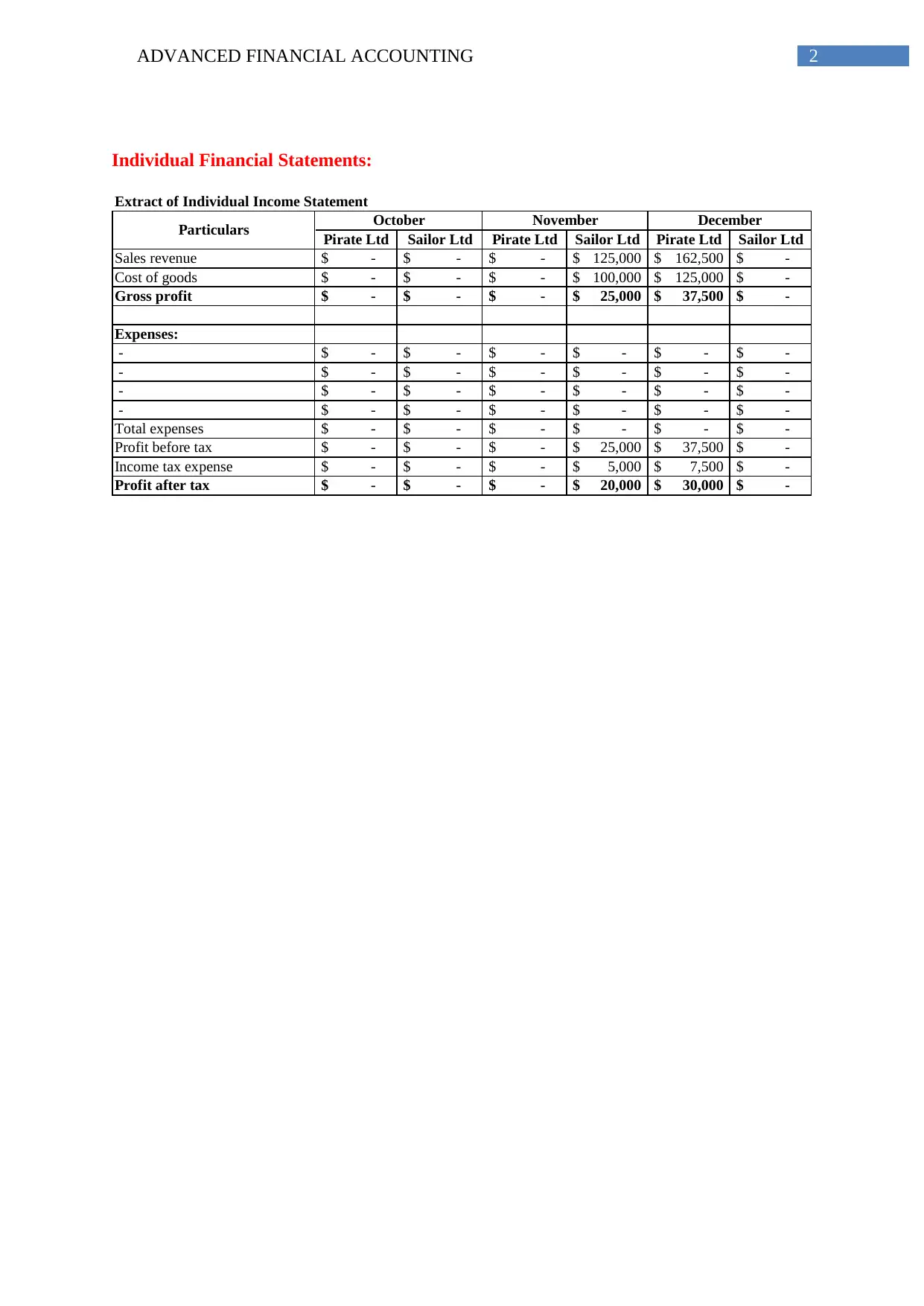

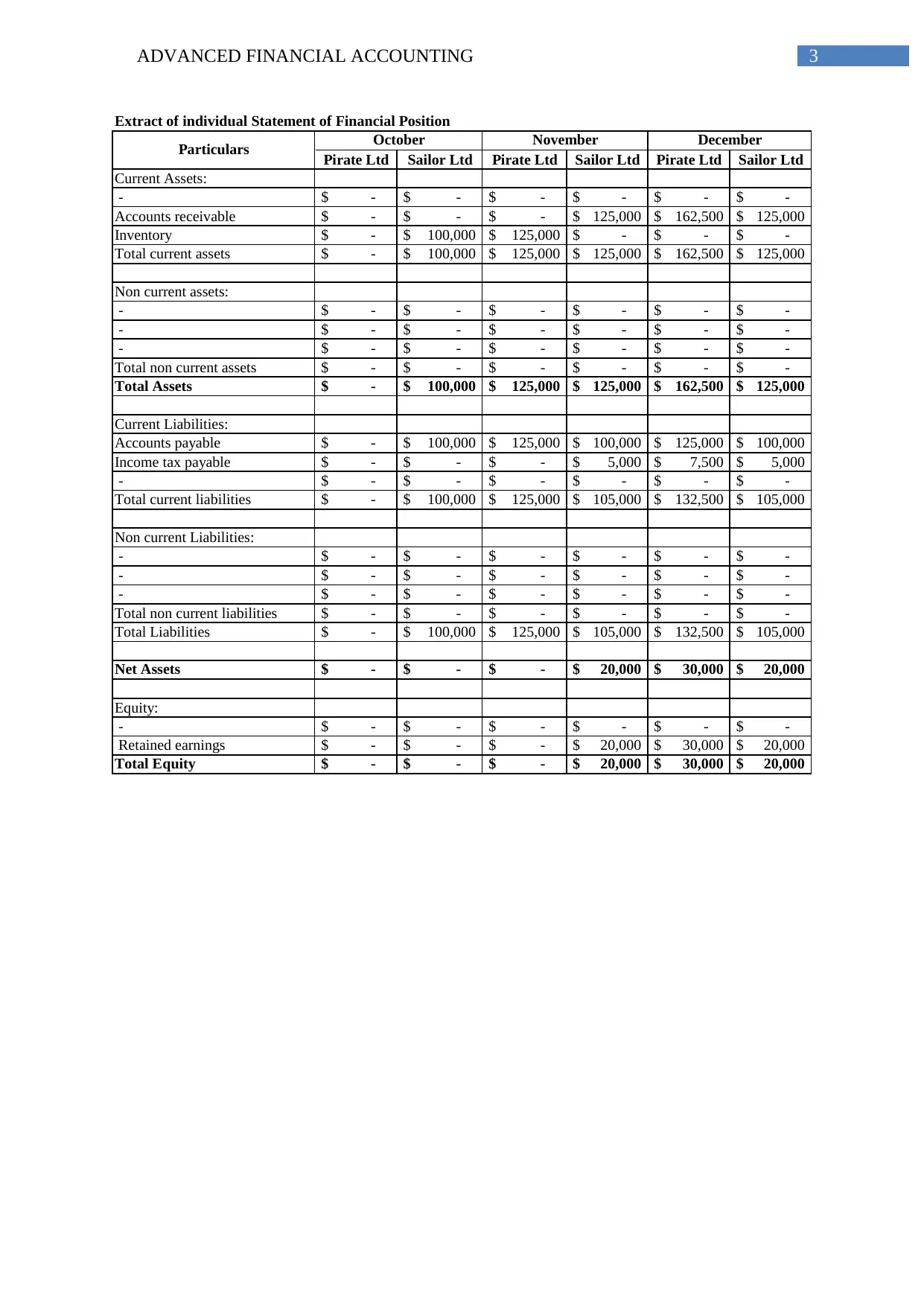

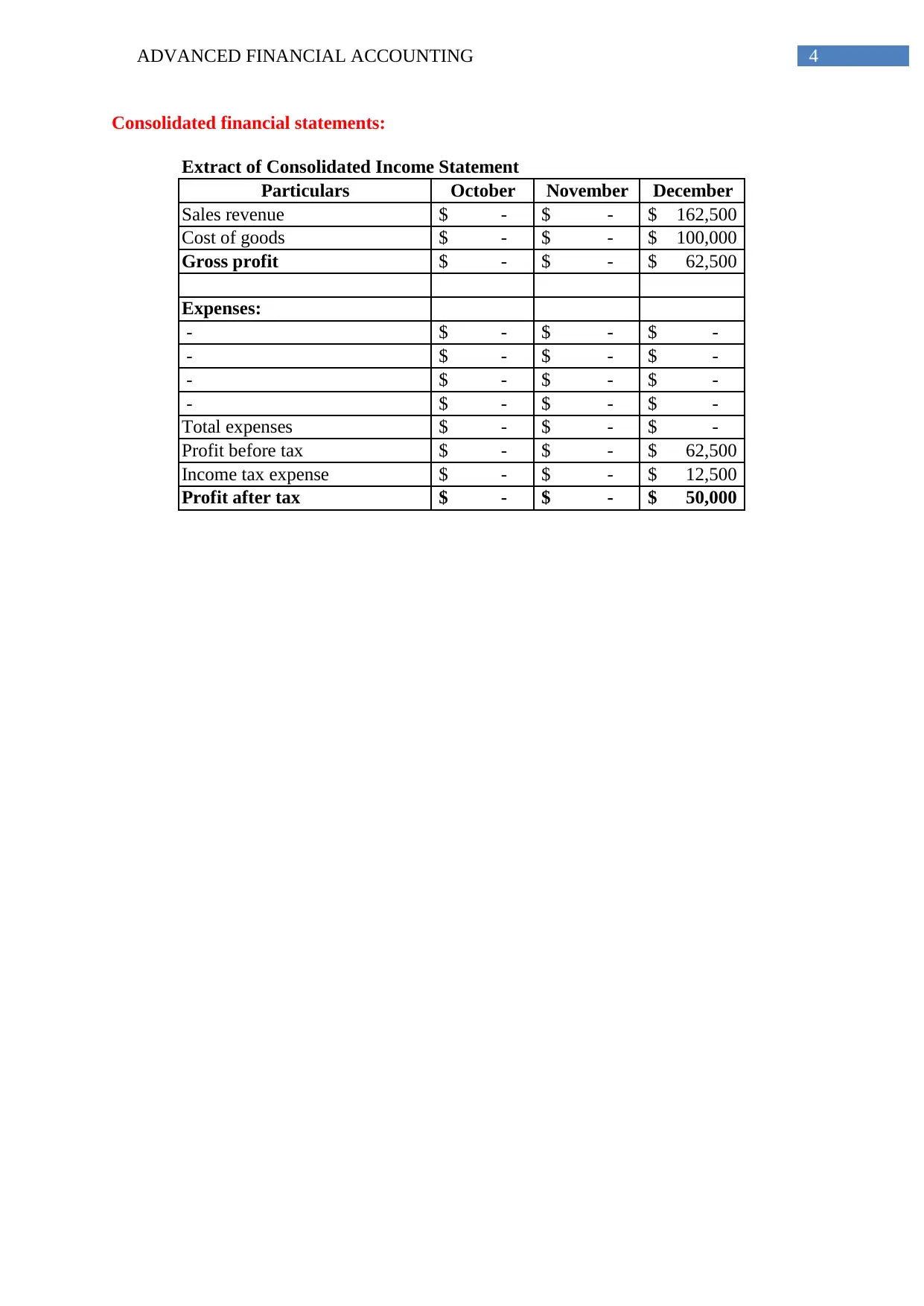

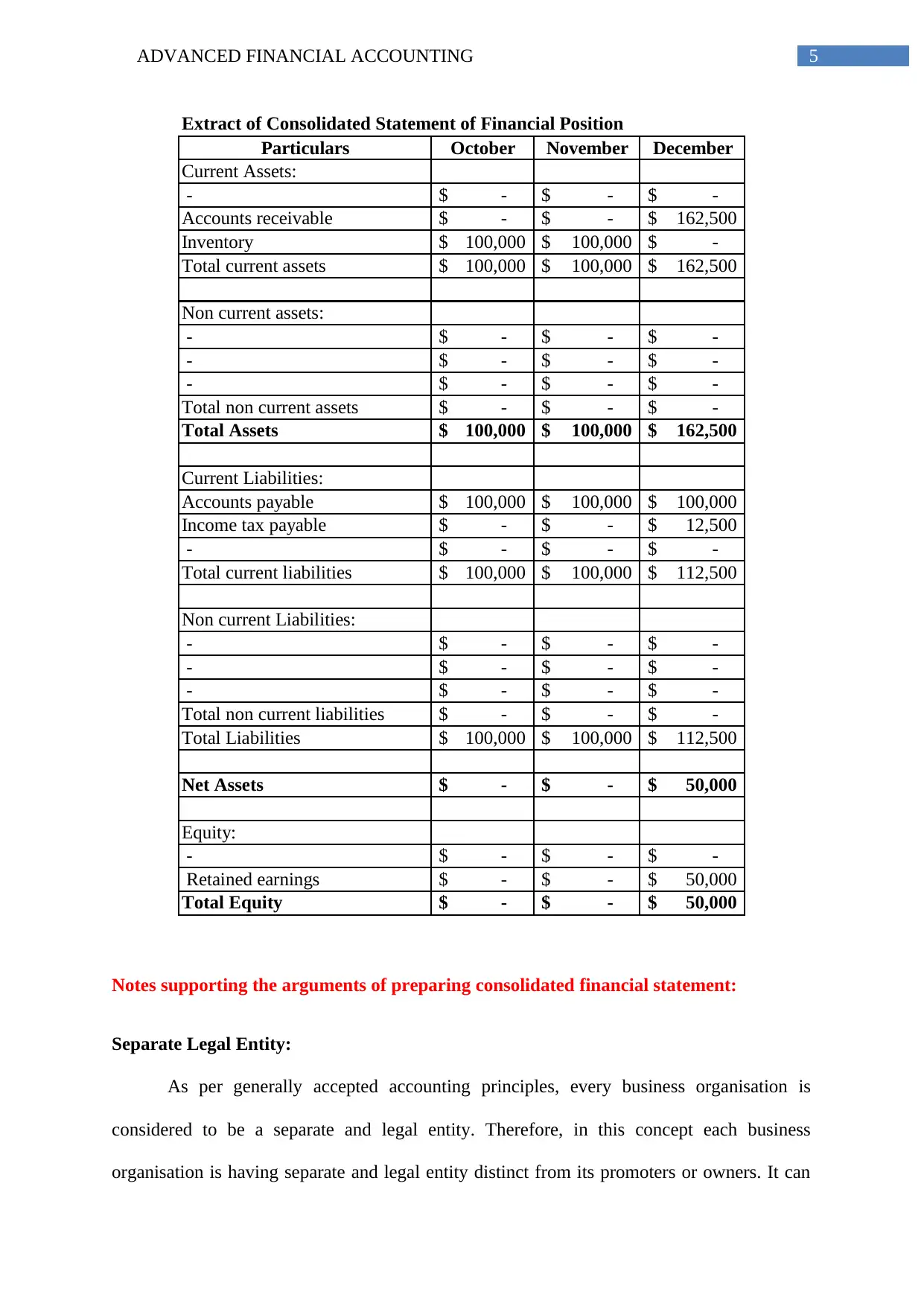

This assignment analyzes the financial statements of Pirate Ltd. and Sailor Ltd., focusing on consolidated financial statements. The solution includes individual and consolidated income statements and statements of financial position for October, November, and December, reflecting intercompany transactions. The assignment explains the concepts of separate legal entities versus one economic entity for consolidation, the holding-subsidiary relationship, and the importance of consolidated statements. Key accounting principles such as historical cost, revenue recognition, and the matching principle are discussed. The document also addresses why consolidated financial statements are crucial for assessing a company's financial performance and position, particularly for stakeholders like banks. The student demonstrates the correct application of these principles and their impact on financial reporting.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.