Holmes Institute, T3 2019: Advanced Financial Accounting Report

VerifiedAdded on 2023/01/18

|8

|2839

|73

Report

AI Summary

This report delves into advanced financial accounting principles, specifically examining the concept of a reporting entity and the qualitative characteristics of financial information. It defines a reporting entity as one where users rely on general-purpose financial reports (GPFR) for decision-making, illustrated with the example of Crown Resorts Limited. The report then explores the fundamental qualitative characteristics: relevance and representational faithfulness. Relevance is defined by its predictive and confirmatory value, while representational faithfulness emphasizes completeness, neutrality, and freedom from error. The analysis of Crown Resorts Limited's financial reports demonstrates these characteristics, highlighting how the company provides relevant and faithfully represented financial information. The report concludes that for financial statements to be useful to stakeholders, they must embody relevance and faithful representation, making the financial information significant for its users. The analysis considers that the financial statements of Crown Resorts Limited are prepared according to the Australian Accounting Standards, and the report includes analysis of how the company follows the accounting principles in its financial reporting.

Running Head: ADVANCED FINANCIAL ACCOUNTING

ADVANCED FINANCIAL ACCOUNTING

Name of the Student

Name of the University

Author Note

ADVANCED FINANCIAL ACCOUNTING

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Introduction...................................................................................................................2

Company’s Background............................................................................................2

Discussion.....................................................................................................................2

Reporting Entity.........................................................................................................2

Fundamental Qualitative Characteristics..................................................................3

Relevance..............................................................................................................4

Representational Faithfulness...............................................................................4

Conclusion....................................................................................................................5

Reference.....................................................................................................................6

Table of Contents

Introduction...................................................................................................................2

Company’s Background............................................................................................2

Discussion.....................................................................................................................2

Reporting Entity.........................................................................................................2

Fundamental Qualitative Characteristics..................................................................3

Relevance..............................................................................................................4

Representational Faithfulness...............................................................................4

Conclusion....................................................................................................................5

Reference.....................................................................................................................6

2ADVANCED FINANCIAL ACCOUNTING

Introduction

Financial accounting is the specialized branch of the accounting, which keeps

track of the financial transactions of entity. The accounting transactions are

summarized, recorded and presented with the help of using the standardized

guidelines in financial statements. Businesses employs various strategies for

increasing their market share. The firms make those strategic decisions that helps in

fostering longevity and growth of business. The involvement of company in

transactions of foreign currency sets stage for the international growth. All these

strategies affect financial reporting for business organization (Grossi and Steccolini

2015). Hence, this report aims to discuss about reporting entity. Further, discussion

will be on qualitative characteristics with respect to useful information of the financial

statement. All the discussion will be in reference to Crown Resorts Limited.

Company’s Background

Crown Resorts Limited

Crown Resorts Ltd. is largest Australian groups of entertainment. It manages

and operates entertainment as well as gaming facilities, restaurants, bars, retail

outlets, cinemas and nightclubs. It also develops conference centres facilities. This

company operates in the consumer discretionary sector. It derives revenue from the

investment and businesses in entertainment and gaming sector. The total

employment of people is approx. 18,000 and it operates in Australia, US, UK and it is

administered by its head office at Victoria. Cross Resorts Limited is listed on ASX

under code CWN (Crownresorts.com.au. 2020).

Discussion

Reporting Entity

Entity is defined as any administrative, legal or fiduciary arrangements,

structure organization or the other party that is having capacity for scarce resources

for achieving the objectives. Reporting entity is the entity in which it is reasonable for

expecting that some of the users are dependent on the GPFR for gaining

understanding of the financial performance and position of company and making

decisions based on the financial as well as other information. “General purpose

financial report” is defined as the financial report that is intended for meeting needs

of the information that is common to the users, who are basically not able for

commanding preparation of the tailored reports so as for satisfying all the needs of

the information (Carey, Potter and Tanewski 2014). These users can be creditors,

lenders, potential investors, employees and shareholders. There is no dependency

of “reporting entity” concept upon sector such as private or public, within which entity

operates, purposes based on which entity is created, profit or for not profit or the

manner in which company is established such as legal or other. Further, “reporting

entity” concept and identification of the boundaries of “reporting entity” are linked

with each other. For instance, if “reporting entity” concept adopted was based on the

class of legal entity then this implies identification of the boundaries of company by

legal considerations reference. This implies that only the companies of that particular

class of legal could be combined for forming “reporting entity” (Aasb.gov.au. 2020).

The “reporting entity” concept is linked with informational needs of users of

the GPFR in evaluating and making the decisions of resource allocations. The

informational provisions for these particular purposes are criteria used for

Introduction

Financial accounting is the specialized branch of the accounting, which keeps

track of the financial transactions of entity. The accounting transactions are

summarized, recorded and presented with the help of using the standardized

guidelines in financial statements. Businesses employs various strategies for

increasing their market share. The firms make those strategic decisions that helps in

fostering longevity and growth of business. The involvement of company in

transactions of foreign currency sets stage for the international growth. All these

strategies affect financial reporting for business organization (Grossi and Steccolini

2015). Hence, this report aims to discuss about reporting entity. Further, discussion

will be on qualitative characteristics with respect to useful information of the financial

statement. All the discussion will be in reference to Crown Resorts Limited.

Company’s Background

Crown Resorts Limited

Crown Resorts Ltd. is largest Australian groups of entertainment. It manages

and operates entertainment as well as gaming facilities, restaurants, bars, retail

outlets, cinemas and nightclubs. It also develops conference centres facilities. This

company operates in the consumer discretionary sector. It derives revenue from the

investment and businesses in entertainment and gaming sector. The total

employment of people is approx. 18,000 and it operates in Australia, US, UK and it is

administered by its head office at Victoria. Cross Resorts Limited is listed on ASX

under code CWN (Crownresorts.com.au. 2020).

Discussion

Reporting Entity

Entity is defined as any administrative, legal or fiduciary arrangements,

structure organization or the other party that is having capacity for scarce resources

for achieving the objectives. Reporting entity is the entity in which it is reasonable for

expecting that some of the users are dependent on the GPFR for gaining

understanding of the financial performance and position of company and making

decisions based on the financial as well as other information. “General purpose

financial report” is defined as the financial report that is intended for meeting needs

of the information that is common to the users, who are basically not able for

commanding preparation of the tailored reports so as for satisfying all the needs of

the information (Carey, Potter and Tanewski 2014). These users can be creditors,

lenders, potential investors, employees and shareholders. There is no dependency

of “reporting entity” concept upon sector such as private or public, within which entity

operates, purposes based on which entity is created, profit or for not profit or the

manner in which company is established such as legal or other. Further, “reporting

entity” concept and identification of the boundaries of “reporting entity” are linked

with each other. For instance, if “reporting entity” concept adopted was based on the

class of legal entity then this implies identification of the boundaries of company by

legal considerations reference. This implies that only the companies of that particular

class of legal could be combined for forming “reporting entity” (Aasb.gov.au. 2020).

The “reporting entity” concept is linked with informational needs of users of

the GPFR in evaluating and making the decisions of resource allocations. The

informational provisions for these particular purposes are criteria used for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ADVANCED FINANCIAL ACCOUNTING

determining boundaries of particular “reporting entity”. This is significant for those

who are charged up with the governance for documenting whether the entity has

users who are dependent upon GPFR for enabling them for defining entity as

reporting or non-reporting (Carini et al. 2018). The company is known to be

“reporting entity”, if it is preparing GPFR. In Australia, the accounting standards of

Australia are required to be applied in order to prepare financial report of listed

company. All the “reported entities” such as listed entities are required to prepare

financial report, as these reports are accessed by the external shareholders and

other users. There are various risks and benefits associated with each of the

reporting framework (Flower 2015). The greatest key risk is for addressing that

whether particular entity is reporting entity. In case, if definition of entity is incorrect

then ASIC will do the investigation of those charged up with the governance for

incorrect financial report preparation and hence breaching requirements of

“Australian Accounting Standards” and “Corporation Act 2001”. Further, some of

listed entities uses GPFR as the marketing document for promoting their activities

and demonstrating their social standing and responsibility with community (Carini et

al. 2017).

In case of Crown Resorts Limited, its financial report is GPFR that has been

prepared according to the “Australian Accounting Standards”, “Corporation Act 2001”

and the other authoritative pronouncements of AASB. It is the for profit entity that is

limited by the shares and whose shares are publically traded on “Australian Stock

Exchange” (Kulikova and Gafieva 2014). In amounts shown in financial report of

Crown Resorts Limited is shown in dollars and it is rounded off to the closest

hundred thousand. This company is the entity to which this particular instrument

applies (Crownresorts.com.au. 2020). For year ended June 30, 2019, Crown Resorts

Ltd. and its controlled companies was authorized to issue according to the resolution

of directors on September 11,2019 subject to subcommittee’s final approval.

Moreover, financial report of Crown Resorts Limited complies with accounting

standards of the Australia as issued by AASB and IFRS as issued by IASB. The

preparation of entity’s financial report is done according to costing technique of the

historical cost. This is apart from consideration of contingent, investment as well as

derivative financial instrument, as all these are measured according to fair value

(Crownresorts.com.au. 2020).

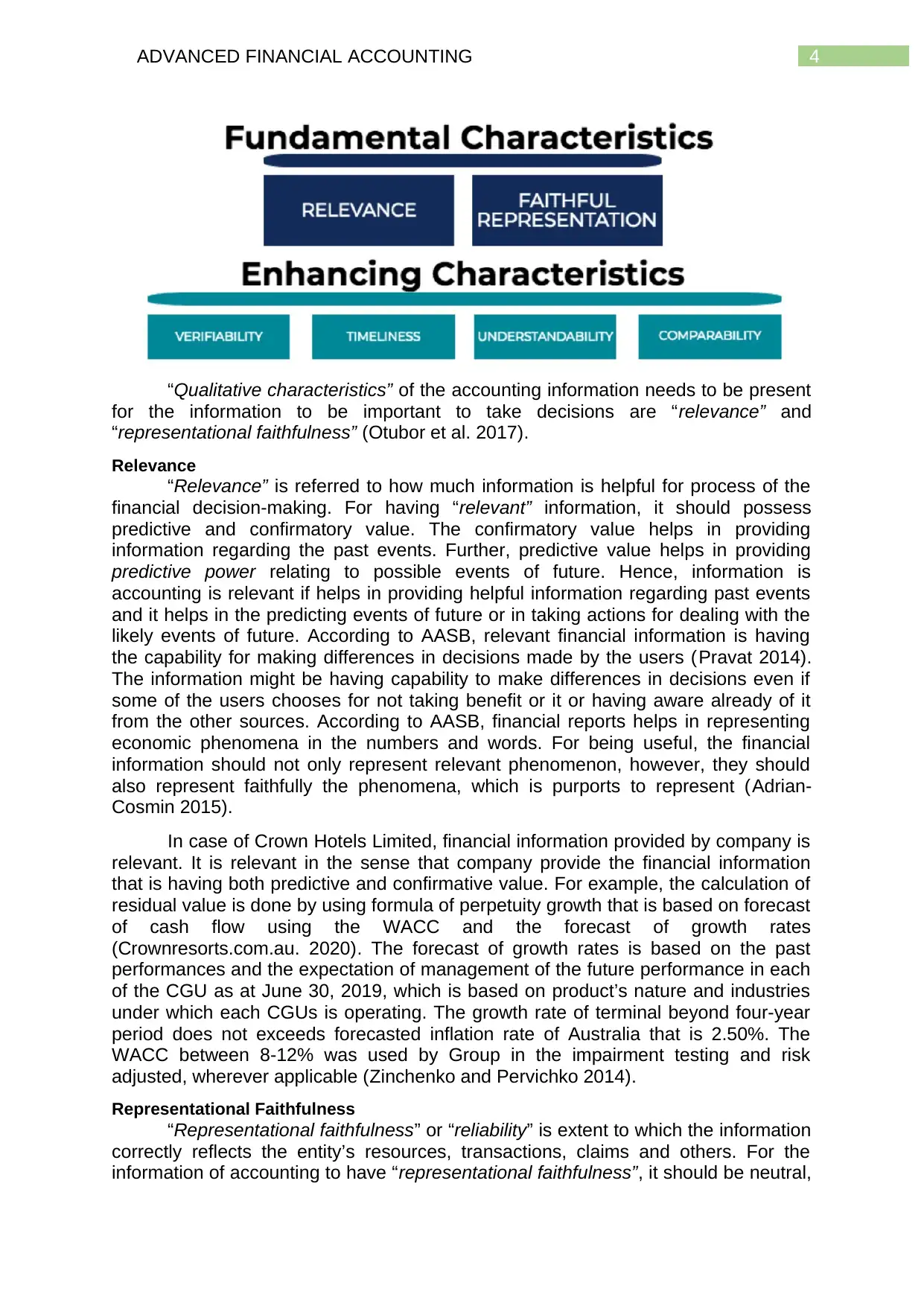

Fundamental Qualitative Characteristics

The call for the accounting information by users such as creditors, lenders,

investors and others create the “fundamental qualitative characteristics”, which are

required in the information of accounting. All organizations are required to provide

the financial information, which should possess “fundamental qualitative

characteristics”. The accounting information should be backed by 6 “fundamental

qualitative characteristics”. However, two of six “qualitative characteristics” are

considered to be fundamental, while remaining of the four “qualitative characteristics”

are considered as enhancing (Grigoras-Ichim and Morosan-Danila 2016).

determining boundaries of particular “reporting entity”. This is significant for those

who are charged up with the governance for documenting whether the entity has

users who are dependent upon GPFR for enabling them for defining entity as

reporting or non-reporting (Carini et al. 2018). The company is known to be

“reporting entity”, if it is preparing GPFR. In Australia, the accounting standards of

Australia are required to be applied in order to prepare financial report of listed

company. All the “reported entities” such as listed entities are required to prepare

financial report, as these reports are accessed by the external shareholders and

other users. There are various risks and benefits associated with each of the

reporting framework (Flower 2015). The greatest key risk is for addressing that

whether particular entity is reporting entity. In case, if definition of entity is incorrect

then ASIC will do the investigation of those charged up with the governance for

incorrect financial report preparation and hence breaching requirements of

“Australian Accounting Standards” and “Corporation Act 2001”. Further, some of

listed entities uses GPFR as the marketing document for promoting their activities

and demonstrating their social standing and responsibility with community (Carini et

al. 2017).

In case of Crown Resorts Limited, its financial report is GPFR that has been

prepared according to the “Australian Accounting Standards”, “Corporation Act 2001”

and the other authoritative pronouncements of AASB. It is the for profit entity that is

limited by the shares and whose shares are publically traded on “Australian Stock

Exchange” (Kulikova and Gafieva 2014). In amounts shown in financial report of

Crown Resorts Limited is shown in dollars and it is rounded off to the closest

hundred thousand. This company is the entity to which this particular instrument

applies (Crownresorts.com.au. 2020). For year ended June 30, 2019, Crown Resorts

Ltd. and its controlled companies was authorized to issue according to the resolution

of directors on September 11,2019 subject to subcommittee’s final approval.

Moreover, financial report of Crown Resorts Limited complies with accounting

standards of the Australia as issued by AASB and IFRS as issued by IASB. The

preparation of entity’s financial report is done according to costing technique of the

historical cost. This is apart from consideration of contingent, investment as well as

derivative financial instrument, as all these are measured according to fair value

(Crownresorts.com.au. 2020).

Fundamental Qualitative Characteristics

The call for the accounting information by users such as creditors, lenders,

investors and others create the “fundamental qualitative characteristics”, which are

required in the information of accounting. All organizations are required to provide

the financial information, which should possess “fundamental qualitative

characteristics”. The accounting information should be backed by 6 “fundamental

qualitative characteristics”. However, two of six “qualitative characteristics” are

considered to be fundamental, while remaining of the four “qualitative characteristics”

are considered as enhancing (Grigoras-Ichim and Morosan-Danila 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ADVANCED FINANCIAL ACCOUNTING

“Qualitative characteristics” of the accounting information needs to be present

for the information to be important to take decisions are “relevance” and

“representational faithfulness” (Otubor et al. 2017).

Relevance

“Relevance” is referred to how much information is helpful for process of the

financial decision-making. For having “relevant” information, it should possess

predictive and confirmatory value. The confirmatory value helps in providing

information regarding the past events. Further, predictive value helps in providing

predictive power relating to possible events of future. Hence, information is

accounting is relevant if helps in providing helpful information regarding past events

and it helps in the predicting events of future or in taking actions for dealing with the

likely events of future. According to AASB, relevant financial information is having

the capability for making differences in decisions made by the users (Pravat 2014).

The information might be having capability to make differences in decisions even if

some of the users chooses for not taking benefit or it or having aware already of it

from the other sources. According to AASB, financial reports helps in representing

economic phenomena in the numbers and words. For being useful, the financial

information should not only represent relevant phenomenon, however, they should

also represent faithfully the phenomena, which is purports to represent (Adrian-

Cosmin 2015).

In case of Crown Hotels Limited, financial information provided by company is

relevant. It is relevant in the sense that company provide the financial information

that is having both predictive and confirmative value. For example, the calculation of

residual value is done by using formula of perpetuity growth that is based on forecast

of cash flow using the WACC and the forecast of growth rates

(Crownresorts.com.au. 2020). The forecast of growth rates is based on the past

performances and the expectation of management of the future performance in each

of the CGU as at June 30, 2019, which is based on product’s nature and industries

under which each CGUs is operating. The growth rate of terminal beyond four-year

period does not exceeds forecasted inflation rate of Australia that is 2.50%. The

WACC between 8-12% was used by Group in the impairment testing and risk

adjusted, wherever applicable (Zinchenko and Pervichko 2014).

Representational Faithfulness

“Representational faithfulness” or “reliability” is extent to which the information

correctly reflects the entity’s resources, transactions, claims and others. For the

information of accounting to have “representational faithfulness”, it should be neutral,

“Qualitative characteristics” of the accounting information needs to be present

for the information to be important to take decisions are “relevance” and

“representational faithfulness” (Otubor et al. 2017).

Relevance

“Relevance” is referred to how much information is helpful for process of the

financial decision-making. For having “relevant” information, it should possess

predictive and confirmatory value. The confirmatory value helps in providing

information regarding the past events. Further, predictive value helps in providing

predictive power relating to possible events of future. Hence, information is

accounting is relevant if helps in providing helpful information regarding past events

and it helps in the predicting events of future or in taking actions for dealing with the

likely events of future. According to AASB, relevant financial information is having

the capability for making differences in decisions made by the users (Pravat 2014).

The information might be having capability to make differences in decisions even if

some of the users chooses for not taking benefit or it or having aware already of it

from the other sources. According to AASB, financial reports helps in representing

economic phenomena in the numbers and words. For being useful, the financial

information should not only represent relevant phenomenon, however, they should

also represent faithfully the phenomena, which is purports to represent (Adrian-

Cosmin 2015).

In case of Crown Hotels Limited, financial information provided by company is

relevant. It is relevant in the sense that company provide the financial information

that is having both predictive and confirmative value. For example, the calculation of

residual value is done by using formula of perpetuity growth that is based on forecast

of cash flow using the WACC and the forecast of growth rates

(Crownresorts.com.au. 2020). The forecast of growth rates is based on the past

performances and the expectation of management of the future performance in each

of the CGU as at June 30, 2019, which is based on product’s nature and industries

under which each CGUs is operating. The growth rate of terminal beyond four-year

period does not exceeds forecasted inflation rate of Australia that is 2.50%. The

WACC between 8-12% was used by Group in the impairment testing and risk

adjusted, wherever applicable (Zinchenko and Pervichko 2014).

Representational Faithfulness

“Representational faithfulness” or “reliability” is extent to which the information

correctly reflects the entity’s resources, transactions, claims and others. For the

information of accounting to have “representational faithfulness”, it should be neutral,

5ADVANCED FINANCIAL ACCOUNTING

free from error and complete. The accounting information is complete when financial

statements does not exclude any of transactions. The accounting information is

neutral that means degree to which the information is free from any kind of bias.

Further, there are estimation and subjectivity that is consists in the financial

statements. Hence, information cannot be neutral in true sense. Lastly, accounting

information is free from the error that means degree to which the information is free

from the errors (Aasb.gov.au. 2020).

In case of Crown Resorts Limited, the company reports its financial

information in words and numbers. The company is a profit entity. The consolidated

financial statements of the Crown Resorts Limited is consist of company itself and its

all subsidiaries of company. The company has eliminated in full all the inter-company

transactions and balances including the unrealized profits that arises from the intra-

group transactions. The adopted policies of accounting have been consistently

applied throughout two periods of reporting. The example of the representational

faithfulness is the fact that the carrying amounts of some liabilities and assets are

determined often based on the estimates, judgements and assumptions of the future

events (Al-dmour, Abbod and Al-dmour 2017). Further, the key judgements,

assumptions and estimates that is having significant risk to cause material

adjustment to the carrying amounts of certain liabilities and assets within next annual

reporting periods includes impairments of the non-financial assets, fair value of the

financial instruments, taxes, debts that are doubtful and the other significant items.

Moreover, whenever company adopts new accounting standard or whenever there is

revision of standards then company discloses and represents the changes in the

notes of financial statements for instance, the company discloses that upon adoption

of new accounting standard “AASB 16 Leases”, there will be increase in the interest

expenses and amount of depreciation, which will be partially offset by the increase in

EBITDA (Crownresorts.com.au. 2020). Moreover, the company has disclosed that

plant, property and equipment is specified at the cost less to accumulated

depreciation and any impairment in value. Calculation of amortization and

depreciation is based on the straight line over estimated asset’s useful lives

(Kythreotis 2014).

Conclusion

Therefore, this report concludes that the entity is required for making sure that

they are correctly described as reporting entity and for matching the framework of

financial reporting. It has been defined that reporting entity is the concept that is tied

to GPFR objectives and it is the concepts that requires all the organizations with the

dependent users on GPFR for the information for preparing these reports. It has

been analyzed that Crown Resorts Limited is the reporting entity. Moreover, this

report has analyzed that for financial statements to be significant to stakeholders of

company, they should embody certain qualitative characteristics that are “relevance

and faithful representation”. These “qualitative characteristics are qualities, which

make the financial information useful to users. Lastly, it has been analyzed that

Crown Resorts Limited is having the qualitative characteristics that makes their

financial information significant for their users.

free from error and complete. The accounting information is complete when financial

statements does not exclude any of transactions. The accounting information is

neutral that means degree to which the information is free from any kind of bias.

Further, there are estimation and subjectivity that is consists in the financial

statements. Hence, information cannot be neutral in true sense. Lastly, accounting

information is free from the error that means degree to which the information is free

from the errors (Aasb.gov.au. 2020).

In case of Crown Resorts Limited, the company reports its financial

information in words and numbers. The company is a profit entity. The consolidated

financial statements of the Crown Resorts Limited is consist of company itself and its

all subsidiaries of company. The company has eliminated in full all the inter-company

transactions and balances including the unrealized profits that arises from the intra-

group transactions. The adopted policies of accounting have been consistently

applied throughout two periods of reporting. The example of the representational

faithfulness is the fact that the carrying amounts of some liabilities and assets are

determined often based on the estimates, judgements and assumptions of the future

events (Al-dmour, Abbod and Al-dmour 2017). Further, the key judgements,

assumptions and estimates that is having significant risk to cause material

adjustment to the carrying amounts of certain liabilities and assets within next annual

reporting periods includes impairments of the non-financial assets, fair value of the

financial instruments, taxes, debts that are doubtful and the other significant items.

Moreover, whenever company adopts new accounting standard or whenever there is

revision of standards then company discloses and represents the changes in the

notes of financial statements for instance, the company discloses that upon adoption

of new accounting standard “AASB 16 Leases”, there will be increase in the interest

expenses and amount of depreciation, which will be partially offset by the increase in

EBITDA (Crownresorts.com.au. 2020). Moreover, the company has disclosed that

plant, property and equipment is specified at the cost less to accumulated

depreciation and any impairment in value. Calculation of amortization and

depreciation is based on the straight line over estimated asset’s useful lives

(Kythreotis 2014).

Conclusion

Therefore, this report concludes that the entity is required for making sure that

they are correctly described as reporting entity and for matching the framework of

financial reporting. It has been defined that reporting entity is the concept that is tied

to GPFR objectives and it is the concepts that requires all the organizations with the

dependent users on GPFR for the information for preparing these reports. It has

been analyzed that Crown Resorts Limited is the reporting entity. Moreover, this

report has analyzed that for financial statements to be significant to stakeholders of

company, they should embody certain qualitative characteristics that are “relevance

and faithful representation”. These “qualitative characteristics are qualities, which

make the financial information useful to users. Lastly, it has been analyzed that

Crown Resorts Limited is having the qualitative characteristics that makes their

financial information significant for their users.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ADVANCED FINANCIAL ACCOUNTING

Reference

Aasb.gov.au. 2020. [online] Available at:

https://www.aasb.gov.au/admin/file/content102/c3/SAC1_8-90_2001V.pdf [Accessed

25 Jan. 2020].

Aasb.gov.au. 2020. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/ACCED264_06-15.pdf [Accessed

25 Jan. 2020].

Adrian-Cosmin, C., 2015. ACCOUNTING INFORMATION SYSTEM-QUALITATIVE

CHARACTERISTICS AND THE IMPORTANCE OF ACCOUNTING INFORMATION

AT TRADE ENTITIES. Annals of'Constantin Brancusi'University of Targu-Jiu.

Economy Series, 2(1).

Al-dmour, A., Abbod, M.F. and Al-dmour, H.H., 2017. Qualitative Characteristics of

financial reporting and non-financial business performance. International Journal of

Corporate Finance and Accounting (IJCFA), 4(2), pp.1-22.

Carey, P., Potter, B. and Tanewski, G., 2014. Application of the Reporting Entity

Concept in A ustralia. Abacus, 50(4), pp.460-489.

Carini, C., Rocca, L., Teodori, C. and Veneziani, M., 2017. The Reporting Entity in

Private-Public Accounting Harmonisation. Is Control Enough for the Local

Government Consolidated Financial Statements?. Financial Reporting.

Carini, C., Rocca, L., Veneziani, M. and Teodori, C., 2018. The Reporting Entity

Concept in the Public Consolidated Financial Statement. International Journal of

Business and Social Science, 9(1), pp.1-21.

Crownresorts.com.au. 2020. [online] Available at:

https://www.crownresorts.com.au/CrownResorts/files/09/09b9547d-9e41-4d83-962f-

09c0efbe7757.pdf [Accessed 25 Jan. 2020].

Evans, M.E., Houston, R.W., Peters, M.F. and Pratt, J.H., 2015. Reporting regulatory

environments and earnings management: US and non-US firms using US GAAP or

IFRS. The Accounting Review, 90(5), pp.1969-1994.

Ewelt-Knauer, C., 2014. Determining reporting entity boundaries in the light of

neoinstitutional theories beyond the conceptual framework of IFRS. Journal of

Business Economics, 84(6), pp.827-864.

Flower, J., 2015. The international integrated reporting council: a story of

failure. Critical Perspectives on Accounting, 27, pp.1-17.

Grigoras-Ichim, C.E. and Morosan-Danila, L., 2016. Hierarchy of accounting

information qualitative characteristics in financial reporting. The USV Annals of

Economics and Public Administration, 16(1 (23)), pp.183-191.

Grossi, G. and Steccolini, I., 2015. Pursuing private or public accountability in the

public sector? Applying IPSASs to define the reporting entity in municipal

consolidation. International Journal of Public Administration, 38(4), pp.325-334.

Kulikova, L.I. and Gafieva, G.M., 2014. Development of financial reporting

principles. Mediterranean Journal of Social Sciences, 5(24), pp.38-38.

Reference

Aasb.gov.au. 2020. [online] Available at:

https://www.aasb.gov.au/admin/file/content102/c3/SAC1_8-90_2001V.pdf [Accessed

25 Jan. 2020].

Aasb.gov.au. 2020. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/ACCED264_06-15.pdf [Accessed

25 Jan. 2020].

Adrian-Cosmin, C., 2015. ACCOUNTING INFORMATION SYSTEM-QUALITATIVE

CHARACTERISTICS AND THE IMPORTANCE OF ACCOUNTING INFORMATION

AT TRADE ENTITIES. Annals of'Constantin Brancusi'University of Targu-Jiu.

Economy Series, 2(1).

Al-dmour, A., Abbod, M.F. and Al-dmour, H.H., 2017. Qualitative Characteristics of

financial reporting and non-financial business performance. International Journal of

Corporate Finance and Accounting (IJCFA), 4(2), pp.1-22.

Carey, P., Potter, B. and Tanewski, G., 2014. Application of the Reporting Entity

Concept in A ustralia. Abacus, 50(4), pp.460-489.

Carini, C., Rocca, L., Teodori, C. and Veneziani, M., 2017. The Reporting Entity in

Private-Public Accounting Harmonisation. Is Control Enough for the Local

Government Consolidated Financial Statements?. Financial Reporting.

Carini, C., Rocca, L., Veneziani, M. and Teodori, C., 2018. The Reporting Entity

Concept in the Public Consolidated Financial Statement. International Journal of

Business and Social Science, 9(1), pp.1-21.

Crownresorts.com.au. 2020. [online] Available at:

https://www.crownresorts.com.au/CrownResorts/files/09/09b9547d-9e41-4d83-962f-

09c0efbe7757.pdf [Accessed 25 Jan. 2020].

Evans, M.E., Houston, R.W., Peters, M.F. and Pratt, J.H., 2015. Reporting regulatory

environments and earnings management: US and non-US firms using US GAAP or

IFRS. The Accounting Review, 90(5), pp.1969-1994.

Ewelt-Knauer, C., 2014. Determining reporting entity boundaries in the light of

neoinstitutional theories beyond the conceptual framework of IFRS. Journal of

Business Economics, 84(6), pp.827-864.

Flower, J., 2015. The international integrated reporting council: a story of

failure. Critical Perspectives on Accounting, 27, pp.1-17.

Grigoras-Ichim, C.E. and Morosan-Danila, L., 2016. Hierarchy of accounting

information qualitative characteristics in financial reporting. The USV Annals of

Economics and Public Administration, 16(1 (23)), pp.183-191.

Grossi, G. and Steccolini, I., 2015. Pursuing private or public accountability in the

public sector? Applying IPSASs to define the reporting entity in municipal

consolidation. International Journal of Public Administration, 38(4), pp.325-334.

Kulikova, L.I. and Gafieva, G.M., 2014. Development of financial reporting

principles. Mediterranean Journal of Social Sciences, 5(24), pp.38-38.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ADVANCED FINANCIAL ACCOUNTING

Kythreotis, A., 2014. Measurement of financial reporting quality based on IFRS

conceptual framework’s fundamental qualitative characteristics. European Journal of

Accounting, Finance & Business, 2(3), pp.4-29.

Otubor, C.O., Gbande, R., Onumah, P., Yuguda, A.U. and Abubakar, S.I., 2017.

Assessing the Qualitative Characteristics of Useful Financial Information for

Business Development.

Pravat, I.C.B., 2014. Considerations on the treatment of qualitative characteristics of

accounting information at the international level and in various national accounting

systems. Studies and Scientific Researches. Economics Edition, (19).

Zinchenko, Y.P. and Pervichko, E.I., 2014. Qualitative Characteristics of Emotion

Regulation Process in Adolescents with Mitral Valve Prolapse. Procedia-Social and

Behavioral Sciences, 146, pp.76-82.

Kythreotis, A., 2014. Measurement of financial reporting quality based on IFRS

conceptual framework’s fundamental qualitative characteristics. European Journal of

Accounting, Finance & Business, 2(3), pp.4-29.

Otubor, C.O., Gbande, R., Onumah, P., Yuguda, A.U. and Abubakar, S.I., 2017.

Assessing the Qualitative Characteristics of Useful Financial Information for

Business Development.

Pravat, I.C.B., 2014. Considerations on the treatment of qualitative characteristics of

accounting information at the international level and in various national accounting

systems. Studies and Scientific Researches. Economics Edition, (19).

Zinchenko, Y.P. and Pervichko, E.I., 2014. Qualitative Characteristics of Emotion

Regulation Process in Adolescents with Mitral Valve Prolapse. Procedia-Social and

Behavioral Sciences, 146, pp.76-82.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.