Advanced Financial Accounting Report: RIO Tinto and AASB 16 Analysis

VerifiedAdded on 2022/10/19

|11

|2555

|206

Report

AI Summary

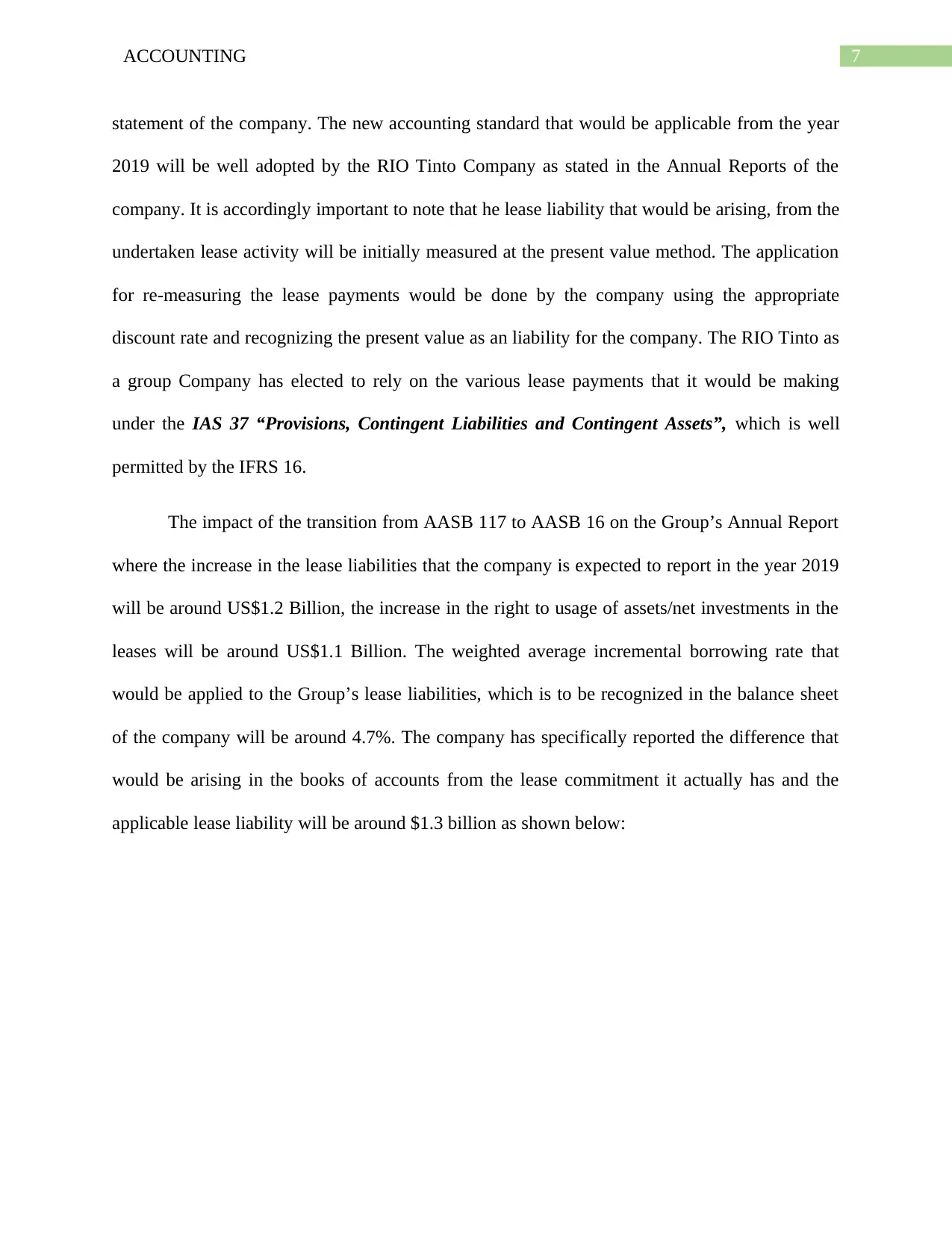

This report provides a detailed analysis of the RIO Tinto Company's annual report, focusing on the application of key accounting concepts and the adoption of the new AASB 16 standard for lease accounting. The report identifies and describes various accounting concepts such as revenue recognition, the economic entity concept, the matching concept, and materiality. It then delves into the specifics of AASB 16, explaining its implications for lease recognition, including the requirement for lessees to recognize assets and liabilities for leases exceeding 12 months. The report further examines the key disclosures made by RIO Tinto regarding its accounting for leases, including the transitional provisions and the financial impact of transitioning from AASB 117 to AASB 16. The analysis includes examples from the company's financial statements and footnotes, illustrating the practical application of these accounting principles and standards. The report also discusses the impact of the transition from AASB 117 to AASB 16 on the Group’s Annual Report where the increase in the lease liabilities that the company is expected to report in the year 2019 will be around US$1.2 Billion, the increase in the right to usage of assets/net investments in the leases will be around US$1.1 Billion. The weighted average incremental borrowing rate that would be applied to the Group’s lease liabilities, which is to be recognized in the balance sheet of the company will be around 4.7%. The company has specifically reported the difference that would be arising in the books of accounts from the lease commitment it actually has and the applicable lease liability will be around $1.3 billion. The report concludes by summarizing the key findings and implications of the analysis.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.